Currency

Quotable

“Life is a series of natural and spontaneous changes. Don’t resist them – that only creates sorrow. Let reality be reality. Let things flow naturally forward in whatever way they like.”

Lao Tzu

Commentary & Analysis

Inching closer to “Discredit Time” on monetary and fiscal policy failure…

(be sure to read Jack’s summary of Lacy Hunt’s work at the end of this article – MT Ed)

I am going to try to keep this simple, because it is too easy to make it all so damn complicated. First let’s state the premise of this missive:

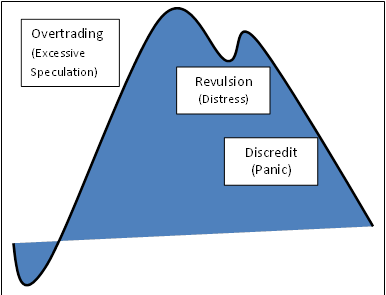

We are very close to what the great Charles Kindleberger referred to as “discredit.”

He identified three stages market movements:

We know these three stages by other names such as markup, distribution, and mark-down….But I think Professor Kindleberger’s term, especially “Discredit,” are much more apt in this cycle, as it better describes the mind-set at work that eventually leads to an unraveling of all that speculative excess those Wizards implementing monetary and fiscal policy have worked so hard to sustain.

As we know, those in the know are the ones that distribute to those not in the know. This is the “Revulsion” stage. This is why major bull markets tend to roll over gradually, given the ubiquitous “they,” time to unload. I think we are in the midst of that stage now, as the market “corrects.”

The next stage will be “Discredit.” This is the point at which even your soccer mom friends understand the policies of credit expansion heaped on us by the world’s largest governments and central banks were a complete disaster for the “average” person. This is panic selling time. This is recession/depression in key parts of the globe time. This is bankruptcy for individuals and institutions time. This is social unrest time. This is debt Jubilee time.

Why do I believe we will reach this stage? Because the numbers are telling us so; assuming we care to listen…

Before I give you the ugly details, let me digress just a bit, set the stage, and pat myself on the back for getting something right, I think.

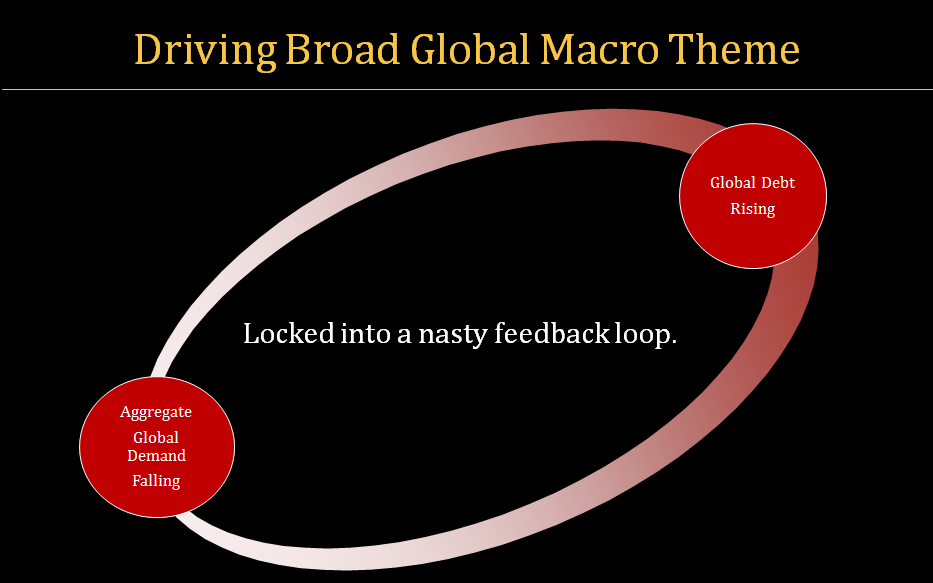

Just after the credit crunch, about six years ago, Black Swan created the chart you see below to help our readers better understand the powerful and negative feedback loop between debt and demand.

This nasty feedback of debt’s impact on aggregate demand was also part and parcel to our view deflationary pressures would continue to build in the global economy—reserves in the banking system didn’t matter as it isn’t inflationary in the standard sense of the word until those reserves lead to chasing real prices in the real economy higher. It hasn’t because of debt. But if we look at the stock market, I think it is fair to say there is a whole lot of inflation there thanks to the leakage of all these reserves, among other reasons.

We penned a special report back in September of 2009 on deflation. At the time we caught plenty of flak from the “there must be inflation” crowd (you can view the report by clicking here).

I remember Marc Faber was making the rounds when we penned out Deflation Rising report; he of course was telling everyone it was 100% guaranteed we would be witnessinghyperinflation because of quantitative easing. I noticed since the stock market corrected a bit, Mr. Faber is again seeking out microphones and cameras, as usual, to share his doom. So how did that short bond trade work out for you Marc?

And of course Jim Rogers was singing the praises of inflation which would no doubt lead to a never-ending bull market in commodities at the time; yup quantitative easy is sending us into the Weimar Republic land of runaway inflation good old Jim told us. Food was where it was at. How’s that long wheat trade working out for you Jim? Coincidently Jim has emerged from a summer hibernation to start pontificating again.

The point is not to slam these two guys for being wrong (though it’s fun to do). Both have been very right many times throughout their careers and have made a lot more money than I have. But I share to make a point they and many others missed: debt matters when it reaches a critical level. It is about money AND CREDIT…not just money.

Now some six-years after the credit crunch and what have our Best and Brightest in government and Central Banks wrought: an even greater level of debt in the global economy. I keep saying that if you made this stuff up no one would believe you.

Some of the guys I like did get it right early on when it comes to deflationary forces in the economy; they included Gary Schilling, Bob Prechter, and my favorite of all Lacy Hunt. These guys seem to do their thinking before they run in front of a microphone. I don’t have numbers to back this up, but I would bet Lacy Hunt has been more right on the bond market for more time than any other financial economist in history. The guy is plain brilliant in my humble opinion.

That said, why re-create the wheel. I have summarized some numbers from Lacy’s latest economic missive to show why monetary and fiscal policy has been an abject failure in this cycle and will lead to “discredit.”

- Real median household income stands at the same level it did seventeen years ago.

- Econometric studies have shown that a country’s growth rate will lose about 25% of its ‘normal experience growth’ when combined public and private debt reach 250%-275% of GDP. The US debt to GDP is about 334%.

- The US is in better shape than Europe or Japan; their debt levels are 460% and 655% to GDP, respectively. It helps explain why the US is growing faster than Europe and Japan, even though US growth is tepid at best and well below historical trends.

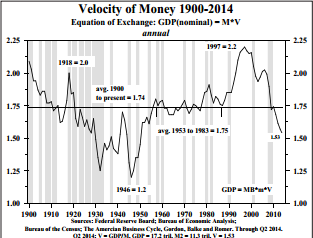

- Key point here: If the debt [created] is unproductive or counterproductive, meaning that a sustaining income stream is absent, or worse the debt subtracts from future income, then V [monetary velocity] will fall. If debt is productive and produces an income stream to repay principal, then V [monetary velocity} rises. [Auto and home loans are being pumped up again by lower credit standards—this is an example of unproductive debt.]

If we assume the equation: Nominal GDP = Monetary Base x Monetary Velocity; then we how can we expect growth to be strong when money supply numbers globally are flat at best and monetary velocity is crashing through the floor? [This is a global phenomenon, not just a US problem.]

If we assume the equation: Nominal GDP = Monetary Base x Monetary Velocity; then we how can we expect growth to be strong when money supply numbers globally are flat at best and monetary velocity is crashing through the floor? [This is a global phenomenon, not just a US problem.]

- From the Geneva Reports on the World Economy: Deleveraging? What deleveraging?:

“Contrary to widely held beliefs, the world has not yet begun to delever and the global debt-to-GDP is still growing, breaking new highs.” Further, it is a “poisonous combination” when world growth and inflation are lower than expected and debt is rising. “Deleveraging and slower nominal growth are in many cases interacting in a vicious loop, with the latter making the deleveraging process harder and the former exacerbating the economic slowdown.” […as per Black Swan’s graphic in the chart on page two.]

And for those of you who still believe emerging markets will help pull us out of this muck, Lacy writes:

This research [Geneva Reports] also identifies two other highly significant trends. First, global debt accumulation was led by developed economies until 2008. Second, the debt build-up since 2008 has been paced by the emerging economies. The authors write that the rise in Chinese debt is especially “stunning”. They describe China as “between a rock (rising and high debt) and a hard place (lower growth).” In addition to China they identify India, Turkey, Brazil, Chile, Argentina, Indonesia, Russia and South Africa as belonging to the “fragile eight” group of countries that could find themselves in the unwanted role of host to “the next leg of the global leverage crisis.”

- Increasing the flow of credit is extremely counterproductive when the fundamental problem is too much debt, and excessive debt can fuel asset bubbles.

- Even as the monetary base exploded from $1.7 trillion in 2009 to $4.1 trillion today, and stock prices have soared, the US economy has experienced the worst economic expansion on record.

- Rising relative yields and growth means more money will continue to flow to the United States.

As I read the news and various economic commentators, I get a feeling some have caught on, and many more are catching on, to the fact central bank and government fiscal policy has failed the real economy mightily. And now we are faced with the prospect of clearing that debt, at some point. Mr. Market being freed to clear away the dead wood of debt (malinvestment) is the “discredit” point Professor Kindleberger talks about in his appropriately named book: Manias, Panics, and Crashes.

I leave you with this tidbit taken from Murray Rothbard’s masterpiece, The Great Depression; the comments that follow are from our Deflation Rising report back in 2009:

To prolong a Depression…

1) Prevent or delay liquidation. Lend money to shaky businesses, call on banks to lend further, etc.

2) Inflate further. Further inflation blocks the necessary fall in prices, thus delaying the adjustment and prolonging the depression.

3) Keep wages up. Artificially maintenance of wage rates in a depression insures permanent mass unemployment.

4) Keep prices up. Keeping prices above their free-market levels will create unsalable surpluses, and prevent a return to prosperity.

}5) Stimulate consumption and discourage savings. We have seen the more saving and less consumption would speed recovery; more consumption and less saving aggravate the shortage of capital even further. As a matter of fact, any increase in taxes and government spending will discourage saving and investment and stimulate consumption, since government spending is all consumption. Some of the private funds [taxed away] would have been saved and invested; all of the government funds are consumed.

The real threat is government’s attempts at a solution is not only prolonging, and possibly dooming, subpar global growth for years to come, but it could be sowing the seeds of yet another crisis, or double-dip recession. This is especially dangerous when you consider central banks and global authorities are already running low on ammunition to counter the impact of deflationary pressures.

Nuff said!

Jack Crooks

President, Black Swan Capital

Twitter: @bswancap

HAI: The U.S. dollar has been rising and hit a four-year high earlier this month. Is the dollar going to continue to rally from here?

Marc Faber : The trade and current account deficit of the U.S. has been coming down because the balance in the energy trade has improved a lot. The U.S. is almost oil self-sufficient. It’s become the largest crude oil producer in the world.

And even though the U.S. economy is not doing particularly well, it’s in a slightly better position than the European economy. Thus, there are some reasons the dollar should be stronger.

That said, based on sentiment figures, everybody is now bullish on the U.S. dollar. Usually when you have this kind of consensus, what can happen is a powerful contra-move. In other words, the dollar could weaken for a while. That would be good for stocks and precious metals.

Additionally, if the Fed finds that the dollar is too strong, it can print money. But you just don’t know what these academics will eventually decide to do. That’s why I recommend investors have a diversified portfolio, because nobody knows what the world will look like five years from now.

…related:

Marc Faber : Gold Has Bottomed

….that would be good for Stocks & Precious Metals

Based on sentiment figures, everybody is now bullish on the U.S. dollar. Usually when you have this kind of consensus, what can happen is a powerful contra-move. In other words, the dollar could weaken for a while. That would be good for stocks and precious metals.

The trade and current account deficit of the U.S. has been coming down because the balance in the energy trade has improved a lot. The U.S. is almost oil self-sufficient. It’s become the largest crude oil producer in the world.

And even though the U.S. economy is not doing particularly well, it’s in a slightly better position than the European economy. Thus, there are some reasons the dollar should be stronger.

Additionally, if the Fed finds that the dollar is too strong, it can print money. But you just don’t know what these academics will eventually decide to do. That’s why I recommend investors have a diversified portfolio, because nobody knows what the world will look like five years from now.

US Dollar from its recent sharp peak Oct 3rd

…more from Marc Faber:

Real Estate , Equities , Bonds : the return on these Assets will be very disappointing

The US dollar has relentlessly blasted higher in recent months, achieving its longest consecutive-week rally in history. Speculators have flooded into the world’s reserve currency for a variety of reasons, ranging from Federal Reserve rate-hike hopes to festering Eurozone worries. But the resulting massive dollar surge has left it super-overbought while breeding universal bullishness, the precursors to a sharp selloff.

While only a small fraction of traders speculate in currencies, the foreign-exchange market is the largest in the world by far. Trillions of dollars change hands in currency trades every day, dwarfing all the other markets! And currency prices, particularly the fortunes of the dominant US dollar, can greatly affect everything else in the financial-market and economic realms. No one can afford to ignore the US dollar.

When the dollar is strong, the rest of the world’s currencies as well as popular commodities including oil and gold are forced lower. Higher dollar prices also retard US exports, making goods produced here more expensive for foreign customers. This cuts into corporate profits, which in turn adversely impacts stock prices. But a strong dollar also reduces import costs, giving Americans more purchasing power.

And of course the opposite is true when the US dollar weakens. Other currencies and commodities rise, US exports grow, and importing gets more expensive for consumers and corporations alike. The dollar’s impact is truly universal, so investors and speculators must pay attention to it. Particularly in times like today witnessing extraordinary moves, where the dollar’s influence on global markets waxes large.

The most popular way to track the US dollar’s price levels is through the venerable US Dollar Index. The USDX was born an impressive 41 years ago in March 1973, and measures the dollar against a basket of 6 leading world currencies. This flagship index is dominated by the euro, which accounts for 57.6% of its weight. This is followed by the Japanese yen and British pound sterling at 13.6% and 11.9%.

The US Dollar Index was initially set at 100.0 all those decades ago. And today stock traders can gain direct USDX exposure through the PowerShares DB US Dollar Index Bullish Fund USDX ETF which trades as UUP. And given the euro’s heavy weighting, the USDX is effectively the anti-euro. So stock traders can bet against the dollar with the leading CurrencyShares Euro Trust euro ETF which trades as FXE.

The mighty currency markets often slumber, and the USDX listlessly ground sideways for two-and-a-half years leading into mid-2014. But starting in early July, the US dollar began climbing. The initial catalyst was the European Central Bank, which currently holds policy meetings on the first Thursday of every month. On July 3rd, the ECB did nothing to combat the super-low inflation plaguing the Eurozone.

So the euro dropped, which naturally pushed up the US Dollar Index with its heavy euro weighting. And after that triggering event, the dollar buying persisted for various reasons. First the US stock markets started to top and then drop, leading to dollar safe-haven buying. Then upside momentum built on hopes the Fed would end its zero-interest-rate policy sooner rather than later, raising the dollar’s effective yield.

Generally the higher prevailing interest rates are, the more attractive a currency becomes in the eyes of foreign investors. This dynamic led the euro to plunge in early September after another ECB meeting where it surprised by slashing its main interest rate to effectively zero. So the zero-yielding euro was sold aggressively by futures traders while the zero-yielding-but-not-forever US dollar was snatched up.

With the US dollar soaring, euphoria started setting in which seduced in even more capital. Wall Street has long loved a strong dollar, led by perma-bulls like Larry Kudlow nearly worshipping it as “King Dollar”. They believe that a rising dollar attracts foreign investment into US financial markets, which is certainly true to an extent. This deeply-held bias left Wall Street eager to jump on to the strong-dollar bandwagon.

As a result, the US Dollar Index blasted 9.5% higher in the 4.9 months between early May and early October. While this was far from the dollar’s largest rally in history, it happened to be the first time the USDX has ever rallied for 12 consecutive weeks! If you look at a one-year dollar chart, the recent surge looks parabolic. This anomalous rally has wreaked havoc on commodities including oil and gold.

Since commodities are globally priced in dollar terms, the higher the dollar travels the fewer of them it takes to buy a base unit of commodities. So American futures speculators, particularly in the oil and gold markets, closely watch the USDX for trading cues. The great majority of the sharp recent weakness in oil and gold was the result of heavy futures selling by speculators in response to the dollar’s big gains.

But the mighty US dollar has moved up too far too fast, it is super-overbought. Such anomalously sharp rallies quickly ramp greed and euphoria, which soon burn themselves out. Exciting widely-watched jumps to major highs suck in all willing and available capital, pulling future buying forward. That leaves nothing but sellers, resulting in sharp corrections that usually completely unwind the preceding fast rallies.

This first chart reveals that critical dollar-trading symmetry, fast moves up are nearly always followed by fast moves down. And the recent sharp dollar surge looks big even in longer-term context. The USDX just catapulted up toa 51.8-month high, levels not seen since soon after 2008’s once-in-a-lifetime stock panic. Incidentally that crazy event sparked the biggest and fastest USDX rally ever witnessed, on safe-haven buying.

When stock markets start falling fast, like during that crazy stock panic, cash truly is king. Sellers rush to park capital in US dollars and short-term US Treasuries, leading to serious dollar spikes. In the second half of 2008 the USDX skyrocketed an astounding 22.6% higher in 4.2 months, its largest rally ever by far. The US dollar has a strong inverse correlation to the US stock markets, especially in times of turmoil.

But it’s critical to understand the strategic context. The mighty US dollar, despite Wall Street’s perpetual calls for a new bull, has been mired in a secular bear since July 2001 when the USDX crested at 120.9. As usual at major tops, bullishness was astounding. I was one of a very small handful of contrarian traders calling for a new dollar bear back in the summer of 2001when most believed the dollar would rally indefinitely.

Between that euphoric secular-bull peak and April 2008, the USDX had dropped a breathtaking 41.0% to an all-time low of 71.4! Strong dollar my foot, that notion is a total fallacy. The US dollar was very low and oversold heading into 2008’s bond panic closely followed by that notorious stock panic. There wasn’t exactly universal dollar bearishness then since Wall Street loves it, but there was great euro bullishness.

Major new lows coupled with negative sentiment creates the ideal cauldron for brewing major uplegs, so the bullish USDX setup heading into the stock panic couldn’t have been better. And that stock panic, the first one since 1907, sparked the greatest fear superstorm we’re likely to see in our lifetimes which led to extremely anomalous safe-haven US dollar buying. That’s why that USDX rally was its biggest ever.

Yet even in those perfect dollar conditions, that huge USDX rally collapsed near 88 which was still quite low in the context of the dollar’s secular bear. The catalyst was the US stock markets bottoming and bouncing sharply in November 2008, reversing the safe-haven capital flows back out of the US dollar. The USDX plunged dramatically after that, and didn’t reverse higher until the stock markets dropped lower again.

The USDX again soared in early 2009 as the stock markets weakened in dread of the horrendous new taxation and regulatory burdens the new Obama Administration was talking about saddling Americans with. Again the USDX peaked right when the US stock markets bottomed. And again the USDX started to plunge right after that sharp rally. In March 2009, it suffered its largest down day in history thanks to the Fed.

While the Fed’s first quantitative-easing campaign of creating new dollars out of thin air to monetize bonds had been underway for months, it was formally expanded at the FOMC’s March 2009 meeting. The USDX plummeted 2.9% that day! FOMC meetings and their subsequent minutes have long been major catalysts for sharp US dollar moves, so this week’s FOMC-minutes-driven dollar drop shouldn’t have surprised anyone.

The USDX again took off in early 2010, rocketing higher in the lower end of its secular-bear trading range. Once again the primary catalysts were sharp US-stock-market selloffs, along with growing fears of the Eurozone fracturing as profligate Greece received its first bailout. That led to heavy euro shorting by futures traders, boosting the US dollar since they are merely opposite sides of the same currency coin.

But again after that sharp and massive US dollar upleg peaked in mid-2010, the USDX didn’t stabilize but it fell sharply. That same phenomenon happened again at a smaller scale in both mid-2012 and mid-2013. The moral of the story is impressive USDX surges haven’t marked the births of new secular bulls as Wall Street perpetually hopes, but simply bear-market rallies with no fundamental foundation.

How can the dollar’s fundamentals ever improve until the Fed fully unwinds its quantitative-easing bonds bought, and fully normalizes interest rates? Why should foreign investors want to own a currency that a central bank is rapidly inflating while artificially forcing its yield to zero? It is hard to imagine this secular dollar bear ending before pre-2008 normalcy returns to the Fed’s balance sheet and interest rates.

In the first 8 months of 2008 before the stock panic, the Fed’s balance sheet averaged $875b. Today thanks to quantitative easing, it is a staggering $4408b. The Fed doesn’t just need to stop new bond buying, but to sell the mind-boggling $3.5t of bonds it monetized since late 2008! And in the quarter-century between the early-1980s rate spike and 2008’s stock panic, the benchmark federal-funds rate averaged 5.3%.

Fundamentals can’t support a new secular dollar bull with trillions of new dollars of supply and this currency trapped in the Fed’s zero-interest-rate-policy environment. Global demand just isn’t sufficient to absorb this deluge of inflation. And heading into the stock panic, central banks around the world were actively diversifying out of the US dollar thanks to its terrible performance for the better part of a decade.

Thus I strongly suspect that the recent sharp USDX rally that has generated such excitement will collapse just as fast and hard as the rest of the post-stock-panic QE-era US dollar rallies. And that has huge bullish implications for the battered euro and commodities, particularly gold. And this may have begun with this week’s FOMC minutes, as the euphoric USDX was already super-overbought heading into them.

Overboughtness arises when prices move too far too fast. One way to measure this is to look at a price relative to its 200-day moving average. Many years ago I developed a trading methodology based on this calledRelativity Trading. It divides a price by its 200dma, yielding a multiple that tends to form a horizontal trading range over time. And the USDX is super-overbought by this standard over recent years.

The USDX has generally traded between 0.93x its 200dma on the low side to 1.05x on the high side since the stock panic, support and resistance. While the epic stock-panic safe-haven rally and its echo in 2010 on stock-market selling pushed the USDX way above those relative multiples, those were extreme anomalies. Ever since 2011, the USDX has generally peaked once it gets around 5% above its 200dma.

Just last Friday, the USDX blasted 1.2% higher on that blowout upside surprise on the US’s September jobs report. Currency speculators figured that raised the odds the Fed would hike rates sooner rather than later, and higher yields should make the USDX more attractive. That pushed the USDX to 86.7, a 52-month high, and propelled the relative USDX multiple to 1.07x which was also the highest since mid-2010.

Major currencies usually move gradually, sharp moves are uncommon in these gargantuan markets since they have supertanker-like inertia. So to see the US Dollar Index a whopping 7% above its own 200dma in the absence of usual drivers like a sharp stock-market selloff was ominous. This currency had risen too far too fast, and Wall Street was getting euphoric on it as evidenced by many CNBC interviews.

There was major downside risk because any economic data or stock-market weakness that started to be perceived as staying the Fed’s hand on rate hikes could lead to fast selling of the crowded dollar long positions. Not to mention fast covering of the extreme euro and yen futures shorts, which would also hammer the dollar. And that’s what happened this week, the overbought dollar started collapsing fast.

When the minutes from the September FOMC meeting came out Wednesday and were uber-dovish, the USDX fell hard. The FOMC members were worried about slowing worldwide economic growth, and the strong dollar itself hurting US exports. Traders interpreted this as the FOMC being very reluctant to hike interest rates too soon. I had warned our Zeal Speculator subscribers about this the day before, writing…

“Much of the bullish psychology that is behind the dollar’s near-parabolic surge hinges on the belief the Fed will start hiking rates soon. What if that thesis starts to fade due to weaker economic data and weaker US stock markets? The downside risks to the euphoric dollar are just huge if anything looks to delay rate hikes at all. And futures speculators will rush to buy gold as the dollar rolls over.” And so it was.

The core message traders extracted from those FOMC minutes on rates waslower for longer. And the longer the Fed’s ZIRP policy stays in force, and the slower the pace of rate hikes to normalize interest rates afterwards, the longer the US dollar’s secular bear will persist. Against this backdrop, odds are the super-overbought US Dollar Index will plunge fast as the momentum traders on the bullish side quickly abandon it.

And a weaker dollar will directly boost the euro and other currencies, and also oil and gold. Gold in particular has exceptional upside potential as the US dollar retreats. Futures speculators used the strong dollar as an excuse to recently catapult their highly-leveraged short-side bets on gold to their third-highest levels of its secular bull if not ever. Their heavy shorting will be unwound fast as the dollar falls.

In addition the wildly-overextended and dangerously-overvalued US stock markets are long overdue to decisively roll over into a major selloff. As the stock markets weaken, the Fed will be far less likely to hike rates since higher rates really weigh on stock prices. That will ensure ZIRP lasts for longer than the dollar bulls anticipated, which will extend this currency’s longstanding Fed-driven secular bear market.

One of the hallmarks of our hardcore contrarian trading approach at Zeal is we constantly watch the global financial markets as a whole, and always consider their interrelationships. You can’t trade stocks or commodities successfully without watching the currency markets, which greatly affect them from time to time. So considering the US dollar’s most-likely near-term direction is essential for timing other trades.

You can reap the profitable fruits of our decades of market studies and trading through our acclaimed weekly and monthly newsletters. They draw on our hard-won experience, knowledge, wisdom, and ongoing research to explain what’s going on in the markets, why, and how to trade them with specific stocks. They will help you cultivate that rare contrarian perspective essential to thrive. Subscribe today!

The bottom line is the US dollar is super-overbought. Wall Street has always had a perpetually-bullish bias on the dollar, so mainstream traders were eager to pile on as it rallied sharply in recent months. A combination of ECB decisions hitting the euro, US stock-market selloffs, and hopes of the Fed starting to hike rates sooner rather than later catapulted the US Dollar Index up for a record 12 weeks in a row.

But such sharp dollar rallies to overbought levels, especially within the dollar’s secular bear when its supply-and-demand fundamentals remain very negative, soon crumble. The dollar falls as fast and far as it rose, reversing all the peripheral trades that suffered during the dollar’s rally. So sell the US dollar high when everyone loves it, and buy euros, yen, oil, and gold while they are still low before they rebound.

Adam Hamilton, CPA

October 10, 2014

Please consider joining us each month for tactical trading details and more in our premium Zeal Intelligence service at …www.zealllc.com/subscribe.htm

Copyright 2000 – 2014 Zeal LLC (www.ZealLLC.com)

FOMC’s fear of a strong dollar drives greenback lower

NEW YORK (MarketWatch) — The U.S. dollar turned lower against rivals Wednesday afternoon after the FOMC released minutes from its September meeting, revealing that members raised concerns that a one-two punch of a strong dollar and stagnant growth abroad could impede U.S. growth.

The closely followed central bank minutes also showed that several Fed officials wanted to remove language indicating that short-term interest rates would likely remain low “for a considerable time,” but held off in part because of concern that the market would misinterpret it as a policy shift.

Worries about tepid growth in Europe and Japan could relieve pressure on the Fed to raise rates sooner rather than later but already have been weighing on the greenback.

Really bad news for Europe and Japan

Check out the stock market’s volatility since the dollar has been rising. In normal times 200 point moves on the Dow are pretty notable. But they’ve happened in four of the past six sessions:

One explanation for this surge in volatility is that the dollar is spiking at a time when stocks are priced for perfection, producing Fear (that an appreciating currency will price US exports out of world markets and make domestic debts harder to manage) to contend with the Greed generated by a long bull market.

The Fed understands the risk posed by a surging dollar and is using it as an excuse to do what it wants to do in any event: continue to hold interest rates at artificially low levels and keep the helicopter money flowing.

US equity markets loved this reprieve, of course. But now the question becomes: If too-strong currencies helped to push Europe and Japan back into recession, and weaker currencies (versus the dollar) were those economies’ main hope for avoiding an ugly deflationary crash, then what does the Fed’s desire to keep a lid on the dollar mean? The answer isn’t pretty. If the dollar goes down from here that’s the same thing as saying the yen and euro go up. And if those currencies rise, Japan and Europe are toast.

So this story has just begun, and the next chapter is likely to involve some seriously desperate/experimental actions from the European Central Bank and Bank of Japan.

About John Rubino:

DollarCollapse.com is managed by John Rubino, co-author, with GoldMoney’s James Turk, of The Money Bubble (DollarCollapse Press, 2014) and The Collapse of the Dollar and How to Profit From It (Doubleday, 2007)

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair