Energy & Commodities

In the recent recession “spending on food in the United States dropped by three percent, compared to 22 percent decline for car sales, 14 percent for furniture, etc. Within the food category, the drop in spending was primarily a shift from high value foods to economy foods rather than a decline in total calories consumed.”

“A coming boom in agriculture? I think so. The old way of looking at food supply and demand is giving way to a new emphasis on the changing diets of hundreds of millions of people. Those changes will substantially increase demand for grains, putting upward pressure on prices.”

“Consumers don’t change their food consumption much as their incomes change, nor as the price of food products change.” – Bill Conerly Forbes Magazine

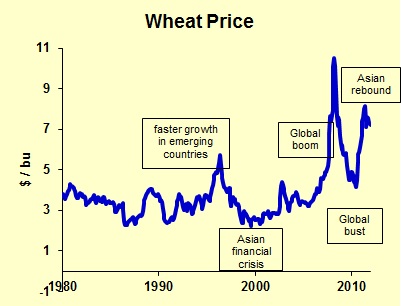

Ed: A coming boom in agriculture facing a shortage in Potash, the primary ingredient for fertilizer, Since food demand remains relatively stable regardless what is happening economically, even shifting more towards grains during economic contractions (the worse the better,) an investment in the Potash industry would seem both conservative and very long term bullish:

Will Development Pitfalls Create a Global Potash Shortage?

by Andrea Rubakovic

Here’s the story on potash according to Salman Partners Analyst Andrea Rubakovic: The major players are planning for long-term demand by developing brownfield projects, but they’re running into hurdles. Meanwhile, juniors are having trouble financing greenfield projects. Does this mean we’re in for a global supply pinch? If so, who could be positioned to profit? Here is what Rubakovic has to say in her interview:

The Energy Report: What’s your outlook for the potash industry at this point?

Andrea Rubakovic: We are expecting a cautious global potash market for the remainder of the year. Chinese and Indian potash demand is slowing. Demand from developing nations in general is softening due to economic concerns in the U.S. and Europe. Nevertheless, we believe that the combination of existing producers’ supply management and foreseen difficulties in bringing new supply onstream should keep global potash markets relatively balanced. So potash prices should be at steady levels in the short and medium terms. In the longer term though, we believe fundamental demand drivers for potash are intact and we are bullish on the industry’s prospects. We expect to see demand rising in order to supply more and better-quality food to a growing global population from a relatively finite area of arable land.

TER: A number of potash projects are under development. Do you expect to see them reach production?

AR: Current potash producers have announced significant brownfield expansions and a number of junior players around the world are developing greenfield potash projects. However, some brownfield projects under construction today may have high costs and could take as long to reach full operational capability as a greenfield mine would. (Ed: Definition of Greenfields vs Brownfields HERE)

On the greenfield front, we have seen negative development announcements from most major projects, which is a positive for the supply-demand balance. Just this morning, K+S Potash Canada (SDFG:FSE), which is in the early stages of developing its Legacy project in Saskatchewan, announced capital expenditures (capex) escalation and delayed timelines. In addition, EuroChem, a privately held company that is advancing two projects in Russia, has encountered a number of delays, while Vale S.A. (VALE:NYSE) recently announced suspension of work on its greenfield project in Argentina due to escalating costs. We have historically viewed BHP Billiton Ltd.’s (BHP:NYSE; BHPLF:OTCPK) Jansen project as the most serious risk to the potash supply-demand balance, and while the company continues to perform development work at its site in Saskatchewan, it has yet to receive formal board approval.

On the junior greenfield development front, a number of companies have significantly derisked their projects from a technical perspective. Some have completed feasibility studies and a few have secured the required environmental permits. The investment thesis a few years ago was that reaching these milestones could spark large investment by Indian, Chinese and Brazilians entities looking to secure fertilizer supplies. We have seen investments made in the sector since then; however, no overwhelming inflow of capital or straight takeovers by these parties has taken place. The main theme we are now seeing is that the junior potash companies are suffering the same fate as most junior miners: a challenging financing environment is hindering project progress.

We believe that only a small portion of greenfield developers will ultimately finance and construct their projects, and those that do are likely to experience significant delays in production start times and overruns in costs. The present challenging financing environment will filter these projects, and only the highest-quality projects or those with unique strategic appeal will develop further.

TER: Many projects these days need to have offtake agreements in place in order to have any chance of getting into production. Is this the new norm?

AR: Yes. Strategic partnerships and/or offtake agreements help mitigate the financing risk. They make project debt and equity financing easier to obtain. We view offtake agreements with an equity stake in a particularly positive light; those agreements represent a higher level of commitment.

TER: I see that you just initiated coverage on MBAC Fertilizer Corp. (MBC:TSX; MBCFFOTCQX) in January. What’s the story there?

AR: Brazil is one of the world’s fastest-growing potash and phosphate consumers and a leading importer. It is one of the few countries in the world with an underutilized land base and a favorable climate to facilitate continued expansion of cultivated land. The country currently imports 50% of its annual phosphate needs and is estimated to have the largest demand growth profile of any major phosphate consumer.

Furthermore, MBAC has a very knowledgeable management team with over 150 years of combined experience in development and financing of fertilizer projects in Brazil. The company’s CEO, Antenor Silva Jr., helped develop an innovative phosphate metallurgical process that led to highly profitable development and growth for phosphate fertilizer production in Brazil.

MBAC intends to become a significant integrated producer of fertilizers in the Brazilian and Latin American markets. The company is developing a number of fertilizer projects in Brazil, and we believe it is positioned to greatly benefit from the country’s large demand growth profile, stable political environment and a well-developed infrastructure.

The company’s flagship Itafos phosphate project, located in central and northern Cerrado—the center of Brazil’s largest agricultural region and new agricultural frontier—is expected to reach initial production later this year. The company addressed certain development issues at Itafos earlier this year, and we believe MBAC is on track to realize its potential upside if it successfully executes this project. On top of that, we believe that MBAC is a potential takeover target by a Brazilian entity that appears to have intentions to consolidate the Brazilian fertilizer sector and is already a large shareholder of the company.

TER: You also cover Encanto Potash Corp. (EPO:TSX.V). How does that situation look at this point?

AR: Encanto is another interesting company that is developing a potash play in Saskatchewan through a joint venture with the Muskowekwan First Nations group. The Muskowekwan project is relatively earlier stage compared to other Saskatchewan companies in our coverage universe, but we believe it stands to benefit from working directly and exclusively with the First Nation group through a significantly faster permitting and development process compared to negotiating with multiple land-owners.

In February, Encanto announced it is in talks with India’s Rashtriya Chemicals and Fertilizers Ltd., a state-owned fertilizer and chemical marketer that represents a consortium of Indian fertilizer companies. They have not yet struck an agreement for future potash sales, but it’s certainly encouraging that Encanto is holding these discussions. Just keep in mind that an announcement of discussions certainly does not ensure signing and completion of an offtake agreement.

Our long-term view is that completion of a positive feasibility study and receipt of the Environmental Impact Assessment (EIA) approval are necessary hurdles to pass before an offtake agreement and financing are secured; we would remind investors that these were the necessary obstacles to overcome for Potash One before being taken out by K+S. We believe the entry of a strategic partner, acquirer or offtake partner is more likely when a company completes its bankable feasibility study and receives the necessary EIA approval.

TER: Karnalyte Resources Inc. (KRN:TSX) is another company you cover. How do its prospects look at this time?

AR: Karnalyte is focused on bringing its Wynyard potash project in Saskatchewan to production. We like that the project and plant have been designed so they can be built in stages; this offers significant advantages in terms of capex. Even though we are discouraged by the large number of producers already looking to develop potash projects in Saskatchewan, we feel the high quality of the project and phased approach to production separate the Wynyard project from others in the basin as having the best chances of being financed through construction.

Gujarat State Fertilizers & Chemicals made a CA$45 million strategic investment and offtake agreement in the company early this year. We viewed this as a big vote of confidence in the project and believe the entry of the strategic partner and offtake partner marked the beginning of wider project-financing activities for Karnalyte. Our understanding is that Karnalyte will continue its discussions with other potential strategic partners, the entry of which we view to be a strong possibility. We believe there’s room for a second strategic investor to enter the picture in the near term.

TER: You recently visited Allana Potash Corp.’s (AAA:TSX; ALLRF:OTCQX) project in Ethiopia and just increased your 12-month target price. What would be the catalysts to cause that substantial move from the current price?

AR: Allana’s is another interesting story we have been following for a while. The company’s focus is on developing a potash project in Ethiopia. This is expected to be one of the lowest-cost potash projects globally due to shallow depths of mineralization and a favorable hot climate that should allow for solar evaporation, materially lowering energy costs in the solution-mining process. We also like that the company is uniquely situated to appeal to key import markets in India and China and enjoys long-standing financial support from strategic investors, IFC, a member of the World Bank Group, and Liberty Metals and Mining Holdings. We are also encouraged by the Ethiopian government’s support for companies such as Allana as part of its commitment to move Ethiopia from an agricultural to an industrial economy.

We upgraded our target price after the company significantly derisked the project with a positive feasibility study earlier this year. We expect the receipt of the Environmental, Social and Health Impact Assessment and the mining license, anticipated for receipt later this quarter, to serve as significant catalysts for the story. In addition, we are encouraged by the advanced offtake discussions the company is conducting with a number of parties and strategic partners. We feel that combined, these mark the project as a high candidate to be financed through production—no small feat in today’s unfavorable financing environment.

TER: What level of risk do companies that export from the port of Djibouti face, considering the reports of piracy in the area?

AR: The piracy problem appears to be winding down as the presence of Somali pirates, who have historically been plaguing the waters surrounding the Horn of Africa, have effectively been shut down in the past two years due to a large military presence by a number of countries in the port of Djibouti and surrounding areas. This is a very positive data point for anyone planning to transfer goods in this region.

TER: What’s your strategy on how investors should approach potash stocks in the current market environment to minimize risks and take best advantage of the opportunities you see now?

AR: A lot of the junior and small-cap stocks have been crushed in the current market, along with the stocks in the junior potash developer sector. We believe in strong long-term demand drivers for potash; the depressed prices present opportunities to accumulate shares of select junior potash developers. However, we caution that due to the large number of companies present in the universe, focusing on the highest-quality names is imperative.

We favor companies that have strong management teams, appeal to strategic investors or have distinct advantages in capital and other costs. The quality of the project, presence and likelihood of offtake partners, the cash balance and the potential sources of funding are all hugely important.

TER: Thank you for sharing your market insights with us.

AR: Thanks for having me.

Andrea Rubakovic is a research analyst covering the Canadian agriculture and fertilizer sectors. Prior to joining Salman, Rubakovic worked for a Toronto specialist investment firm, researching the Canadian resource sector. She graduated from the University of Toronto, Rotman School of Management.

Want to read more Energy Report interviews like this? Sign up for our free e-newsletter, and you’ll learn when new articles have been published. To see a list of recent interviews with industry analysts and commentators, visit our Interviews page.

DISCLOSURE:

1) Zig Lambo conducted this interview for The Energy Report and provides services to The Energy Report as an employee or as an independent contractor. He or his family own shares of the following companies mentioned in this interview: None.

2) The following companies mentioned in the interview are sponsors of The Energy Report: None. Streetwise Reports does not accept stock in exchange for its services or as sponsorship payment.

3) Andrea Rubakovic: I or my family own shares of the following companies mentioned in this interview: None. I personally am or my family is paid by the following companies mentioned in this interview: None. My company has a financial relationship with the following companies mentioned in this interview: Salman Partners Inc. has provided investment banking services to MBAC Fertilizer Corp. and Allana Potash Corp. For a complete list of disclosures, please contact Salman Partners Inc. at SalmanResearch@salmanpartners.com. I was not paid by Streetwise Reports for participating in this interview. Comments and opinions expressed are my own comments and opinions. I had the opportunity to review the interview for accuracy as of the date of the interview and am responsible for the content of the interview.

4) Interviews are edited for clarity. Streetwise Reports does not make editorial comments or change experts’ statements without their consent.

5) The interview does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer.

6) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned and may make purchases and/or sales of those securities in the open market or otherwise.

Related Articles

Bright Spots in the Fertilizer Market: Robert Winslow

Marc Faber on the April Gold & Silver Price Crash

Marc Faber on the April Gold & Silver Price Crash

That will offer an excellent buying opportunity. I would just like to make one comment. At the moment, a lot of people are knocking gold down. But if we look at the records, we are now down 21% from the September 2011 high. Apple is down 39% from last year’s high. At the same time, the S&P is at about not even up 1% from the peak in October 2007. Over the same period of time, even after today’s correction gold is up 100%. The S&P is up 2% over the March 2000 high. Gold is up 442%. So I am happy we have a sell-off that will lead to a major low. It could be at $1400, it could be today at $1300, but I think that the bull market in gold is not completed.”

“$1300. Nobody knows for sure but I think the fundamentals for gold are still intact. I would like to make one additional comment. Today we have commodities breaking down including gold. At the same time we have bonds rallying very strongly. If you stand aside and you look at these two events, it would suggest that they are strongly deflationary pressures in the system. If that was the case, I wouldn’t buy stocks or sovereign bonds because the stock market would be hit by disappointing profits if there was a deflationary environment.”

On gold falling lower if we have a deflationary environment:

“Yes, I agree. That’s why I said if the gold market collapse is saying something about deflation and at the same time we have this sharp rise in bond prices and the signals are correct that we have deflation, I wouldn’t buy stocks because in a deflationary environment, corporate profits will disappoint very badly.”

On whether a deflationary environment is possible right now:

“Everything is possible…In the economy of the cuckoo people that populate central banks, everything is possible. What you have is gigantic bubbles, the NASDAQ in 2000, then the housing bubble and then commodities in 2008 when oil went from $78 to $147 before plunging to $32 within sixth months. That kind of volatility comes from expansionary monetary policies from money-printing.”

“All I’m saying is that I think we’re going to have a major low in gold in within the next couple of weeks. Gold, as of today, you should actually buy as a trade. I think it can rebound in the next two days by $40.”

On why gold will rebound $40 in the next two days:

“Because we are about in gold as oversold and we were essentially during the crash in 1987. From there we have a strong rebound. All I am saying as a trader I would probably enter the market quickly for a rebound of $20 or $40. From a longer term perspective, I would give it some time. We may go lower. I am not worried. I am happy gold is finally coming down, which will provide a very good entry point.”

On whether investors should also stay in cash:

“My argument is that you should always have in this kind of high volatility environment a fair amount of cash because opportunities will always arise again and again and if you have cash you can then buy assets at a reasonable price. I think Patience is very important in this environment. The question is, how do you hold your cash? Hopefully not with a Cyprus bank.”

More from Marc’s website:

Marc Faber : If the U.S. Government was a Company, the deficit would be $5 Trillion

Marc Faber : “I think the problem in most countries,” he says, “ is a political problem. You have, essentially, large mandatory expenditures…and as a percentage of the population, less and less people working. And so these unfunded liabilities…accrue at a very fast pace.”

“If the U.S. Government was a company, the deficit would be $5 trillion because they would have to account by general accepted accounting principles. But actually they encourage government spending, reckless government spending, because the government can issue Treasury bills at extremely low interest rates.” – in a recent interview with Porter Stansberry

Find out about a few of the junior minors “on the move.”

Rare Earth Weekly

The global rare earth industry is experiencing price deterioration which has exacerbated declines in revenues, earnings and share prices of junior minors. Molycorp (MCP), with its heavy concentration of light rare earths (“LREE”), experienced price declines of 30% quarter-over-quarter. The price deterioration does not seem to be abating anytime soon. According to the Motley Fool, it’s a wonder that some junior minors are even still in business:

The price of common rare-earth minerals has been dropping since 2011, the year prices peaked, which is why revenue is slipping. It’s a wonder at this point that miners without production, like Rare Element Resources (REE) and Avalon Rare Metals (AVL), are still in business at all. If Molycorp can’t make money now that it’s in full production, then how could there be enough demand to support all of these companies?

…..read more HERE

About the author: Shock Exchange

B.A. in economics and MBA from top 10 business school. I have over 10 years of M&A / corporate finance experience. Currently head the New York Shock Exchange (www.newyorkshockexchange.com), a youth mentorship program that teaches investment management skills and competitive basketball skills.

B.A. in economics and MBA from top 10 business school. I have over 10 years of M&A / corporate finance experience. Currently head the New York Shock Exchange (www.newyorkshockexchange.com), a youth mentorship program that teaches investment management skills and competitive basketball skills.

Uh-oh… We’ve got good news and bad news. But you’ll have to figure out which is which.

We also have what is probably the most important thing you will read this year…

Yesterday, the Dow fell again – 81 points. Gold went up – by almost $10 per ounce. Gold does not seem inclined to go down much more… at least, not immediately. And though some big players seem to be dumping gold – we won’t mention any names – most of the gold orders are buys, not sells.

Here’s Paul Tustain, CEO of physical gold storage business BullionVault, on gold’s recent correction:

[H]ere are some BullionVault statistics from the last few days, which I think offer a useful reminder about how markets work. Remember, first of all, that for all those people who sold in a bit of a panic, someone bought.

-

Monday and Tuesday were our strongest 48-hour period for new customers this year.

-

Since Friday, the gross value of customer bullion sales increased markedly. About 1% of gold we look after was sold back to the main market. That was characterized by a few large sellers. Holders of 99% of BullionVault inventory were not panicked.

-

Those who did sell have mostly not withdrawn their cash from the BullionVault system. To me, that suggests they may be intending to buy back into gold sooner rather than later.

-

We normally have about 230 deposits a day (300 on a Monday) and about 100 withdrawals a day (120 on a Monday). Mondays are usually higher because they include weekend activity. On Monday, we had 723 deposits versus 284 withdrawals. On Tuesday, we had 732 deposits versus 150 withdrawals.

-

Monday was a record day for business transacted, beating the previous peak of September 2011.

|

62 Years of Uninterrupted Gains? I recently discovered an incredible investment that has nothing to do with stocks, bonds, ETFs or mutual funds. Most brokers have probably never heard of it — yet, it’s gone up at least 5% every year since 1950. And since 1998, while the stock market has seen two major crashes, this investment has gone up an average of 12% per year, like clockwork. What is this unique alternative to stocks? Watch this video to find out. |

Candy for the Mind

And now… here’s why you really shouldn’t pay attention to any news. It’s “public information” – with little integrity, little quality and little usefulness.

Here’s our friend, the Swiss novelist Rolf Dobelli.

News is bad for you. It’s like sugar. It gives you a rush. It’s a distraction from your own concerns. It’s easy to digest. But this “candy for the mind” can be toxic.

In the past few decades, the fortunate among us have recognized the hazards of living with an overabundance of food (obesity, diabetes) and have started to change our diets. But most of us do not yet understand that news is to the mind what sugar is to the body.

News is easy to digest. The media feeds us small bites of trivial matter, tidbits that don’t really concern our lives and don’t require thinking. That’s why we experience almost no saturation. Unlike reading books and long magazine articles (which require thinking), we can swallow limitless quantities of news flashes, which are bright-colored candies for the mind.

Today, we have reached the same point in relation to information that we faced 20 years ago in regard to food. We are beginning to recognize how toxic news can be.

News Misleads

Take the following event (borrowed from Nassim Taleb). A car drives over a bridge, and the bridge collapses. What does the news media focus on? The car. The person in the car. Where he came from. Where he planned to go. How he experienced the crash (if he survived). But that is all irrelevant. What’s relevant? The structural stability of the bridge.

That’s the underlying risk that has been lurking and could lurk in other bridges. But the car is flashy, it’s dramatic, it’s a person (non-abstract), and it’s news that’s cheap to produce. News leads us to walk around with the completely wrong risk map in our heads. So terrorism is overrated. Chronic stress is underrated. The collapse of Lehman Brothers is overrated. Fiscal irresponsibility is underrated. Astronauts are overrated. Nurses are underrated.

We are not rational enough to be exposed to the press. Watching an airplane crash on television is going to change your attitude toward that risk, regardless of its real probability. If you think you can compensate with the strength of your own inner contemplation, you are wrong. Bankers and economists – who have powerful incentives to compensate for news-borne hazards – have shown that they cannot. The only solution: Cut yourself off from news consumption entirely.

News Is Irrelevant

Out of the approximately 10,000 news stories you have read in the last 12 months, name one that – because you consumed it – allowed you to make a better decision about a serious matter affecting your life, your career or your business. The point is: The consumption of news is irrelevant to you. But people find it very difficult to recognize what’s relevant. It’s much easier to recognize what’s new. The relevant versus the new is the fundamental battle of the current age.

Media organizations want you to believe that news offers you some sort of a competitive advantage. Many fall for that. We get anxious when we’re cut off from the flow of news. In reality, news consumption is a competitive disadvantage. The less news you consume, the bigger the advantage you have.

News Has No Explanatory Power

News items are bubbles popping on the surface of a deeper world. Will accumulating facts help you understand the world? Sadly, no. The relationship is inverted. The important stories are non-stories: slow, powerful movements that develop below journalists’ radar but have a transforming effect. The more “news factoids” you digest, the less of the big picture you will understand. If more information leads to higher economic success, we’d expect journalists to be at the top of the pyramid. That’s not the case.

News Is Toxic to the Body

It constantly triggers the limbic system. Panicky stories spur the release of cascades of glucocorticoid (cortisol). This deregulates your immune system and inhibits the release of growth hormones. In other words, your body finds itself in a state of chronic stress. High glucocorticoid levels cause impaired digestion, lack of growth (cell, hair, bone), nervousness and susceptibility to infections. The other potential side effects include fear, aggression, tunnel vision and desensitization.

News Increases Cognitive Errors

News feeds the mother of all cognitive errors: confirmation bias. In the words of Warren Buffett: “What the human being is best at doing is interpreting all new information so that their prior conclusions remain intact.” News exacerbates this flaw. We become prone to overconfidence, take stupid risks and misjudge opportunities. It also exacerbates another cognitive error: the story bias. Our brains crave stories that “make sense” – even if they don’t correspond to reality. Any journalist who writes, “The market moved because of X” or “The company went bankrupt because of Y” is an idiot. I am fed up with this cheap way of “explaining” the world.

News Inhibits Thinking

Thinking requires concentration. Concentration requires uninterrupted time. News pieces are specifically engineered to interrupt you. They are like viruses that steal attention for their own purposes. News makes us shallow thinkers.

But it’s worse than that. News severely affects memory. There are two types of memory. Long-range memory’s capacity is nearly infinite, but working memory is limited to a certain amount of slippery data. The path from short-term to long-term memory is a choke point in the brain, but anything you want to understand must pass through it. If this passageway is disrupted, nothing gets through.

Because news disrupts concentration, it weakens comprehension. Online news has an even worse impact. In a 2001 study, two scholars in Canada showed that comprehension declines as the number of hyperlinks in a document increases. Why? Because whenever a link appears, your brain has to at least make the choice not to click, which in itself is distracting. News is an intentional interruption system.

News Works Like a Drug

As stories develop, we want to know how they continue. With hundreds of arbitrary story lines in our heads, this craving is increasingly compelling and hard to ignore.

Scientists used to think that the dense connections formed among the 100 billion neurons inside our skulls were largely fixed by the time we reached adulthood. Today we know that this is not the case. Nerve cells routinely break old connections and form new ones. The more news we consume, the more we exercise the neural circuits devoted to skimming and multitasking while ignoring those used for reading deeply and thinking with profound focus.

Most news consumers – even if they used to be avid book readers – have lost the ability to absorb lengthy articles or books. After four, five pages they get tired, their concentration vanishes, they become restless. It’s not because they got older or their schedules became more onerous. It’s because the physical structure of their brains has changed.

News Wastes Time

If you read the newspaper for 15 minutes each morning, then check the news for 15 minutes during lunch and 15 minutes before you go to bed, then add five minutes here and there when you’re at work, then count distraction and refocusing time, you will lose at least half a day every week. Information is no longer a scarce commodity. But attention is. You are not that irresponsible with your money, reputation or health. Why give away your mind?

News Makes Us Passive

News stories are overwhelmingly about things you cannot influence. The daily repetition of news about things we can’t act upon makes us passive. It grinds us down until we adopt a worldview that is pessimistic, desensitized, sarcastic and fatalistic. The scientific term is “learned helplessness.” It’s a bit of a stretch, but I would not be surprised if news consumption at least partially contributes to the widespread disease of depression.

News Kills Creativity

Finally, things we already know limit our creativity. This is one reason that mathematicians, novelists, composers and entrepreneurs often produce their most creative works at a young age. Their brains enjoy a wide, uninhabited space that emboldens them to come up with and pursue novel ideas. I don’t know a single truly creative mind who is a news junkie – not a writer, not a composer, mathematician, physician, scientist, musician, designer, architect or painter.

On the other hand, I know a bunch of viciously uncreative minds who consume news like drugs. If you want to come up with old solutions, read news. If you are looking for new solutions, don’t.

Society needs journalism – but in a different way. Investigative journalism is always relevant. We need reporting that polices our institutions and uncovers truth. But important findings don’t have to arrive in the form of news. Long journal articles and in-depth books are good, too.

I have now gone without news for four years, so I can see, feel and report the effects of this freedom firsthand: less disruption, less anxiety, deeper thinking, more time, more insights. It’s not easy, but it’s worth it.

[This is an edited extract from an essay first published at dobelli.com.]

Regards,

![]()

Bill

Like Bill’s Diary?

Republish our articles on your website or blog for free. Learn How

Have a question for our editorial team?

Contact Us

Bill Bonner started Diary of a Rogue Economist to share his over 30 years of economics and market experience with as many interested readers as possible.

Diary of a Rogue Economist is always free, and it’s delivered to your email each business day.

NOT even GOLD will SAVE YOU from the coming WORLD SYSTEMIC CRISIS – Marc Faber

……Watch the Video Below or read it all HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair