Currency

Austria, 1920-21: The government printed money to cover its debts from World War I.

Austria, 1920-21: The government printed money to cover its debts from World War I.

Food and fuel costs exploded. Banks urged their customers to convert Austrian kronen into a more stable currency… even though it was against the law.

A law-abiding widow is wiped out on the day of a bank run. Her diary entry is reproduced in Adam Fergusson’s book When Money Dies…

“Why don’t you think the krone will recover again?” [I asked my banker.]

“Recover!” [he] said with a laugh… “just test the promise made on this 20 kronen note and try to get, say, 20 silver kronen in exchange.”

Yes, but mine are government securities: Surely, there can’t be anything safer than that?”

“My dear lady, where is the state that guaranteed these securities to you? It is dead.”

We’ve recounted the tale before. We tell it again now for two reasons. First as a reminder that most of the imbalances that caused the Panic of 2008 remain woefully out of balance. But you already knew that.

There’s extra urgency to our telling now: The one “X factor” the pundit class touts as the U.S. dollar’s savior? It might prove the dollar’s final undoing. Bank runs, capital controls, an effective default on the national debt — and all because of the “prosperity” we’re enjoying now.

Our suspicions were first raised in January…

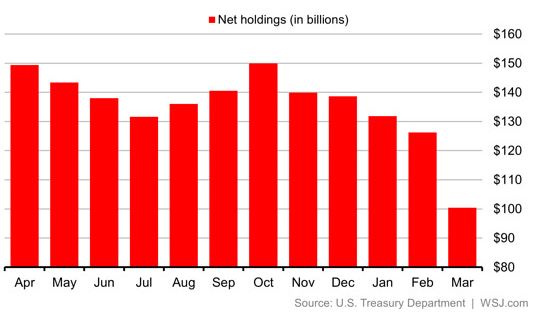

Russians sold out of U.S. Treasury debt in droves in March as the U.S. authorized sanctions against Moscow and Russia’s central bank intervened against a plummeting ruble, new U.S. figures showed Thursday.

Russians sold out of U.S. Treasury debt in droves in March as the U.S. authorized sanctions against Moscow and Russia’s central bank intervened against a plummeting ruble, new U.S. figures showed Thursday.

Russia’s net Treasury security holdings dropped $25.8 billion in March to $100.4 billion, tumbling 20% from February’s $126.2 billion, according to U.S. Treasury Department’s report on international capital flows. Treasury’s report doesn’t explain what caused the cash flows. But…..

Not so long ago, a reasonably-presentable American could live an hour outside of a city and commute in for a government or banking job, thus getting the best of both worlds: city-level wages and a 3,000 square foot house with a big yard for the kids.

But then municipal governments ran out of money and started laying off, while banks, traumatized by their 2009 near-death experience, cut back on mortgage and consumer lending and fired the related staff. The only other jobs available were in service industries like food and retail that paid next to nothing and didn’t offer benefits.

Meanwhile, the cost of living in and commuting from suburbia has been rising. The chart below shows the average price of a gallon of gas, a pretty good proxy for the cost of a daily commute, up by nearly 50% since 2005. At about $3.60 a gallon, the current national average price is 7 cents higher than it was a year ago, with no letup in sight.

All of a sudden our hypothetical suburbanites find themselves with barely enough income to cover their mortgage or rent, let alone their health care, food (which is also way up lately) and gas. And now the kids are about to go off to college…

The result: millions of formerly middle class families living in nice suburban houses or expensive apartments are slowly going broke. The New York Times just published a long, fascinating but very depressing article on the morphing of suburbia to ghetto in California’s Inland Empire. An excerpt follows; the full article is here:

“Hardship Makes a New Home in the Suburb

MORENO VALLEY, Calif. — The freeway exits around here are dotted with people asking for money, holding cardboard signs to tell their stories. The details vary only slightly and almost invariably include: Laid off. Need food. Young children.

Mary Carmen Acosta often passes the silent beggars as she enters parking lots to sell homemade ice pops, known as paletas, in an effort to make enough money to get food for her family of four. On a good day she can make $100, about double what she spends on ingredients. On a really good day, she pockets $120, the extra money offering some assurance that she will be able to pay the $800 monthly rent for her family’s three-bedroom apartment. Sometimes, usually on mornings too cold to sell icy treats, she imagines what it would be like to stand on an exit ramp herself.

“Everyone here knows they might have to be like that,” said Ms. Acosta, 40, neatly dressed in slacks and a chiffon blouse, as she waited for help from a local charity in this city an hour’s drive east of Los Angeles. Both she and her husband, Sebastian Plancarte, lost their jobs nearly three years ago. “Each time I see them I thank God for what we do have. We used to have a different kind of life, where we had nice things and did nice things. Now we just worry.”

Five decades after President Lyndon B. Johnson declared a war on poverty, the nation’s poor are more likely to be found in suburbs like this one than in cities or rural areas, and poverty in suburbs is rising faster than in any other setting in the country. By 2011, there were three million more people living in poverty in suburbs than in inner cities, according to a study released last year by the Brookings Institution. As a result, suburbs are grappling with problems that once seemed alien, issues compounded by a shortage of institutions helping the poor and distances that make it difficult for people to get to jobs and social services even if they can find them.

In no place is that more true than California, synonymous with the suburban good life and long a magnet for restless newcomers with big dreams. When taking into account the cost of living, including housing, child care and medical expenses, California has the highest poverty rate in the nation, according to a measure introduced by the Census Bureau in 2011 that considers both government benefits and living costs in different parts of the country. By that measure, roughly nine million people — nearly a quarter of the state’s residents — live in poverty.

Not long ago, the Inland Empire, as the sprawling suburban area east of Los Angeles is known, attracted people hoping to live out that good life. Before the recession, it was booming; housing developments were cropping up all the time, quickly followed by big box stores and strip malls to cater to the new residents.

The region was — and still is — the fastest growing in the state. But the jobs have never really followed the people who come here looking for cheaper housing. The median home value is $325,000 and the median rent is $1,690, according to the real estate database Zillow. That compares with $462,000 and $1,860 in Los Angeles.

For many, those costs are still unaffordable. Unemployment in the region hovers around 10 percent and nearly one-fifth of all residents live in poverty, the highest rate among the largest metropolitan areas in the country. By the official federal measure, nearly one-third of all children here are poor. The number of poor in San Bernardino and Riverside Counties nearly doubled over the last decade.

“This is where poor people live now, and this is where they are going to live,” said Alan Berube, an author of the Brookings Institution study. “When poverty moved out of the inner cities it didn’t just go next door, it went 30 miles away. But at the time those families might not have been poor — they were just chasing the middle-class dream. Then, boom, that evaporated.”

Some thoughts

The theme of this series (the previous articles are here) is that much of what affluent people in general and Americans in particular have come to take for granted is turning out to be a delusion bought with debt, unrealistic energy assumptions and fraudulent bookkeeping, and is evaporating as those, um, mistakes come to light. Entitlements like Social Security and Medicare, for instance, only exist in their current forms because so much of their real cost is hidden in largely-unreported “unfunded liabilities.” Cities have been able to offer good roads and quick police response because they pay their cops and road workers with the promise of wildly unrealistic future pensions.

The concept of suburbia, meanwhile, always depended on debt and cheap energy. For a typical American family to heat and cool four times the space of its counterparts in other countries — and to move two tons of metal 100 miles each day just to get to a job — is only possible as long as the rest of the world is kept poor and therefore unable to consume fossil fuels at the North American rate. But as China, India and Brazil get into the game, energy costs are rising. Combine this with the ongoing decline in finance/government jobs, and the unworkability of modern suburbia becomes obvious.

But calling suburbia’s demise inevitable doesn’t make it any less tragic for the victims. Anyone who’s lived in an affluent suburb knows they are (or at least used to be) home to perhaps the world’s highest concentration of innately happy, optimistic beings, namely kids, dogs and adults with big houses and good jobs, none of whom are guilty of anything more than a lack of attention to macroeconomic trends. So while schadenfreude is appropriate for, say, imploding law firms or investment banks, dying suburbs just deserve our pity.

\

“Our main format is now video analysis…”

Here are today’s videos:

US Dollar Meltdown Begins Charts Analysis

Gold Money Flows Charts Analysis

Silver Fuel Cell Charts Analysis

GDX Dark Clouds Charts Analysis

Gold Stock Exhaustion Gap Charts Analysis

Thanks,

Morris

There seems to be no shortage of bad ideas in Washington. They usually involve an unspecified cost to the people at large to provide an undisclosed benefit for the influential and well-connected. But it takes peeling the onion to see what’s really going on in some of these Washington schemes.

One of the latest — a really bad idea that popped up this week — is from Senator Marco Rubio. Rubio has been sharing a lot of his ideas about Ukraine and Russia lately. In March, he offered a package of “8 Steps Obama Must Take to Punish Russia.” Among them was his idea that we must make a renewed push for the Republic of Georgia to join NATO.

Another NATO member on Russia’s border? Bad idea. There is enough dry tinder for one conflagration already.

There is as well — if anybody cares — the issue of U.S. integrity. Rubio may be too young to remember, but the Soviet Union was still a fearsomely armed world power when it dissolved. It had 380,000 troops in East Germany, a military presence resulting from Germany’s unconditional surrender ending World War II. Now the Soviet Republics were being set free and the Warsaw Pact was expiring. It was a remarkable thing seeing the Evil Empire, armed though it was with thousands of nuclear warheads, simply come to an end. Without a shot being fired.

Gorbachev was willing to let all this happen. And he was willing to let Germany reunify. But Gorbachev did ask for one assurance: that NATO not expand its war machine to Russia’s border.

Gorbachev was willing to let all this happen. And he was willing to let Germany reunify. But Gorbachev did ask for one assurance: that NATO not expand its war machine to Russia’s border.

It seems to have been a reasonable point. Russia, like other nations, is concerned about expansive military might on its border. That’s really the source of the flare-up in Ukraine today.

In any event, it seemed reasonable enough to President Reagan’s secretary of state, James Baker. “Not one inch eastward” were his words about NATO expansion as he discussed conditions with Gorbachev in Moscow. The deal was confirmed in the Kremlin the next day by Germany. Chancellor Helmut Kohl agreed, while his foreign secretary, Hans-Dietrich Genscher, assured the Kremlin that “for us, it stands firm: NATO will not expand itself to the East.”

And with that the Cold War — having bled the people of two continents for more than a generation — simply died.

Still some people would like to see it resurrected. Rubio has joined 20 other senators as a sponsor of the Russian Aggression Prevention Act of 2014. It calls for more armaments for Ukraine. It authorizes increased spending on NATO. It demands joint military exercises with Ukraine, Georgia, Moldova, Azerbaijan, Bosnia and Herzegovina, Kosovo, Macedonia, Montenegro, and Serbia.

Perhaps its least noted provision is the most loaded with explosives. It appropriates $10 billion for the U.S. to meddle in the internal political affairs of Russia, in the same way that the government spent $5 billion meddling in the internal affairs of Ukraine and micromanaging a regime change in Kiev.

Bad ideas all.

But now Rubio has offered another big idea, launching it on the editorial page of Tuesday’s Wall Street Journal. Rubio is calling for the establishment of a “currency board” to prop up the value of the hryvnia, Ukraine’s national currency. Rubio says Americans must extend to Ukrainians the benefits of having “a trustworthy sovereign currency.”

Shouldn’t the trustworthiness of Ukraine’s money depend on Ukraine’s fiscal and monetary probity? The world is crawling with countries that would like to have trustworthy sovereign currencies but are unwilling to act responsibly to get them. Why then should the American people, still straining under the “new normal” conditions of their own economy, be taxed to provide for them what they are not willing to provide for themselves?

If Rubio understands exactly what a currency board is, it is not apparent in the text of his proposal. One should always be skeptical of grandiose government plans and schemes that don’t come with hard and reliable numbers attached. Rubio offers not a single number that would make clear the cost involved in funding a reserve sufficiently large to provide an unlimited liquid market for a broken currency at a fixed and artificially high price.

Ukraine is free to establish a rule-bound exchange rate using its own currency reserves, but Rubio has his eye on your money, citing IMF loans of unspecified scope. Of course the IMF is a device for laundering U.S. taxpayer money, since we are the largest contributing nation. Right now Congress is considering a measure that effectively doubles the U.S. commitment to the IMF, a package to approve $65 billion to IMF core funding and about $106 billion for an IMF supplementary fund.

Despite its failure to meet the terms of two prior IMF loans, the institution has approved a new $17 billion package for Ukraine. In the air around these multinational deals and proposals like Rubio’s, one catches the desperate scent of bankers anxious to be spared the risk of a default. A good chunk of the new IMF package will be used by Ukraine to pay banks and Gazprom, the Russian gas giant which is owed $2.2 billion.

So to peel the onion: Americans will borrow money from foreign creditors like Russia (yes, Russia is a major creditor of the U.S. Treasury) and China to launder through the IMF to give to Ukraine which in turn will give the money to multinational banks and Russian plutocrats. It’s enough to bring a tear to your eye.

And now we are asked to fund a currency board to prop up Ukraine’s hryvnia.

What about our own currency? Has Senator Rubio looked at the fundamentals of the dollar lately? It would make a grown man cry.

Best wishes,

Charles Goyette

P.S. Don’t wait one moment longer to read the shocking truth behind the most devastating scandal of this or any other century!

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair