Currency

China’s economy and markets have been defying the laws of economics since 2009. Amid a worldwide financial crisis during that year, they managed to grow their economy by 8.7%. But that growth was fueled by a $586 billion dollar government stimulus package, which was followed by an additional $20 trillion dollars in new construction spending over the next seven years.

China’s economy became the envy of the world as the economy expanded through the edict of government to build massive cities that were mostly vacant. In fact, estimates are that 52 million homes in China are currently vacant and 90% of those empty units were purchased for investment purposes.

As investors sat on empty real estate, debt levels in the shadow banking system rose to troubling levels. A real estate bubble of this magnitude would bring most economies to the brink of destruction. But fear not; the megalomaniacs in Beijing had a solution: in 2015 they created a new bubble in the stock market to offset the fragile real estate bubble.

And to accomplish this, 40 online brokerage lenders helped arrange more than 7 billion yuan worth of loans for stock purchases.

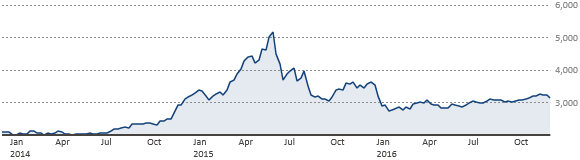

As you can imagine, China’s leverage problem quickly reached epic proportions. Fueled by margin debt the Shanghai Composite (SSE) started 2015 at 3,234 and hit 5,023 by June 4th; a 150% surge from the preceding 12 months, before plunging.

Shanghai Index:

With markets in free-fall, the totalitarian regime made daily policy modifications in a desperate attempt to stop the bleeding. Surprise interest rate cuts by the central bank, relaxations in margin trading and other “stability measures” did little to calm investors’ angst. But eventually, the central planners stepped in and stemmed the market’s decline.

However, the nation was far from out of the woods. Once a model of fiscal prudence, China became a country swimming in debt and asset bubbles. China’s corporate debt levels are now over 150% of its GDP, and estimates of total debt are as high as 280% of GDP.

Consumer credit has grown by over 300% in just the past six years. In October of 2015, debt levels for consumers hit 23.5 trillion yuan ($3.41 trillion). The expectations are that this will more than double by the end of 2020, reaching nearly 53 trillion yuan ($7.66 trillion).

The nation has now reached a 10-year high in delinquent corporate loans. Bloomberg reports that China has had nearly three times the number of defaults recorded in 2015.

Even the International Monetary Fund (IMF) is beginning to wave the warning flag that failing to act quickly to rein in corporate debt could prove detrimental to both China’s economy and the world as a whole.

Of course, supporting the rotating carousel of real estate, commodity, and stock bubbles, while also trying to stem bond defaults, comes at a cost. All of that debt and money creation usually results in a decimated currency. However, China uses its currency reserves (held mostly in dollar denominated Treasuries) to keep the value of the yuan from falling too quickly. But what had once been China’s get out of financial crisis free card–their immense foreign exchange reserves–is dwindling at an alarming rate.

November’s severe drop in reserves marked the fifth straight month of declines and are at the lowest level since March 2011. In fact, Japan just superseded China as the largest holder of U.S. sovereign debt.

IMF guidelines put $2.8 trillion as the minimum prudent level for China to hold in reserves–it is closing in on that level at the current pace. The yuan fell to an 8-1/2-year low in November and has dropped 6% against the dollar so far this year despite the government’s efforts.

Adding to pressure on the yuan is the newly elected U.S. president, Donald Trump, who has threatened to label China as a currency manipulator on his first day in office and impose huge tariffs on imports of Chinese goods. Pushing even further down on the yuan are the threatened three Fed rate hikes scheduled for 2017.

In January, Chinese citizens will get an even lower quote from Beijing for exchanging their local currency into foreign dollars. Yes, China’s government even tries to dictate the exact value of its currency. Many believe this will create a repeat of the market chaos that ensued at the start of 2016, as capital outflows surge.

Scotiabank Vice President of Economics, Derek Holt, believes these fears are warranted. He said in a recent article: “Why wouldn’t they convert like there is no tomorrow?” … “After another year of yuan depreciation, would you keep your life savings in a currency that is losing international purchasing power and within a banking and shadow finance system that gets all manner of negative headlines?”

Therein lies China’s dilemma: Allow the yuan to intractably fall, which will increase capital flight and destroy its asset-bubble economy. Or, raise interest rates to stabilize the currency and risk collapsing asset bubbles that will crumble under the weight of rising debt carrying costs.

China embodies a Keynesian dystopia that results from central planning gone mad. It’s mirage of prosperity should soon be coming to an unpleasant end. The misguided belief any government can print unlimited amounts of money and issue a massive amount of new credit; while providing the conditions that are the antitheses necessary for viable growth, has one significant Achilles heel: eventually, it will destroy your currency. Currency is always the pressure valve that explodes in an economy that has reached the apogee of dysfunction. The Red nation isn’t the only offender on this front, but is certainly one of the worst. Therefore, China and the yuan may have finally run out of time.

….also Live From The Trading Desk with Michael Campbell & Victor Adair: US Dollar Powers To a 14Yr High

Victor on the recent collapse in Precious Metals that motivated him to cover his short position. More on the CDN Dollar, 14 yr high in the US Dollar, 14 yr low in the Euro, Stocks, Bonds and a market that has made a big move producing a big opportunity – Crude Oil

….Michael’s Shocking Stat: Astonishingly Large Numbers Courtesy of Youtube

Over the past year, central banks, commercial bankers and prominent economists have expressed the view that digital money and transfers should replace large denomination cash and cash transactions. This dramatic transition has been fostered under the guise of the public interest in an effort to curb terrorism, tax evasion and criminal activity. Many observers contemplate more sinister motives that involve increased government control of economic activity. The latest country to engage in this ‘war on cash’ is India.

Over the past year, central banks, commercial bankers and prominent economists have expressed the view that digital money and transfers should replace large denomination cash and cash transactions. This dramatic transition has been fostered under the guise of the public interest in an effort to curb terrorism, tax evasion and criminal activity. Many observers contemplate more sinister motives that involve increased government control of economic activity. The latest country to engage in this ‘war on cash’ is India.

In a TV announcement on November 8th, India’s Prime Minister Narendra Modi announced that the Reserve Bank of India’s large denomination 500 and 1,000 rupee bank notes, worth some $7.5 and $15 respectively, would lose their status as legal tender on midnight on December 31, 2016. That meant holders of those notes (which represent 86 per cent of the value of all outstanding rupee notes) had less than two months to exchange the notes for smaller new notes, or lose out completely. The government also mandated than any large exchanges had to be accompanied by tax returns in order to prove that the cash generated had already been taxed.

The shock waves from this announcement fueled fear and panic among the Indian population which is heavily cash-oriented. As few people have bank accounts and banks are thinly spread in rural areas, many Indians have been left holding paper currency redeemable only in banks which often are difficult to access. To make matters worse, banks soon ran out of small denomination notes. The result was chaos, rioting and trauma-induced deaths. Millions of poor Indians were unable to buy necessities or transact business. Many merchant shops had no alternative but to close.

The BBC’s website notes that India, the world’s seventh largest economy “…is overwhelmingly a cash economy, with 90% of all transactions taking place that way.” At a sudden single stroke a socialist Prime Minister has converted most of the nation’s private cash into bank deposits subject to direct governmental controls including spending and withdrawal limitations. Furthermore, the new bank deposits can be leveraged up as bank loans to government and to allow banks to purchase government bonds to finance social programs.

It remains to be seen how severely India will be hit and what effect it will have on the international economy. With much of the world focused on the U.S. Presidential election, this Indian currency event was little reported in the western media.

The Indian action was a largely unexpected escalation of the ‘demonetization’ movement that has been spreading through the U.S. and Europe. This past year, Larry Summers proposed the withdrawal of the $100 bill and the ECB announced an end to printing 500-euro notes. The idea has been supported widely. With the notable exception of The Wall Street Journal, major news media including The Economist, The New York Times and a recent Harvard paper have called for the elimination of high denomination currency.

It could hardly be coincidental that just this week Nicolas Maduro, the bumbling socialist dictator of Venezuela, surprised his nation with monetary changes that are nearly identical to those being pursued by India. The collapsing Venezuelan economy already had the highest inflation rate in the world, and its starving citizens have had to transact what little commerce they can with ever larger stacks of nearly worthless currency. But to add insult to injury, Madura just deactivated the 100 Bolivar note, the country’s largest note denomination, which until recently had a value of just 3 U.S. cents. Although the government predictably claimed that the move was aimed at speculators and foreign capitalists, it will be the poorest Venezuelans who will suffer most acutely.

As in India and Venezeula, the reasons given for the elimination of cash is to protect citizens from terrorism, tax evasion and crime. Of course, when all financial transactions have to flow through banks, they can be monitored easily. Undoubtedly this does hinder some aspects of terrorism, tax evasion and crime. But the real reasons for demonetization are given far less oxygen. The move is spurred by the need to protect the ever larger “too big to fail” banks and the ability of governments to control and even legally utilize the private wealth of citizens. Cash can be sheltered from government, bank deposits cannot.

The advent of zero and negative interest rates has reduced investment reward and resulted in a tax on savings. In a low, or negative, rate environment, those with cash have little if any financial incentive to hold money in banks. Cash hoarding is the logical alternative. In economic terms, hoarded cash becomes dead money. Outside the system it contributes nothing to economic activity. Specifically, it deflates the velocity of monetary circulation, a vital element of economic growth. Perhaps more importantly to a technically insolvent banking system, deposits withdrawn from banks, especially when combined with a rising rate of non-performing loans, can result in potentially fatal capital shortages. In today’s over-leveraged and derivative-infused financial markets, a serious banking failure could escalate like lightning and threaten the entire international financial system.

In their 2015 rescue of Cypriot banks, the IMF, ECB and western politicians effectively devised the ‘bail-in’ as a new, less visible alternative to politically unpopular citizen bank bailouts. In a bail-in, it is the shareholders, bondholders and, ultimately, bank depositors who are called upon to fund an insolvent bank rather than injecting public funds. Despite the precedent of Cyprus, it remains surprising how many citizens remain blissfully unaware that when they open an account, they become creditors of the bank. Despite retaining rights to the funds, they no longer own the monies.

In addition, if excessive government borrowing results in a collapse of government bond markets and a potentially crippling rise in interest rates, legislation mandating that each citizen hold a certain percentage of their wealth in government bonds would not be unrealistic. With digital money, bank computers can execute such commands quickly and easily. The depositor has no recourse other than the ballot box.

While cash hoarding may offer added security to cash holders, as dead money it results in politically harmful damage to economic growth rates rendering banks more vulnerable. It follows that the increasingly ferocious and aggressive war on cash is a sign that central banks may see a dangerously deteriorating situation, one that has led to a feeling of desperation by governments and a strong wish to establish a legal means to control the wealth of citizens. They appear to be using political statements by banks, economists and the mass media to secure a meek surrender to a cashless society and the potential utilization of citizens’ accumulated cash wealth by legal means.

Cash is an efficient, free, and private means of payment for ordinary citizens, particularly those without the funds to pay ever-increasing bank charges. Following the January 2016 World Economic Forum in Davos, the war on cash appeared to intensify. At that meeting, PayPal’s CEO, Dan Schulman, claimed that 85 percent of transactions, by volume rather than by value, are in cash. Regardless, at the same conference, Deutsche Bank co-CEO, John Cryan, described cash as “terribly inefficient.” He predicted that we would “probably” see no more cash within the next ten years.

Already, some major countries have limited cash transactions for law abiding citizens. In Italy, the legal limit for cash purchases is some $1340, in France the limit is 1,000 euros. Even in the UK, any cash transaction above some 15,000 pounds must be reported to the Inland Revenue. In the U.S., the mandated reporting figure to the Internal Revenue Service is $10,000.

Some notably highly leveraged banks including Deutsche and UBS have called for the elimination of cash, while Citibank has eliminated cash in some of its Australian branches. As early as 2015, JPMorgan Chase warned that it would no longer accept cash in its safe deposit boxes. Separately, Chase said it was restricting cash payments for credit cards, mortgages, equity lines and auto loans.

The Indian government’s capture and compulsory transfer into bank accounts of some 86 percent of its citizens’ cash was a shock to Indians and to informed people around the world. It will be studied for lessons learned by the western nations as they pursue their own wars on cash. Likely they will take a more gradual approach, supported by mass media and senior bankers’ statements to support their assaults on the cash of compliant citizens. Whereas recently impoverished Indians may turn to silver, those in the developed world may look increasingly to gold as a store of wealth.

The extent and speed of the exercise of governmental power to restrict the use or to control the accumulated wealth of citizens never should be ignored or underestimated.

Quotable

“I saw a report yesterday. There’s so much oil, all over the world, they don’t know where to dump it. And Saudi Arabia says, ‘Oh, there’s too much oil.’ They – they came back yesterday. Did you see the report? They want to reduce oil production. Do you think they’re our friends? They’re not our friends.”

–Donald Trump

Commentary & Analysis

The oil currency—Norwegian Krone; is it undervalued? Hmmm…

The krone is an oil currency. The currency tends to track very closely with the price of oil over time. It makes sense given Norway’s dependence on oil as an economic driver. But lately, we have seen a divergence in the two prices—oil and Krone/USD, as you can see clearly in the chart below:

Another way of looking at this Krone versus oil relationship over the longer term is by look at the ratio (calculated by dividing NOKUSD by WTI oil futures price). As you can see below, this ratio is anything but stable over the longer term [the ratio would be an interesting play in its own right]. The decline in the ratio is telling us oil has become relatively more expensive when priced in NOK/USD.

I am not sure what these charts are telling us. But it’s likely they are telling us different things depending on the time frame we choose. Near-term it seems the divergence in the first chart above presents a trading opportunity; longer term if one believes the US dollar will continue to rally over the next couple of years, and oil prices at least remain stable, the NOKUSD – Oil ratio could go a lot lower.

If we keep our focus over near-term time frame; here are three thoughts or considerations:

1) NOK/USD is telling us the oil move is limited: i.e. crude prices have spiked on OPEC deal sentiment (though adherence to said agreement is still suspect); but global supply data still suggest there is a lot of oil out there; indicating a $50 oil price may not be sustainable given still suspect global demand. I am not just thinking about all those tankers filled with crude parked offshore, I am thinking about a vast new supply coming on stream should a President Trump unleash the US domestic oil and gas industry.

2) The krone is considerably undervalued relative to oil: Given the huge run we have seen in the US dollar lately, maybe this move in the Krone is a near-term anomaly only—and the divergence displayed in the chart on page 1 above is about to be closed (thus this is all about the US dollar and not oil).

3) Even if it’s all about the US dollar; a window will open for the swift: Though I keep touting this idea, which increasingly is becoming suspect to reality, even in bull markets there is usually time made for a correction in price. If the beginning of a dollar correction can be identified, and granted I have done a lousy job of doing that so far proving it is dangerous to fade a trend, the krone may be a screaming buy against the US dollar. This will be especially true if oil rallies on a weaker US dollar (something that used to happen during the last cycle day after day).

But no matter what we say now or how we view these charts, the longer term will likely be defined by the Trump agenda, and even if we know the agenda, it only gets us part way there. I say that because there is the usual tug-of-war in play here (consider it the natural feed-back loop so common in market prices).

Should President-elect Trump be able to get his policies through congress, it does setup the potential for a virtuous circle of global capital flow into the US (as I discussed on the most recent Currency Currents (12/3/16) posted at our blog); potentially driving the US dollar higher for years to come. Same token, Trump’s policies, as indicated, could unleash a huge amount of energy supply onto the market. The question then becomes: Will the expected economic growth from Trump-ism create enough demand to soak up all the increased supply of oil?

Once again, unless we are visited by Mr. Market Hindsight anytime soon, none of this will be easy to sort out ahead of time. That said, at least over a speculator’s normal time frame, the Norwegian Krone could be setting up for a great trade. Stay tuned.

**********************************************************************

Free Trial all Black Swan subscription-based services

*************************************************************

Have a great week.

Jack Crooks

President, Black Swan Capital

All of the World’s Money and Markets in One Visualization

All of the World’s Money and Markets in One Visualization

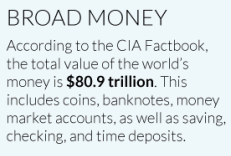

How much money exists in the world?

Strangely enough, there are multiple answers to this question, and the amount of money that exists changes depending on how we define it. The more abstract definition of money we use, the higher the number is.

In this data visualization of the world’s total money supply, we wanted to not only compare the different definitions of money, but to also show powerful context for this information. That’s why we’ve also added in recognizable benchmarks such as the wealth of the richest people in the world, the market capitalizations of the largest publicly-traded companies, the value of all stock markets, and the total of all global debt.

The end result is a hierarchy of information that ranges from some of the smallest markets (Bitcoin = $5 billion, Silver above-ground stock = $14 billion) to the world’s largest markets (Derivatives on a notional contract basis = somewhere in the range of $630 trillion to $1.2 quadrillion).

In between those benchmarks is the total of the world’s money, depending on how it is defined. This includes the global supply of all coinage and banknotes ($5 trillion), the above-ground gold supply ($7.8 trillion), the narrow money supply ($28.6 trillion), and the broad money supply ($80.9 trillion).

All figures are in the equivalent of US dollars.

About the Money Project

The Money Project acknowledges that the very concept of money itself is in flux – and it seeks to answer these questions.

The Money Project aims to use intuitive visualizations to explore ideas around the very concept of money itself. Founded in 2015 by Visual Capitalist and Texas Precious Metals, the Money Project will look at the evolving nature of money, and will try to answer the difficult questions that prevent us from truly understanding the role that money plays in finance, investments, and accumulating wealth.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair