Economic Outlook

Here’s a news flash for you: Donald Trump is controversial and caustic. He says exactly what’s on his mind, no matter how incendiary, and he’s not afraid to make enemies, even with members of his party. “Bully” is a word many people use to describe the 45th U.S. president.

Here’s a news flash for you: Donald Trump is controversial and caustic. He says exactly what’s on his mind, no matter how incendiary, and he’s not afraid to make enemies, even with members of his party. “Bully” is a word many people use to describe the 45th U.S. president.

The thing is, no one who voted for Trump—I think it’s safe to say—didn’t already know this about him. His being a bully is baked right into his DNA, and he expertly honed this persona during his stint as the tough-as-nails host of NBC’s The Apprentice.

Remember when Trump received flak a few weeks back for retweeting a gif of himself

body-slamming “CNN”? The clip actually came from WrestleMania 23 in 2007, when the future president defeated World Wrestling Entertainment (WWE) CEO Vince McMahon—and consequently got to shave his head—in a fight billed as the “Battle of the Billionaires.” Trump’s bombastic style and rough edges were so aligned with the smack-talking world of professional wrestling that he was inducted into the WWE Hall of Fame in 2013.

That’s who Trump is. He’s a bully. But I’m convinced that’s why he was elected—to stand up to even bigger bullies.

Standing Up to the Beltway Party

Right now those bullies include members of the beltway party, sometimes referred to as “the deep state”—career bureaucrats, lobbyists, regulators and other officials who make it their mission to oppose any Washington outsider who threatens to shake up the status quo.

The beltway party isn’t a new phenomenon, of course. For the past 50 years, the number of government workers relative to the entire U.S. workforce has remained virtually the same. Meanwhile, the percentage of Americans employed in manufacturing has steadily plummeted.

Think about it: We have fewer people in this country who innovate and build things than people who enforce the laws that often prevent manufacturers from innovating and building at their fullest potential. What hope do they have?

When you have a bully problem, you don’t send in a Boy Scout. That’s what we learned with Jimmy Carter, whose presidency Trump’s administration so far resembles in an interesting way, according to former Federal Reserve chair Ben Bernanke. Carter and Trump, both outsiders, were sent to Washington to “drain the swamp” of the beltway party. We all know unsuccessful Carter was, but that’s likely because he was simply too nice and “decent” for the White House.

I don’t think anyone would ever accuse President Trump of being too nice and decent, but I also don’t think decency is what we need right now. Decency won’t motivate Congress to pass tax reform. Decency won’t roll back strangulating regulations.

Unlike Carter, Trump is a disruptor. He’s disrupting government just as Sam Walton, Jeff Bezos and Elon Musk disrupted the marketplace with Walmart, Amazon and Tesla. These entrepreneurs and businesses were initially criticized for shaking up the status quo and setting new precedents. Similarly, Trump gets harshly maligned, and for the very same reasons.

A Battle Brewing over Financial Regulations

Most everyone is aware of the fight that took place this past weekend between now-retired Floyd Mayweather and UFC Lightweight Champion Conor McGregor. Although official pay-per-view data hasn’t been released yet, the number of people who paid the $100 to tune in is expected to exceed the roughly 4.6 million who bought access to watch the Mayweather-Manny Pacquiao fight in 2015. This year, Mayweather’s purse was a guaranteed $100 million but will likely be northwards of $200 million. When all is said and done, McGregor’s payday is estimated to be about half that, according to ESPN.

It wasn’t called “the Money Fight” for nothing.

But over the weekend, a “money fight” of a different kind took place, with the first volley fired in Jackson Hole, Wyoming, where the annual economic symposium of central bankers was held. In what could be her last speech as chair of the Federal Reserve, Janet Yellen defended the efficacy of financial regulations that were enacted following the subprime mortgage crisis nearly 10 years ago.

Because of the reforms, Yellen said, “credit is available on goods terms, and lending has advanced broadly in line with economic activity in recent years, contributing to today’s strong economy.” Banks are “safer” today, she insisted.

Never mind that her conclusions here are questionable at best. Post-crisis reforms such as 2010’s Dodd-Frank Act have actually led to a large number of community banks drying up,giving borrowers, especially in rural areas, fewer options. Because of added compliance costs, many banks have done away with free checking, which disproportionately affects lower-income customers.

Leaving all that aside for now, Yellen’s intent was crystal clear. She made it known to President Trump that, should he re-nominate her to head the Fed when her term ends in February, she will do what she can to protect post-crisis regulations.

Trump, of course, has another point of view. He’s promised to do a “big number” on Dodd-Frank, which he claims has prevented “business friends” from getting loans.

So far he’s been true to his word. In April, he signed an executive order issuing a review of Dodd-Frank. Many of his top-level appointments to the Federal Deposit Insurance Corporation (FDIC), the U.S. Securities and Exchange Commission (SEC) and other such federal agencies have come from a pool of people the big banks feel comfortable with. And his Cabinet is well-stocked with former investment bankers, most notably Steven Mnuchin, who heads the Treasury Department.

In June, the Treasury Department released its recommendations for regulatory reform.Among them are a wholesale reduction in financial regulations, a decrease in their complexity and greater coordination among regulators.

But there’s only so much the executive branch can do alone. A bill designed to repeal key provisions in Dodd-Frank easily passed the House in June and is now in the Senate’s hands. Because it will need to clear a 60-vote threshold, a clean repeal bill looks unlikely, but relief of any kind is better than none.

Abrasive as his style may be, Trump is our greatest hope right now in bringing sensible reform to our complex tax code and regulatory infrastructure.

Looking Ahead to 2020

The Democrats might very well take a page out of the Republicans’ handbook and put up a similarly confrontational, in-your-face candidate in 2020. Right now I can think of no one more fitting of that description than Massachusetts senator Elizabeth Warren. A Democratic Socialist cut from the same cloth as Bernie Sanders, Sen. Warren can be every bit as much a bully as Trump. If you’ve seen her grill someone during a Congressional hearing, you’ll know what I’m talking about.

The Democrats might very well take a page out of the Republicans’ handbook and put up a similarly confrontational, in-your-face candidate in 2020. Right now I can think of no one more fitting of that description than Massachusetts senator Elizabeth Warren. A Democratic Socialist cut from the same cloth as Bernie Sanders, Sen. Warren can be every bit as much a bully as Trump. If you’ve seen her grill someone during a Congressional hearing, you’ll know what I’m talking about.

But whereas Trump supports free markets and business-friendly policies, I believe a President Warren would usher in a new age of punitive taxes and regulations on steroids.

As I’ve often said, it not the politics that matter so much as the policies. I support the candidate who makes it easier for Americans to conduct business and create capital. Sen. Warren has many admirable qualities, I’m sure, but her socialist, far-left ideology would be devastating to businesses and investors alike.

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor. By clicking the link(s) above, you will be directed to a third-party website(s). U.S. Global Investors does not endorse all information supplied by this/these website(s) and is not responsible for its/their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. None of the securities mentioned in the article were held by any accounts managed by U.S. Global Investors as of 6/30/2017.

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

WASHINGTON (MarketWatch) — The U.S. economic rebound in the second quarter was stronger than initially reported, as a lift to consumer spending and business investment led to the strongest growth in more than two years.

WASHINGTON (MarketWatch) — The U.S. economic rebound in the second quarter was stronger than initially reported, as a lift to consumer spending and business investment led to the strongest growth in more than two years.

Gross domestic product rose at 3% rate from April to June, up from an initial 2.6% reading, the Commerce Department said Wednesday.

Economists surveyed by MarketWatch expected a smaller upward revision in second-quarter GDP to a 2.8% rate.

The economy picked up from a 1.2% rate in the first quarter. A slow first quarter followed by an improved second quarter also occurred in two of the past three years. Economists say that the most recent data suggest the U.S. is on track to maintain a 3%-plus clip in the third quarter.

The last time the U.S. economy had two quarters above 3% was in 2014.

President Donald Trump is relying on growth above 3% to generate enough revenue for the government to pay for tax cuts and more infrastructure spending.

….also analysis and charts from ZeroHedge:

US Second Quarter GDP Revised Sharply Higher To 3.0%, Best In Two Years

In 1886 there were only 38 states in the United States.

In 1886 there were only 38 states in the United States.

Electric power was still cutting edge technology that few people had ever seen.

The Statue of Liberty hadn’t even been dedicated yet.

But it was that year that a man named Richard Sears founded a small retail company in Minneapolis, Minnesota that would grow into a retail juggernaut.

Sears was truly the Amazon of its day.

Even in the late 1800s the company was able to deliver just about any product you wanted right to your doorstep.

This was no small feat considering the first delivery truck wouldn’t be invented until 1895. There was no transportation infrastructure. And two-thirds of the population lived in remote rural areas.

Yet despite those challenges, Sears was still able to put any product you wanted in your hands.

Over time as consumer trends changed, the company started opening physical retail stores.

And once the concept of the ‘shopping mall’ became popular, Sears department stores became a mainstay at malls across America.

To give you an idea of the size and dominance of Sears back at its peak– the company owned stock broker Dean Witter Reynolds (now part of Morgan Stanley), Coldwell Banker (real estate brokerage), Allstate Insurance (currently a $33 billion company) and it started the Discover card (a $22 billion company).

Sears seemed unstoppable… a company so large and powerful that it would rule retail forever.

Then Wal-Mart entered the scene.

And after years of focusing on efficient logistics and cost savings, Wal Mart eventually outmaneuvered Sears to become the world’s largest retailer.

By 2001, Wal-Mart’s revenues were about five times that of Sears.

Then Amazon was founded… and consumers began changing their tastes to shop online.

Sears totally missed the trend. And today the company is a tiny shell of its former self.

Over the past three years alone, Sears has lost more than $5 billion. And its stock price is down nearly 75% since 2014.

Plus the company has had to lay off more than half of its peak workforce, around 200,000 employees.

To add insult to injury, the company spent about $6 billion over the past decade buying back its shares at prices as high as $174 a share.

Shares now trade below $9. That’s a 95% loss to shareholders.

Sears recently announced it will close an additional 43 stores (on top of the 265 closures it already announced this fiscal year).

This will leave the company with 1,140 stores – just above half its 2012 size.

This is a death spiral. And it could mean the sudden loss of 140,000 American jobs.

And that’s just Sears. We could see several, large retailers shutter causing hundreds of thousands of lost jobs.

Retailers have announced more than 3,200 store closures this year. And investment bank Credit Suisse expects that number will increase to more than 8,600 before the end of the year.

For the sake of context, the WORST year on record for retail store closures was in 2008 when the global financial crisis kicked off.

But even in 2008, only 6,163 retailers closed.

Bear in mind that about one in 10 Americans works in retail.

And given the rise of e-commerce, most of those retail jobs are going away. Quickly.

E-commerce currently accounts for 9% of the approximately $22 trillion in annual retail sales, up from 0.6% in 1999.

And that number is only growing.

Most retail stores operate very LOW margin businesses. They rely on having LOTS of customers in order to stay profitable.

If even a small percentage of their prospective customers stay home and shop online, they’re finished– from Sears all the way down to the small mom and pop stores.

We could see hundreds of thousands of retail workers lose their jobs as companies like Sears fail.

Sure, e-commerce will pick up some of the jobs.

Large e-commerce companies like Amazon have had to quickly build infrastructure and warehouses to serve customers around the country. That requires lots of hiring.

But it’s temporary work.

Think of it this way: it took a lot of men to lay railroad tracks across the US. It takes far fewer workers to maintain the rail system.

And as shipments increase, you simply run more cars across those tracks.

Plus, e-commerce warehouses are becoming more automated and efficient, requiring less human labor than ever before.

This sort of creative destruction and disruption isn’t anything to be afraid of; there aren’t exactly too many blacksmiths and buggy repairmen anymore either.

Progress occasionally requires the decimation of entire industries, and that’s what’s happening now.

In the long-run it’s better for everyone. But shorter-term, there’s going to be a lot of pain.

Some of the largest and most vulnerable retailers include Sears, Macy’s and JC Penney, and in total those companies employ close to 400,000 people.

All three of these companies could – and probably will – go bankrupt. But it would only take one of these stores going under (a near certainty) to roil the US economy.

You may remember during the US Presidential campaign that candidates Trump and Clinton made a big deal about the declining number of coal jobs in the US.

To put things in perspective, the US coal industry employs just over 76,000 workers.

Sears alone employs almost double that amount.

And the pace of job losses across the entire retail sector is gaining steam.

The US economy has been in ‘recovery’ now for more than eight years, i.e. it’s been nearly 100 months since the end of the last recession.

Yet the average time between recessions in modern US history is 57 months, according to the National Bureau of Economic Research.

In other words, the economy is overdue for a recession.

And the rapid loss of hundreds of thousands of jobs could certainly end up triggering it.

To your freedom,

Simon Black

Founder, SovereignMan.com

The American Health Care Act (HR 1628) finally passed by the House yesterday reducing taxes on the American people by over $1 trillion. The bill abolishes the most abusive taxes imposed by Obama and the Democrat party back in 2010 known as Obamacare. The Democrats helped the insurance companies and burdened the youth trying to force them to pay for insurance they did not need to get insurance companies to cover people they would not.

The American Health Care Act (HR 1628) finally passed by the House yesterday reducing taxes on the American people by over $1 trillion. The bill abolishes the most abusive taxes imposed by Obama and the Democrat party back in 2010 known as Obamacare. The Democrats helped the insurance companies and burdened the youth trying to force them to pay for insurance they did not need to get insurance companies to cover people they would not.

Obama as a presidential candidate back in 2008, had promised repeatedly that he would NOT raise any tax on any American earning less than $250,000 per year. That was an outright lie. As always, they claim they will only tax the rich, but it never ends up that way.

In KING v. BURWELL, 576 US – (2015), the Supreme Court upheld Obamacare claiming it was a tax. There was no constitutional power for Congress to punish someone who did not buy health insurance. The only way to uphold such a power was under the taxing powers. Justice Scalia wrote in his dessenting opinion:

The Act that Congresspassed provides that every individual “shall” maintain insurance or else pay a “penalty.” 26 U. S. C. §5000A. This Court, however, saw that the Commerce Clause does not authorize a federal mandate to buy health insurance. So it rewrote the mandate-cum-penalty as a tax.

With the repeal of Obamacare, tens of millions of middle income Americans will get tax relief from Obamacare’s long list of tax hikes that have oppressed so many. The taxes that will be abolished are:

- The Obamacare Individual Mandate Tax which hits 8 million Americans each year.

- The Obamacare Employer Mandate Tax Together with repeal of the Individual Mandate Tax repeal this is a $270 billion tax cut.

- Obamacare’s HSA withdrawal tax. This is a $100 million tax cut.

- Obamacare’s 10% excise tax on small businesses with indoor tanning services. This is a $600 million tax cut.

- The Obamacare health insurance tax. This is a $145 billion tax cut.

- The Obamacare 3.8% surtax on investment income. This is a $172 billion tax cut.

- The Obamacare medical device tax. This is a $20 billion tax cut.

- The Obamacare tax on prescription medicine. This is a $28 billion tax cut.

- Obamacare’s Medicine Cabinet Tax which hits 20 million Americans with Health Savings Accounts and 30 million Americans with Flexible Spending Accounts. This is a $6 billion tax cut.

- Obamacare’s Flexible Spending Account tax on 30 million Americans. This is a $20 billion tax cut.

- Obamacare’s Chronic Care Tax on 10 million Americans with high out of pocket medical expenses. This is a $126 billion tax cut.

- The Obamacare tax on retiree prescription drug coverage. This is a $2 billion tax cut.

…also from Martin:

French Elections – A Sell Signal Long-term for the EU Regardless of Who Wins

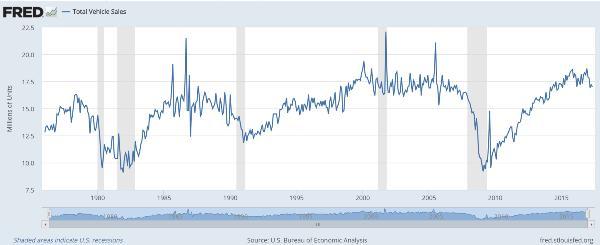

The past decade’s historically low interest rates convinced millions of Americans to buy cars they could only afford with hyper-cheap credit. This made auto sales one of the drivers of the recovery, but it also left far too many people with underwater “car mortgages” that will limit their spending on other things and prevent them from buying their next car until sometime in the 2020s.

Like all artificial (that is, credit-driven) booms, this had to end eventually, and it’s looking like now is the time:

U.S. Auto Makers Post Sharp Sales Decline in June

(Wall Street Journal) – Detroit’s car companies reported steep sales declines in June, capping a bumpy first half of the year for the U.S. auto industry and setting a bleak tone for the summer selling season.

The reports, released Monday, come as analysts expect overall auto sales to have fallen more than 2% in June compared with the prior year, according to JD Power. The firm said the industry’s selling pace hit its lowest point since 2014 over the first six months of 2017, and traffic at dealerships—measured by retail sales—fell to a five-year nadir in June.

Edmunds.com, a consumer-research company, said buyers are stretching more than ever to afford cars and trucks that are growing increasingly more expensive due to a barrage of safety gear and connectivity options. The firm estimates the average auto-loan length reached a high of 69.3 months in June, with the average amount of financing reaching $30,945, up $631 from May.

General Motors Co. GM +2.91% said U.S. sales fell 5% to 243,155 vehicles, while Ford Motor Co. F +4.07% said sales totaled 227,979 vehicles, down 5.1% from a year earlier, and Fiat Chrysler Automobiles N.V. posted a 7% decline to 187,348 vehicles.

The following charts show a steady rise in car sales and inventories from their 2009 low to a 2015-2016 peak. If they’ve shifted into a cyclical decline the bottom, based on history, is a long way down.

Meanwhile, the cheap lease deals of the past few years are starting to run off, producing a tidal wave of nearly-new used cars to compete with much more expensive new ones. The result: falling used car prices that will, over time, cut demand for new cars even further.

Used cars are getting cheaper: CarMax

(Fox News) – CarMax (KMX), the nation’s largest used-car retailer, reported a decline in selling prices during its fiscal first quarter.

Used-car prices are expected to decline this year, as vehicles leased during the U.S. auto sales boom in recent years begin to hit the market. Manufacturers and dealers are closely watching price trends because cheaper used cars could soften demand for new vehicles .

CarMax CEO Bill Nash said Wednesday the Richmond, Virginia-based dealership chain has already seen an influx of off-lease vehicles, which is driving prices lower.

“As more of them come in, prices will continue to drop,” Nash told analysts during a conference call.

The trend put downward pressure on CarMax’s average selling prices for the first quarter, offsetting a high mix of more expensive pickup trucks and SUVs. CarMax sold used vehicles for $19,478 on average, a 1.9% drop from the year-ago quarter’s average selling price of $19,858. Prices for wholesale vehicles also fell 2.9% to $5,113.

This is obviously bad news for an economy dependent on people buying stuff they don’t need with money they don’t have. So other things being equal, expect disappointing numbers for GDP, inflation, wages, etc., going forward as this major industry morphs from tailwind to headwind.

And expect the process of interest rate normalization to become an even harder sell for the Fed, which needs a boom to justify making loans more expensive for tomorrow’s car and house buyers. As the saying goes, it’s inflate or die.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair