Energy & Commodities

As stated previously, asset monetization by small E&P operators will start in earnest in the second half of this year out of cash flow necessity. Most, if not all, smaller market capitalization companies, public or private, are still free cash flow negative (operating cash flow less capital expenditure) and only a few of the larger ones are now, or will be, based on guidance. The point is, with volumes languishing (and probably poised to decline) tied to a flat oil futures price curve and with economics marginal at $60 per barrel, many E&P operators find themselves running through hedges in 2015 and still in need to finance their already reduced capital spending.

As stated previously, asset monetization by small E&P operators will start in earnest in the second half of this year out of cash flow necessity. Most, if not all, smaller market capitalization companies, public or private, are still free cash flow negative (operating cash flow less capital expenditure) and only a few of the larger ones are now, or will be, based on guidance. The point is, with volumes languishing (and probably poised to decline) tied to a flat oil futures price curve and with economics marginal at $60 per barrel, many E&P operators find themselves running through hedges in 2015 and still in need to finance their already reduced capital spending.

With Wall Street unwilling to lend anymore and prospects of fall credit line redeterminations looming, further reducing liquidity, it islikely small E&P operators will turn to either mature producing asset sales or, more likely, to undeveloped assets which require more capital spending. We are seeing this being factored into stock prices as we speak, as small cap E&P valuations have collapsed to 4-6 times the Enterprise Value/Earnings Before Interest, Taxes, Depreciation, and Amortization (EV/EBITDA) from 6-8X EV/EBITDA. This not only reflects solvency risk but also the natural course of bringing assets to a price more in line with their underlying sale value.

Wall Street is famous for getting public prices at levels that magically make deals happen and, with better funded E&P companies

trading at substantial premiums vs. the leveraged ones, this is what is occurring. Take the collapse of Goodrich Petroleum (GDP) as a prime example as to what is now taking place and what will continue through the latter half of this year. Here is a company with $100million in liquidity but who continues to be free cash flow negative on current strip pricing in 2015 & 2016. However, it has a capital spending budget of $100 million for 2015 and 2016 and a free cash deficit of $60 million-$80 million in each of 2015 and 2016 depending on asset price assumptions. To plug the hole it hopes to sell its Eagle Ford assets this year.

This isn’t intended to make a case on GDP but to demonstrate the quantifiable ongoing stupidity of perpetuating models that aren’t self-funded which were being fueled by easy money from the Federal Reserve. This also demonstrates how the OPEC strategy of maintaining an oil price ceiling is affecting U.S. E&P companies, forcing a consolidation which I believe will be unprecedented in size and scope. This will eventually improve the industry cash flow break even points, based on improved cost and scale and, as a result, cast doubt over the long term viability of the OPEC strategy. It appears the Saudis, despite being educated here in the US, have neglected their capital market & economic classes as we are witnessing the E&P model self-correcting itself. State run oil companies don’t do this very well and usually fail to adjust to price movements while free market capital-based societies do.

The revival of the US oil industry will occur after the upcoming consolidation and will reduce the number of cost inefficient players as well as the short selling in group while ultimately, self-healing the industry by improving cash flows, given the likelihood of oil remaining below $100. I fully expect valuations to expand in 2016, once the wave of asset sales starts in the months ahead. These operators with plenty of cash will be the biggest beneficiaries.

On a final note, listening to the Federal Reserve yesterday it was clear that the pressure on the dollar rise is being lifted as they now realize that, despite attempts to fudge economic statistics, the US economy is in recession and rate hikes are a farce based on hope and little else. Expect the dollar to weaken considerably, breaching the 2015 lows thus supporting oil prices now and into 2016. This reality is not baked into expectations and the 1-2 percent dollar correction which took many by surprise is only the beginning.

Its all about Copper supply – “The problem is: copper is not being discovered fast enough to meet upcoming demand. A study by Wood Mackenzie found that there will be a 10 million tonne supply deficit by 2028. That’s equal to the annual production of the world’s biggest copper mine (Escondida) multiplied by a factor of ten.”

View the Looming Copper Supply Crunc HERE including full & larger image Analysis

With Oil prices down and dividend percntages up its a good idea to take a look where in Canada future gains can be made – Money Talks Ed.

Introduction

Introduction

The election of a new, more leftist politician in the province of Alberta has some Canadian oil companies starting to look to investments outside of the oil sands province. Canadian Natural Resources (NYSE: CNQ), Canada’s largest heavy oil producer, has three quarters of its assets inside Alberta, but with the prospect of heavier taxation coming down the pike, Canadian Natural is considering a shift of resources, diverting more of its investment to non-Alberta projects. That could see more of a focus not just abroad, but also in the provinces of Saskatchewan and British Columbia.

But the future could also be bright for some of Canada’s eastern provinces.

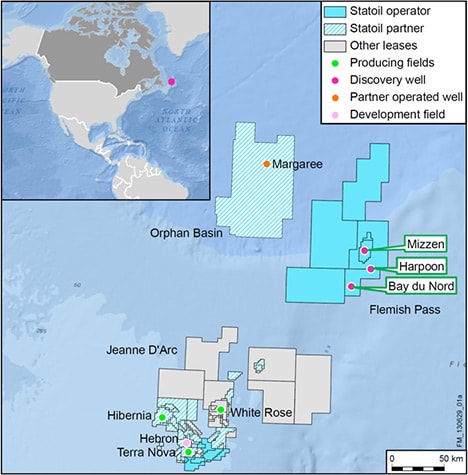

Newfoundland and Labrador

The province of Newfoundland and Labrador on the Atlantic Coast is not normally thought of as a huge growth area for oil production. But the provincial government is looking to overhaul its tax regime in order to attract new investment. The exact terms, expected to be more enticing for the industry, should be revealed in a few weeks. Newfoundland Premier Paul Davis recently spoke at a conference and said that the terms his province will offer will be modeled after successful structures seen in Norway and other high production areas. Newfoundland has a lot riding on the prosperity of the industry, which could help plug a $1.1 billion deficit.

The signature project on offer is the Bay du Nord, a field discovered by Statoil (NYSE: STO)that could hold around 600 million barrels of oil. Located 500 kilometers east of St. John’s, the 2013 discovery was Statoil’s third in the Flemish Pass. Statoil has a 65 percent stake and Husky Energy Inc. (TSE: HSE) controls the remaining 35 percent. The two other discoveries – Mizzen and Harpoon – also have potential for significant oil reserves, but the Bay du Nord is the most promising.

But unlike a lot of other offshore basins around the world, the province of Newfoundland requires that companies allow the provincial energy company, Nalcor Energy, to take a minority stake. That has been a key stumbling block for Statoil, which has thus far been reluctant to commit any financial resources to developing the prospect.

Statoil has been negotiating with the provincial government over development terms and on June 16, 2015, Premier Paul Davis said the two sides are “weeks away” from sealing an agreement. “Statoil wants a deal. We want a deal,” Davis said. “I’m optimistic that we will be successful in reaching terms.”

Statoil came out a day later with a more measured tone, with a company spokesman sayingthat it needs a deal “that provides us with competitive terms given the global fight for capital that we’re in.”

If developed, the Bay du Nord would be Canada’s fifth offshore project. Statoil says it will finish its exploration program by May 2016. A final investment decision on Bay du Nord is unlikely before then. If all goes according to plan, it could begin producing by 2020.

The Bay du Nord has raised excitement about Newfoundland’s offshore potential. There are currently only a handful of rigs plying the cold waters off the coast of Newfoundland, but they have been surprisingly resilient amid the bust in oil prices. That demonstrates the seriousness with which some of the oil players are approaching the Flemish Pass, and the Jeanne D’Arc basin just south of there. The number of rigs operating in the region could in fact double over the next three to five years. In an Executive Report from December 2014, we took an initial look into Newfoundland’s offshore potential.

Nova Scotia

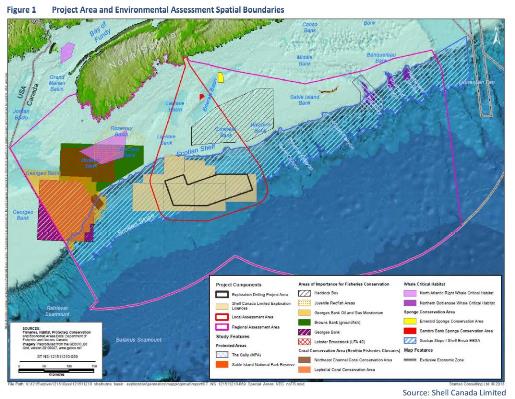

Southwest of Newfoundland is the province of Nova Scotia, not too far from the U.S. state of Maine. Nova Scotia has a much smaller history with oil and gas. The Sable offshore natural gas project run by ExxonMobil (NYSE: XOM) has seen its production suffer from consistent decline. The field is running out and will eventually have to be put to rest.

The province thus far has been a minnow when it comes to hydrocarbon production. But the government hopes for that to change. East of the Nova Scotian coast is a project that Shell Canada, a division of Royal Dutch Shell (NYSE: RDS.A), is targeting. Shell just received an environmental permit to begin exploratory drilling off the coast of Nova Scotia. Drilling could begin before the end of 2015.

Shell plans on drilling seven exploratory wells. It finished 3D seismic surveying of the area and if it moves forward, it will drill two wells in the first phase, with follow up drilling dependent on the preliminary results. Shell spent almost $1 billion for four sections in the Shelburne basin, along with its partners ConocoPhillips (NYSE: COP) and Suncor Energy (NYSE: SU). The latter two companies bought stakes in Shell’s Shelburne program, which should be seen by investors as a vote of confidence in the play.

The provincial government estimates that the Shelburne holds 120 trillion cubic feet of natural gas along with potentially 8 billion barrels of oil.

BP (NYSE: BP) also paid around $1 billion to secure the rights to drill of the coast of Nova Scotia. The four blocks BP won the rights to are 300 kilometers southeast of Halifax. BP completed a seismic survey of its holdings in September 2014, and the results looked good. The British company is in the process of putting together a drilling program, which could begin in 2017.

Nova Scotia has only modest prospects for its oil and gas potential but, having had very little to date, the addition of BP and Shell to the mix is nothing short of momentous for the province. It is still early days, however.

Conclusion

Canada is one of the world’s top oil producers. The bulk of that production is in Alberta’s oil sands. But companies are suddenly looking at other Canadian provinces that are trying to roll out the welcome mat.

Of course, provinces like Nova Scotia and Newfoundland and Labrador do not have the vast reserves that are found in Alberta. But they are also extraordinarily underdeveloped, offering enormous upside potential. Many companies have stayed away due to insufficient data on what lies beneath.

But if a few companies push forward and drill some promising exploration wells, the attention could grow. Statoil’s project in Newfoundland remains the most promising at this point. But it will be up to the provincial government to hash out an attractive deal with Statoil.

Jim Rogers says Choose Farming for Your Family and Finances

Jim Rogers says Choose Farming for Your Family and Finances

and…

Latin America – the Saudi Arabia of Agriculture

“Sometimes we investors can get blinded by statistics. The numbers can hide the truth. But in this case the stats say it all. We all know the world’s population is growing exponentially, and therefore food demand will increase. So who will supply it? Latin America.

Latin America has always been one of the world’s breadbaskets …

According to the Inter-American Institute for Cooperation on Agriculture (IICA), Latin America has 42% of the world’s agricultural ‘spare capacity’. I take these sort of exact projections with a pinch of salt. But if you look at a world map its clear that’s not far off. Latin America has less than 10% of the world’s population but almost 30% of the world’s freshwater supply and 30% of the globe’s spare farmland. In short it’s the Saudi Arabia of agriculture…”

…..read more about Latin America – the Saudi Arabia of Agriculture HERE

…..read more about the Jim Rogers interview “Choose Farming for YOur Family and Finances HERE“

The fallout of the collapse in oil prices has a lot of side effects apart from the decline of rig counts and oil flows.

Oil production in North Dakota has exploded over the last five years, from negligible levels before 2010 to well over a million barrels per day, making North Dakota the second largest oil producing state in the country.

But the bust is leaving towns like Williston, North Dakota stretched extremely thin as it tries to deal with the aftermath. Williston is coping with $300 million in debt after having leveraged itself to buildup infrastructure to deal with the swelling of people and equipment heading for the oil patch. Roads, schools, housing, water-treatment plants and more all cost the city a lot of money, expected to be paid off with revenues from oil production that are suddenly not flowing into local and state coffers the way they once were.

Williams County Commissioner Dan Kalil says that a lot of unemployed people who flocked to North Dakota are left in the wake of the bust, something that the local government has to sort out. “We attracted everyone who had failed in Sacramento, everyone who failed in Phoenix, everyone who failed in Las Vegas, everybody who had failed in Houston, everyone who failed in Florida,” Kalil said in a June 3 interview with WHQR.org. “And they all came here with unrealistic expectations. And it’s really frustrating for those of us left to clean up the mess.”

Output is still only slightly off its all-time high of 1.2 million barrels per day, which it hit in December 2014. But more declines are expected with drillers pulling their rigs and crews from the field. Rig counts in North Dakota have fallen to just 76, as of June 12, far below the 130 or so that state officials believe is needed to keep production flat.

But North Dakota was experiencing a lot of the negative side effects of an oil boom even before prices crashed. The massive increase in

drilling brought a huge wave of cash and people to once sleepy towns, fueling a boom not only in oil, but also in violent crime, prostitution, and drug trafficking.

Now the state and the federal government are playing catch up with the crime wave.

A joint effort by the federal government and the state of North Dakota is seeking to crack down on crime in the Bakken. The U.S. Justice Department, in conjunction with North Dakota’s Attorney General, announced the creation of a “strike force” on June 3 that would target organized crime in the oil producing state. The Justice Department stated that the strike force would be targeted at “identifying, targeting and dismantling organized crime in the Bakken, including human trafficking, drug and weapons trafficking, as well as white collar crimes.”

The effort is a direct response to the rise in crime in North Dakota and Montana, which has been fueled by “dramatic influxes in the population as well as serious crimes, including the importation of pure methamphetamine from Mexico and multi-million dollar fraud and environmental crimes.”

The Justice Department says that it has had success in Montana with Project Safe Bakken, a 2013 program under which federal and state authorities prosecuted hundreds of cases. The Strike Force in North Dakota is expected to yield similar results, the feds believe.

With the state’s economy now almost entirely hitched to the fortunes of the oil industry, they are hoping for a rebound. With several smaller drilling companies having been forced out of the market, the discount that Bakken oil traded for relative to WTI has all but vanished, shrinking from several dollars per barrel down to just cents on the barrel. That could provide a floor beneath the price of Bakken crude, which, in the absence of a dramatic price rebound, is at least helpful for some companies.

The bust may not turn to boom again anytime soon, but with WTI now in the $60 territory, many are hoping the worst is over.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair