Energy & Commodities

Or, how long does it take the Street to identify an elephant in the room? Apparently the answer to that question is a time period longer than should be the case. As portrayed in the chart below, Agri-Food prices have been rising fairly dramatically thus far this year. With an average gain of about 10% since the beginning of the year, eating is becoming far more expensive. Rather than a short-term phenomenon, higher prices for Agri-Foods over time are part of the future, an unavoidable one.

Prices rise for Agri-Foods when demand grows faster than supply. The world wants to eat more dairy products, butter included, and broilers, or table chicken. Supply simply does not respond in short-term to that increased demand. Response to higher demand by the marketplace is simply to raise prices for the commodity. A milk cow does not check the internet each morning for wholesale price of butter, and decide to produce more milk fat in response to higher quotes. And you can be assured that laying hens to do not try to lay more eggs when chicken prices are rising.

Prices rise for Agri-Foods when demand grows faster than supply. The world wants to eat more dairy products, butter included, and broilers, or table chicken. Supply simply does not respond in short-term to that increased demand. Response to higher demand by the marketplace is simply to raise prices for the commodity. A milk cow does not check the internet each morning for wholesale price of butter, and decide to produce more milk fat in response to higher quotes. And you can be assured that laying hens to do not try to lay more eggs when chicken prices are rising.

As chart to right portrays, prices for Agri-Commodities have been rising for quite some time, and recently reached a record high. That history suggests that something different has been happening with Agri-Commodity prices. That something different is that world demand for food is beginning to bump up against the world’s long-term ability to supply food. Higher prices for beef will not change the reality that it takes about nine months for a calf to be born. The internet cannot change that fact. Higher prices for Agri-Commodities will not create another acre of arable land in either China or the U.S.

In top chart prices per pound for U.S. broilers, table chicken, are plotted. Those prices recently hit another new high. Chicken is both a price bargain relative to beef for consumers and an economic bargain to the world. To produce a kilogram of chicken requires slightly more than two kilograms of grain while with beef thirteen kilograms are required. (Agrimoney(2013), p. 150) Higher demand for chickens means that demand for feed grains should rise. As the price of soybeans shows in the second chart, strong global demand for animal feed has pushed up the prices of soybeans. Regardless of growth rate of China’s GDP, the chickens in that country still eat every day. More than half of soybean harvest is destined to become chicken feed. Soybeans

And we can assure you that the internet cannot produce a single soybean. Still requires a farmer in the field using equipment, fertilizer, and seed. Still requires someone to gather, process and move those soybeans around the world in order to feed global consumers. In that process money, our real interest, flows from consumers to farmers. Agri-Equities are the ultimate benefit of this flow of money, and they remain largely ignored by the investment community.

Ned W. Schmidt,CFA is publisher of The Agri-Food Value View, a monthly exploration of the Agri-Food Super Cycle, and The Value View Gold Report, a monthly analysis of the real alternative currency. To contract Ned or to learn more, use either of these links: www.agrifoodvalueview.com or www.valueviewgoldreport.com

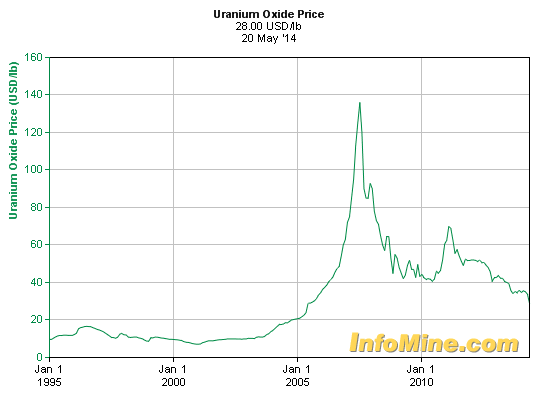

The news on uranium mine closures seems to be coming regularly now.

Last week, I wrote about major producer Cameco delaying its Millennium mine in Saskatchewan. And this week we got news of another high-profile producer that’s being lost to the market.

That’s the Imouraren mine in Niger. Being developed by French nuclear major Areva.

Imouraren had been scheduled to open this year, alongside Areva’s two existing mines in Niger. But sources in Niger’s mining ministry were quoted as saying that development of the project will now be suspended–as part of a new production agreement Areva is signing in the country.

Once again, the reason for the deferral is reportedly simple economics. With Reuters noting that Imouraren won’t proceed “until uranium prices improve.”

This is another significant loss for global uranium supply. The Imouraren mine had been slated to be a sizeable one–with a total resource of more than 100 million pounds. Production capacity had been announced at over 11 million pounds of uranium yearly.

None of that will now see the light of day. At least not for the foreseeable future.

It’s possible that some of the delay is a result of politics. With Areva lately having been locking in a disagreement with Niger’s government about fiscal terms for uranium production in the country.

But it’s also completely plausible the delay is simply a matter of low prices. Fitting with the pattern we’ve seen lately of almost every major uranium development globally being shelved. From Canada to Africa to Kazakhstan, there just doesn’t seem to be any appetite for new projects in current market environment.

That’s not surprising at today’s prices. Which see uranium oxide sitting at an ultra-low $28 per pound on the spot market.

Few producers new or old are making money at these rates. We’ll see how long supply can hold out if mining developments keep disappearing.

Here’s to a shrinking market,

dforest@piercepoints.com / @piercepoints / Facebook

![]()

Separate and Unequal

In a note last week, I discussed the danger in assessing all critical metals together rather than individually. I am just back from Montreal where I chaired the 6th Annual Lithium Supply and Markets Conference hosted by Industrial Minerals.

Of the many takeaways, this idea of analyzing the prospects for these metals individually is evident in the case of lithium.

In the wake of Tesla’s (TSLA:NASDAQ) Gigafactory announcement, many lithium junior companies, who were left for dead, have been given a new lease on life. There are challenges that must be overcome to make the Gigafactory a reality, and am still unconvinced that a junior mining company not close to production can participate and benefit its shareholders, but we shall see. On the other hand, I try and make a habit of betting on successful visionaries like Elon Musk.

It is clear that the automotive sector is the real growth driver for lithium, as David Merriman of Roskill pointed out in his remarks:

It is important to remember that although electrified vehicles accounted for just 2% of global auto sales in 2013, this number was 1% as recently as 2011. Anyone who has driven any type of EV knows that this technology could gain widespread adoption subject to better economics (or higher gas prices).

What Happened to Leverage?

It is most surprising that despite the bloodbath in the junior lithium sector, lithium prices have held steady (roughly $6,000 per tonne depending on the purity for battery grade). Demand has continued to increase on an annualized basis to approximately 168,000 tpy in 2013. According to Dr. Jon Hykaway of Stormcrow, one of the conference speakers and a widely followed expert in the critical metals space, demand has grown by 80% in the past 5 years.

Unfortunately most lithium juniors haven’t benefitted from this stability and growth. Their share prices have collapsed by 72% as a group since 2011 according to Luis Santillana, CFO of Li3 Energy (LIEG:OTCBB).

It is a widely held view that junior mining companies gain from their discoveries and from leverage associated with higher raw materials (in this case lithium) prices. Why then can’t most lithium juniors seem to get back on their feet without the help of Elon Musk?

This likely has to do with a point I have made in the past regarding the lithium markets. The lithium market is an oligopoly. Realistically, this is a market well supplied by a small number of participants and despite the growth projections for the industry (something which I believe in over the long term), it is also a well supplied market.

Talison Lithium, a company that performed very well for our subscribers, has tailings at its Greenbushes mine with a reported higher grade than many other hard rock projects throughout the world. Facts like these give end users and other participants along the value chain pause when considering which early stage plays to fund. It is for reasons such as this that lithium juniors have suffered in the face of a healthy lithium market; while demand is steady, current supply is ample.

Another complicating factor is that an exorbitant amount of R&D dollars are being allocated towards battery technology calling into question exactly what the “winning” battery chemistry will be. It is clearly a challenge for end users or battery manufacturers to make large capital budgeting decisions when a question of this magnitude looms large. That said, the general consensus from the conference was that lithium ion battery technology is currently the best available. Nobody in attendance saw this changing anytime soon. Even if it were to, the time it would take for new supply chains to be built and new materials to be integrated into them is substantial, confirming the steady growth profile for lithium in the coming years.

I Have Said this Before: Don’t Throw the Baby Out With the Bathwater

Despite the uncertainties I mentioned above, avoiding lithium juniors altogether would be a mistake. We are still at the bottom of this cycle with an inflection point perhaps two years away. Lithium is an exciting commodity with a number of additional avenues of demand. This hedge against a fall off in demand from one sector is a very important benefit.

Given our focus on disruptive discovery, lithium must be viewed in this context. Now is not the time to indiscriminately begin acquiring a basket of lithium junior mining companies, but I do believe there are those in the sector that are well positioned for success.

Strong balance sheets and projects in stable political jurisdictions coupled with strategic alliances or potential for lowering production costs are the keys at this stage of the cycle.

During the conference, we learned about several technologies including solvent extraction which can help achieve lower costs. In addition to this, POSCO (005490:KRX, PKX:NYSE) one of the largest global players in the steel business, has made significant inroads into dominating the downstream lithium industry. POSCO has relationships with several lithium junior mining companies and one in particular I am conducting advanced due diligence on as the combination of this company’s management, balance sheet, asset, and POSCO’s potential low cost lithium production technology make it unique amongst its peers.

Takeaways

With or without the Gigafactory, the future for lithium across multiple industries appears sound. Everyone who has experienced driving an EV (as I have) knows that this technology can become a more widespread commercial reality in the future, although calls for the death of the internal combustion engine are certainly premature. That doesn’t mean that every lithium junior will succeed (or deserves to). Given ample supply of the commodity itself, investors must find those stories which have the right blend of sustainability and upside catalysts as the global economy works through the current disinflationary environment.

The material herein is for informational purposes only and is not intended to and does not constitute the rendering of investment advice or the solicitation of an offer to buy securities. The foregoing discussion contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995 (The Act). In particular when used in the preceding discussion the words “plan,” confident that, believe, scheduled, expect, or intend to, and similar conditional expressions are intended to identify forward-looking statements subject to the safe harbor created by the ACT. Such statements are subject to certain risks and uncertainties and actual results could differ materially from those expressed in any of the forward looking statements. Such risks and uncertainties include, but are not limited to future events and financial performance of the company which are inherently uncertain and actual events and / or results may differ materially. In addition we may review investments that are not registered in the U.S. We cannot attest to nor certify the correctness of any information in this note. Please consult your financial advisor and perform your own due diligence before considering any companies mentioned in this informational bulletin.

The information in this note is provided solely for users’ general knowledge and is provided “as is”. We at the Disruptive Discoveries Journal make no warranties, expressed or implied, and disclaim and negate all other warranties, including without limitation, implied warranties or conditions of merchantability, fitness for a particular purpose or non-infringement of intellectual property or other violation of rights. Further, we do not warrant or make any representations concerning the use, validity, accuracy, completeness, likely results or reliability of any claims, statements or information in this note or otherwise relating to such materials or on any websites linked to this note. I own no shares in any company mentioned in this note.

The content in this note is not intended to be a comprehensive review of all matters and developments, and we assume no responsibility as to its completeness or accuracy. Furthermore, the information in no way should be construed or interpreted as – or as part of – an offering or solicitation of securities. No securities commission or other regulatory authority has in any way passed upon this information and no representation or warranty is made by us to that effect. For a more detailed disclaimer, please see the disclaimer on our website.

As a general rule, the most successful man in life is the man who has the best information

One of the most famous large, high-grade sulphide nickel deposits might be Voisey’s Bay.

In 1993, Albert Chislett and Chris Verbiski, while exploring for diamonds discovered significant sulphide mineralization south of Nain, Labrador.

Drilling at the site – now known as Discovery Hill – commenced in late 1994.

The second drill hole returned 41 meter’s of2.96% Ni, 1.89% Cu and 0.16% Co. The third, fourth and fifth drill holes returned similar grades.

An electromagnetic (EM) survey was done. Most rocks don’t conduct electricity, sulphide minerals do. Electromagnetic surveys take advantage of the fact that the iron sulphide pyrrhotite is a good conductor of electricity. A primary electromagnetic field is generated penetrating into the subsurface where it generates a much weaker secondary field around any conductive rocks in the area. Results indicated the presence of material that conducts electricity. A large EM anomaly had been found, it was drilled and the rest is mining history.

Hole VB-95-07 returned 104 m of high-grade massive sulphide core grading 3.9% Ni, 2.8% Cu and 0.14% Co. They had found the Ovoid, a huge, bowl-shaped accumulation of massive sulphides containing 32 million tonnes grading 2.83% Ni, 1.69% Cu and 0.12% Co.

Within a year, deep drilling east of the Ovoid had discovered a second nearby sulphide zone – the Eastern Deeps. A third discovery, the Reid Brook Zone was made just to the west of the Ovoid.

Several things stand out regarding the Voisey’s Bay deposit:

Several things stand out regarding the Voisey’s Bay deposit:

- The realized potential for additional discoveries, after the initial discovery, is extremely high because of the depositional model of these types of deposits.

- The Ovoid can be mined very easily, and extremely economically, by open-pit methods. It is the deposits ‘starter pit’ and makes mining the Eastern Deeps, Robert Friedland’s ‘Ocean of 1% nickel’ all that more attractive.

- At Voisey’s Bay a lot of high-grade nickel sulphide ore is close to surface and to deep-water access. Voisey’s Bay might be the only place in the world where this situation exists. The high price tag for Voisey’s Bay ($4.3b) was because the deposit was a game changer in the nickel sector. Nothing like it had been found before, and nothing like it has been found since.

Or has there?

Speculative fear (of missing out) and greed (reaping the great rewards associated with world class discoveries) has got to be on your radar screen.

Are they?

If they aren’t, they should be.

Richard (Rick) Mills

About Richard Mills:

Richard lives with his family on a 160 acre ranch in northern British Columbia. He invests in the resource and biotechnology/pharmaceutical sectors and is the owner of Aheadoftheherd.com. His articles have been published on over 400 websites, including:

WallStreetJournal, USAToday, NationalPost, Lewrockwell, MontrealGazette, VancouverSun, CBSnews, HuffingtonPost, Beforeitsnews, Londonthenews, Wealthwire, CalgaryHerald, Forbes, Dallasnews, SGTreport, Vantagewire, Indiatimes, Ninemsn, Ibtimes, Businessweek, HongKongHerald, Moneytalks, SeekingAlpha, BusinessInsider, Investing.com and the Association of Mining Analysts.

Please visit www.aheadoftheherd.com

If you are interested in advertising on Richard’s site please contact him for more information, rick@aheadoftheherd.com

***

Legal Notice / Disclaimer

This document is not and should not be construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment.

Richard Mills has based this document on information obtained from sources he believes to be reliable but which has not been independently verified.

Richard Mills makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness. Expressions of opinion are those of Richard Mills only and are subject to change without notice. Richard Mills assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission.

Furthermore, I, Richard Mills, assume no liability for any direct or indirect loss or damage or, in particular, for lost profit, which you may incur as a result of the use and existence of the information provided within this Report.

I’ve talked a lot recently about growing exports of natural gas liquids from the U.S.

This is a space where staggering numbers have been thrown around of late. When it comes to financial metrics for some of the companies involved.

One of the biggest beneficiaries is expected to be shipping companies. Firms that operate gas carrier vessels–the kind that transport commodities like propane and butane to overseas buyers.

In December, I discussed how shipping analysts at DNB Markets saw big gains for shipping prices. Predicting that day rates for gas carriers could rise by over 700% during the next few years.

Now it appears those gains are coming sooner than expected.

The chart below tells the story. Over the last few weeks, day rates for very large gas carriers (VLGCs) have gone through the roof. Rising more than 300% in an incredibly short time.

Why the sudden leap? Analysts have attributed it a pick up in propane shipments. Following the ultra-cold winter in the U.S.–which saw a lot of propane supply used domestically, for heating.

But it appears that global flows of natural gas liquids are now strengthening. Leading to the shocking run up in VLGC rates shown above.

The incredible thing is, analysts like DNB markets think this could be just the beginning. The group has predicted VLGC rates could rise as high as $300,000/day. Which would be another 200% gain from today’s lofty levels.

In short, this is a market that’s going through massive change. Creating the potential for huge profits for shipping companies, vessel owners and other players in the space.

There are few commodities seeing these kinds of gains today. Making this one of the most exciting sectors to arise in natural resources for some time. It’s also one that few market observers are aware of. Yet.

Here’s to a great-looking chart,

dforest@piercepoints.com / @piercepoints / Facebook

![]()

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair