Catalyst Check: Natural Resources Watchlist at Three Months

At the Cambridge House Canadian Investment Conference in June, The Gold Report Publisher Jason Mallin asked a panel of experts picking a portfolio of stocks with upside potential for the 2014 Streetwise Reports Natural Resources Watchlist what they wanted to see in an equity. As always, Sprott US Holdings Inc. CEO Rick Rule, summed up the ideal beautifully. “We like reality at a discount,” he said. Now that three months have passed, we decided to check in with Rick and co-panelists Joe Mazumdar from Canaccord Genuity and Keith Schaefer from Oil & Gas Investments Bulletin to see how that reality is playing out. You can always check the portfolio in real time at the Portfolio Tracker.

The Gold Report: Joe, some of your picks from the Natural Resources Watchlist have performed quite well. Do you want to give us some updates?

The Gold Report: Joe, some of your picks from the Natural Resources Watchlist have performed quite well. Do you want to give us some updates?

Joe Mazumdar: Junior mining sector equities in the gold space, as proxied for by the Market Vectors Junior Gold Miners ETF (GDXJ:NYSE.MKT), have outperformed gold since the June Cambridge House conference. The inter-period high for gold was $1,335–1,340/ounce ($1,335–1.340/oz), about a 7% return. Gold is down about 3% since the conference, on the back of a strong U.S. dollar.

The benchmark Market Vectors Junior Gold Miners ETF experienced an inter-period high of about $45/share, generating a 30%+ return since the conference. But it is currently flat again. On both metrics, the ETF has outperformed the gold price. Our selections averaged an inter-period high of 50%, which included underperformers (+18–26%) and some significant outperformers (+70–115%). Currently, the average return for our selection since the conference is a more modest 14–15%. [NOTE: Figures cited were current 9/30/14.]

TGR: During that panel discussion, you called explorers a lottery ticket and Cayden Resources Inc. (CYD:TSX.V; CDKNF:OTCQX) was a lottery ticket that paid off. What was your other “lottery ticket” pick?

JM: Exploration stories tend to be for the more risk-tolerant investors, potentially an “educated” guess rather than a lottery ticket. Our other exploration story was Cordoba Minerals Corp. (CDB:TSX.V). Cordoba Minerals underperformed, both with respect to inter-period highs (+18%) and current return (-54%) since the June conference. A diamond drilling program (2,000 meters [2,000m]) began at the San Matias copper-gold project in Colombia in mid-July 2014, targeting anomalies from a 5,000m, shallow hole, rotary air blast (RAB) drill program. Results are still pending. The only reported results were from RAB drilling at the Costa Azul prospect, which returned 19m grading 0.74 grams/ton gold (0.74 g/t) and 0.32% copper in early August 2014.

Downward pressure on the stock is, in part, due to the lack of news flow. We consider this to be a long-term exploration play, seeking to prove up a cluster of gold-rich porphyry systems that have returned up to 101m grading 1.0% Cu and 0.54 g/t Au from previous drilling. In terms of infrastructure, its location in the northern part of Colombia, at a low elevation with two operating open pit mines located nearby and abundant roads, ports and power, is also attractive.

TGR: What about the more developed picks you have under coverage? The Watchlist was all about catalysts. Did these companies hit their catalysts or is there good news to come?

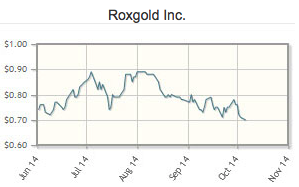

JM: Roxgold Inc. (ROG:TSX.V) is well financed to production at its Yaramoko gold project in Burkina Faso, West Africa, expected by the first half of 2016. The catalysts are a blend of milestones from derisking its development timeline and quantifying the upside on its substantial land package. The company has managed to deliver on both fronts since the conference.

With respect to the development timeline, Roxgold derisked some of the financing, technical and execution risk by securing a US$75 million (US$75M) project debt facility, having its environment and social impact assessment approved, and awarding the underground mining contracting to a reputable firm with relevant underground experience in West Africa. Also, on the exploration front, the drill program at Bagassi South intersected 39.6 g/t gold over 4.5m. We believe Roxgold will continue to quantify the upside on its land package.

Despite these releases, the stock underperformed the Market Vectors Junior Gold Miners ETF with respect to its inter-period high (+23% versus +30%), but has outperformed it since (+5.6% versus +0.4%). Some of the drag on the stock may be related to additional financing required to bring the project into production. We have modeled an additional equity financing to support the project’s development.

In our opinion, few projects offer the high internal rate of return that the Yaramoko project does due to its high grade (>10 g/t Au) and low throughput (740–750 tons per day), requiring low upfront capital (US$110–120M) to get it into production. The high return should attract investors to the name in a volatile gold price environment. We have Roxgold on our Canaccord Genuity Focus List.

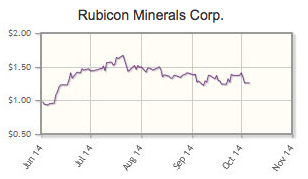

Rubicon Minerals Corp. (RBY:NYSE.MKT; RMX:TSX) is financed to go into production in H2/15 at its wholly-owned Phoenix gold project (F2 Zone), which lies within the highly sought Red Lake District of northwest Ontario. Similar to Roxgold, Rubicon Minerals has two streams of catalysts. The catalysts are related to production timeline and drilling, both infill and definition, to better define the mineable resource.

Since the June conference, to further quantify the upside potential, the company raised additional funds (CA$12M in flow-through financing) to support exploration, and added a new vice president of exploration. Recently, the company announced an intersection of 136.5 g/t Au over 4m from the infill program, which has found additional mineralization outside currently modeled stope blocks. On the development front, Rubicon continued to maintain its guidance for production by mid-2015, in line with our forecast. Preproduction capital left to spend is approximately CA$132M. As of the end of August 2014, the company had about CA$158M in cash, with an additional US$45M expected from its streaming transaction with Royal Gold (RGL:TSX).

Rubicon Minerals easily outperformed the Market Vectors Junior Gold Miners ETF, both in the inter-period high (+68% versus +30%) and to date (+31% versus +0.4%), as Phoenix represents a high grade (8.0 g/t Au) underground gold project that is well financed to near-term production in a prime jurisdiction) and a highly sought gold district.

Dalradian Resources Inc. (DNA:TSX) is an advanced explorer that is metamorphosing into a developer at its wholly owned Curraghinalt high-grade (8.0 g/t Au) underground gold project in Northern Ireland.

Dalradian Resources underperformed the Market Vectors Junior Gold Miners ETF both in the inter-period high (+26% versus +30%) and to date (-8% versus +0.4%), as the company had to await financing. It raised CA$27M in late July 2014 to fund its underground exploration program (CA$30M, 12–15 months), which will underpin a prefeasibility study in H2/15. On a positive note, the financing was both upsized and overallotted. Not many junior mining companies have experienced demand on that level in 2014.

The underground exploration program will verify continuity of grade and thickness of the gold-bearing structures, provide confidence in the chosen mining method as it assesses underground geotechnical and hydrogeological conditions, and generate samples for metallurgical testing. These derisking catalysts will combine with an updated scoping study expected in Q4/15, based on the 2014 resource update. From a permitting perspective, the impacts of underground mining will be simulated during the underground exploration program.

We remain concerned about the usage of cyanide in Northern Ireland, and have removed it from our modeled flow sheet. In our project plan for Curraghinalt, the project produces gold through a gravity circuit and a flotation circuit, generating a gold-bearing concentrate that is shipped overseas, thus avoiding the use of cyanide at the site, which we believe would be less problematic to permit.

We have modeled the company as a takeout candidate, but only after a potential suitor would be confident that an underground mining operation can work on that scale in Northern Ireland, with a prefeasibility complete and a permit in hand.

TGR: Is the recent $590,000 grant from the Northern Ireland government a good sign on the permitting front?

JM: Yes. The government had already granted the permit for bulk tonnage sampling in early 2014. And the recent grant is a positive sign that the government wants jobs in Northern Ireland, and believes that this is a good project with a capable management team that can generate meaningful local employment.

TGR: It has been three months since that conference. If you were to pick again, is there another company you would have added to the list?

JM: Hindsight is 20-20. One company that I visited recently that I would have added isConstantine Metal Resources Ltd. (CEM:TSX.V), which is advancing the Palmer massive volcanogenic massive sulphide (VMS) exploration project in southeast Alaska.

Constantine recently intersected 89m (calculated true width) grading 0.79% copper, 5.03% zinc, 21.2 g/t Ag and 0.32 g/t Au that tested an electromagnetic (geophysical) conductor at the South Wall zone at the Palmer volcanogenic massive sulphide (VMS) deposit in southeast Alaska. Dowa Metals & Mining Co. Ltd., a Japanese mining and smelting company, is earning in to a 49% stake by spending US$22M over a four-year earn in schedule. 2014 is the second year of the earn-in. The attraction is the quality of the potential zinc concentrate, and the proximity to infrastructure. Drilling is seeking to increase the tonnage at the project to a critical 8–10 million ton (8–10 Mt) threshold. The project is located on a significant north-south trending belt called the Alexander Terrane, which stretches from British Columbia, through Alaska, and back into British Columbia. The belt also hosts the Windy Craggy deposit and the Greens Creek mine, an underground VMS deposit operated by Hecla Mining Co. (HL:NYSE).

I do not cover the company, but given the forecast deficits in the zinc market, high-grade projects such as the Palmer project (4.75 Mt grading 1.84% copper, 4.57% zinc, 29 g/t silver and 0.28 g/t gold) that are close to infrastructure—a half-hour from the deep-water port at Haines, Alaska—will be in demand. Hence Dowa’s interest—but note that Constantine retains a majority interest (51%) after the earn-in.

TGR: It sounds like Constantine has a lot more going for it than your average lottery ticket.

JM: In the current environment, grassroots exploration companies are finding it difficult to attract financing to generate catalysts. Projects that are more advanced may be a better option in the near to medium term; projects that have the financing support to generate the catalysts required to move forward.

TGR: Rick, would you update us on the companies you called out on the panel?

Rick Rule: Sprott Inc. (SII:TSX) has $10 billion ($10B) in investments, overwhelmingly in the natural resources space. When the sector recovers—as it has five times in my career—this is a portfolio that will do very well.

Devon Energy Corp. (DVN:NYSE) has done very well since we bought it a year and a half ago. Depending on your opinion of the U.S. economy, you might put a trailing stop on it, or sell it now. I believe energy prices are soft right now because I don’t believe we are seeing a U.S. recovery, and oil and gas prices are leveraged to the economy. As a company, Devon is making the right moves internally. It is shedding nonperforming assets and holding down costs, but it can’t control energy prices.

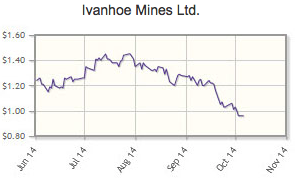

Ivanhoe Mines Ltd. (IVN:TSX) is a stock for an investor who is financially and psychologically capable of holding an equity for two, three or four years. This isn’t one that is going to move up in three months. It is up against a lot of challenges, including platinum and palladium group metals (PGM) commodity prices, country risk, and the ability to raise money in the current environment. I will tell you that PGM prices have to go up. And CEO Robert Friedland is a man who has succeeded before in difficult geographic locations. He can raise the millions required. Extraordinary stories fund themselves.

But Ivanhoe is going to take time. This is not a stock for traders. This is for long-term investors who can hold until the time is right.

TGR: Keith, would you give us an update on your companies?

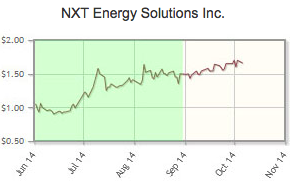

Keith Schaefer: NXT Energy Solutions Inc. (SFD:TSX.V; NSFDF:OTCBB) is an airborne geological survey company that finds oil and gas reservoirs. The stock is moving, but not because of any news the company has put out. The Street is excited about Mexico’s planned liberalization of the oil industry, anticipating that opening the sector to foreign investment will mean bigger contracts for services like airborne geological surveys, and those contracts being awarded faster. It is a powerful story. As I said in June, the company has a neat technology that is proven out in the field.

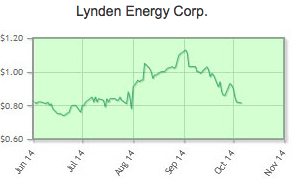

Lynden Energy Corp. (LVL:TSX.V) is an oil and gas exploration company with the Wolfberry and Mitchell Ranch projects in Texas. The stock had a great run in August for two reasons. Management has been vocal about wanting to sell, and the company owns five–six chunks of land in the Permian Basin in West Texas, the epicenter of some huge wells that have recently been drilled. The Street likes this area all of a sudden. It really is a great land package.

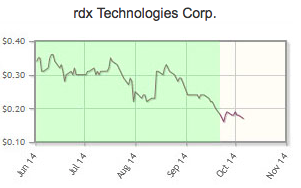

rdx Technologies Corp. (RDX:TSX.V) has a system that takes waste fluid streams from oil and gas operations, and turns that into diesel fuel. It is trying to franchise that technology and grow the company. But it has a lot of work ahead of it. It has had challenges and the stock price reflects that.

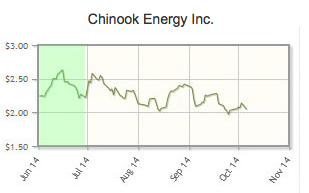

Chinook Energy Inc. (CKE:TSX.V) is an oil and gas exploration and production company with property in western Canada. Since the panel discussion in June, Chinook delivered on its catalyst, and sold its Tunisian asset. Management is now working on consolidating. The stock has bounced up and down in the $2/share range for the last three months.

TGR: After three months, is there anything you would have said differently from that stage?

KS: What I know now that I didn’t know then is that we were at the top of the market. I would have told everyone to sell everything.

No one can really predict where the market is going. The energy market has been ugly and will have to rebase. But some of these companies could do well in the process.

Joe Mazumdar joined Canaccord Genuity in December 2012 from Haywood Securities, where he also was a senior mining analyst focused on the junior gold market. The majority of his experience is with industry including corporate roles as director of strategic planning, corporate development at Newmont in Denver and senior market analyst/trader at Phelps Dodge in Phoenix. Mazumdar worked in technical roles for IAMGold in Ecuador, North Minerals in Argentina/Chile and Peru, RTZ Mining and Exploration in Argentina and MIM Exploration and Mining in Queensland, Australia, among others. Mazumdar has a Bachelor of Science degree in geology from the University of Alberta, a Master of Science degree in geology and mining from James Cook University and a Master of Science degree in mineral economics from the Colorado School of Mines.

Rick Rule, CEO of Sprott US Holdings Inc., began his career in the securities business in 1974. He is a leading American retail broker specializing in mining, energy, water utilities, forest products and agriculture. His company has built a national reputation on taking advantage of global opportunities in the oil and gas, mining, alternative energy, agriculture, forestry and water industries. Rule writes a free, thrice-weekly e-letter, Sprott’s Thoughts.

Keith Schaefer is editor and publisher of the Oil & Gas Investments Bulletin,which finds, researches and profiles growing oil and gas companies that Schaefer buys himself. He identifies oil and gas companies that have high, or potentially high growth rates, and that are covered by several research analysts. He has a degree in journalism and has worked for several Canadian dailies, but has spent more than 15 years assisting public resource companies in raising exploration and expansion capital.

Want to read more Gold Report interviews like this? Sign up for our free e-newsletter, and you’ll learn when new articles have been published. To see recent interviews with industry analysts and commentators, visit our Streetwise Interviews page.

Related Articles

DISCLOSURE:

1) JT Long conducted this interview for Streetwise Reports LLC, publisher of The Gold Report, The Energy Report, The Life Sciences Report and The Mining Report, and provides services to Streetwise Reports as an employee. She owns, or her family owns, shares of the company mentioned in this interview: None.

2) Joe Mazumdar: I own, or my family owns, shares of the following companies mentioned in this interview: None. I personally am, or my family is, paid by the following companies mentioned in this interview: None. My company has a financial relationship with the following companies mentioned in this interview: Dalradian Resources Inc. and Rubicon Minerals Corp. I was not paid by Streetwise Reports for participating in this interview. Comments and opinions expressed are my own comments and opinions. I determined and had final say over what companies would be included in the interview based on my research, understanding of the sector and interview theme. I had the opportunity to review the interview for accuracy as of the date of the interview and am responsible for the content of the interview.

3) Keith Schaefer: I own, or my family owns, shares of the following companies mentioned in this interview: rdx Technologies Corp., NXT Energy Solutions Inc., Chinook Energy Inc. and Lynden Energy Corp. I personally am, or my family is, paid by the following companies mentioned in this interview: None. My company has a financial relationship with the following companies mentioned in this interview: None. I was not paid by Streetwise Reports for participating in this interview. Comments and opinions expressed are my own comments and opinions. I had the opportunity to review the interview for accuracy as of the date of the interview and am responsible for the content of the interview. I determined and had final say over what companies would be included in the interview based on my research, understanding of the sector and interview theme.

4) Rick Rule: I own, or my family owns, shares of the following companies mentioned in this interview: Sprott Inc. I personally am, or my family is, paid by the following companies mentioned in this interview: Sprott Inc. My company has a financial relationship with the following companies mentioned in this interview: None. Sprott funds owns shares of Randgold Resources Ltd., Goldcorp Inc., Potash Corp., Cameco Corp., BHP Billiton Ltd., Devon Energy Corp. and Ivanhoe Mines Ltd. I was not paid by Streetwise Reports for participating in this interview. Comments and opinions expressed are my own comments and opinions. I had the opportunity to review the interview for accuracy as of the date of the interview and am responsible for the content of the interview. I determined and had final say over what companies would be included in the interview based on my research, understanding of the sector and interview theme.

5) The following companies mentioned in the interview are sponsors of Streetwise Reports: Cayden Resources Inc. The companies mentioned in this interview were not involved in any aspect of the interview preparation or post-interview editing so the expert can speak independently about the sector. Streetwise Reports does not accept stock in exchange for its services.

6) Interviews are edited for clarity. Streetwise Reports does not make editorial comments or change experts’ statements without their consent.

7) The interview does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer.

8) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their families are prohibited from making purchases and/or sales of those securities in the open market or otherwise during the up-to-four-week interval from the time of the interview until after it publishes.

South Africa has the world’s richest mineral deposits, with $3.3 trillion in platinum, gold,

South Africa has the world’s richest mineral deposits, with $3.3 trillion in platinum, gold,

Horizontal drilling and fracking have opened new opportunities for investing in domestic energy, whether for pure-play explorers in developing shales, producers in mature areas, or service companies opening up the monster wells. Oil and Gas Investor Editor-in-Chief Leslie Haines has been following the revolution for nine years, and agreed to share with readers of

Horizontal drilling and fracking have opened new opportunities for investing in domestic energy, whether for pure-play explorers in developing shales, producers in mature areas, or service companies opening up the monster wells. Oil and Gas Investor Editor-in-Chief Leslie Haines has been following the revolution for nine years, and agreed to share with readers of  The monthly U.S. Energy Information Administration (EIA) reports show that in H1/14, U.S. gas natural production alone increased by more than 4 billion cubic feet a day (4 Bcf/d). The bulk is coming from the Northeast, from the Marcellus and Utica plays in Pennsylvania, Ohio and West Virginia. Also, a lot of new natural gas is coming on, in association with oil production in West Texas, in the Permian Basin, and in south Texas, in the Eagle Ford play. While some gas areas might be declining, we’re getting enough new natural gas to offset that decline. In fact, both oil and natural gas production in this country are the highest they’ve been in about 35 years.

The monthly U.S. Energy Information Administration (EIA) reports show that in H1/14, U.S. gas natural production alone increased by more than 4 billion cubic feet a day (4 Bcf/d). The bulk is coming from the Northeast, from the Marcellus and Utica plays in Pennsylvania, Ohio and West Virginia. Also, a lot of new natural gas is coming on, in association with oil production in West Texas, in the Permian Basin, and in south Texas, in the Eagle Ford play. While some gas areas might be declining, we’re getting enough new natural gas to offset that decline. In fact, both oil and natural gas production in this country are the highest they’ve been in about 35 years. In one basin, you may find the number of formations that can be tapped is quite numerous. In the Permian Basin of West Texas, for example, more than 5,000 vertical feet of pay can be tapped. If you sink three horizontal legs into that well, three different horizons can be fracked and produce from one well. It triples the effect of that well and acreage.

In one basin, you may find the number of formations that can be tapped is quite numerous. In the Permian Basin of West Texas, for example, more than 5,000 vertical feet of pay can be tapped. If you sink three horizontal legs into that well, three different horizons can be fracked and produce from one well. It triples the effect of that well and acreage. Sanchez Energy Corp. (SN:NYSE)

Sanchez Energy Corp. (SN:NYSE)