Currency

The US dollar is up 10% since May when the Canadian Dollar made it high for the year. Victor on the huge moves in the currency markets, Gold, Stocks and interest rates and the 28% move in Copper in the last 5 weeks.

….also from Michael & Ozzie: The Hottest Properties Right Now

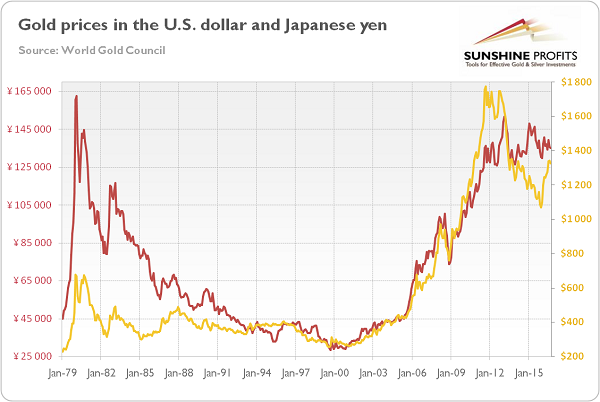

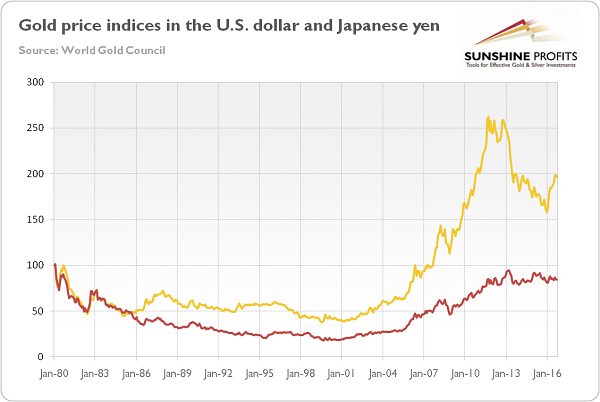

Our Market Overview would be incomplete without remarks about gold priced in the Japanese yen. Chart 1 shows nominal gold prices denominated both in the U.S. dollar and the Japanese currency, while Chart 2 plots the indices of gold prices in these two currencies.

Chart 1: The price of gold in U.S. dollars (yellow line, right axis) and in Japanese yen (red line, left axis) from January 1979 to September 2016.

Chart 2: Indices of gold prices in the U.S. dollar (yellow line) and the Japanese yen (red line), January 1980=100.

As one can see, gold prices denominated in the greenback and the yen often move together. There were only two significant divergences in the relative performance of gold priced in the U.S. dollar versus gold prices in the yen. The first case occurred in the 1980s, when the yen strengthened against the greenback, leading to strong declines in yen-denominated gold prices. The second case started in mid-2014. In the second half of that year, gold priced in yen has outperformed its dollar cousin due to the strength of the greenback against the yen and the decline in Japanese real interest rates. However, in 2016 the U.S. dollar depreciated against the Japanese currency, which led to the underperformance of the yen-denominated gold prices. The reason may be the Fed being more-dovish-than-expected and the rising conviction that the Bank of Japan has been approaching the limits of monetary easing. Indeed, the introduction of negative interest rates in January and changes in the monetary policy framework in September have largely failed to weaken the yen, as investors judged that these actions implied that the BoJ had little scope to ease policy further. Such a belief diminished the perceived divergence in monetary policies between the Fed and the BoJ, which supported the gold market this year. Let’s analyze the chart below which plots gold prices against the balance sheets of the Fed and the BoJ, showing the divergence in the monetary pumping.

Chart 3: The price of gold (yellow line, right axis, P.M. London Fix), the Fed’s balance sheet (green line, left axis, in $ million) and the BoJ’s balance sheet (red line, left axis, in 100 ¥million), from January 2003 to August 2016.

As one can see, there is no clear correlation between gold prices and central banks’ total assets. However, the price of gold entered the bear market period at the end of 2012 when the BoJ adopted a more aggressive stance associated with Abenomics and the growth of its monetary base accelerated.

Looking forward, we expect that the divergence in monetary policy between the Fed and the BoJ will persist, supporting the U.S. dollar. The divergence has receded somewhat this year as the Fed has dialed back expectations for the pace of rising interest rates, however it may return to the spotlight in December when the Fed may hike interest rates, while the ECB and the BoJ would probably continue to loosen their monetary policies. Indeed, the BoJ left the possibility of more asset purchases and further interest rates cuts – at the press conference after its September meeting, Kuroda said:

“We won’t hesitate to adjust monetary policy with an eye on economic and price developments. “We will ease further when necessary. We can cut short-term rates, lower the long-term rate target, buy more assets or if conditions warrant, accelerate the pace of expansion in monetary base. There’s room to ease further with the three dimensions of quantity and quality of assets as well as interest rates.”

It goes without saying that a strong dovish statement from the BoJ could weaken the yen and strengthen the U.S. dollar, which would be negative for the price of gold. In a scenario of the broadening divergence in monetary policy between the major central banks, investing in gold priced in the yen (or the euro) would be a smarter choice than investing in gold priced in the U.S. dollar. Naturally, there is only one “gold” that can be purchased and the above simply means that those who hold the euro or yen and use it for purchasing gold, will likely benefit more (vs. the value of these currencies) than those, who hold the US dollars.

Thank you.

Arkadiusz Sieron Sunshine Profits

….related:

The US$ oil price and the Canadian Dollar (C$) have tracked each other closely over the past 2 years. When divergences have happened they have always been eliminated within a couple of months, usually by the oil market falling into line with the currency market.

In a 25th May blog post I wrote that an interesting divergence had developed over the preceding few weeks between these markets, with the C$ having turned downward at the beginning of May and the oil price having continued to rise. This suggested that either the currency market was wrong or the oil market was wrong. As I stated at the time, my money was on the oil market being wrong. In other words, I expected the divergence to be eliminated via a decline in the oil price.

The oil price was $49 at the time. Over the ensuing two weeks it moved a little higher (to $51) and then dropped by 20% within the space of two months. The result was that by early-August the gap between the oil price and the C$ had been fully closed.

The oil price and the C$ then traded in line with each other for about 6 weeks before another divergence began to develop. Again it was the oil market showing more strength than was justified by the currency market, and by early-October it was again likely that there would be a gap-closing decline in the oil price.

As expected, there was a significant decline in the oil price from mid-October through to early-November. However, the following chart shows that the gap was only partially eliminated and that a rebound in the oil price over the past 1-2 weeks has potentially set the stage for another significant gap-closing move.

I won’t be surprised if the oil price trades a bit higher within the coming two weeks, but my guess is that it will drop to the $30s within the coming three months.

![]()

…more from Steve: The prices of US government debt securities have been falling since early-July and plunged over the past two weeks. This prompts the question: Where did all the money that came out of the bond market go?

The greenback has been on a tear as of late, rallying about 5.5% since the dollar index bottomed out just below 96 on election night.

In fact, the dollar index is up 10 days straight — the biggest surge since May 2015.

That puts the dollar at its best level in over 14 years.

Reasons: Simple …

FIRST, is all the flight capital leaving other countries and regions of the world that are in far worse shape than the U.S. Europe is going down the drain. So is Japan. So is the Middle East.

Plus, the more China opens up its currency market, the more yuan leave as wealthy Chinese get the opportunity to diversify and invest … and their main target is the U.S. of A.

SECOND, is that the dollar is now pricing in an inevitable rate hike from our Federal Reserve.

And THIRD, is general optimism over President-elect Trump’s policy of strongly desiring to repatriate the nearly $3 trillion of U.S. corporate money sitting overseas. A tax holiday of some sort is in the offing for that huge stash of cash and repatriating it would be hugely bullish for the dollar and for the U.S equity markets.

So it’s no surprise that my AI models have forecasted this rise in the dollar for some time now. And those same models are telling me that this trend should continue.

In fact, this chart clearly shows that the dollar index could easily continue moving higher heading into next year …

So, what does this all mean?

Most would argue that a stronger dollar may have significant financial, as well as trade, effects on emerging markets.

Reason: Many companies in these markets have borrowed in dollars. So the cost of repaying their debt rises when the greenback gains ground against their domestic currencies.

Plus, much of this borrowing is conducted through the banking system, leaving the banks exposed to the risk of a rising dollar.

In other words, a stronger dollar could cause a tightening of credit conditions in emerging markets — leading to slower growth.

The good news is that if the dollar continues rising — as I expect it will — emerging market exports become even cheaper. That can be a big driver of demand, sales and profits. And that means more growth globally and here in the U.S.

Unless President-elect Trump trashes trade deals and slaps tariffs on China and other countries that rely on exports. Then we’ll have a real mess on our hands, not unlike the trade wars of the 1930s.

For now, I recommend staying in dollars. Even if President-elect Trump starts to talk tough again on trade, it will be some time before anything concrete is decided.

Best wishes,

Larry

….related by Victor Adair: Huge Moves – Time to TipToe Short Term

The Dollar & Bonds market reaction to Donald Trumps election has been massive and the movements dramatic. Its time to step carefully depending on your time frame. Victor on the likelihood of a Fed interest rate move and the huge ETF sales in the Gold.

…related Dr. Michael Berry: The Fed is Throwing Up Its Hands

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair