Currency

US DOLLAR AND CURRENCIES- SUMMARY

The Dollar moved slightly higher on Tuesday on more safe haven buying.

The US Dollar Index gained.034 to settle at 79.552.

Spain successfully sold 4 billion euros of 3 and 6-month bills on Tuesday, although yields were higher than the previous auctions. Spanish Prime Minister Rajoy on Thursday is expected to unveil additional austerity measures when he presents his 2013 budget. Italy today successfully sold zero-coupon 2014 bonds at 2.532%, down from 3.064% on Aug 28.

Spanish ten year bond yields rose over 6 bp to 5.745%.

The GfK Oct German consumer confidence index of 5.9 was unchanged from September’s 5.9 and was in line with market expectations.

The Euro was up .22% against the Dollar.

Japan’s Sep small business confidence index rose slightly to 45.1 from 44.8 in August.

The Yen was down .05% against the Dollar.

China’s Aug leading economic indicator rose 1.7% m/m after a +0.6% m/m gain in July, which was a possible sign that the Chinese economy is stabilizing. Positive factors in the leading indicator included a rebound in real estate and credit growth, and an improvement in consumer expectations. The market consensus is that Chinese GDP likely eased to about +7.4% in Q3 from +7.6% in Q2.

China’s central bank today injected a record 290 billion yuan ($46 billion) into the banking system to address a liquidity squeeze ahead of next week’s Chinese holiday week.

As long as there is faith in the dollar and fiat money as a whole-and by and large there is, I see the system holding together for quite a while. I think it’s Ian McAvity who calls the dollar “the prettiest horse in the glue factory.” This became dramatically evident this week.

Owning Dollars other than for trading purposes is a fool’s bet in my opinion. As a long term plan, you should be looking to exit Dollars and move into hard assets or strong natural resource based currencies. I particularly favor the Canadian Dollar. Other choices include the Australian Dollar, the Singapore Dollar and, of course, the Chinese Renminbi. My view is that we’re ultimately headed back to the March 18, 2008 low of 70.698 and will later see 66.00 or much, much lower, possibly even the 30.00 area. This could occur between 2014 and 2018. Short-term (between now and early 2013) we should see the 73.00-74.00 area. For political reasons we may never experience the sudden overnight sudden devaluation as seen by Argentina, Brazil or Mexico in recent decades, but instead continue to see a slow diabolical deterioration. -Ed Note: Try Mark Leibovit’s Special Trial Offer HERE

Mac Slavo: If you think the Federal Reserve’s quantitative easing will only affect the U.S. dollar, think again. Now that the United

Moreover, because everyone is joining the fray, all of that extra money will make its way into key resource stocks and commodities, adding further upside price pressure to essential goods like food and fuel.

It’s a race to the bottom, and the losers are the 99.9% of us who aren’t being kept in the loop.

Quantitative easing is really another word for currency wars. A weak U.S. currency puts continued pressure on the Japanese Yen, the Chinese Yuan, the South Korean Won, the Australian dollar and other currencies.

Cheap money also fuels speculation and this money quickly drifts into commodity markets and the ETFs that help propel commodity market speculation. This is inflationary for food prices.

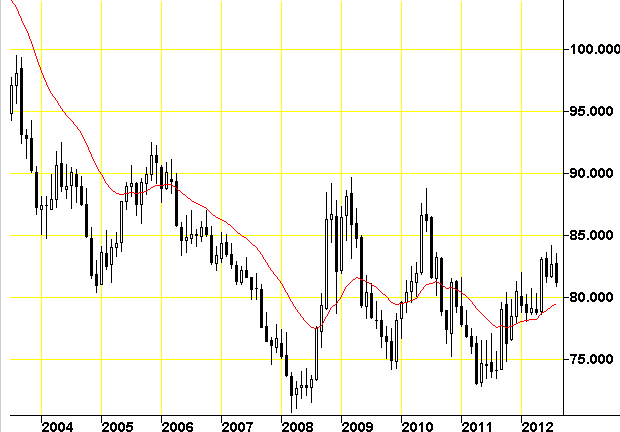

The lower the U.S. dollar the greater the intensity of currency wars.The break below the key uptrend line on the Dollar Index chart was an early warning of the third round of quantitative easing (QE3).

The most important question now is to use the chart to examine the potential downside limits of a QE3 weakened U.S. dollar.

The weekly close below this uptrend line was the first signal of a major change in the trend direction. It came before the announcement of QE3, last week.

The third significant feature is historical support near 74.5. This is the upper edge of a consolidation band between 73.5 and 74.5. This is the downside target for the Dollar Index following a fall below 79.

This target can be reached very rapidly over three to four weeks. A rapid collapse of the U.S. dollar puts immediate pressure on other dollar-linked currencies.

There is a very low probability the U.S. dollar will resume its uptrend. The move below the value of the uptrend line and a fall below 79 confirm thata new downtrend has developed.

The weakness in the U.S. Dollar will hurt export dependent economies and companies.

There are two ways this may end – neither of which is going to be good for the average Joe:

- The Fed et. al. continue to print, so much so that prices for food, gas, utilities and other key commodities that are linked to US dollar movements will rise exponentially. This rise in prices will accelerate the pressure on consumers as more jobs are lost in an ever progressing, self reinforcing economic death spiral. The pressure of rising prices, even though the Dow Jones may reach 20,000 or 50,000 points, will be so great that American consumers simply won’t be able to pay their bills or put food on the table.

- The Fed and their brethren around the world won’t be able to print fast enough to maintain stable financial markets, leading to stock market crashes in Europe, Japan, China and the United States, which then leads to a shift of capital to US Treasury bonds, ironically strengthening the dollar. A weak US economy that isn’t creating jobs and is adding tens of thousands of people to an already overburdened social safety net every week will eventually lead to confidence being lost in the US government’s ability to repay its debts. As we noted in 2012 Predictions of a Mad Tin Foilist, the end result will be a currency crisis, or de facto default by way of hyperinflating away our debt.

Both scenarios are virtually the same, as both will end with complete and utter destruction of Americans’ wealth.

Despite the mainstream notion that inflation is under control and most of the money is sitting on the sidelines with banks, all we need to do is look at the price increases for consumers since private and public bailouts begin in late 2008. Gas has doubled. Food is up over 25%. Electricity costs and the cost of just about every other non-debt based asset has steadily risen.

This is not going to stop.

While timelines remain elusive because of never ending government intervention into financial markets and economies, the policies being instituted by central banks around the world can only lead to continued degradation of paper currencies and the rise in prices of all goods linked to those currencies.

In January of 2010 we suggested a strategy of buying physical commodities at today’s lower prices and consuming those commodities at tomorrow’s higher prices. The trend for fiat paper money and physical assets has not changed and is, in fact, more pronounced now than ever before.

The US dollar is being systematically weakened until it no longer exists as a viable means of exchange. When this happens you’d better be prepared to operate in a society where traditional money is replaced with mechanisms of exchange like precious metals, food, critical supplies and production skills.

You can begin taking simple steps to prepare now. The collapse of the existing global paradigm is accelerating and if you’re not ready for it the price you’ll pay will be severe.

Related Tickers: SPDR Gold Trust (NYSEARCA:GLD), iShares Silver Trust (NYSEARCA:SLV), Ultra Silver

Quotable

From February 2010:

“Shorting Treasuries is a ‘no brainer…every single human being should have that trade.’”

Nassim Taleb

LOL…hoisted on the horns of a Black Swan petard were you Mr. Taleb?

Commentary & Analysis

Guru Follies

The newsletter crowd, to which I plead guilty, loves to tell you scary stories that often seem to be missing an important element—facts. Let’s take a short stroll down memory lane and review the latest stories from the gurus.

1. Always a favorite, the US dollar is going to get killed. This one is back on the front burner thanks to QE3. Of course, the fact that the dollar didn’t get killed by QE1 or QE2 seems not to matter. It is QE3 that will surely do the dirty deed this time. The newsletter gurus seem to lose sight of one very important axiom of price, it is this: If supply increases, but demand for the increased supply increases even more, price doesn’t collapse; it tends to rise (cateris paribus). The demand for dollar liquidity in a world where the European banking system is desperately deleveraging and many in the private world are doing the same likely means the world reserve currency remains supported.

2. Inflation will soar. This is one of my favorites, as the newsletter crowd remains stark-raving loony over this one despite the facts. After all, this inflation call is simple…more money means more inflation. Slam dunk! But we haven’t seen inflation as defined by the newsletter crowd. We have seen some commodity prices surge on investment liquidity and supply problems, granted. As I have shared with you many times before, if money doesn’t make it into the real economy to be used by real people to bid up the prices of real goods, it isn’t inflation in the normal sense we think of when we say “inflation.” But if we say there has been a massive inflation in financial assets; that would make sense. That’s because much of the money the Fed has created has leaked into financial assets. We can say there has been asset inflation driven by the financial economy. We can say that overall there has been a decline in the purchasing power of global fiat currencies as we view the price of gold. But this is different and more easily deflated.

3. There is a massive bond bubble out there just waiting to pop. I believe we are on our third fear-mongering bond bubble theme since QE started…it could be more, I really have lost track of this favorite scare story. And of course with QE3 fresh in the minds of newsletter buyers, this bubble story is hot again. The flimsy logic behind a bond bubble is the idea that money has moved into bonds irrationally, for some speculative gains and all these investors just don’t understand that hyper-inflation is just around the corner. And if you hold US bonds, you are really in trouble because QE3 is the straw that has broken the greenback’s back and that will add to the pain for bonds. Let us consider some real reasons why bonds are loved and why they could remain loved for a very long time: a. Global demographics – As people get older their portfolio tends to shift toward what they perceive is less volatile and more safe investments such as fixed income.

b. Secular change in consumption patterns – The credit crunch really was a sea change I think. Massive personal balance sheet overleverage, coupled with the decline in the biggest personal asset—real estate—seems to have triggered a sea change in both real consumption and attitude toward future consumption. This means more savings. More savings tends to mean more money in fixed income net…net.

i. The knock-on effect of a change in global consumption/increased savings is the catalyst for rebalancing the current account deficit nations with the current account surplus nations. It is especially bad news for those with export-dominated growth models who will take the brunt of the adjustment domestically…and we know who you are: China, Germany, and Japan…

c. Massive global debt levels equals below capacity future growth. Below capacity future growth will tend to push down the expected return from growth assets—stocks—relative to fixed income. And slower growth is usually accompanied by lower future inflation expectations. And lower future inflation expectations are usually discounted into the current yield for fixed income. Thus, bonds will tend to remain supported.

d. Risk bid. If I am right that the Eurozone crisis is far from over, and that China will likely experience either a hard landing or lead to a major negative growth surprise, the idea of a major risk bid of global money running for safe haven is still a high probability. And safe haven money flows into…you guessed it…fixed income.

e. Historical parallels. This from Hoisington Research, a fixed income investment management firm based in Houston who has been more right on bonds and interest rates for the last five years than anyone I have seen….

“Long-term Treasury bond yields are an excellent barometer of economic activity. If business conditions are better than normal and improving, exerting upward pressure on inflation, long-term interest rates will be high and rising. In contrary situations, long yields are likely to be low and falling. Also, if debt is elevated relative to GDP, and a rising portion of this debt is utilized for either counterproductive or unproductive investments, then long-term Treasury bond yields should be depressed since an environment of poor aggregate demand would exist. Importantly, both low long rates and the stagnant economic growth are symptoms of the excessive indebtedness and/or low quality debt usage.”

We know that debt levels in the industrialized world are in the ozone and still rising. Now take a look at what yields did historically during three similar crisis periods—Japan 1989, United States 1873, and United States 1929–when debt levels were much lower globally than they are now.

Back to Hoisington:

“In the aftermath of all these debt-induced panics, long-term Treasury bond yields declined, respectively, from 3.5%, 3.6% and 5.5 % to the extremely low levels of 2% or less in all three cases (Chart above). The average low in interest rates in these cases occurred almost fourteen years after their respective panic years with an average of 2% (Table below). The dispersion around the average was small, with the time after the panic year ranging between twelve years and sixteen years. The low in bond yields was between 1.6% and 2.1%, on an average yearly basis. Amazingly, twenty years after each of these panic years, long-term yields were still very depressed, with the average yield of just 2.5%. Thus, all these episodes, including Japan’s, produced highly similar and long lasting interest rate patterns. The two U.S. situations occurred in far different times with vastly different structures than exist in today’s economy. One episode occurred under the Fed’s guidance and the other before the Fed was created. Sadly, there is no evidence that suggests controlling excessive indebtedness worked better with, than without, the Fed. The relevant point to take from this analysis is that U.S. economic conditions beginning in 2008 were caused by the same conditions that existed in these above mentioned panic years. Therefore, history suggests that over-indebtedness and its resultant slowing of economic activity supports the proposition that a prolonged move to very depressed levels of long-term government yields is probable.”

Now, you may want to sell this bond market here based on the view it is a bubble. But before you do, let me share an anecdote. I remember it vividly. The recently deceased renowned global strategist, Barton Biggs, who spent most of his years toiling away at Morgan Stanley and was a rock-star when global strategists played those roles, made a bond bubble call back in the mid-1990’s. He said that shorting the Japanese government bond market was the “trade of a lifetime.” Well, maybe. Unfortunately Mr. Biggs didn’t live long enough to see that trade work out.

Webinar Announcement: I edit two currency trading newsletters for Weiss Research. I am doing a free webinar on Thursday, September 20th, at 12:00 p.m. ET, covering key global macro themes and my view on the direction of the dollar and other major pairs as we head into 2013. I invite you to attend and encourage your questions during the event.

The webinar is free. All we ask is that you seriously consider becoming a Member of one of our services offered by Weiss Research.

Please click here to register.

Thank you.

Jack Crooks

Black Swan

www.blackswantrading.com

Quote

“Rather than stimulating a real recovery by focusing on a strong dollar and market interest rates, the Fed’s announcement today shows a disastrous detachment from reality on the part of our central bank.”

– Ron Paul

(Ed Note: Jack Crooks is this weeks Money Talks Guest)

Of Interest

- Troika could give Greece more time for reforms (Telegraph)

- Era of ‘jobs-targeting’ begins as Fed launches QE3 (Telegraph)

Commentary

The Federal Reserve was set-up to disappoint; but they didn’t. And why would they have? Bernanke’s received more than a few pats on the back for his decisions to date:

“QE has made a massive difference,” said Tim Congdon from International Monetary Research. “If they had not done it we would have gone into another Great Depression.”

There were high expectations for Fed action yesterday. They delivered mostly at those expectations, except for one thing – they put no end-date on their operations. Twist … to infinity and beyond.

And that may be the difference maker.

We’d seen several indicators and pieces of analysis to suggest Fed expectations were priced in. That may be true; and the price action yesterday (following the announcement) and this morning may be a blow-off squeeze of sorts. In the recent history of QE and Twisting, the rumors and expectations in the months leading up to the actual action have created the environment for risk assets to rally. These assets, however, have sold off in the periods after the actual action. It is the classic “buy the rumor, sell the news” dynamic.

Action

As of now, that dynamic seems to make the most sense. The market is ripe for a downturn. But once that downturn runs its course (maybe lasting a month or so), there is little reason right now to expect anything but an extended uptrend for risk assets. Certainly this unlimited monetary accommodation will juice up inflation expectations and liquidity, justifying investments in commodities and stocks.

But what about the fundamentals? The Fed’s comments suggest there is nothing horribly worrisome about US growth potential, barring continued pressure on jobs. So has our fundamental analysis been horribly misguided? We don’t think so. Actually, recent Fed action seems to validate our pessimism. But our expectations for price action have been off target. Looking ahead, we are considering ways to hedge current bearish positioning. And unless a real crisis in confidence materializes soon, it will likely make sense to adopt a bullish stance on the markets. Stay tuned.

Pimco’s Gross: I’m Leaning Toward Gold Over Bonds

When the world’s biggest money manager talks, every one listens.

PIMCO’s Bill Gross, manager of the world’s largest bond fund, just told the world he likes gold more than stocks or bonds. The world’s money managers followed suit. (Click HERE or on the link above to watch the 11.18 minute Video)

The European Central Bank just announced a new and potentially unlimited bond buying plan. Prepare the blank checks; the United States already has.

The U.S. economy added 96,000 jobs in August, a disappointing result that could prompt an aggressive response from the Federal Reserve. Ammunition for another round of QE has been served.

If you didn’t believe me before, I seriously hope you do now: Gold will go a lot higher.

Last Sunday, in my letter, “America’s Gold Wiped Out,” I talked about the world’s current financial war: The

Currency War

As a reminder:

A “currency war” is a fight between countries to achieve a lower exchange rate for their own currency. In other words, its competitive devaluation. In short, the cheaper your currency, the more money you attract from foreign entities; this leads to increased exports, growth, and job creation.

The dollar, the yuan, and the euro, are the three super power currencies leading the global currency war. The one on top will be the one that devalues its currency the fastest.

Currency is the heart of a nation; without it, it cannot survive. Its value is its Achilles heel. Collapse its value and everything goes with it.

Stocks, bonds, derivatives, and other investments are all linked through a complex network. If one sector is failing, another might be winning. For example, if stock and bonds are failing, one could turn to commodities to pick up the pieces.

However, all of these investment vehicles are priced in a nation’s currency. Destroy the currency and you destroy all of the markets within the nation. Destroy the markets, and you destroy the nation.

That is why currency is the target in any financial war.

And that is exactly why major battles are no longer fought with AK-74’s and tanks – these merely provide support.

In a controversial book published in 1999 by Col. Qiao Ling and Col. Wang Xiangsui of China’s People’s Liberation Army, they stated:

“In a world where “even nuclear warfare” will perhaps become obsolete military jargon, it is likely that a pasty-faced scholar wearing thick eyeglasses is better suited to be a modern solider than is a strong lowbrow with bulging biceps. We believe that before long, “financial warfare” will undoubtedly be an entry in the various types of dictionaries of official military jargon…financial war has become a “hyper strategic” weapon that is attracting the attention of the world. This is because financial war is easily manipulated and allows for concealed actions, and is also highly destructive.”

Everything around the world is interconnected. Bonds could be issued in Brazil, underwritten in London, and sold through New York. You could even package everything in the form of a derivative from one country and sell it to another; selling securities for cash, backed by nothing more than someone else’s performance.

That means any form of currency manipulation or attacks have serious repercussions around the world. And the two heavy weights of the world are in a full fledged battle against one another.

China vs. United States

While Europe is China’s largest trading partner, China’s main link with the global financial system is the U.S. government bond market.

China earns several hundred billion dollars every year from their trade surplus. This is a lot of money that needs to be invested, and few places can handle that type of investment without severely affecting market prices.

That’s why the Chinese have turned their surpluses into the one place that can handle the size of investments China needs to make – the U.S. government bond market.

China’s foreign reserves hold more than $1 trillion worth of dollar-denominated U.S. securities – that’s more than any country in the world. But this number may be greater than that.

That’s because not every government security is issued by the Treasury. Many of them are issued by Fannie Mae, Freddie Mac, and other banks and agencies; thus making it harder to track.

With such a large holding of U.S. dollar-denominated securities, China has a major concern: They fear that the United States will devalue their currency through massive money printing and inflation, destroying the value of China’s foreign reserves. All while the United States benefit from more exports due to a devalued currency.

China should worry (from last week’s letter):

“Prior to 2011, no one was winning the currency war. China was experiencing a surplus and the US was negative. So the U.S. did everything it could, including persuasions through the G20, to convince China to appreciate their currency to balance out the major trade deficit. But China wouldn’t allow their yuan to appreciate because it would hamper their own growth. Why would they hamper their growth for the benefit of a competing country?

As a result, the United States, empowered by its world reserve status, pulled out its secret weapon: Quantitative Easing (QE). The United States effectively devalued its own currency by increasing its own money supply, forcing inflation onto China.” –

Hypothetically, China could unleash its U.S. treasuries in an open market, highly visible fire sale, in retaliation for the United States’ strategic devaluation. This would cause U.S. interest rates to blow up and the dollar to collapse on foreign markets, forcing a world of financial dislocation and hurt onto U.S. soil.

However, this would also be a big blow to China because the treasury market would collapse long before China could unload even a small portion of its holdings. That means if China attempted to unload, it would mean economic suicide.

The Real Twist

But there is one thing China could do that everyone ignores: operation twist, China.

The Chinese could shift the mix of Treasury holdings from longer to shorter maturities without selling a single bond and without reducing their total holdings. It would be damaging to the U.S. and much more cost effective for the Chinese.

Shorter maturities are less volatile and more liquid, which means the Chinese would be less vulnerable to market shocks. They also wouldn’t have to dump their holdings in a fire sale, but simply wait them out until maturity.

But don’t think the U.S. doesn’t already know this.

Under the United States’ operation twist, the maturity extension program, the Federal Reserve intends to sell or redeem a total of $667 billion of shorter-term Treasury securities by the end of 2012 and use the proceeds to buy longer-term Treasury securities. This will extend the average maturity of the securities in the Federal Reserve’s portfolio.

According to the Fed, “by reducing the supply of longer-term Treasury securities in the market, this action should put downward pressure on longer-term interest rates, including rates on financial assets that investors consider to be close substitutes for longer-term Treasury securities. The reduction in longer-term interest rates, in turn, will contribute to a broad easing in financial market conditions that will provide additional support for the economic recovery.”

In reality, the United States is combating China’s operation twist with its own. If China won’t buy their long-term securities, the United States will just print money to pay for them – further devaluing the foreign holdings of China.

Now do you see the moves being made by both countries?

The media will never tell you this because the U.S. will never say this publicly – it would be politically incorrect. That’s why stuff like this never gets reported.

China has been aggressively diversifying their cash reserve positions away from dollar-denominated instruments of any kind and is deploying its new reserves elsewhere.

Because investment options in other currencies are limited, China has focused on the one thing that makes sense when inflation is in the picture: commodities.

A Major Shift in Currency

For the last few years, China has been diversifying its massive trade surplus into commodities such as gold, oil, copper, agricultural land, water, and stocks of mining companies around the world. This diversification is well underway and gaining extreme traction.

Rumours are already flowing that state-owned China National Gold Corp. is considering bidding for African Barrick.

Earlier in the year, China Guangdong Nuclear Power Corp paid $3.37 billion for uranium developer Kalahari Minerals and its partner, Extract Resources, in Namibia.

China’s Zijin Mining Group is about takeover Australian gold producer Norton Gold Fields.

China National Offshore Oil Co. is bidding $15.1-billion to buy Calgary-based Nexen Inc.

The list continues to grow. (See my letter from last year, Action Speak Louder than Words)

From 2004 to 2009, China secretly doubled its official holdings of gold through one of its sovereign wealth funds, the State Administration of Foreign Exchange (SAFE); they have continued to accumulate under the radar since then. How did they do this without causing a major spike in prices?

SAFE has been making purchases all over the world through global dealers. Since it is not part of China’s central bank, all of these purchases were made off the record. Then, in a single transaction in 2009, SAFE transferred its entire position of 500 tons of gold to the central bank – then announced it to the world.

Combined with the long-term gold buying program already underway, the Chinese is clearly diversifying away from the dollar and encouraging a new financial instrument to the world.

Deals have already been struck by China and other countries such as Russia to bypass the dollar in bilateral trades (see A Really Big Problem). The currency war is in full swing and it’s a ticking time bomb.

A lot of conspiracy theories regarding big bank bailouts, derivatives, and the financial war are real. These things play in the background while citizens around the world act like pawns in a game of chess between countries, bankers, and oligarchs.

Over the next month, I am going to continue sharing the truth about our current financial war. Some of what I say may shock you. Some of what I say may offend you. But all of what I say will give you a new perspective on life.

Next week, I am going to share a dramatic timeline of events that will knock you off your seats. Once you see it, you’re going to be a believer in gold, silver, and other tangible assets – if you’re not already.

Gold Breaks Through

Gold and precious metal stocks broke out once again this past week. The Market Vectors Gold Miners ETF (GDX) is up 8.59% this week and up nearly 20% since early August, when I told readers to become more aggressive in the sector.

The Market Vectors Junior Gold Miners ETF (GDXJ) is up 11.84% this week.

Take a look at the three stocks featured in the Equedia Reports this year:

Timmins Gold Corp (TSX: TMM) (NYSE MKT: TGD) up 22%

Timmins hit a high of CDN$2.74 on Friday, before closing at $2.69. That’s nearly a 22% increase in less than 2 weeks; the initial research report was released on August 26, 2012 when Timmins was trading at $2.21.

Timmins closed at US$2.74 on the NYSE MKT.

Balmoral Resources (TSX.V: BAR) (OTC: BALMF) up 60%

Balmoral hit a high of CDN$0.93 on Friday, before closing at CDN$0.91. That’s nearly a 60% increase in less than 5 months; the initial research report was released on May 13, 2012 when Balmoral was trading at $0.57.

Balmoral closed at US$0.93 on the OTC.

MAG Silver (TSX: MAG) (NYSE.A: MVG) up 37%

MAG hit a high of CDN$11.17 on Friday, before closing at CDN$11.03. That’s nearly a 37% increase in less than 8 months; the initial research report was released on February 2, 2012 when MAG was trading at CDN $8.06.

MAG closed at US$11.29 on the NYSE Amex.

I haven’t sold a single share in any of these companies.

The Bulls are Running

The world’s largest money manager has just publicly stated that gold is a better investment than bonds or stocks.

Money managers around the world are starting to pile into the sector begging for better returns.

Europe has been given a blank check to support the failing countries.

Poor unemployment numbers have given ammunition to the Fed to fire another massive round of stimulus.

The gold stampede is about to begin. Saddle up.

Your Input is Valuable

The Equedia Weekly Letter has become one of the fastest growing investment newsletters in Canada, followed by thousands of bankers, fund managers, analysts, brokerage houses, and retail investors. We’re also now exploding into Europe and the United States thanks to your support.

We’re in an amazing time to own precious metals stocks and that means I am constantly looking for our next big winner. I am becoming very aggressive now.

If there are any companies you feel I should look at, please reply to this email with the subject line: Evaluate

I am currently looking for companies with the following traits:

-

- Advanced-stage exploration, near currently producing mines

- Companies nearing milestones such as an upcoming resource, prefeasibility studies, or major company-changing announcements

- Producing gold/silver companies with strong cash flow and growth prospects

- Undervaluation due to the lack of market exposure and retail following

- Liquidity – companies that trade

- Strong and proven management

- CANNOT be grassroots exploration plays*

*Only serious evaluations will be looked at.

I am also looking at companies with great properties that need to be sold or joint ventured. If you know of any, my friends may be interested. If so, please reply with the subject line: Property

Companies in this report:

Timmins Gold Corp (TSX: TMM) (NYSE MKT: TGD)

Balmoral Resources (TSX.V: BAR) (OTC: BALMF)

MAG Silver Corp (TSX: MAG)(NYSE.A: MVG)

Until next week,

Ivan Lo

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair