Energy & Commodities

![]() Recently, I wrote on these pages that a remarkable turnaround was taking place in the President’s fortunes. It’s an impressive display of rising from the depths of falling popularity last fall, and it is starting to be felt in many areas, with major impacts on the future of energy.

Recently, I wrote on these pages that a remarkable turnaround was taking place in the President’s fortunes. It’s an impressive display of rising from the depths of falling popularity last fall, and it is starting to be felt in many areas, with major impacts on the future of energy.

At his lowest point, the U.S. President was widely regarded as a lame duck, shedding influence and power, and on a down-hill slide.

This was followed by a number of embarrassments, with one of the worst coming from Russia, when it chose to provide sanctuary to Edward Snowden who revealed that the U.S. was hacking the strategic communications of its closest allies.

More damaging, the revelation came at the worst possible time for the U.S., seriously discrediting its campaign to enlist allies against alleged Russian and Chinese hackers.

This was followed by another embarrassment where the U.S. utterly failed to prevent U.S. allies from joining the Chinese-sponsored Asian infrastructure bank. It seemed that the doomsayers were proving correct about America’s decline and fall.

Since then, Obama has been on a roll, with victories in Congressional trade agreements and at the Supreme Court with decisions that removed legal and constitutional challenges to the President’s health program, and gay marriage.

Following hot upon these achievements were the successful negotiations with Cuba and Iran, that went far beyond expectation, climaxing with the signing of the historic Iran nuclear agreement.

Even more surprising was the President’s ability to marginalize the powerful lobbies and opponents of these agreements, including hard-liners in the U.S., Iran, Israel, and the Gulf Kingdoms.

Not Your Father’s Sanctions

In the past, the effectiveness of sanctions was often questioned because of the difficulty of tracking compliance. The result was that targeted countries easily hid and continued banned activities. The sanctions golden rule: if you can’t track them, you can’t enforce them.

But current sanctions are nothing like they were in the past. The difference is that technology has lifted surveillance to unprecedented levels. What with spy satellites, drones, and sophisticated listening devices, the U.S. now has the capacity to pierce nearly every form of communication and transaction. That is the secret weapon which enables the west to impose iron bound constraints that can level just about any economy.

Whether the participants in the recent negotiations will comply with the terms of their agreements, only the future can tell. But there’s little question that none would have come to the table without the sanctions.

Recall also that only first stage sanctions had been imposed on Cuba, Iran, and Russia, with each nation clearly warned that far worse lay in store if targeted activities continued.

The message was hardly lost on the ever pragmatic President Putin, who despite brave words of resistance, suddenly saw that it was to his country’s benefit to cooperate with the U.S. and its allies, particularly in the Iranian nuclear negotiations, and the ongoing war in Syria and Iraq.

Nor was the message lost on China either, who also suddenly found it in their interest to stop island building in the South China Sea, and began negotiations with its neighbors over territorial claims, as urged by the U.S. and its allies in the region. China ‘acting poor’ when Russia recently came calling for financial help also smacked of western influence.

Contrary to their rhetoric, Iran and Russia were deeply chastened by sanctions, even more so by the oil price collapse, and have agreed to major concessions. It’s no accident that both countries are also becoming ever more important in the world’s anti-terrorism campaign, an effort clearly being coordinated with the U.S.

OPEC Support

Playing into Obama’s hand was a different sort of victory taking place during the same period. That was the Saudis leading OPEC to defend their traditional market share by flooding the oil markets.

The ensuing trade war against competitors has caused every other major oil producing country and oil companies to cut future development plans. Importantly, the oil glut reinforced the damaging effects of sanctions on targeted countries.

Some conspiracy theorists have claimed that the U.S. Administration conspired with the Saudi King to create an oil glut by over-producing, directly aimed at crashing the Russian economy, where energy accounts for nearly 50 percent of its budget.

U.S. Investment Bank, Morgan Stanley recently reported that the Saudi’s were over-producing by some 1.5 million barrels per day in a market with a surplus of around 800,000 barrels per day.

The Bank added that the oil markets’ fall could be worse and last longer than the one created 1986, in which Saudi Arabia grew tired of shouldering the burden of production cuts and decided to flood the market in an effort to pursue market share.

With Iran expected to return to markets, thereby adding to the glut, the bank also stated that these current moves made the risk in oil markets “historically unanalyzable,” a red alert to the investment community.

Oil Glut Ricochet

The Saudis enthusiastically took up the opportunity to lower global energy prices, ostensibly claiming they were not aiming to kill off rivals in Russia or the U.S., but merely that they were not the highest cost producer.

There were also other unexpected reversals. It has been widely reported that the Gulf Kingdoms are outraged over the U.S. drawing closer to Iran, as well as the U.S. distancing itself from the wars in the Middle East. Evidence for this view can be found in the Saudis’ multi-billion dollar deals with the Russia, which fly in the face of U.S./EU sanctions.

The clincher in the Russian-Saudi entente may just have occurred with the sudden ISIS terrorist attacks in Saudi Arabia.

The Saudis are all too aware of the threat that ISIS presents, the monster that some claim they created, and are now badly in need of military assistance, especially with the U.S. declining full scale military engagement in the region.

The Glut’s Toll

The result of the ensuing glut is a fast declining industry that is now willingly accepting new production cutbacks, while oil producing countries like Russia, Canada and Australia, are edging dangerously close to recession, with their currencies hitting six year lows.

As reported by CNBC, global job losses in the oil industry have reached over 141,200, with severe ripple effects across supporting industries. The U.S. is by no means immune to the downtrend, where current lay-offs in the energy field are approaching 71,000, and expected to climb.

U.S. Strategy for the Middle East

If, as it seems, Obama is back on top as a world leader, it’s important to understand his overall strategy and the likelihood of success.

The consensus amongst energy mavens is that if the Iran nuclear deal eventually leads to a withdrawal of sanctions, the results will be increased Iranian supplies, forcing prices lower by some $10 per barrel, according to World Bank estimates.

But Iran’s nuclear deal is about much more than the price per gallon. What the U.S. and its allies are trying to accomplish is no less than the reversal of political hostilities that have marginalized Iran for over thirty years and fueled hostility across the region.

As the President recently stated, the nuclear agreement is also meant to restore Iran as a regional leader in the Mid-East and turn a hostile relationship into at least a neutral one. That could go a long way in changing the political structure of the Middle East, while reducing the West’s dependency on its traditional allies in the region.

That’s not to say that the U.S. and Iran are destined to become close allies, but to recognize that they have important shared interests in combatting radical Islam that could lead to far greater cooperation.

There are some who claim that despite denials, the U.S. and Iran are already cooperating in the West’s battle against ISIS in Iraq and Syria. If so, that could go far in supporting Obama’s goal to pivot from the Middle East and towards Asia.

As stated here, another overriding U.S. goal is to prevent Iran’s drift eastward into a commercial and military alliance with Russia and China, as a partner in the recently formed Shanghai Cooperation Organization, the Eurasian Economic Union, and Silk Road project. Instead, the U.S. wants Iran positioned as a competitor to Russia for EU and Asian energy markets, and as a bulwark against Russian and Chinese expansion.

The problem for the administration is that hard-liners at home and abroad, having failed to kill the deal, are continuing their efforts to stop any broader entente emerging between the Iran, its neighbors, and the world.

Here, the road is likely to be far less smooth for Obama. Unlike the nuclear deal that was undertaken under the banner of a UN resolution, any further U.S. political deals with Iran would be subject to congressional approval, something few experts view as forthcoming.

What with these formidable barriers to entente, a continuing drift eastward by Iran towards a closer commercial and military relationship with Russia and China remains a strong possibility.

But I think that the nearly two years of nuclear negotiations with Iran, if it accomplished nothing else, restored Iran to the position of a recognized regional power.

Iran is also unlikely to forget that both China and Russia voted in the UN to support sanctions against Iran. Nor is the fact likely to be ignored that Russia also declined to breach sanctions to deliver a previously contracted system of advanced missile defense systems to its erstwhile ally. Russia’s sudden close relationship with the Saudis is also not likely to sit well in Tehran.

For Iran, an over-riding goal in the deal was the repeal of sanctions, enabling the country to regain its former status as OPEC’s third largest producer. With that goal more realistic in light of a successful conclusion of the recent negotiations, Iran is unlikely to adopt policies to antagonize its newfound partners.

Instead of becoming captive to either Russia or China, Iran is far more likely to promote itself as an anti-terror partner with both west and east, while building investment markets with both sides of the ‘great game’ for its own benefit.

At the same time, Iran is leading the movement to form a united front against terrorism, partnering with the U.S., the Gulf Kingdoms, Turkey, Russia, and Syria.

Conclusion

In a region often beset by conflicts, with hardliners at home and abroad working against it, the odds are high against the success of the American strategy and the Iran deal.

Israel’s Prime Minister Netanyahu has turned the deal into a partisan issue in the midst of a presidential election campaign, in which it will undoubtedly play a major part.

Leading U.S. Democrat Congressmen have gone rogue against their administration, voicing opposition to the deal. Advocates on both sides are now raising the specter of war as the sure results of their opponents’ plans. Can pictures of mushroom clouds be far behind?

Arrayed against the deal opponents are the powerful interests of the international business community, now impatiently chomping at the bit to get into Iran’s virtually untapped market.

Nearly every major western country has recently sent trade missions to Iran in anticipation of sanctions being lifted. Representatives included major international oil companies, banks, and manufacturers. Their enormous influence and immense wealth will weigh heavily in resolving the issue.

A surprising announcement came that may hint at trending opinions in Europe: Yesterday Switzerland became the first country in the world to lift sanctions on Iran, in support of the nuclear deal.

For the President’s supporters, the deal holds real promise for the creation of a partnership of former adversaries united against terror.

If it proves successful, the world may finally have cause to breathe a sigh of relief, but as nearly everyone involved agrees, the outcome is still far from certain.

Trading position (short-term; our opinion): No positions are justified from the risk/reward perspective.

Although crude oil climbed above $43.50 on Friday, the combination of a stronger greenback and the Baker Hughes report pushed the commodity lower. As a result, light crude gained 1.28%, but closed the day below important resistance zone. What’s next?

Friday’s data showed that U.S. producer prices were higher for a third straight month in July and factory output increased at the fastest rate in eight months, which supported the greenback and made crude oil less attractive to users of other currencies. Additionally, Baker Hughes reported that U.S. oil rigs increased by two to 672 last week for the week ending on August 7, marking the fourth straight week of weekly builds. In these circumstances, light crude gave up some gains, but closed the day above the March low, invalidating earlier breakdown. Will we see higher values of the commodity in the coming week? (charts courtesy of http://stockcharts.com).

Looking at the weekly chart we see that although crude oil slipped under the March low, the commodity rebounded and closed the week above this important support level.

What impact did this move have on the very short-term picture? Let’s examine the daily chart and find out.

From this perspective, we see that crude oil moved little higher on Friday and invalidated the breakdown under the March low. Although this is a positive signal, which suggests further improvement, light crude is still trading under the solid resistance zone created by the green and blue declining resistance lines and also the green horizontal line based on the Jan low. Additionally, Friday’s move is quite small (compared to previous upward moves marked with blue) and materialized on tiny volume, which means that oil bulls are not as strong as it seems at the first sight.

What does it mean for the commodity? In our opinion, all the above in combination with the current position of the indicators (there are no buy signals, which could encourage oil bulls to act) suggests that another test of the support area created by the March low and the red declining support line is very likely. Nevertheless, we believe that the risk of re-entering short positions is too high at the moment. The reason? We think that the best answer to this question will be the quote from our previous Oil Trading Alert:

(…) Please consider the way crude oil declined in January 2015. Black gold declined sharply at first, but the final days (and weeks) of the decline were not sharp – crude oil declined slowly and the thing that was indeed sharp, was the corrective upswing that we saw in the final part of the month. We wouldn’t want to be holding short positions should something like that happened once again and the risk of such action is not negligible.

Summing up, crude oil moved higher and invalidated earlier breakdown under the March low. Despite this (seemingly positive) development, light crude remains under the solid resistance zone, which increases the probability of another test of the red declining support line. Nevertheless, in our opinion, the outlook for crude oil is not bearish enough to justify opening another short positions – at least not yet. We’re happy with the profits that we took off the table recently and we don’t want to risk losing capital before a trade is really justified from the risk/reward point of view. We will continue to monitor the market, look for another profitable trading opportunity and report to you accordingly.

Very short-term outlook: mixed

Short-term outlook: mixed

MT outlook: mixed with bearish bias

LT outlook: mixed with bearish bias

Trading position (short-term; our opinion): No positions are justified from the risk/reward perspective.

Looking at the weekly chart we see that although crude oil slipped under the March low, the commodity rebounded and closed the week above this important support level.

What impact did this move have on the very short-term picture? Let’s examine the daily chart and find out.

Four weeks after gold tumbled to 5-year lows on revelation of far lower Chinese gold holdings than previously anticipated, gold bulls find out that one of the world’s greatest hedge fund managers made gold the biggest holding in his fund in Q2. He also loaded up on 2 large miners.

Stan Druckenmiller’s family office, Duquesne Capital Management, bought 2.9 mn shares of SPDR Gold Trust’s GLD ETF, worth $323.6 million at the end of June, according to the Securities and Exchange Commission’s quarterly filing. Duquesne’s gold ETF purchase bumped the fund’s Facebook holdings off the 2nd position to become the biggest holding in the $1.47 bn fund.

Druckenmiller acted as George Soros’ chief strategist when he helped execute the shorting of the British pound to the extent of forcing the UK out of the Exchange Rate Mechanism in September 1992. Since its inception in 1986, Duquesne has had an average return of 30% per year. In early May, Druckenmiller told Bloomberg in May that interest rates were likely to stay near 0% for 10 years, casting doubt over whether the Fed would ever move to liftoff.

Druckenmiller vs Paulson

Despite the scale and timing of Druckenmiller’s gold position, it remains unclear whether the trade is a long-term bet on the stabilisation of gold resulting from a possible peak in the USD and lack of Fed hikes, or is a short-term trade aimed at taking profit after a brief bounce. The fact that Druckenmiller has also purchased 1.28 mn shares of gold miner Newmont Mining and 3.6 mn shares of copper giant Freeport-McMorcan in the same quarter could indicate he’s in it for the long run.

In contrast to Druckenmiller, John Paulson, the biggest holder of the GLD ETF, sold 11% of his holdings in Q2 after initially slashing them by 50% in Q2 2013 during gold’s 25% collapse that quarter. While Paulson is the biggest owner of GLD, accounting 4% of the ETF, the fund makes up less than 5% of Paulson & Co’s holdings, ranking 7th out of 64 different securities.

As John Paulson is quietly planning an exit out of his gold holdings, Druckenmiller is prominently loading up on the yellow metal.

Commodity Weakness Persists

In today’s Outside the Box, good friend Gary Shilling gives us deeper insight into the global economic trends that have led to China’s headline-making, market-shaking devaluation of the renminbi. He reminds us that today’s currency moves and lagging growth are the (perhaps inevitable) outcome of China massive expansion of output for many products that started more than a decade ago. China was at the epicenter of a commodity bubble that got underway in 2002, soon after China joined the World Trade Organization.

As manufacturing shifted from North America and Europe to China—with China now consuming more than 40% of annual global output of copper, tin, lead, zinc and other nonferrous metal while stockpiling increased quantities of iron ore, petroleum and other commodities—many thought a permanent commodity boom was here.

Think again, Australia; not so fast, Brazil. Copper prices, for instance, have been cut nearly in half as world growth, and Chinese internal demand, have weakened. Coal is another commodity that is taking a huge hit: China’s imports of coking coal used in steel production are down almost 50% from a year ago, and of course coal is being hammered here in the US, too.

And the litany continues. Grain prices, sugar prices, and—the biggee—oil prices have all cratered in a world where the spectre of deflation has persistently loomed in the lingering shadow of the Great Recession. (They just released grain estimates for the US, and apparently we’re going to be inundated with corn and soybeans. The yield figures are almost staggeringly higher than the highest previous estimates. Very bearish for grain prices.)

Also, most major commodities are priced in dollars; and now, as the US dollar soars and the Fed prepares to turn off the spigot, says Gary, “raw materials are more expensive and therefore less desirable to overseas users as well as foreign investors.” As investors flee commodities in favor of the US dollar and treasuries, there is bound to be a profound shakeout among commodity producers and their markets

(Excerpted from the August 2015 edition of A. Gary Shilling’s INSIGHT)

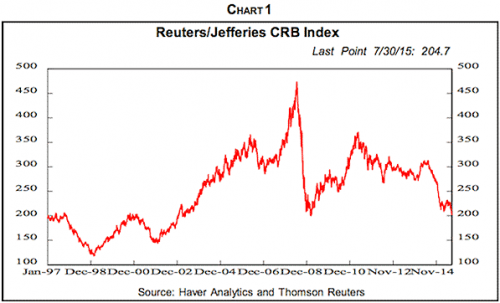

The sluggish economic growth here and abroad has spawned three significant developments – falling commodity prices, looming deflation and near-universal currency devaluations against the dollar. With slowing to negative economic growth throughout the world, it’s no surprise that commodity prices have been falling since early 2011 (Chart 1). While demand growth for most commodities is muted, supply jumps as a result of a huge expansion of output for many products a decade ago. China was the focus of the commodity bubble that started in early 2002, soon after China joined the World Trade Organization at the end of 2001.

China, the Manufacturer

As manufacturing shifted from North America and Europe to China – with China now consuming more than 40% of annual global output of copper, tin, lead, zinc and other nonferrous metal while stockpiling increased quantities of iron ore, petroleum and other commodities – many thought a permanent commodity boom was here.

So much so that many commodity producers hyped their investments a decade ago to expand capacity that, in the case of minerals, often take five to 10 years to reach fruition. In classic commodity boom-bust fashion, these capacity expansions came on stream just as demand atrophied due to slowing growth in export-dependent China, driven by slow growth in developed country importers. Still, some miners maintain production because shutdowns and restarts are expensive, and debts incurred to expand still need to be serviced. Also, some mineral producers are increasing output since they believe their low costs will squeeze competitors out. Good luck, guys!

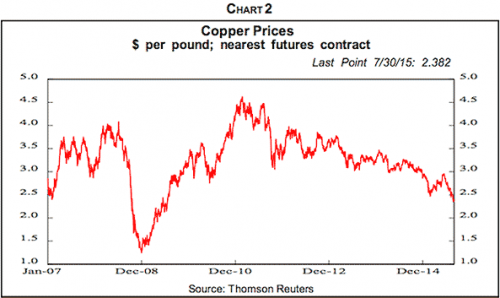

Copper, Our Favorite

Copper is our favorite industrial commodity because it’s used in almost every manufactured product and because there are no cartels on the supply or demand side to offset basic economic forces. Also, copper is predominantly produced in developing economies that need the foreign exchange generated by copper exports to service their foreign debts. So the lower the price of copper, the more they must produce and export to get the same number of dollars to service their foreign debts. And the more they export, the more the downward pressure on copper prices, which forces them to produce and export even more in a self-reinforcing downward spiral in copper prices. Copper prices have dropped 48% since their February 2011 peak, and recently hit a six-year low as heavy inventories confront subdued demand (Chart 2).

Even in 2013, after two solid years of commodity price declines, major producers were in denial. That year, Glencore purchased Xtrata and Glencore CEO Ivan Glasenberg called it “a big play” on coal. “To really screw this up, the coal price has got to really tank,” he said at the time. Since then, it’s down 41%. But back in February 2012 when the merger was announced, coal was selling at around $100 per ton and Chinese coal demand was still robust.

Nevertheless, Chinese coal consumption fell in 2014 for the first time in 14 years and U.S. demand is down as power plants shift from coal to natural gas. Meanwhile, coal output is jumping in countries such as Australia, Colombia and Russia. China’s imports of coking coal used in steel production are down almost 50% from a year ago. Many coal miners lock in sales at fixed prices, but at current prices, over half of global coal is being mined at a loss. U.S. coal producers are also being hammered by environmentalists and natural gas producers who advocate renewable energy and natural gas vs. coal.

Losing Confidence?

Recently, major miners appear to be losing their confidence, or at least they seem to be facing reality. Anglo-American recently announced $4 billion in writedowns, largely on its Minas-Rio $8.8 billion iron ore project in Brazil, but also due to weakness in metallurgical coal prices. BHP took heavy writedowns on badly-timed investments in U.S. shale gas assets. Rio Tinto’s $38 billion acquisition of aluminum producer Alcan right at the market top in 2007 has become the poster boy for problems with big writeoffs due to weak aluminum prices and cost overruns.

Glencore intends to spin off its 24% stake in Lonmin, the world’s third largest platinum producer. Iron ore-focused Vale is considering a separate entity in its base metals division to “unlock value.” Meanwhile, BHP is setting up a separate company, South 32, to house losing businesses including coal mines and aluminum refiners. That will halve its assets and number of continents in which it operates, leaving it oriented to iron ore, copper and oil.

Goldman Sachs coal mines suffered from falling prices and labor problems in Colombia. It is selling all its coal mines at a loss and has also unloaded power plants as well as aluminum warehouses. The firm’s commodity business revenues dropped from $3.4 billion in 2009 to $1.5 billion in 2013. JP Morgan Chase last year sold its physical commodity assets, including warehouses. Morgan Stanley has sold its oil shipping and pipeline businesses and wants to unload its oil trading and storage operations.

Jefferies, the investment bank piece of Leucadia National Corp., is selling its Bache commodities and financial derivatives business that it bought from Prudential Financial in 2011 for $430 million. But the buyer, Societe Generale, is only taking Bache’s top 300 clients by revenue while leaving thousands of small accounts, and paying only a nominal sum. Bache had operating losses for its four years under Jefferies ownership.

Grains and other agricultural products recently have gone through similar but shorter cycles than basic industrial commodities. Bad weather three years ago pushed up grain prices, which spawned supply increases as farmers increased plantings. Then followed, as the night the day, good weather, excess supply and price collapses. Pork and beef production and prices have similar but longer cycles due to the longer breeding cycles of animals.

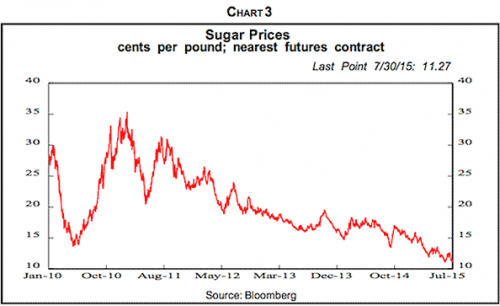

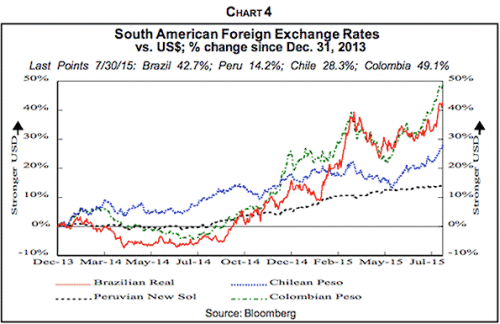

Sugar prices have also nosedived in recent years (Chart 3). Cane sugar can be grown in a wide number of tropical and subtropical locations and supply can be expanded quickly. Like other Latin American countries, Brazil – the world’s largest sugar producer – enjoyed the inflow of money generated from the Fed’s quantitative easing. But that ended last year and in combination with falling commodity prices, those countries’ currencies are plummeting (Chart 4). So Brazilian producers are pushing exports to make up for lower dollar revenues as prices fall, even though they receive more reals, the Brazilian currency that has fallen 33% vs. the buck in the last year since sugar is globally priced in dollars.

Oil Prices

Crude oil prices started to decline last summer, but most observers weren’t aware that petroleum and other commodity prices were falling until oil collapsed late in the year. With slow global economic growth and increasing conservation measures, energy demand growth has been weak. At the same time, output is climbing, especially due to U.S. hydraulic fracking and horizontal drilling. So the price of West Texas Intermediate crude was already down 31% from its peak, to $74 per barrel by late November.

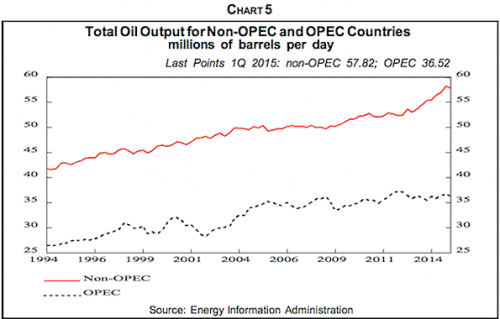

Cartels are set up to keep prices above equilibrium. That encourages cheating as cartel members exceed their quotas and outsiders hype output. So the role of the cartel leader—in this case, the Saudis—is to accommodate the cheaters by cutting its own output to keep prices from falling. But the Saudis have seen their past cutbacks result in market share losses as other OPEC and non-OPEC producers increased their output. In the last decade, OPEC oil production has been essentially flat, with all the global growth going to non-OPEC producers, especially American frackers (Chart 5). As a result, OPEC now accounts for about a third of global production, down from 50% in 1979.

So the Saudis, backed by other Persian Gulf oil producers with sizable financial resources—Kuwait, Qatar and the United Arab Emirates—embarked on a game of chicken with the cheaters. On Nov. 27 of last year, while Americans were enjoying their Thanksgiving turkeys, OPEC announced that it would not cut output, and they have actually increased it since then. Oil prices went off the cliff and have dropped sharply before the rebound that appears to be temporary. On June 5, OPEC essentially reconfirmed its decision to let its members pump all the oil they like.

The Saudis figured they can stand low prices for longer than their financially-weaker competitors who will have to cut production first. That list includes non-friends of the Saudis such as Iran and Iraq, which they believe is controlled by Iran, as well as Russia, which opposes the Saudis in Syria. Low prices will also aid their friends, including Egypt and Pakistan, who can cut expensive domestic energy subsidies.

The Saudis and their Persian Gulf allies as well as Iraq also don’t plan to cut output if the West’s agreement with Iran over its nuclear program lifts the embargo on Iranian oil. As much as another million barrels per day could then enter the market on top of the current excess supply of two million barrels a day.

The Chicken-Out Price

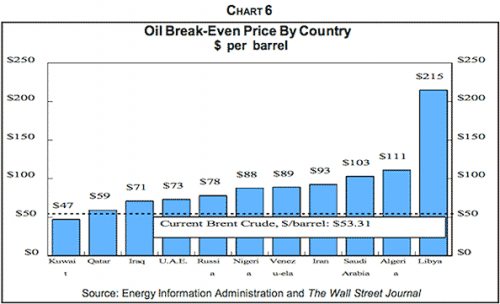

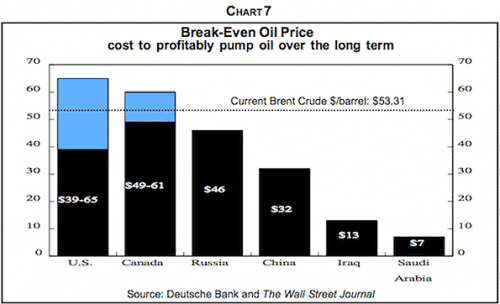

What is the price at which major producers chicken out and slash output? It isn’t the price needed to balance oil-producer budgets, which run from $47 per barrel in Kuwait to $215 per barrel in Libya (Chart 6). Furthermore, the chicken-out price isn’t the “full-cycle” or average cost of production, which for 80% of new U.S. shale oil production is around $69 per barrel.

Fracker EOG Resources believes that at $40 per barrel, it can still make a 10% profit in North Dakota as well as South and West Texas. Conoco Phillips estimates full-cycle fracking costs at $40 per barrel. Long-run costs in the Middle East are about $10 per barrel or less (Chart 7).

In a price war, the chicken-out point is the marginal cost of production – the additional costs after the wells are drilled and the pipelines laid – it’s the price at which the cash flow for an additional barrel falls to zero. Wood Mackenzie’s survey of 2,222 oil fields globally found that at $40 per barrel, only 1.6% had negative cash flow. Saudi oil minister Ali al-Naimi said even $20 per barrel is “irrelevant.”

We understand the marginal cost for efficient U.S. shale oil producers is about $10 to $20 per barrel in the Permian Basin in Texas and about the same on average for oil produced in the Persian Gulf. Furthermore, financially troubled countries like Russia that desperately need the revenue from oil exports to service foreign debts and fund imports may well produce and export oil at prices below marginal costs—the same as we explained earlier for copper producers. And, as with copper, the lower the price, the more physical oil they need to produce and export to earn the same number of dollars.

Falling Costs

Elsewhere, oil output will no doubt rise in the next several years, adding to downward pressure on prices. U.S. crude oil output is estimated to rise over the next year from the current 9.6 million level. Sure, the drilling rig count fell until recently, but it’s the inefficient rigs – not the new horizontal rigs that are the backbone of fracking – that are being sidelined. Furthermore, the efficiency of drilling continues to leap. Texas Eagle Ford Shale now yields 719 barrels a day per well compared to 215 barrels daily in 2011. Also, Iraq’s recent deal with the Kurds means that 550,000 more barrels per day are entering the market. OPEC sees non-OPEC output rising by 3.4 million barrels a day by 2020.

Even if we’re wrong in predicting further big drops in oil prices, the upside potential is small. With all the leaping efficiency in fracking, the full-cycle cost of new wells continues to drop. Costs have already dropped 30% and are expected to fall another 20% in the next five years. Some new wells are being drilled but hydraulic fracturing is curtailed due to current prices. In effect, oil is being stored underground that can be recovered quickly later on if prices rise Closely regulated banks worry about sour energy loans, but private equity firms and other shadow banks are pouring money into energy development in hopes of higher prices later. Private equity outfits are likely to invest a record $21 billion in oil and gas start-ups this year.

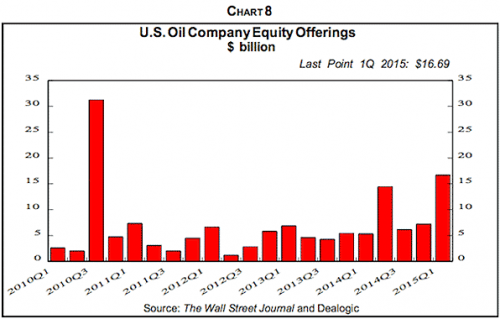

Earlier this year, many investors figured that the drop in oil prices to about $45 per barrel for West Texas Intermediate was the end of the selloff so they piled into new equity offerings (Chart 8), especially as oil prices rebounded to around $60. But with the subsequent price decline, the $15.87 billion investors paid for 47 follow-on offerings by U.S. and Canadian exploration and production companies this year were worth $1.41 billion less as of mid-July.

Dollar Effects

Commodity prices are dropping not only because of excess global supply but also because most major commodities are priced in dollars. So as the greenback leaps, raw materials are more expensive and therefore less desirable to overseas users as well as foreign investors. Investors worldwide rushed into commodities a decade ago as prices rose and many thought the Fed’s outpouring of QE and other money insured soaring inflation and leaping commodity prices as the classic hedge against it. Many pension funds and other institutional investors came to view them as an investment class with prices destined to rise forever. In contrast, we continually said that commodities aren’t an investment class but a speculation, even though we continue to use them in the aggressive portfolios we manage.

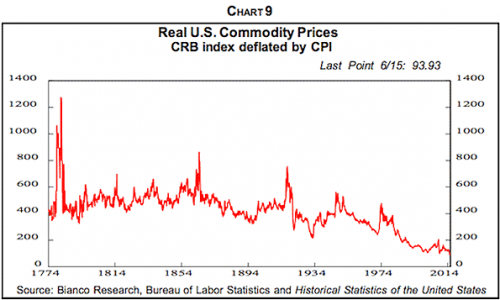

We’ve written repeatedly that anyone who thinks that owning commodities is a great investment in the long run should study Chart 9, which traces the CRB broad commodity index in real terms since 1774. Notice that since the mid-1800s, it’s been steadily declining with temporary spikes caused by the Civil War, World Wars I and II and the 1970s oil crises that were soon retraced. The decline in the late 1800s is noteworthy in the face of huge commodity-consuming development then: In the U.S., the Industrial Revolution and railroad-building were in full flower while forced industrialization was paramount in Japan.

At present, however, investors are fleeing commodities in favor of the dollar, Treasury bonds and other more profitable investments. Gold is among the shunned investments, and hedge funds are on balance negative on the yellow metal for the first time, according to records going back to 2006. Meanwhile, individual investors have yanked $3 billion out of precious metals funds.

Commodity Price Outlook

Commodity prices are under pressure from a number of forces that seem likely to persist for some time.

- Sluggish global demand due to continuing slow economic growth.

- Huge supplies of minerals and other commodities due to robust investment a decade ago.

- Chicken games being played by major producers in the hope that pushing prices down with increasing supply will force weaker producers to scale back. This is true of the Saudis in oil and hard rock miners in iron ore.

- Developing country commodity exporters’ needs for foreign exchange to service foreign debt. So the lower the prices, the more physical commodities they export to achieve the same dollars in revenue. This further depresses prices, leading to increased exports, etc. Copper is a prime example.

- Increased production to offset the effects on revenues from lower prices, which further depresses prices, etc. This is the case with Brazilian sugar producers.

- The robust dollar, which pushes up prices in foreign currency terms for the many commodities priced in dollar terms. That reduces demand, further depressing prices.

It’s obviously next to impossible to quantify the effects of all these negative effects on commodity prices. The aggregate CRB index is already down 57% from its July 2008 pinnacle and 45% since the more recent decline commenced in April 2011. To reach the February 1998 low of the last two decades, it would need to drop 43% from the late July level, but there’s nothing sacred about that 1998 number. In any event, ongoing declines in global commodity prices will probably renew the deflation evidence and fears that were prevalent throughout the world early this year. And they might prove sufficient to deter the Fed from its plans to raise interest rates before the end of the year.

SUBSCRIBE TO GARY SHILLING’S INSIGHT AND YOU’LL RECEIVE:

12 MONTHLY REPORTS (25-35 PAGES) VIA E-MAIL FOR $335

($375 VIA REGULAR MAIL)

PLUS

A FREE COPY OF OUR JANUARY 2015 INSIGHT FEATURING

ALL OF OUR INVESTMENT THEMES FOR 2015

PLUS

A FREE SPECIAL REPORT DETAILING GARY SHILLING’S OUTLOOK

FOR THE U.S. ECONOMY

TO SUBSCRIBE, CALL US AT 1-888-346-7444 OR 973-467-0070.

OR E-MAIL US AT INSIGHT @ AGARYSHILLING.COM.

BE SURE TO MENTION OUTSIDE THE BOX TO GET YOUR FREE COPY OF OUR JANUARY 2015 INSIGHT AS WELL AS THE FREE SPECIAL REPORT.

(THIS OFFER IS AVAILABLE ONLY TO NEW SUBSCRIBERS)

The article Outside the Box: Commodity Weakness Persists was originally published at mauldineconomics.com.

Related podcast interview:

Dr. Gary Shilling: The Era of Slow Growth Is Not Over – 30 Year Treasury Bond Could Hit 2% CLICK HERE to subscribe to the free weekly Best of Financial Sense Newsletter .

The uranium sector has been waiting a long time for this week. When one of the world’s most important markets for the metal has finally come back online.

That’s Japan. Where the long-awaited restart of the country’s nuclear reactor fleet officially began yesterday.

Major utility Kyushu Electric Power reported that it flipped the switch on the Sendai number one power plant in southern Japan on Tuesday. With the reactor now expected to reach full power generation capacity by Friday.

The move is of course a small one in terms of Japan’s overall nuclear capability. With over 40 other reactors around the country still sitting idle, after having been shut down in the wake of the Fukushima incident in 2011.

But the restart shows that Japan is intent on returning to nuclear power. Which could pave the way for other plants to return to service soon — potentially beginning with the number two reactor at Sendai, which lies within the same complex as the plant that was rebooted this week.

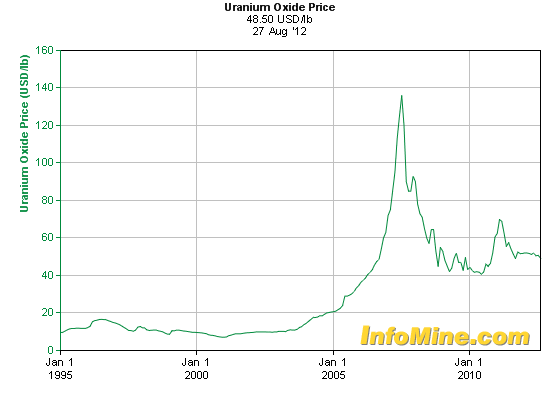

It will be interesting to see if this psychological boost for the nuclear market provides some support for uranium prices. Which have been languishing around $35 per pound since late April.

Prior to that, announcements about potential nuclear restarts in Japan had prompted notable rallies in the uranium price. Including a rapid jump to $44 in late 2014 — and a test of $40 this past April.

If we do see a similar rise in the price based on this week’s restart, it could create a firmer floor. Potentially leading to a more-sustained rally in the metal.

That would be especially true if more Japanese reactors come online over the coming months. A scenario that is likely — with the restart of the Sendai number two plant currently scheduled for October.

All of which would be welcome news for the commodities complex, given that uranium is one of the only metals holding steady in terms of price lately.

Here’s to a bright spot,

Dave Forest

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair