Commodity markets saw big winners and losers this week.

Commodity markets saw big winners and losers this week.

On making (and losing money): I moved to Dallas from West Texas in 1989 worth about $25 million ($25M). I ran that $25M up to $4 billion ($4B) in 2007. 2008 and 2009 were a disaster. I lost $2B. I’ve given away over $1B and have $1B left.

On leveraging the oil and gas renaissance in the U.S.: I launched the Pickens Plan in 2008 because I felt that I was running out of time, and this country desperately needs an energy plan. We’re the only country in the world without one. We use more oil than any other country, 18 million barrels a day (18 MMbpd) with China’s 10 MMbpd a distant second, and we import about half of what we use.

Five years ago, we discovered the biggest gas field in the world, the Marcellus Shale in Pennsylvania. We are now the world’s largest natural gas producer; we have more reserves of natural gas than any other country in the world. That is huge for this country. It’s huge for the world. It is going to change the dynamics of the oil and gas industry. It’s a renaissance that started in the U.S.

We have the cheapest fuel of any country in the world. Our oil here is 10% cheaper. Our natural gas is 75% cheaper. Our gasoline is 50% cheaper. We’re now moving businesses back to the U.S because of cheap energy.

On the challenges to energy independence: The only problem is that this administration hates the oil and gas industry. It doesn’t want to use fossil fuels. Hedge fund manager and environmentalist Thomas Fahr Steyer recently told me he is going to spend $100M to block the Keystone Pipeline and he wants to get rid of all fossil fuels. His plan to replace all that transportation fuel is to ask the government to find an alternative. We’ll see what happens with that.

Some politicians say that we need to export more oil, we should go to Europe and fix the Russian dominance of natural gas, but it’s not doable. We will not have one liquefied natural gas (LNG) export facility until late 2015, over a year from now.

The biggest problem is that this country has never had an energy plan.

On use of the reserve: Go back to the Arab oil embargo in 1973. We were cut off from the Mideast’s oil and it scared the devil out of everybody. In 1974, we passed a law requiring a 750 million barrel (750 MMbbl) Strategic Petroleum Reserve (SPR) in the salt caverns in Louisiana and Mississippi just in case we had another Arab embargo. In the last 40 years, the most we have ever taken out at any one time is 28 MMbbl. So we have over 700 MMbbl in storage, and the greatest amount we’ve taken out at one time is 28 MMbbl. Do we really need that much storage?

It would take 10 years to remove even 400 MMbbl without disrupting the market. Selling that oil would result in a profit, because it was purchased at $28/barrel ($28/bbl) and today oil is $103/bbl. That is a big profit, one of the few big profits I’ve ever seen the government have.

Profits from the reserve could be used to develop energy in America by switching all the heavy-duty trucks to natural gas. A $30,000 tax credit would roughly cover the incremental cost for converting from diesel, which is twice as expensive, to natural gas engines.

The government should use the cheapest fuel for our federal vehicles. That is its fiduciary responsibility. By making sure we use the cheapest fuel—which also happens to be 30% cleaner—we could reduce our imports by 3 MMbpd. That would put a dent in the 4–4.5 MMbpd we import from OPEC.

On funding both sides of the war: Eliminating Middle East imports is important because some portion of the money for oil purchased from OPEC inevitably goes to the Taliban. That’s not really because the Saudis are trying to hurt us; they’re just paying ransom so the Taliban will leave them alone. That means by using Mideast oil, we’re paying for both sides of the war: the Fifth Fleet to protect the world oil transport through the Straits of Hormuz while funding the terrorists that attack those transport ships. And we only get 10% of the oil we are protecting. It makes no sense. That is why I am working so hard for an energy plan.

Porter Stansberry: You have been so successful. Your commodity fund is up 24% this year and your equity fund is up 19%. You are 86 and clearly enjoying life and newly married. Why are you still in the game?

TBP: I love the game. I’m not going to do something I don’t like to do. As long as I can play the game, I’m going to bluff my way through.

PS: I think a lot of people are stuck doing jobs that they don’t love. I tell people all the time, if you don’t love what you do, if you wouldn’t do it for free, then you have no chance at being the best at it.

TBP: Excellent advice.

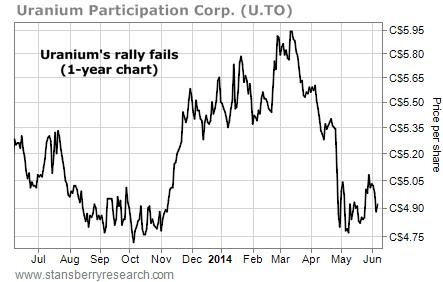

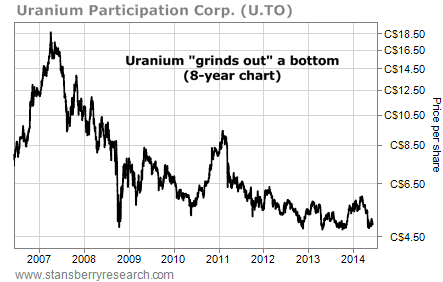

PS: Let’s talk commodities. Would you invest in coal or uranium? These are two energy commodities that have seen their prices plummet.

TBP: Over 40% of the power generation in the U.S. comes from coal. We’re going to have to use coal. A congressman once said to me that he was going to get rid of all coal-fired plants. I responded that if you shut down all the coal-fired plants, you could multiply the price of electric fuel by 10.

PS: They’re doing that in Germany.

TBP: They went to turbines, and they don’t even have good wind.

PS: And they invested in solar, without any sun.

TBP: At the same time France put a moratorium on fracking wells. Then they complain about relying on Russia.

PS: So you would be an investor in coal. What about uranium?

TBP: We have had three failures over the years. Another report on the viability of nuclear is on the way. I can tell you what the executive summary will say. Do not build a nuclear plant on the coast. Do not build it on seismic faults. That’s it. You can put it in stable areas and it works.

PS: So I’ll take that as a yes, you would invest in coal and uranium.

TBP: Not today, but I would, yes. There will be a time to come into both of those. I am not just an oil and gas guy. I’m a guy who wants the best, cleanest energy for America.

PS: Berkshire Hathaway Vice-Chairman Charlie Munger has said that as long as the world agrees to exchange worthless paper for oil, we should let them. To me, it sounds foolish because if you do that long enough, your paper is going to be worthless, and that’s going to cause much bigger problems. I think his argument is nonsensical, but I wondered what you thought about it.

TBP: Of course the paper dollar is worth something.

PS: Less and less every year.

TBP: I haven’t talked to Charlie face-to-face in probably five years, but I can’t agree with Charlie on that.

The Energy Report via Porter Stansberry: Does OPEC have the influence it used to have? Does the Middle East matter anymore?

TBP: It does because OPEC sets the price for oil. Of the 92 MMbbl produced every day in the world, OPEC is producing a third of it. It is big enough, and it is organized and credible. It is a cartel. 30% of oil can set the price by adjusting on spot. Saudi Arabia has made it very clear that it has to have $100/bbl for oil to meet its social commitments. Over half the people don’t work in Saudi Arabia. Theirs is not an economy that provides jobs, so Saudi Arabia has to pay its people.

Now the Iranians are a little bit squirrelly. Credibility is not that important to them. They’ll tell you they have to have about $23/bbl. But they have increased production, and China is cooperating with them. China has an energy plan and imports half its oil. China uses 10 MMbpd and imports 5 MMbpd through deals with Venezuela, Brazil and Iran. China loans them money and gets oil in payment at a discount.

PS: What do you think the chances are, in the next couple years, of finding a really huge shale oil field that can produce a 100 MMbpd well either through technology or luck?

TBP: Slim to none. East Texas was discovered in 1931. It is a huge field. It’s out of the Woodbine sand, but it comes from source rock—the shale reservoirs—that was heated, pressured and squeezed into the trap. The East Texas field is a conventional trap for oil. Even then, we knew the oil was in the shale, but not until George Mitchell, the father of fracking, did we think we could get more than 5% of the gas out of the Barnett Shale. Lo and behold, now we’re going to get 40%. We may get 80% before it’s over.

Audience Question: How long do you think it will take to get natural gas infrastructure in place in the U.S. so that conversions to natural gas engines are viable to the public?

TBP: Actually, it’s there now. I’ve got a natural gas car. I could plug it in in my garage and my fuel costs would be $1/gallon through the gas line that powers my stove. There are plenty of fueling stations in California.

PS: One last question. What’s your favorite way to profit from energy in the stock market today?

TBP: I’d get into the commodities. We’ve done a great job. Why do you think the economy has recovered in the U.S.? It’s all due to energy.

But let me make one request. I’ve got 2.5M people signed up with me in PickensPlan.com. Please join us.

PS: Thank you very, very much for your time.

(Editor’s note: We followed the T. Boone Pickens discussion and a panel discussion on the shale boom with some questions of our own for Porter Stansberry and his associate, Matt Badiali.)

TER: Porter, I would like to ask you to answer the question you asked T. Boone. Based on the new technologies like zipper fracking and the challenge of a lack of infrastructure, how do you suggest gaining exposure to the energy market?

PS: There are a lot of opportunities in the energy sector because as the cost of dry holes disappears and as production methods become more efficient, the cost of production will decline. Eventually that should lead to lower oil prices, which sounds bad at first. But, as long as margins remain reasonably robust, lower total energy prices will actually increase demand substantially. . .and that will power the industry forward for decades, not merely for a period of temporary high prices.

The best way over the next few years to profit from these trends is to gain the arbitrage between the low domestic price of oil and gas and the higher international price. That’s why there’s been an explosion in propane exports. These “refined” products and all of the infrastructure associated with them will do very well over the next three to five years. Firms that are able to vertically integrate from wellhead to export markets will do best. “Capture the arb” will be the strategy that wins in the medium term.

The best way over the longer term to participate in these trends is to focus on buying the most attractive energy resources at the lowest possible price. That’s why we see companies like Devon Energy Corp. (DVN:NYSE), for example, making material changes to their asset base, selling off marginal assets and focusing their production and exploration activities in the highest quality shales close to centers of distribution.

We think Devon is in the midst of a substantial turnaround that will transform the company into one of the country’s large producers of crude oil. Its U.S.-based oil production is now increasing at over a 50% annual pace, and it owns large amounts of acreage in the most attractive area in the two best shale plays in the U.S.—the Permian and the Eagle Ford.

Devon also owns a very large legacy asset, the third largest natural gas reserves in the U.S., mostly located in the in the Barnett Shale. These gas assets are far more valuable than the market currently realizes, as they are the key to the international arbitrage strategy I mentioned earlier. They will become far more attractive to investors as more and more export facilities are built in the U.S.

Thus, with Devon, investors are getting world class (but currently “stranded”) natural gas reserves plus all the liquids growth of a more highly focused shale oil driller like EOG Resources Inc. (EOG:NYSE). Best of all, given its controlling interest in EnLink Midstream LLC (where it owns 70% of the general partner), we also believe that Devon is uniquely vertically integrated to take advantage of all export opportunities, both currently available (with propane) and in the future with crude oil.

Today Devon’s assets trade at a huge discount to the other shale oil drillers. There’s a wide gap between the value we perceive going forward and the market’s current view.

TER: What are some other companies that fit that investing approach?

PS: Energy XXI (EXXI:NASDAQ) fits into the second, longer-term strategy, owning the best assets in good locations. Its strategy is to buy large, existing conventional reservoirs of oil and gas in the shallow Gulf areas and, using new technologies, revive production. It has zero exploration risk. Energy XXI is located very close to the major distribution areas of the Gulf Coast, and it has low production costs because of the conventional nature of the reservoirs. The company also has a kicker. It owns a share in nearly a dozen ultra-deep wells that contain trillions of cubic feet of gas and could also contain huge amounts of oil. If these wells can be put into production, Energy XXI could quickly become a major producer of hydrocarbons. I like this strategy, and because so much investor attention is focused on onshore production right now, good Gulf of Mexico resources have simply been forgotten.

TER: Matt, same question: How will new technologies open new investing opportunities and what companies are well positioned to take advantage of those opportunities?

Matt Badiali: The economics of shale wells are improving every single day. Sometimes it’s due to new techniques like zipper fracking, sometimes it’s due to simply longer horizontal legs and more sand in the fracks. Halcón Resources Corp. (HK:NASDAQ) is a great example of this. It could easily be the next EOG Resources or the next Petrohawk Energy Corp. (HK:NYSE), which BHP Billiton Ltd. (BHP:NYSE) bought for $12.1B. Halcón is the management team from Petrohawk, reunited to do it all again.

T. Boone Pickens is a geologist, entrepreneur in the oil and gas industry and chair of the hedge fund BP Capital Management. He is also the author of “The First Billion is the Hardest: Reflections on a Life of Comebacks and America’s Energy Future.” He is an outspoken advocate for U.S. energy independence and advocates for an energy plan in public appearances and through his Pickens Plan website.

Porter Stansberry founded Stansberry & Associates Investment Research, a private publishing company based in Baltimore, Maryland, in 1999. His monthly newsletter, Stansberry’s Investment Advisory, deals with safe-value investments poised to give subscribers years of exceptional returns. Stansberry oversees a staff of investment analysts whose expertise ranges from value investing to insider trading to short selling. Together, Stansberry and his research team do exhaustive amounts of real-world independent research. They’ve visited more than 200 companies in order to find the best low-risk investments. Prior to launching Stansberry & Associates Investment Research, Stansberry was the first American editor of the Fleet Street Letter, the oldest English-language financial newsletter.

Matt Badiali is the editor of the S&A Resource Report, a monthly investment advisory that focuses on natural resources, including silver, uranium, copper, natural gas, oil, water and gold. He is a regular contributor to Growth Stock Wire, a free pre-market briefing on the day’s most profitable trading opportunities. Badiali has experience as a hydrologist, geologist and consultant to the oil industry. He holds a master’s degree in geology from Florida Atlantic University.

Read what other experts are saying about:

Want to read more Energy Report interviews like this? Sign up for our free e-newsletter, and you’ll learn when new articles have been published. To see recent interviews with industry analysts and commentators, visit our Streetwise Interviews page.

Related Articles

- Porter Stansberry: Are You Playing the Right Energy Trend?

- Leave No Rock Unturned to Find Natural Resource Stocks with Game-Changing Catalysts

- What To Look For in an E&P Company: Foucaud’s Secrets for International Investing

DISCLOSURE:

1) The following companies mentioned in the interview are sponsors of Streetwise Reports: Energy XXI. Streetwise Reports does not accept stock in exchange for its services.

2) Porter Stansberry: I own, or my family owns, shares of the following companies mentioned in this interview: None. I personally am, or my family is, paid by the following companies mentioned in this interview: None. My company has a financial relationship with the following companies mentioned in this interview: None. I was not paid by Streetwise Reports for participating in this interview. Comments and opinions expressed are my own comments and opinions. I had the opportunity to review the interview for accuracy as of the date of the interview and am responsible for the content of the interview.

3) Matt Badiali: I own, or my family owns, shares of the following companies mentioned in this interview: None. I personally am, or my family is, paid by the following companies mentioned in this interview: None. My company has a financial relationship with the following companies mentioned in this interview: None. I was not paid by Streetwise Reports for participating in this interview. Comments and opinions expressed are my own comments and opinions. I had the opportunity to review the interview for accuracy as of the date of the interview and am responsible for the content of the interview.

4) Interviews are edited for clarity. Streetwise Reports does not make editorial comments or change experts’ statements without their consent.

5) The interview does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer.

6) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their families are prohibited from making purchases and/or sales of those securities in the open market or otherwise during the up-to-four-week interval from the time of the interview until after it publishes.