Currency

This simple move requires no extra effort… in fact, it happens automatically when you invest in these companies.

I’ve told you before about the enormous number of high-yielding stocks abroad. If you remember, my research team and I found only 17 profitable U.S. companies were paying yields of more than 12%… compared to 227 overseas.

Although the numbers fluctuate daily, that means roughly 92% of the world’s highest yields are found outside of U.S. markets. To me the amount of high-yield international dividend-payers out there is one of the market’s biggest secrets.

But there’s another big potential benefit to investing in international companies that most investors fail to consider.

This simple move could make investors extra gains of 10% or more — even in a single year. It doesn’t require any extra effort… in fact, it happens automatically when you invest in international companies.

Here’s how it works…

Say six years ago you took the trip of a lifetime to Australia. Back then, $1 U.S. bought you roughly $1.30 Australian. That means a hotel room priced at $100 Australian dollars only cost about $77 U.S. dollars, thanks to a favorable exchange rate.

But today, even though the U.S. dollar has seen some gains of late, in relative terms it has plummeted against most currencies — including the Australian dollar. It now trades at a 5% discount to the Aussie dollar. So that $100 room in Aussie dollars will now cost you $105 U.S. dollars — a36% increase, even though the hotel’s rate didn’t change.

What does this have to do with increasing dividends? Well, what’s bad news for your vacation is great news for your international income investments.

Say you bought an Australian company five years ago that paid a dividend of 10 Australian dollars each year. Back then, you would have earned $7.70 in U.S. dollars after conversion.

But today, that same 10 Aussie dollar dividend would be worth $10.05 in the U.S… or 31% more.

The bottom line is if the U.S. dollar weakens versus other major foreign currencies, then your dividends will increase over time… even if the company you invest in keeps its dividend payment the same.

The best news is that despite a recent rally, I see the downtrend in the dollar continuing over the long-term. That will help investors looking abroad.

And I’m not the only one who thinks this:

|

“The dollar is enjoying a safe-haven status, but long run I’m not a fan of the U.S. dollar. Our country has too many problems.” “The dollar rally is overdone.” “While I am now short-term bullish on the dollar, there is still dollar weakness in the long-term.” |

But it’s not just dividends that benefit from a falling dollar when you invest abroad. Every dollar you invest sees the effects as well.

Recognizing this trend years ago — and investing alongside it — has already given international income investors a major boost.

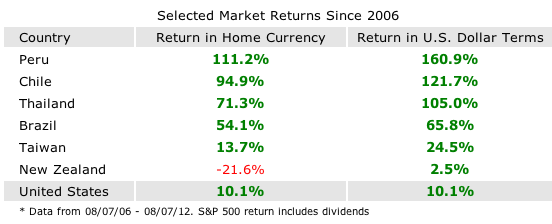

You can see for yourself how the falling dollar has helped score some great returns in international markets…

This table makes it easy to see how a falling dollar actually helps… if you’re invested abroad.

Notice that the New Zealand market actually declined over the past five years when measured in New Zealand dollars, but it’s showing a gain for U.S. investors when you factor in the falling U.S. dollar.

Now keep in mind, if the dollar were to rally, the opposite would happen. Your returns and dividends would lessen by the amount the dollar strengthens. And while the dollar has rallied recently — for a variety of reasons I won’t bore you with today — I think the U.S. dollar will continue to lose value in the coming years.

That gives income investors plenty of time to take advantage of this unique opportunity.

And in my opinion, there’s no easier way right now to boost your profits. Especially since you can own many of the world’s highest yielders without even leaving the U.S. markets.

For more on international dividend-payers, I invite you to watch my latest presentation. I’ve included names and ticker symbols of the 17 American companies that yield more than 12% (some as high as 19.7%) and several high-yield international plays. Visit this link to watch now.

Good Investing!

Paul Tracy

StreetAuthority Co-founder, Chief Investment Strategist — Top Ten Stocks, High-Yield International

P.S. — Don’t miss a single issue! Add our address, Research@DividendOpportunities.com, to your Address Book or Safe List. For instructions, go here.

Disclosure: In accordance with company policies, StreetAuthority always provides readers with at least 48 hours advance notice before buying or selling any securities in any “real money” model portfolio. Members of our staff are restricted from buying or selling any securities for two weeks after being featured in our advisories or on our website, as monitored by our compliance officer.

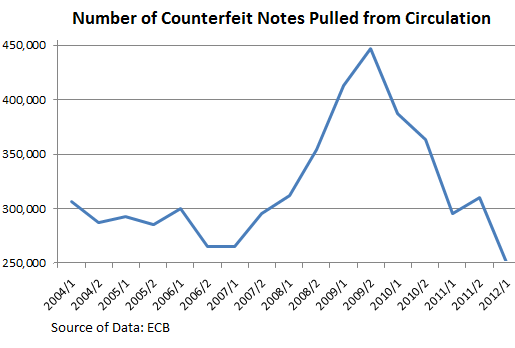

After a fairly steady period through 2006, euro counterfeiting jumped 70% to its peak in the second quarter of 2009. Alas, following on the heels of the financial crisis, the Eurozone debt crisis began to gnaw on periphery countries, and counterfeiters lost confidence along with the rest of the financial markets. By the first half of 2012, counterfeiting had crashed 44%. And not much but thin Alpine air appears to be underneath it.

The fact that counterfeiters are throwing in the towel—worried perhaps that they’ll get stuck with high-risk but unsalable merchandise—is bad enough for Europhiles. But now we see an increasingly clear demarcation of the Eurozone into two separate parts, though not entirely along the lines of North and South often envisioned.

On one side of the line are countries whose governments can borrow at negative yields, that is, where investors agree to lend money to them at a guaranteed loss, however absurd that might have seemed not long ago. That club includes Germany, France, the Netherlands, and Belgium (!); in the secondary markets, Finnish and Austrian government debt has seen negative yields. Eurozone neighbors Denmark and Switzerland also dipped into negative yields. Negative Interest Rate Policy (NIRP) at work.

On the other side are countries whose governments have lost access to the financial markets or are in the process of losing access. The largest two in that group are Spain and Italy.

THE WORLD IS HURTLING TOWARD A DAY IN WHICH MONEY WILL AGAIN BE BACKED BY GOLD OR OTHER HARD ASSETS. UNTIL, THIS ANALYST SEES PLENTY OF TROUBLE.

“Hear Me Now, Believe Me Later,” was the title of two separate and prescient pieces penned by Pomboy, an economist and founder of the MacroMavens research boutique. One, published in March 2006, foretold the disastrous costs of the housing bubble. The second, somewhat later, laid out the consequences of the bubble’s “financial echo.” Today, Pomboy predicts something more draconian: the demise of fiat money—currencies that aren’t backed by anything other than government decrees that they have value.

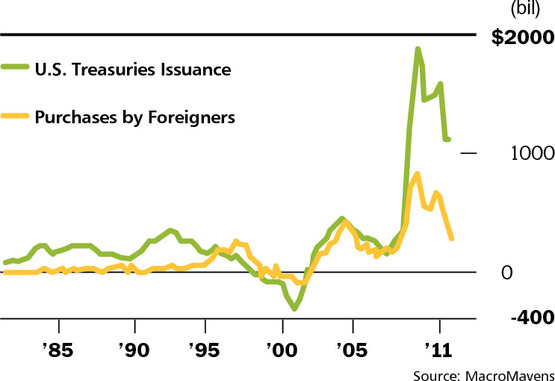

We checked in with her last week, as central banks around the globe weighed more easing and as Fed chief Ben Bernanke described to Congress the headwinds facing the U.S. economy, including the automatic tax increases and spending cuts set for year end, called the “fiscal cliff.” With the Fed being the biggest buyer of Treasuries, Pomboy thinks the 40-year-old fiat system will crack within five years.

Barron’s : What don’t investors anticipate today?

Pomboy: That the Fed will be a presence in the Treasury market for a long, long, long time. Some believe that, with another round of quantitative easing, we move forward, emerge from the morass, and the need for further intervention will dissipate. But the Fed is really the only natural buyer of Treasuries anymore. It will have to continue to monetize Treasury issuance at the same time all the other major developed economies—from the Bank of Japan to the Bank of England to the European Central Bank—are doing the same. Pursue that to its natural conclusion, and you see the inevitable demise of fiat money. To look at our policies and not be concerned about the risks to our currency would be dangerously naive.

One step at a time. When is the next round of QE?

….read her answer and much more HERE

The first chart below shows the strong US dollar. The US dollar is the mirror twin of the euro. As a rule, a strong dollar works against gold. The stronger the dollar, the fewer dollars it requires to buy an ounce of gold; and the opposite is true, the weaker the euro, the more euros it takes to buy an ounce of gold. This is the reason my pen-pal, Dennis Gartman, buys his gold in euro terms.

Below we see gold, and what is so interesting is that gold is holding above support at 1535 in the face of the strong dollar. This is obviously good action in terms of gold.

Just for the hell of it, I’m showing a daily chart of the euro. I think it’s over-priced at 1.22, and I think it’s going to par against the US dollar. I saw enough of Europe during WWII, and with the euro at 1.23, I’m staying in La Jolla where I can still get a meal for less than six bucks. The euro came out at 87 cents, which is what I think it’s really worth.

Ed Note: Richard Russell of Dow Theory Letters is bearish the US Stock Market based on the Dow Theory. His advice to investors right now it that: “This is the time to cut back on needless expenses — get rid of all the debt you can, and prepare for tough times”.

Russell began publishing Dow Theory Letters in 1958, and he has been writing the Letters ever since (never once having skipped a Letter). Dow Theory Letters is the oldest service continuously written by one person in the business. One of the favorite features of the Letter is Russell’s daily Primary Trend Index (PTI), which is a proprietary index which has been included in the Letters since 1971. The PTI has been an amazingly accurate and useful guide to the trend of the market, and it often actually differs with Russell’s opinions. But Russell always defers to his PTI. Says Russell, “The PTI is a lot smarter than I am. It’s a great ego-deflator, as far as I’m concerned, and I’ve learned never to fight it.”

Quote

“All war is based on deception. “ -Sun Tzu

Of Interest – Spanish not exactly loving austerity (Bloomberg)

Commentary

Expectations for China’s GDP growth were 7.6% and “magically” the number came in at 7.6% (lowest in three years). Do you sense the sarcasm in my writing voice?

Analysts noted that electrical usage in the country suggested real economic activity was likely lower than reported. We’re going with the electrical grid numbers instead of those massaged reported. Why? China’s satellite country, aka Australia, is showing signs China’s demand is fading; it reported a decline in June payrolls. We believe the Reserve Bank of Australia will act to lower interest rates. Normally, you might expect that would be good news for Australian stocks, but in a world still driven by hot money liquidity flows it may not be.

Action

As you can see, the three price series—RBA Cash Rate, Australian $- USD, and MSCI Australian Stock Index (EWA)—seem quite positively correlated from a monthly perspective.

We believe the RBA Cash Rate expectations is the driver of this pack. A cut in interest rates in Australia represents growth concerns, represents falling yield differential for the Australian dollar, and triggers money, a lot of hot money intially there for yield, to flow out. At least that is the attempt to link the movement of the price series togther, and we think it makes sense. Remain short EWA.

Be sure to listen to Michael Campbell interview Jack Crooks tomorrow on CKNW 980 @ 9:am PST Saturday June 14th/2012

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair