Economic Outlook

To say that Saudi Arabia is on the verge of its most significant change in decades is not an exaggeration.

To say that Saudi Arabia is on the verge of its most significant change in decades is not an exaggeration.

Inside Saudi Arabia—a Failing Kingdom you will learn:

- How the House of Saud could collapse in four years… and what it means to the region and the globe.

- Why the Saudi government is considering an IPO of its crown jewel—after it helped drive oil prices down.

- Why OPEC is defunct and may never return to its glory days.

- How the Saudis’ policies are empowering ISIS.

- What Middle Eastern oil policies mean for the future of the US shale industry… and why it matters to you.

100,000 refugees have entered Greece since the beginning of the year compared to 5,000 a year ago.

Where can they go? On February 16, Austria announced it will take at most 80 a day. Just this week Macedonia reduced the number of refugees allowed to transit through its territory to about 1,000 a day.

At least 15,000 are trapped in Greece, a country without resources to deal with them. In response to the growing crisis, Greece Withdraws Ambassador to Austria.

Athens withdrew its ambassador to Austria on Thursday in a sign of the mounting acrimony between EU countries over the bloc’s failed refugee policies, a fight that increasingly risks destroying the continent’s passport-free travel zone.

In a statement announcing the decision, Greece’s foreign ministry accused the Austrian government of taking unilateral action outside of EU rules and recent agreements by capping the number of asylum seekers that it would accept across its southern border.

The move by Vienna has angered several member states, particularly Germany, which believe it was a direct violation of principles agreed by Werner Faymann, Austria’s chancellor, at recent EU summits.

While Vienna is capping the number of daily asylum applications it accepts at 80, it is freely allowing as many as 3,200 refugees a day to pass through Austria en route to Germany — even after agreeing not to do so at the most recent EU summit.

Despite anger in Athens and Berlin, Vienna has hastily put together a group of EU and non-EU allies along the so-called “Western Balkans route”, most of whom met in Vienna on Wednesday to agree policies that could constrict tens of thousands of refugees in Greece indefinitely. Neither Germany nor Greece was invited to the Vienna meeting.

The EU’s migration chief, Dimitris Avramopoulos, warned on Thursday that the bloc had 10 days to improve the situation “or else there is risk the whole system will completely break down“.

Even the French and the Belgians have engaged in verbal sparring after Belgium’s decision to impose border controls on its frontier with France. Belgium is concerned it could face an influx of refugees due to an imminent move by the French authorities to clear part of Calais’ so-called “jungle” migrant camp.

Mr Tsipras said Greece would block an agreement at a refugee summit on March 7 that “does not ringfence an obligatory sharing of the responsibility and burden [of the refugee issue] among the member states in a proportional way”.

Whole System Broken Down

I don’t need 10 days to report the obvious: The whole system has already broken down.

The biggest problem at the moment is actually Greece. By letting all refugees in, even though passages to the North are severed, Greece is the problem child, not Austria, nor Hungary, nor Macedonia.

At the expense of its own citizens, with money it dos not have, Greece bears the brunt of the refugee crisis. The smart thing for Greece to do would be to close its own border just as Hungary did.

Border Control Map

The above map is from the BBC on January 25. I added the blue anecdotes that show additional blockages since then.

Blockage Math

- In 56 days, starting January first, 100,000 have entered Greece primarily from Turkey. That’s 1,786 a day.

- As the temperatures climb, the count will rise if Greece does nothing to stop the flow.

- Macedonia reduced the number of refugees allowed to transit through its territory to about 1,000 a day.

- 15,000 are already trapped in Greece and that number will rise by at least 786 a day. In one month, that’s another 23,580.

- If Germany refuses the pass through from Austria, the maximum flow would decline to 80 per day, and the trapped rate would rise from 786 a day to 1,706 per day (51,180 a month).

Not Broken Yet Thesis Recap

Don’t worry. We are told the system is not broken yet. Greece says there’s still 10 days to fix the problem.

Meanwhile, Greece has vowed to veto any solution that does not spread the refugees around, while Austria has called a summit of countries sympathetic to more blockages.

Related Articles

February 16, 2016: “Just Say No”: Austria Announces Daily Quotas on Refugees: Yearly Flow Reduced to 37,500 from 1,000,000.

February 18, 2016: Pass Thru Politics: EU Says Austria’s Refugee Quotas Violate Geneva Convention; In Praise of Austria.

Last we visited on the subject of U.S. inflation (November, 2015) we wrote,

“Using those simplistic numbers suggests that U.S. inflation as measured by the [headline] CPI could rise to an annual rate of about 4% …”

That possibility is now increasingly likely given recent rise in U.S. inflation. This view is reaffirmed by recent data. If an error exists in this projection, it is to underestimate potential for inflation in U.S. to rise.

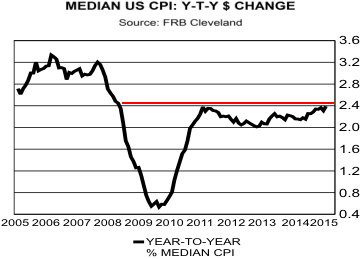

Analyzing the state of U.S. inflation begins with the median CPI produced monthly by Federal Reserve Bank of Cleveland. What is the median CPI? To calculate the headline CPI for any particular month the rate of change is calculated for each of the components of the CPI such as energy, food, and housing. Headline CPI is then calculated by weighting each of those components to produce a weighted average. Median CPI is that rate of change for which half of the components had a higher rate of change and half had a lower rate of change. It divides a ranking of the component rates of inflaton in half. The median is less impacted by extreme changes in the prices for anycomponent which can in someways distort the weighted average CPI.

In top chart is plotted the year-to-year percentage change for the median CPI. Two observations are worthy of mention. These observations suggest that expectations of higher U.S. inflation are reasonable and likely to be correct. First, the latest observation exceeds the previous high. Second,in January the year-to-year percentage change rose to the highest level since 2009.

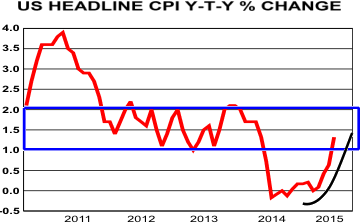

Before we move to what the median CPI might be saying about U.S. inflation, let us take a brief look at recent developments in U.S. inflation. In chart to right is plotted the year-to-year percentage change for the headline CPI. Notice that it has risen fairly dramatically in recent months. See arrow.

Era of no inflation is over. U.S. inflation has moved back into a “trading range” of 1-2% in which it had moved for several years. That may suggest the low inflation experienced was an aberration, not an equilibrium state.

Chart below compares the year-to-year percentage change for the headline CPI, black line, with that for the median CPI, red line. Twice early in the chart the headline CPI moved below the median CPI. In both of those cases the headline CPI rate of change turned up and moved above the median CPI. In the first of those cases the rise in the headline CPI rate of change was roughly 4 percentage points from low to high, as highlighted by blue arrow.

In the second case the rise from low to first high was about 4.5 percentage points and 6 percentage points to the ultimate high in the rate of headline inflation.

Median CPI is one of several measures of central tendency, as is the weighted average used for the headline CPI. However, the median is not distorted by high and low values as is the case with averages. Note how far less volatile the median is compared to the weighted average. It may be in the above instance the better measure of central tendency. It seems to act as a “magnet” for the headline CPI, returning the calculation to a more “normal” reading.

In the more recent data, right hand side of graph, the headline CPI is below is running below the median and it has turned up sharply. Current situation is developing much like the earlier two cases. Using4 percentage points as suggested by those earlier moves, a common number in the above discussion, suggests that the headline CPI which had a low of roughly 0% is likely beginning a move to 4%, as highlighted by the third blue arrow, or higher. Several factors, which includes time and the mechanics of averaging, may contribute to coming rise in U.S. headline inflation.

First of those is oil prices. Writers seem to often have difficulty with verb tense. Oil prices have fallen, meaning yesterday. Oil prices are not falling, meaning present time. Looking forward from today, oil prices are likely to rise, though perhaps by not much. Commodity price are self correcting, though often the process is lengthy. The “dividend checks” from the oil price slide have largely been cashed and spent. Those declining oil prices did have a tendency to depress other prices. That good news is slowly fading into history. Oil prices should now begin to buoy and then cause other prices to rise.

The speculative advance in the value of the U.S. dollar against other currencies is beginning to fade. Rising value of the dollar depressed dollar denominated prices as foreign purchasers could not and cannot afford those dollar denominated commodities and goods. The value of their currency having fallen means foreign consumers cannot purchase the same amount of U.S. goods and commodities. A simple ending of the speculative advance will begin to support dollar denominated prices. And if it declines as it should, dollar denominated prices will rise.

Third is the long overdue normalization of interest rates in the U.S. While the path is unclear, the need to remove the interest rate distortions in the U.S. economyseems obvious to the Federal Reserve. Abnormally low interest rates of recent years have caused funds to shift to the financial sector. Prices of financial assets rose, but are ignored in the calculation of inflation. Normalization of interest rates will shift funds from speculation in financial markets to the real economy, which is included in the calculation of the CPI. As fund flow from speculation to real activity, prices in latter sector should firm and rise, pushing up the CPI.

With U.S. inflation headed to 4%, and likely higher, is your portfolio positioned to prosper? The “markets” have already begun to discount this development. Fantasy “growth” stocks have fallen, and continue to be the most vulnerable. Gold has moved sharply higher, jumping by more than $200 at one point. Gold stock ETFs have risen from their lows by more than 40%. These market adjustments are a reminder to investors that diversification is still smarter than any and all strategists. If you have missed the first step in a new Gold bull market, today is the time to correct that inefficiency.

Ned W. Schmidt,CFA has had for decades a mission to save investors from the regular financial crises created by economists and politicians. He is +publisher of The Value View Gold Report, monthly, with companion Trading Thoughts. These reports again turned to raging bulls on Gold and Silver in 2015. To receive these reports, go to: www.valueviewgoldreport.com Follow us @vvgoldreport

Washington, DC is pretty proud of the employment numbers it has been pumping out. Most recently, the Labor Department reported that the US unemployment rate dropped to 4.9% in January.

That’s an eight-year low going back to the 2008–2009 Financial Crisis.

The actual number of new jobs was a little on the light side, at 151,000 versus the expected 190,000, but most of the Wall Street crowd was impressed with the +0.4% monthly increase in wages.

Another Monday, another set of “surprisingly” bad economic numbers. A few representative headlines:

China manufacturing prices decline for 18th straight month

Oil prices fall 5% on bad China data, OPEC uncertainty

Global factories parched for demand, need stimulus

Junk bonds suffer a rare negative return in January

US consumer spending softens, savings hit 3-year high

US manufacturing weak again in January

China official PMI misses in January, Caixin PMI shows contraction

Japanese bond yields continue to collapse

There’s more, but you get the (very dark) picture. And thanks to the Atlanta Fed’s GDPNowprogram we can see in real time how these numbers translate into current-quarter GDP growth. Apparently the US is looking at yet another weak stretch in which economists (represented by the Blue Chip consensus) are gradually forced to admit that they’ve wildly overestimated our ability to manage our debt.

GDP growth matters for a couple of reasons. First, an economy that’s borrowing a lot of money (as all the major ones are) has to generate large amounts of new wealth or it sinks ever-deeper into a hole that eventually leads to a 1930s-style depression. 1.3% growth does not come close to stopping the expansion of debt/GDP. So every quarter like the current one brings a debt-driven collapse that much closer.

Second and far more interesting in the near-term, slow-growth/high-debt countries eventually conclude that their only remaining option is massive currency devaluation. Europe and Japan are already there, and are aggressively ramping up their own currency war offensives. The US, if history is any guide, will soon (either this year or as part of the next administration’s “first 100 days” political offensive) decide that a too-strong dollar is standing in the way of “progress” and will start looking for ways to devalue.

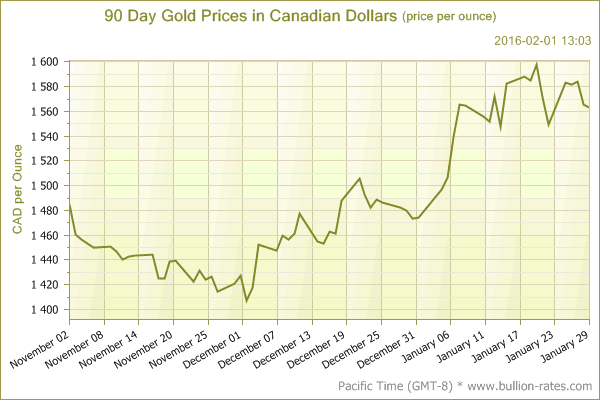

Then the real fun begins — at least for goldbugs. For holders of dollars it won’t be nearly as pleasant. Here’s the Canadian version of what’s coming for US investors, though the US chart will be steeper and will go on for years instead of months:

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair