Currency

Quotable

“We know from chaos theory that even if you had a perfect model of the world, you’d need infinite precision in order to predict future events. With sociopolitical or economic phenomena, we don’t have anything like that.”

–Nassim Nicholas Taleb

Commentary & Analysis

The Fed’s Fake News: Inflation Risks. Buy bonds!

It’s an interesting aspect of the human condition—clinging to our view despite the fact reality has already invalidated them. The Federal Open Market Committee seems to have this characteristic firmly embedded in its DNA.

To wit, today’s headline from Reuters:

Now, not to be too critical of this august body of Ph.D.-laced economists, but if you are on the Federal Open Market Committee it seems you should be aware of the latest research that shows increased fiscal spending when debt-gdp levels are already high doesn’t lead to inflation; but in fact adds to deflationary pressures for the economy.

I place into evidence the following from Hoisington Research; a fixed income investment rd management firm who is arguably the best bond manager in the world. This is from their 3 Quarter 2016 Economic Review and Outlook:

Fed policymakers agree Trump fiscal boost poses inflation risk

WASHINGTON, Jan 4 (Reuters) – Almost all Federal Reserve policymakers thought the economy could grow more quickly because of fiscal stimulus under the Trump administration and many were eyeing faster interest rate increases, minutes from the central bank’s December meeting showed.

If new fiscal measures are enacted, debt-to-GDP ratios will be increased and will further depress growth, thereby causing interest rates to move lower, not higher. In a highly incongruous development, governments will therefore be able to finance their new debt offerings at lower costs. While this may seem to be a good thing for the individual governments, the great majority of their constituents will be harmed. The higher debt will set off a chain reaction of unintended consequences. The 70-75% of the households that receive the bulk of their investment income from interest bearing accounts will have fewer funds for retirement. This, in turn, will cause older members of the workforce to work longer and save more, blocking job opportunities for new entrants into the labor force. Thus, fiscal decisions, which result in higher deficits, are likely to perpetuate and intensify our underlying economic problems.

Impressive scholarly research has demonstrated that the government spending multiplier is in fact negative, meaning that a dollar of deficit spending slows economic output. The fundamental rationale is that the government has to withdraw funds, via taxes or borrowing, from the private sector, to spend their dollars. When that happens, the more productive private sector of the economy has fewer funds to use to make productive investments. Thus the economy slows along with productivity when government spending increases.

*************************************************************************

If you are seeking excellent independent trading ideas covering the key global asset classes, you have found it in our Key Market Strategies service. At $89 per year, most all of our subscribers would tell you it’s a massive bargain. That bargain now is only going to get better, as we are adding coverage of key futures markets in addition to the ETFs we presently cover. But we are also raising our price for the service, accordingly. So, between now and the first week in 2017 you have a chance to subscribe at our current price of $89 per year and be grandfathered in to the service no matter future price increases (as are our current subscribers). So, subscribe today to Key Market Strategies and don’t miss another good idea. Plus, we are putting the finishing touches on our 2017 Forecast Issue covering stocks, bonds, gold, oil, and currencies. Don’t miss it.

This offer expires on Sunday, January 7th. Our 2017 Forecast issue for stocks, bonds, gold, oil, and the major currency pairs is due out tomorrow. And we plan to offer a live webinar next week for subscribers only to discuss this forecast and take questions.

**************************************************************

Let’s face it. There will be disappointment when it comes to the Trump agenda. The Democrats will do all they can to block key parts; and maybe some of Trump’s own party will throw up a few roadblocks. And even if enacted, the benefits of tax cuts and regulation (which is where the benefits flow to the real economy) will take time to flow through. In addition, much of the benefits

Black Swan Capital’s Currency Currents is strictly an informational publication and does not provide personalized or individualized investment or trading advice. Commodity futures and forex trading involves substantial risk of loss and may not be suitable for you. The money you allocate to futures or forex trading should be money that you can afford to lose. Please carefully read Black Swan’s full disclaimer, which is available at http://www.blackswantrading.com/disclaimer

will likely be overwhelmed by existing debt levels and the increased drag from Trump’s infrastructure plans.

So, buy bonds. If the Fed is forecasting inflation, what better contrary indicator do you need?

TLT (iShares 20+ Year Treasury Bond ETF) daily wave view:

Jack Crooks

President, Black Swan Capital

The only thing about international trade is that someone cannot have a trade surplus without another experiencing a trade deficit. We all cannot have trade surpluses simultaneously and we have to begin understanding this reality. The net capital movements around the world are showing clear signs that things will be intensifying and the net capital movement is headed for the dollar – but that does not mean day one. Sure, many will point the finger at Trump and blame him for a trade war etc., but in reality, the net capital movements are intensifying for reasons that have nothing to do with trade. Ushering in Trump will also have a profound impact upon Europe and now Merkel’s greatest challenge will be to hold the EU together for its core design was to enhance German trade by eliminating currency risk.

The only thing about international trade is that someone cannot have a trade surplus without another experiencing a trade deficit. We all cannot have trade surpluses simultaneously and we have to begin understanding this reality. The net capital movements around the world are showing clear signs that things will be intensifying and the net capital movement is headed for the dollar – but that does not mean day one. Sure, many will point the finger at Trump and blame him for a trade war etc., but in reality, the net capital movements are intensifying for reasons that have nothing to do with trade. Ushering in Trump will also have a profound impact upon Europe and now Merkel’s greatest challenge will be to hold the EU together for its core design was to enhance German trade by eliminating currency risk.

The insane policies of Angela Merkel combined with.…continue reading HERE

….also from Martin:

Gold has suffered recently in the wake of higher real interest rates while the US Dollar, thanks to higher yields has reached a 14-year high. Stronger real rates hurt Gold but so does a stronger US Dollar, which remains the dominant global currency. In addition to falling real interest rates Gold likely needs the US Dollar to approach a major peak. It may sound perverse to gold bugs but the sooner the US Dollar climbs and the stronger it gets, the closer Gold could be to the start of a new bull market.

Gold is now officially in its longest bear market ever. If we define a bull market as a multi-year advance then Gold has endured five bear markets over the past 45 years. Four of the five are plotted in the chart below. The current bear market has followed the trajectory of the 1987-1993 and 1996-2001 bears but with more downside.

Gold Bear Analog

Although Gold’s current bear market is the longest ever, its counterpart, the US Dollar is not yet in its longest bull market ever. It would need to rise for nearly another year to achieve that feat. The chart below shows that this run in the greenback has more room to rise. The trajectory of the current bull has closely mirrored that of the 1978 to 1985 bull. If that continues then the US Dollar index could reach 110 in the first half of 2017 and 120 by the end of the year.

US Dollar Index Bull Analog

The two major peaks in the US Dollar (1985 and 2001) coincided with important lows in Gold. However, it is important to note that essentially all of the price damage to Gold during the corresponding bear markets occurred well before the US Dollar peaked. The chart below was inspired by an article from ReadTheTicker. After Gold’s bottom in 1982, the US Dollar surged 37% but Gold only penetrated its previous low by 5%. From Gold’s low in 1999 the US Dollar advanced 17% while Gold did not make a new low.

US Dollar Index & Gold

The bottom line is Gold could be setting up for an epic bottom when the US Dollar becomes strong enough to cause global problems and induce policy more favorable to Gold. History shows that the majority of price damage in Gold bear markets has occurred in the earlier stages of US Dollar bull markets. A higher US Dollar will certainly push Gold lower from here but probably not too far below the 2015 low. A precursor to Gold’s turn will be when it shows strength against foreign currencies and equities while the US Dollar is rising.

We reiterate that we do not want to buy a bunch of investment positions until we see sub $1100 Gold coupled with an extreme oversold condition in bearish sentiment. We certainly see bearish sentiment and some good values in the gold stocks at present. However, some of these good values could become great values before next summer. For professional guidance from Jordan go HERE

Jordan Roy-Byrne, CMT, MFTA

Back in March 2008, as the Credit Crunch was biting, the US Dollar, as measured by the US Dollar Index (USDX), was bottoming after a drop of over six years fuelled by the War on Terror. Silver had previous topped out at about $21 and was later to visit $50 as the dollar faced the abyss again just above the 70 level. To date, that level has been the all time low for the USDX.

Looking at the 45 year chart for the USDX, it is clear the dollar has been on a downward trajectory interspersed with some rallies since 1985. As of 2008, the dollar has been in an 8 year rally. It is no coincidence that gold and silver have struggled during this time and precious metal investors will be wondering when the dollar will resume its 31 year bear?

While writing for subscribers on the US Dollar, another look at the USDX chart suggested that the dollar bull was beginning to outstay its welcome. Lines have been drawn between each high and low to highlight each dollar bull and bear.

Let us tabulate these ups and downs below. As you can see, the USDX has experienced three bulls and three bears since 1971. What is interesting are the similarities in durations ranging from six year and four months to eight years and ten months. The average is 2798 days or seven years and eight months.

|

BEGIN |

END |

DURATION |

MOVE |

|

4th Jan 1971 |

31st Oct 1978 |

7Y 9M 28D (2858d) |

-32% |

|

31st Oct 1978 |

28th Feb 1985 |

6Y 4M 1D (2313d) |

+100% |

|

28th Feb 1985 |

30th Sep 1992 |

7Y 7M 3D (2772d) |

-47% |

|

30th Sep 1992 |

31st Jul 2001 |

8Y 10M 2D (3227d) |

+56% |

|

31st Jul 2001 |

31st Mar 2008 |

6Y 8M 1D (2436d) |

-42% |

|

31st Mar 2008 |

16th Dec 2016 |

8Y 8M 17D (3183d) |

+44% |

As this current dollar bull stands, it is now been on the go for eight years and eight months, which is one year above the average and two months off the longest ever bull. In other words, I would say this dollar bull is getting long in the tooth and will soon be replaced by a dollar bear which will run for an average of seven years and eight months.

What are silver and gold going to be doing during this approaching dollar bear? I would say the odds favour them heading strongly up within that time period.

What are the fundamentals of this cyclical prediction? I don’t know and I have no idea why the dollar should flit in and out of these 6-8 year cycles. But as for the next dollar bear, my bet is that a Trump administration is going to indulge in a dollar depreciation program that is not based on welfare or warfare, but rather heavy infrastructure spending which I shall call wall-fare in honour of that long structure he plans for the Mexican border.

…related: US Dollar & Gold

A free sample copy of our our silver blog at http://silveranalyst.blogspot.com can be obtained by emailing silveranalysis@yahoo.co.uk.

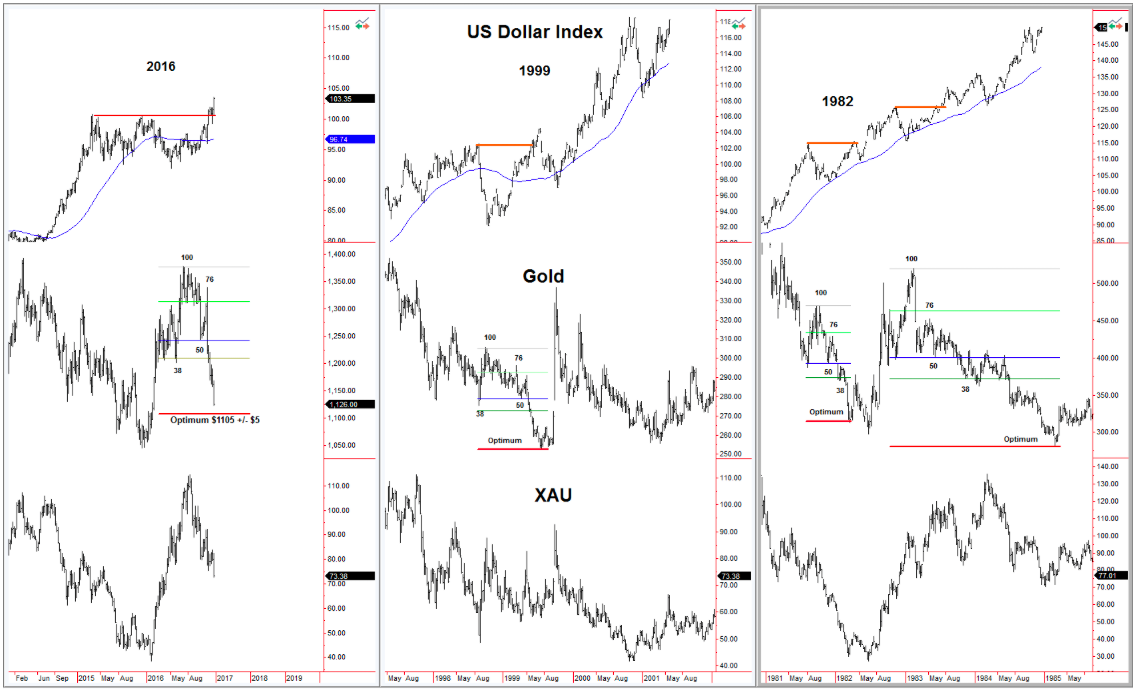

We continue to monitor the seventeen-year cycle in the US Dollar Index and its relationship with gold. Looking at gold since the Dollar bottomed in May, the patterns of 1999, 1982 and 1983-85 are a close match. The Fibonacci levels come into play in each instance.

The October 7th low at $1242 (labelled level 50 on the chart) was the last support before gold broke the May 31st low of $1199. It is deemed to become the midpoint of the eventual decline. The resistance level at 76% was a test of the previous support around $1310 during the summer. April and May become the 38% level in the pattern. The measured range for the downside move is $1105 +/- $5.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair