Currency

Forex Trading Alert originally sent to subscribers on December 15, 2015, 11:26 AM.

Although the U.S. Commerce Department showed that consumer prices were unchanged from a month earlier, year-over-year consumer prices increased by 0.5%, beating expectations for a 0.4% gain. Additionally, core CPI (without food and energy costs) increased by 0.2%, meeting expectations and supporting the greenback. As a result, the U.S. dollar moved higher against its Canadian counterpart, but will we see further rally?

In our opinion the following forex trading positions are justified – summary:

EUR/USD

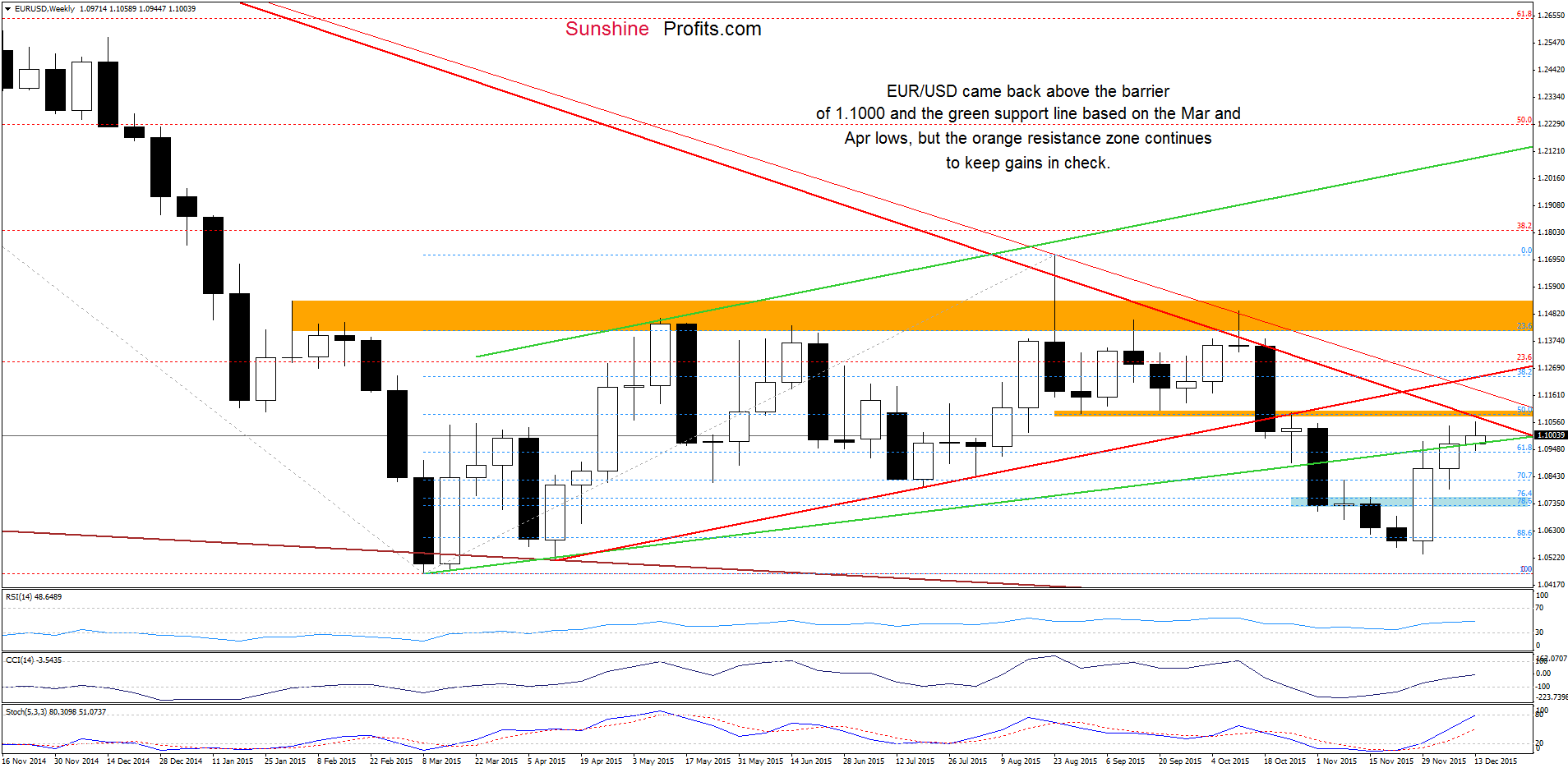

Looking at the weekly chart, we see that EUR/USD came back above the barrier of 1.1000 and the green line based on the Mar and Apr lows, but the orange resistance zone and the long-term red declining resistance line continue to keep gains in check.

Having said that, let’s examine the daily chart…..read more HERE

The massive bubble in US dollars is so obvious in this country

When I did the math in my head last week, I had to pull out my phone’s calculator just to make sure I hadn’t mentally misplaced the decimal point.

When I did the math in my head last week, I had to pull out my phone’s calculator just to make sure I hadn’t mentally misplaced the decimal point.

It turns out I was right. My rental car in Cape Town would cost me just $8/day. And that included all the silly taxes and fees and nonsense.

Eight bucks. I imagine that the car depreciates more than that.

The rest of my time here has been filled with similar awe.

Dinner for two at a high-class restaurant along the oceanfront promenade in one of Cape Town’s most luxurious neighborhoods set me back about $30.

And that included wine, multiple courses, taxes, tip, the whole nine yards.

Nearly everywhere I see here is shockingly cheap… when I convert to dollars.

Grocery stores sell giant bags of food—fresh plums and peaches, for less than a dollar per kilo, or about 40 cents per pound.

And of course, one of the reasons I came here to begin with is because Round-the-World flights starting in South Africa are dirt-cheap.

My itinerary has me traveling from here to Australia, Asia, South America, the US, Europe, and back to South Africa, all for about $5,500. In business class.

A deal like that is absolutely unheard of. And it all comes down to the local currency, the South African rand.

It wasn’t that long ago that the rand was valued at about 8 per dollar. I remember coming here not too long ago when the rand was 6.

Today it takes more than 15 rand to buy a single US dollar– record low territory for the South African currency.

And just last week, the rand lost more than 10% against the dollar.

In currency markets where price swings of 1% to 2% are considered chaotic, a 10% drop in a currency’s value is practically apocalyptic.

This makes South Africa one of the cheapest countries in the world right now, if you’re spending in US dollars.

What’s crazy is that South Africa is not alone. Currencies around the world are trading near record lows.

Colombia. Mexico. Kazakhstan. Nigeria. Indonesia. Turkey. Chile. Brazil. Sri Lanka. Iran.

This strikes me as truly bizarre. It’s not like the economic fundamentals of the United States, and the fundamentals backing the US dollar, are particularly strong.

The US dollar is issued by the Federal Reserve, a central bank that is nearly insolvent according to its own balance sheet.

And of course, the US economy is so ‘strong’ that the Fed has been agonizing for a year whether America is ‘ready’ for a 0.25% interest rate increase this week.

Moreover, the US government is in debt up to its eyeballs and also insolvent according to its own financial statements.

America’s national debt, in fact, exploded by $674 billion just last month. This is nearly twice the size of South Africa’s entire economy!

It’s pure madness to think that this is the ‘strong’ economy.

It makes no sense that a Big Mac costs $4.79 in the US, but the exact same Big Mac costs $1.60 in South Africa.

Or that a round-the-world ticket costs $14,000 in the US, but the exact same itinerary ticketed from South Africa costs only $5,500.

The US dollar is clearly in a massive bubble, while the rand is extremely undervalued.

And while it could take time, modern financial history shows this imbalance does tend to correct itself.

This does present a compelling opportunity right now to buy high quality assets overseas for next to nothing.

Or at a minimum, to enjoy an incredible lifestyle for a fraction of the cost, or to explore the world on a shoestring.

We have that ability today.

This valley where I spent the weekend about an hour from Cape Town was the destination of choice for French Huguenots who fled religious persecution.

When they came from France in the 1600s, they had to brave a treacherous journey across the world, risking disease, starvation, and pirates.

And that was just to get here.

Once they arrived they had nothing. Yet they built a brand new civilization from scratch, bringing with them all the best elements of their culture.

Just like in North American and Australia, early settlers realized that life wasn’t going to improve back home. And if they wanted access to better opportunities, they had to take big risks and look abroad.

Today we have it so much easier.

We can hop on an airplane and wake up on the other side of the world tomorrow morning.

We can access incredible financial opportunities and profit from the next great financial bubble, all without leaving our living rooms.

Despite all the idiots out there trying to start World War III, the world really is full of opportunity.

Whether you’re seeking a better, higher quality lifestyle at a fraction of the cost, or financial opportunities to make more money, it’s all out there.

And with much greater ease than our ancestors dreamed of. All it takes is the willingness to learn… and to take action.

Until tomorrow,

Simon Black

Founder, SovereignMan.com

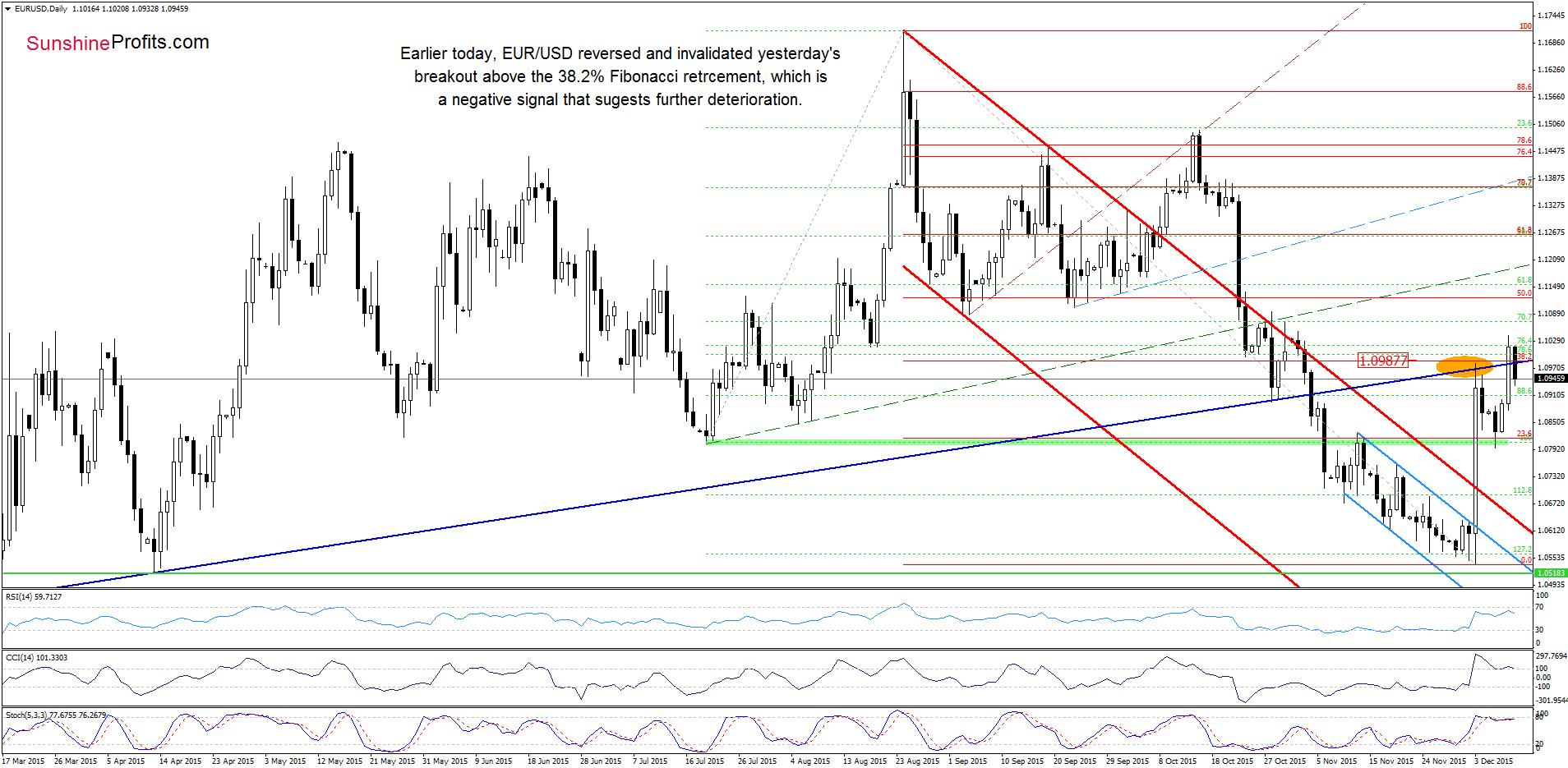

Earlier today, the U.S. Department of Labor reported that the number of initial jobless claims in the week ending December 4 rose by 13,000 to 282,000, missing analysts’ forecasts. As a result, the USD Index moved slightly lower, but did it change anything in the short-term picture of the euro?

Looking at the weekly chart, we see that EUR/USD invalidated breakout above the barrier of 1.1000 and the green line based on the Mar and Apr lows, which suggests further declines.

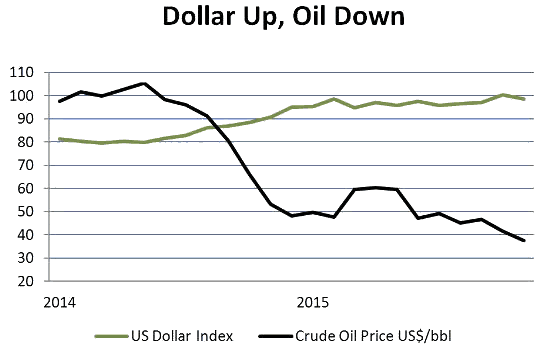

Oil is plunging again, this time in the wake of OPEC’s inability to limit its members’ production. The US dollar, meanwhile, is up on the divergence between Fed tightening and ECB/BoJ/BoC easing.

This widening gap is a perfect storm for the many, many entities that have borrowed dollars to speculate in foreign currencies or drill for oil. Some examples:

Emerging Market Debt Sales Are Down 98 Percent

(Bloomberg) – The commodity-price slump and the slowdown in China’s economy are crippling developing nations’ ability to borrow abroad, even as international debt sales from advanced nations remain at a five-year high.

Issuance by emerging-market borrowers slumped to a net $1.5 billion in the third quarter, a drop of 98 percent from the second quarter, according to the Bank for International Settlements. That was the biggest downtrend since the 2008 financial crisis and reduced global sales of securities by almost 80 percent, the BIS said in a report.

Emerging-market assets tumbled in the third quarter, led by the biggest plunge in commodity prices since 2008 and China’s surprise devaluation of the yuan. The average yield on developing-nation corporate bonds posted the biggest increase in four years, stocks lost a combined $4.2 trillion and a gauge of currencies slid 8.3 percent against the dollar. Sanctions on Russian entities and political turmoil in Brazil and Turkey also affected sales by companies in those countries.

Fears rise that junk bond investors are over their skis

(CNBC) – After years of safely reaching for yield through risky assets like stocks and speculative-grade bonds, Wall Street is heading into 2016 rethinking the strategy.

That trend of low defaults has begun to turn the other way, with the trailing 12-month rate rising to 2.8 percent in November, the highest level in three years, according to ratings agency S&P, which expects defaults to climb to 3.3 percent by Sept. 30, 2016.

Moreover, fellow ratings agency Moody’s reported its liquidity stress index in November hit its highest rate since February 2010. Still more troubling is that some of the damage has begun to spill outside the oil, gas and mining sectors, where most of the defaults had been contained.

Fully one-third of oil and gas and mining and metals companies in Moody’s coverage universe are on review for downgrade or have negative outlooks.

Brazil’s Unprecedented Torrent of Downgrades Is Set to Get Worse

(Bloomberg) – Amid Brazil’s economic and political tumult, the nation’s businesses have seen a record number of downgrades this year – and the total is about to get worse.

Fitch Ratings estimates it may slash the ratings of as many as 10 companies for every one it upgrades in 2016. Fitch said that grim scenario is most likely if it chops Brazil’s grade, an ever-growing possibility as the country’s woes deepen.

A top lawmaker initiated impeachment proceedings against President Dilma Rousseff last week, a move that may further undermine the nation’s finances and exacerbate the worst recession in a quarter century. That spells trouble for companies already finding it hard to obtain financing in the wake of an unprecedented corruption scandal at Brazil’s state oil company.

“You will see companies burning cash,” Fitch’s Carvalho said. “The cross-border market is closed for Brazilian companies, and the local market is selective.”

Saudi Arabia’s big welfare spending faces the oil abyss

(CNBC) – If Saudi Arabia maintains oil production at current levels amid the oil price crash, then it’s going to have to cut its budget – or it will likely be bankrupt by the end of the decade. The big issue is Saudi Arabia’s big spending ways, especially increased government spending on social welfare programs.

According to the IMF, government expenditures in Saudi Arabia are expected to reach 50.4 percent of GDP in 2015, up from 40.8 percent in 2014. That increase can be attributed to two things: falling oil prices (it’s bringing in less revenue) and an inflated budget (it’s spending more money).

It’s no secret that a large portion of Saudi Arabia’s roughly 30 million people rely on the government for economic support. In February, the newly crowned King Salman doled out a reported $32 billion to the Saudi people in bonuses and subsidies to celebrate his ascension to the throne.

“We are a welfare society, so the population depends a lot on government subsidies, directly and indirectly,” Abdullah Al-Alami, a Saudi writer and economist, recently told The New York Times. “But one day we are going to run out of oil, and I don’t believe it is wise to be pampered and subsidized.”

To summarize, the world is entering a classic credit crunch, in which lending dries up for marginal borrowers first before tightening for core entities like multinational corporations and developed world governments. And it’s just beginning.

Most of today’s crises evolved with oil considerably higher and the dollar somewhat lower, so current conditions are actually a lot worse than those that, for instance, caused emerging market debt issuance to evaporate and shoved Brazil into existential crisis.

And since oil overproduction will likely to continue while the differences in central bank policies are etched in stone for the next few months at least, it’s possible that the performance gap between oil and the dollar will widen going forward. This will turbo-charge today’s crises and add a few more, as oil producing US states hit financial walls and big chunks of the developing world follow Brazil down the drain.

The path of rate hikes by the US Fed and how their policy diverges from their fellow G7 nations continues to be heavily debated and will be one of the foremost important themes for the global economy in 2016.

The path of rate hikes by the US Fed and how their policy diverges from their fellow G7 nations continues to be heavily debated and will be one of the foremost important themes for the global economy in 2016.

There is no question the decision makers at US Fed sit between a rock and hard place. A report out of the Financial Times at the end of last week revealed more than a trillion dollars in US corporate debt has been downgraded so far this year. This represents a 72 per cent jump in the total value of US debt that was downgraded in the first 11 months of 2014. Much of the story is related to the energy picture and US companies that face declining revenues with weaker commodity prices, but also linked is the fear and pressure created from higher interest rates from the path of Fed rate hikes.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair