Currency

Quotable

Quotable

“The minute you become emotionally attached to a stock [or any other asset class], you lose the rational ability to keep your losses small. You’ve become emotionally invested in the outcome. “

Michael Martin, The Inner Voice of Trading

Commentary & Analysis

Triffin’s Revenge Helping Mr. Greenback

I attended an investment conference about five years ago in a first-class resort on the beach in a southeastern state. The money spent on attendees and environment was impressive indeed (the newsletter firm clearly cared for, and did a great job in keeping, its customers). It was sponsored by a big-named newsletter house whose head guy was, and unfortunately still is, a very brash and cocky promoter—you would all know his name (fyi I never worked for him; I was a simply guest speaker who bombed with the crowd). I watched in awe at his ability to say anything he wanted to his audience of sycophantic newsletter subscribers, no matter how foolish; they just ate it up (crowd dynamics is a scary thing). They loved it in fact; even though I thought our brash hero was injecting a large dose of hyperbolic BS into his speech. This proves I know very little about how to properly market a newsletter.

I guess I remember this incident so well because of specifically one of the things this guy said when he launched into his expected dollar hate/doom segment: “The US dollar will be gone before my kids attend college.” He really meant gone. We would have a new monetary system and dollars would be history. Of course the dollar doom crowd in attendance (almost all), just loved it.

I kept thinking as I watched this show: 1) Either this guy doesn’t have kids; or 2) they will never be attending college; and 3) if the dollar just goes away as he said, this crowd had better be building bunkers and start sharpening their gold to use as weapons in preparation.

It was at that moment I finally realized, viscerally, many people want to be validated in their investment beliefs first and foremost. Performance and reality are secondary concerns. The two best asset classes defining this odd validation paradigm are gold and the US dollar. There seems a religious zeal to the belief gold has to go up and the dollar has to go down. It really is cult like. It is why these two asset classes are the ones the newsletter world loves to promote, i.e. create outlandish stories around, in order to get subscribers. But the newsletter world’s perennial bullishness on gold and bearishness on the dollar doesn’t seem to be working out too well, does it. But you just wait because once the ubiquitous “they” stop manipulating the gold price it will spike above $2,000; and once the New World order allows it, the dollar will be replaced by the Chinese yuan. You just wait and see. J

I share this seemingly widespread belief in coming dollar doom as a preface to this: A monetary system based around the US dollar has been messy and has led to major global imbalances–agreed. It is no substitute for the original gold standard and degree of discipline by central banks during that era (a bygone era when capital was far superior to labor and CBs cared about their currency values). But we are in a new era where all is possible through the issuance of credit, don’t you know (which was actually marked by the establishment of the Federal Reserve Bank back in 1913—credit for the US oligarchs to benefit mightily from the coming war). Despite all its warts, the dollar as reserve currency has served the world pretty well.

But what is most interesting, as many fret over the dollar’s future, given the lack of global cooperation now, the breakdown of the Washington Consensus and the potential for a complete reversal of globalization, the US dollar as the world reserve currency is actually becoming increasingly dominant and will likely be with us for many years to come—well past the time when my four beautiful grandchildren (more on the way I suspect) attend college. [Sorry, I couldn’t resist.]

Would John Maynard Keynes idea of a “bancor” been a better path to take for the global monetary system during the Bretton Woods agreement back in 1944? Most likely, yes. But President Roosevelt’s favorite local house commie—Harry Dexter White—who led the US delegation at the Bretton Woods hotel had is way with the Englishman and prevailed. Thus it set the stage for the dollar as a substitute for gold (which it was never designed given the US domestic “needs” and irresponsibility of the US government and cheating and reneging by the European governments who were supposed to revalue against the dollar to keep Bretton Woods viable). The breakdown of Bretton Woods of course led to a severing of the link between the dollar and gold thanks to President Richard Nixon in 1971; it ushered in what we have now—a float rate regime of fiat currency that is supposed to be driven by supply and demand factors.

This gets us to the Triffin’s Revenge part. I have shared this before, but will do again as understanding Triffin is important to understanding the US dollar a world reserve currency cuts both ways and has been no picnic for the US to maintain. This section actually comes from our updated Dollar Special Report from October 2013 linked here in case you missed it:

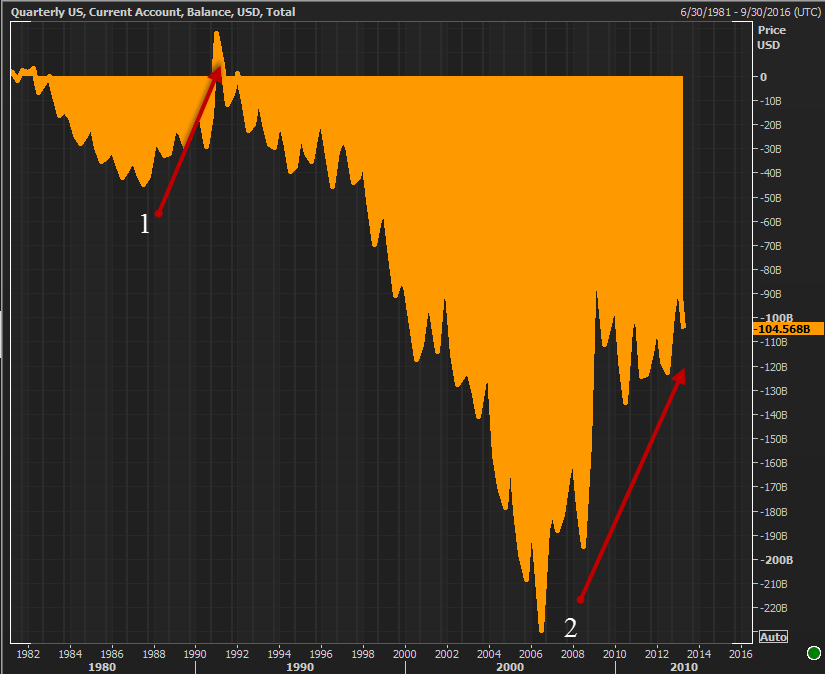

Triffin’s revenge – The US Current Account is improving

The US current account deficit is good depiction of the level of dollar credit going out into the world as it increases, and coming back to the center as it decreases. An improvement in the current account reflects the fact that fewer dollars a being spread across…keep in mind Triffin’s Dilemma which said US dollar replacing gold as reserve currency means the US is forced to run big current account deficits to provide liquidity to the global economy. Thus, reduced dollar supply from a falling current account deficit is taking place as the demand for dollar credit (hoarding dollars) is rising. And keep in mind, the flip side of a US current account improvement(chart below) is the same as a surplus country’s current account relative deterioration—this IS rebalancing.

[Also the dramatic improvement means US demand for goods is leaving the market. This is exerting huge pressure on China and other major exporters dependent on US consumption.]

When US dollars drains from the global system (evidenced by an improving current account deficit in the United States, i.e. money coming back to the center), especially following years of easy credit and bubble building, bad things happen to asset markets.

The improvement in the current account deficit in 1987 preceded:

a. The 1987 stock market crash & Asian Financial Crisis

b. The recession of 1990-91

The improvement in the current account deficit in the 2006 preceded:

c. The great credit crunch of 2007-08 & global conflagration

d. The recession of 2008-10

…helping to trigger the beginning of a multi-year bull market in the US dollar.

Also keep in mind that during the “free credit” era preceding the credit crunch from 2000-2007, the dollar was effectively the carry currency in what was known as the “risk on” trade. This effectively said growth opportunities abound internationally and commodities are in a massive bull market thanks to Chinese demand, so get out of dollar and own emerging markets and commodities investments. That trend came to an abrupt halt when the credit crunch hit. The game has changed.

In summary, as the US current account improves and as more and more foreign direct investment flows to the United States (net plus $6.8 trillion to the US since the credit crunch), dollar credit (added to the globe because of US current account deficits—the role of the reserve currency) is draining from the world. This is dollar bullish on supply alone, but it could turn into a stampede when you consider the growing demand:

- According to Leto Research there is about $15 trillion in dollar denominated debt in the global economy. If the Fed raises rates it creates a lot of pressure at the margin for those demanding dollars as their interest costs rise.

- The US foreign policy view of the world for the most part, at the beginning of President Obama’s administration, has completely broken down. This adds massive global risk and could lead to a major risk bid back into US Treasuries. Remember, to buy Treasuries you have to convert your currency to the dollar.

- The Russia game has changed (Hillary Clintons’ famous reset didn’t seem to work too well) and implications for US relations with Europe is growing increasingly tenuous (especially as it relates to Germany).

- The belief the “Arab Spring” would usher in a whole new generation of moderate Muslim leaders in the Middle East is yet a dream.

- The Eurozone economy continues to spiral lower and now there is concern Germany could be heading into recession.

- China’s leadership continues to consolidate power (during the reform process) and seems to become less tolerant domestically. The Hong Kong protest and troubles in Xinjiang and Tibet will likely lead to more domestic tightening. Plus, China has become decidedly more militaristic of late (this is not to suggest the US is innocent or all of China’s move as a superpower are not justified) and its tensions with its neighbors has grown.

- Japan’s economic rebound is in trouble of stalling and morphing into complete failure.

- US may stop caring, or start caring less, about its world reserve currency role as countries continue to attempt to grab US demand by building surpluses and not making real structural reforms locally. This is where Triffin’s Revenge kicks in big time, as maybe this so-called “exorbitant privilege” is more burden than privilege. This was a good summary from a recent blog post by Michael Pettis (he has been very good on this topic and is well out of the consensus):

- “I had pretty much taken the role of the dollar as a given, and assumed vaguely that its dominance gave the US some ill-defined but important advantage – after all they did call it the “exorbitant privilege”. But after a few years in China (I moved to Beijing in 2002) I became increasingly suspicious of the value of this exorbitant privilege.”

- Frankly it shouldn’t have taken so long. After all it didn’t take much to see evidence of countries that did all they could to avoid receiving any part of this privilege.Capital controls have historically been as much about preventing foreigners from buying local government bonds as it has been about preventing destabilizing bouts of flight capital, and living in China, where an aggressive demand for the privileges of reserve currency status coincide with equally aggressive policies that prevent the RMB from achieving reserve currency status (and that transfer ever more of the “benefits” to the US) made clear the huge gap in rhetoric and practice. After all the US demand that China revalue the RMB is also a demand that the PBoC stop increasing US dollar reserves.

- If a country takes steps to expand its trade surplus, it is also taking steps to expand its net export of savings – these are one and the same thing. The constant trade disputes between the US and Japan in the 1980s over the undervaluation of the yen can be recast as disputes about Japan’s insistence on its right to give the US more of the exorbitant privilege and the US refusal to accept Japan’s seeming generosity. Trade disputes between China and the US in the 2000s were more of the same.

In a world where final demand is still tepid, supply abundant, and the wrecking ball of global rebalancing swings widely, if US growth slows its policy makers could decide to stop accepting the world’s volatility and start limiting purchases of US paper by international players, and raise tariffs to protect themselves as others race to devalue during this dollar bull move. If that happens, or in expectation of that happening, there would likely be a flood of global capital racing back from the periphery into dollars before the barn door is closed. I am not saying this will happen, but expectations tend to drive money flow.

Keep in mind globalization is not a self-fulfilling prophecy. It requires work and cooperation on the part of the major players. I think an objective observer would say, based on global trade flow and the breakdown in global trade negotiations (Europe and Asia), and the political tensions building among the major powers, globalization is now reversing. This is bad news for the global economy and risk assets, i.e. stocks; but perversely good news for those with a long-term bullish view on the US dollar.

Note: You can find our occasional posting of forex view, sent first to our subscribers of our Black Swan Forex service, posted on our site here. Presently and cautiously, we have been playing for a correction in EUR/USD and USD/JPY…you can find our recent daily view at the site. We also send these charts automatically to our Twitter, Linked In and Facebook pages.

Jack Crooks

President, Black Swan Capital

Twitter: @bswancap

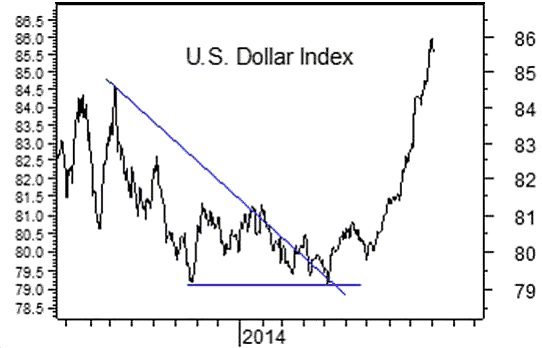

The US Dollar has surged higher the last few weeks…as money leaves the “rest of the world” and comes to America seeking safety and opportunity. We have been relentlessly bullish the US Dollar for months…believing that it is in the early stages of a multi-year bull market…BUT…we think it is WAY OVERDUE for a correction so we are now FLAT the currency markets in our short term trading accounts.

It’s a bi-polar world…with the USA representing ~24% of global GDP and growing…while the other 76% of the world seems to be slowing….setting up the important “diverging central banks” story. The US Dollar may be short term WAY overbought…but in our 40 years of trading currencies we have learned that FX trends go WAY further than you think is possible or reasonable. So we are on the sidelines…waiting for a correction to re-enter long positions on the Dollar…we do NOT want to be short. The Dollar is at 4 ½ year highs…up ~10% in the last 5 months…up ~20% since May 2011…a date we believe was an important Key Turn Date across markets…the date we believe the current multi-year Dollar bull market began.

The Yen is at 6 year lows…down ~28% (!!) since the market realized that Abe was going to win the election in late 2012 and take dramatic steps to end deflation in Japan…one of those steps was to weaken the Yen…a classic “Currency Wars” move!

The Euro is at 2 year lows…down from 3 year highs in May when it reversed with a Weekly Key Reversal Down…it’s down ~11% in the last 5 months.

![]()

The CAD is just above the 5 year lows of 88.50 made in March of this year. On the May 2011 Key Turn Date (and again in July 2011) CAD topped out at 1.06…as the US Dollar started to rise and commodities began to fall. The CAD is down ~16% from its May 2011 highs. We look for the CAD to make new lows this year against the US Dollar and fall further in 2015…BUT…we see the CAD rising against most other currencies.

The CRB commodity Index hit All Time Highs in 2011 and then started to fall as the US Dollar started to rise. The CRB is now at 4 year lows…down ~30% from its highs. A strong US Dollar is “bad news” for commodity prices.

Gold also reversed from All Time Highs in 2011 as the Dollar started to rise…a break of the $1180 lows targets $1000…or lower.

One of the reasons we think that the Dollar is in the early stages of a multi-year Bull market is because the major up and down cycles over the last 40 years have run for about 5 to 7 years. We think the current Bull Cycle started May 2011 and may have another 2 to 4 years to run.

We bought S+P puts September 19…the day the DJIA, DJT and the S&P 500 hit All Time Highs (and Alibaba debuted) and turned lower…BUT…we liquidated those positions last week (well off the lows) as we feared another “buy the dip” surge. The S+P has bounced off the trend line from the November 2012 lows…lows made as Abe took over in Japan and launched his inflation program….lows we consider to have initiated the Latest Bull Leg Higher in the 5 year American stock market rally. We remain skeptical of the stock market but look for it to exhibit “topping action” over the next several weeks rather than just “turn on a dime” and head lower.

Market Psychology began to turn negative the first week of September (Martin Armstrong) while the major US stock market indices continued higher. They (and Treasury yields) turned down on Sept 19…with the DJIA falling 675 points from the Sept 19 top to the Oct 2 bottom as the VIX jumped higher. We have huge respect for the momentum of the 5 year Bull Market in American stocks…we can imagine that some the money flowing into America from the “rest of the world” will go into stocks. We remain skeptical of stocks at these levels but look for “topping” price action for the next few weeks rather than a simple “turn of a dime” transition from a bull to a bear market.

The U.S. Dollar Index has recently been in one of the biggest blowoff moves we have seen in years. The lesson of the past blowoffs is that the downward slope out of the eventual top tends to symmetrically match the slope of the advance up into it.

This week’s chart shows us that the commercial traders of various currency futures contracts are already making a huge bet on a dollar decline. The indicator in the chart is one that I created several years ago by combining the commercial traders’ net position in multiple currency futures contracts into a single indicator. It does not include all of the currency related contracts which are now featured in the most recent Commitment of Traders (COT) reports, because they do not all have the same lengthy and consistent history of reporting. This indicator combines the commercials’ net position in the euro, yen, pound, Mexican peso, Swiss franc, Canadian dollar, and US Dollar Index futures, each weighted according to the dollar value of each position.

The current reading is the highest in the history of this indicator, which dates back to the creation of the euro currency in 1999. That is another way of saying that the “smart money” commercial traders are making a huge bet that this uptrend in the dollar is going to reverse itself. Commercial traders are often early in adopting a lopsided position, but they are nearly always proven to be correct.

This same lopsided position is also apparent when we look at the commercials’ positions in the individual contracts. Here is a chart showing the commercials’ net position in just the Dollar Index futures:

For this contract alone, the commercial traders are not quite at an all-time record net short position. But they are nevertheless at a pretty big one, and this condition usually is associated with an important top for the Dollar Index.

A similar (but opposite) condition exists in the COT Report data for the euro futures. A trader who is long the euro versus the dollar could also be said to be short the dollar versus the euro. The euro is the single biggest component in the Dollar Index, accounting for a larger weight than all of the other components put together. As the euro’s value has fallen in recent weeks, the commercial traders have responded by increasing their net long position to a huge degree, evidently betting on a big upside reversal for the euro (eventually). Upward movement for the euro would mean downward movement for the dollar.

If the commercial traders are correct about the dollar reversing course and heading lower in value, then this will have profound implications across multiple market segments. Commodities prices should rise, commensurate with the percentage amount of the dollar’s fall. Small caps should reverse their recent trend of underperformance which is correlated to the dollar’s outperformance; when the dollar is up, small companies have a tougher time competing in the international markets.

And a falling dollar should also mean rising CPI inflation rates. All of these changes have been modeled by other indicators, as described in the previous articles linked below. It is nice when there are multiple layers of confirmation.

For stock market investors, this all matters because of how changes in the value of the dollar especially affect small cap stocks. Here is a chart comparing the US Dollar Index to a relative strength line for the Russell 1000 Index (large caps) versus the Russell 2000 (small caps).

The relative strength line in this chart rises when large caps are outperforming, or when small caps are underperforming. The 2014 blowoff up move in the Dollar Index has been hurting the Russell 2000 stocks and not having much of an effect on the large caps, thereby making the line rise. Once the dollar tops and turns down, small caps should be expected to be the outperformers again.

And oh, by the way, a big dollar downturn should be a huge tailwind for gold prices finally starting to rise.

Tom McClellan

The McClellan Market Report

www.mcoscillator.com

The dollar is on a tear. And the world is scrambling to figure out what it means.

Beginning with the always-interesting Martin Armstrong in a recent Financial Sense interview:

“I know a lot of people that hate the dollar, but you have to understand the dollar is really only the game in town. Yes, we have a big debt but that debt is absorbed by central banks just having to hold reserves. They’re holding it in U.S. government debt. You can’t hold debt of Greece. Debt of Germany just went negative…France is in trouble as well as Spain and Italy…

You go to New York and it’s all foreigners buying the top-end real estate; same thing in Florida. China is the number one buyer of the highest priced real estate in the U.S. Canada is the number one buyer of real estate as far as the number of properties…

So, this is the trend as war develops more in the Middle East and also in Europe and Asia. Capital has no place to go but the United States and this is going to push the U.S. dollar up higher…”

Another positive take comes from Monty Guild, also on Financial Sense:

Investors, Pay Attention: Causes and Implications of U.S. Dollar Strength

A rising U.S. Dollar has benefits, including higher demand for U.S. Treasuries, lower borrowing costs for the Federal government, foreign demand for U.S. assets (including stocks), lower commodity prices, and especially lower oil prices, which will hurt Russia and benefit the U.S consumer by lowering the cost of gasoline.

Overall, until any negative effects begin to manifest, a stronger Dollar suggests money will continue to be attracted to the U.S. stock market, especially stocks whose sales are primarily domestic, and not international, and particularly for large-cap stocks. This has already begun; larger companies have been outperforming small- and mid-cap companies since early summer. Investors should focus on large U.S. companies that do not get a major share of their profits from abroad. Stocks of companies that sell globally will see their foreign earnings somewhat diminished by a lower value of their foreign currency sales in U.S. dollar terms.

Caroline Valetkevitch at Reuters takes the other side, pointing out that some of those negative effects are already manifesting:

Surging dollar may be triple whammy for U.S. earnings

The suddenly unstoppable U.S. dollar is posing a triple threat to American companies’ profits: driving up the costs of doing business overseas, suppressing the value of non-U.S. sales and, perhaps most worryingly, signaling weak international demand.

The dollar has been on a tear, with an index tracking it against six other major currencies notching roughly an 8 percent gain since the end of June. Few analysts see its breakout performance stalling out anytime soon since the U.S. economy stands on much firmer footing than most others around the world, Europe’s in particular.

For companies in the benchmark S&P 500, that’s a big headwind because so many are multinationals, and as a group they derive almost half of their revenue from international markets.

“You will get some companies that have failed to meet expectations based on the weakness we’re seeing overseas, so it is going to be a source of disappointment,” said Carmine Grigoli, chief investment strategist at Mizuho Securities in New York. Moreover, that weakness, especially in Europe, “is going to be critical here,” he said. “It’s an important component of (U.S.) earnings going forward.”

And while investors and analysts have begun to figure in the negative effects of a fast-strengthening dollar with regard to the approaching third-quarter reporting period, the risk to the fourth quarter and 2015 remains largely unaccounted for.

For instance, third-quarter profit-growth expectations for S&P 500 companies have fallen back to 6.4 percent from about 11 percent two months ago, Thomson Reuters data showed. By contrast, the fourth-quarter growth forecast is down just slightly, to 11.1 percent from a July 1 forecast of 12.0 percent. And profit-growth estimates for 2015 have actually increased in that time from 11.5 percent to 12.4 percent.

“If you try and extrapolate out to the fourth quarter and how much that currency effect is going to be, your guidance is probably going to come down for a good slug of the multinationals on the S&P,” said Art Hogan, chief market strategist at Wunderlich Securities in New York.

WARNING FROM FORD

Ford Motor Co.’s disappointing forecast this week may be a hint of what’s to come. The No. 2 U.S. automaker cut its forecasts for pretax profit this year, citing steeper losses in Russia and South America. “Not to extrapolate too broadly from one company, but I think the negative sentiment . . .has been pretty dramatic,” said Michael James, managing director of equity trading at Wedbush Securities in Los Angeles. Ford shares lost 10.7 percent last week.

The onslaught of quarterly results begins soon, and the next two weeks bring reports from U.S. companies with some of the highest levels of overseas sales. Among them, fast-food restaurant operator Yum Brands, which derives roughly 77 percent of its sales overseas, is due to report on Tuesday, while results from chipmaker Intel, with about 83 percent of its sales coming from overseas, are due on Oct. 14.

Finally, Automatic Earth’s Raúl Ilargi Meijer goes downright apocalyptic in his recent The US Dollar Is About To Inflict Carnage All Around The Planet, where he quotes some representative reports:

“The weakening yen is starting to squeeze Japanese consumers as prices rise for everything from Burgundy wine to instant noodles, threatening Prime Minister Shinzo Abe’s plans to revive the country’s economy. The currency slid to 110 yen to the dollar yesterday, the lowest level in six years, making imported goods and materials more expensive. Though inflation is one of Abe’s monetary goals, the yen’s sharp slide undermines steps to boost consumer spending and endangers public backing for his economic program…. Japan’s GDP shrank an annualized 7.1% in the April-to-June period, the most since the first quarter of 2009.”

“The yen’s slide to a six-year low is amplifying a rout in emerging-market stocks as investors shift their focus to Japanese companies with earnings in dollars, according to Morgan Stanley. The MSCI Emerging Market Index tumbled 7.6% in September, the most since May 2012, led by China and Hong Kong. That compares with a 3.8% drop for the Topix Index in the period. The yen depreciated 5.1% versus the dollar to the weakest level since August 2008 last month, while a gauge tracking developing-nation currencies retreated 3.8%.

Net inflows to U.S. exchange-traded funds that invest in emerging-markets tumbled 82% to $977.9 million in September, led by a 90% decline to China and Hong Kong, data compiled by Bloomberg show.”

“After ticking just above 110.00, USDJPY has been a one-way street lower and that means only one thing… Japanese stocks are cratering. From Friday’s highs, The Nikkei 225 has crashed over 1000 points (despite Abe’s promises yet again of more pension reform buying of stocks). Of note, perhaps, is that, Japanese investors bought a net $3.6 billion of foreign stocks last week – the most since January 2009 – perfectly top-ticking global equities… Well played Mrs. Watanabe.”

“Inflation expectations in the US have just followed the eurozone by plunging lower. Until very recently, the Fed and the ECB had been quite successful at keeping inflation expectations in their normal range – this despite their clear failure to control actual inflation itself, which has consistently undershot expectations. Investors are beginning to realise that contrary to their confident actions and assurances, the Fed and the ECB have failed to prevent a dreaded replay of Japan’s deflationary template a decade earlier in the West.”

Meijer’s conclusion: “It’s going to be carnage out there.”

Some thoughts

Wow. If the world wasn’t already interesting enough, a soaring reserve currency definitely adds some spice.

There are clearly benefits to a strong currency. And in recent years a lot of very smart people have made favorable foreign exchange trends a centerpiece of their analysis, generally citing a strong currency as an investment positive. But there seems to be a missing piece to that scenario, which is debt.

True, other things being equal a strong currency is a sign of (relative) confidence and generally a good thing for a country that has its financial house in order. Appreciating money makes its citizens’ savings more valuable and its corporations better able to snap up cheap acquisitions abroad. On balance, the strong currency society gets richer.

But for an over-indebted country, where local savings are dwarfed by local debt, a strong currency makes the debt burden even heavier, so the net effect is negative. For a real-world test of this thesis, simply look at who had the last batch of strong currencies. Between 2009 and 2013 that would be Japan and Europe, which are now tipping into recessions that threaten to become something much worse.

Which is why the dollar is soaring. Europe and Japan — along with nearly-as-over-indebted China — need weaker currencies not to thrive, but survive. US policymakers, while recognizing the downsides of a soaring dollar, no doubt see taking one for the team (i.e., the global economy) as better than a list of alternatives that includes widespread Depression.

Now the question is whether the strong dollar will do to the US what the strong yen and euro did to Japan and Europe. That is, will America in 2015 be an island of stability in a sea of chaos or will it be a yet another deflationary basket case?

If your speculative or business profit is in any way connected to the directional movement in the forex market, we believe our service can have a considerable impact on your bottom line. Our ideas can be integrated with your current decision-making process to enhance timing, risk-reward ratios and the accuracy of your market predictions and precision of your risk strategies.

If your speculative or business profit is in any way connected to the directional movement in the forex market, we believe our service can have a considerable impact on your bottom line. Our ideas can be integrated with your current decision-making process to enhance timing, risk-reward ratios and the accuracy of your market predictions and precision of your risk strategies.

We apply Elliott Wave analysis to the forex market. We speak to our clients every day. We share all of our research to help our clients develop their own ideas. Our service is easy to follow. We offer specific actionable trading ideas which include entry, risk, and profit levels.

Receive our free Currency Currents go HERE

Listen to Michael Campbell interview Jack Crooks on Oct 4th’s Money Talks HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair