Energy & Commodities

After a restless night, I awake to find gold and silver getting hammered again. While I suspect I won’t be alone in wanting to do this through much of today, I must remind myself that the alternative isn’t a great choice (no matter what some emails say-lol)

After a restless night, I awake to find gold and silver getting hammered again. While I suspect I won’t be alone in wanting to do this through much of today, I must remind myself that the alternative isn’t a great choice (no matter what some emails say-lol)

There were a lot of good articles over the weekend, but I suspect they will mean little to most for much of the day. I’m going to post them anyway because I think they have some useful insight and doesn’t misery love company anyway?

Currently under $1,400, where we close today and most importantly at weeks-end, is what’s really going to matter.

- How the gold market was crashed

- 400 tonnes cruch gold

- GLD holdings plunge

- Gold and silver buyers outpace sellers by 50 to 1

- Expect margin calls Monday morning

- Assault on gold

- Historical perspective of a silver correction

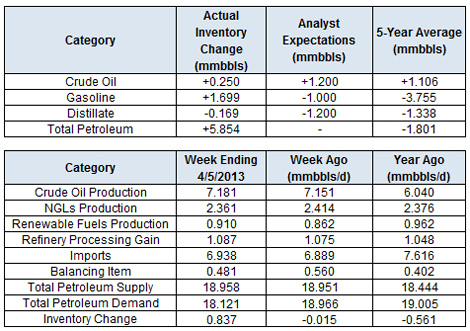

We take a look at the latest developments in the oil market, including charts of all the major inventory categories.

The Department of Energy reported this morning that in the week ending April 5, U.S. crude oil inventories increased by 0.3 million barrels, gasoline inventories increased by 1.7 million barrels, distillate inventories decreased by 0.2 million barrels and total petroleum inventories increased by 5.9 million barrels.

Oil prices were lower after the release of the latest inventory figures. Crude continues to underperform stock markets, which hit fresh record highs in today’s session. Brent remains in a downtrend, and we see prices testing the psychologically significant support level at $100 in the coming weeks.

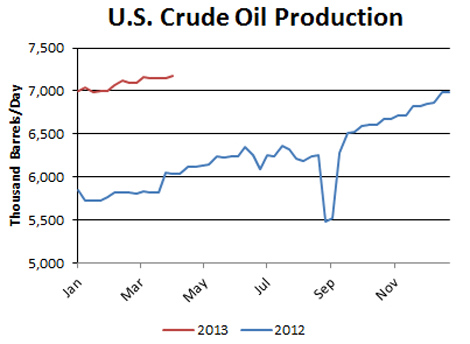

In our view, the surge in U.S. production has played a major role in dampening oil prices. U.S. output hit a fresh 21-year high last week at 7.18 million barrels per day, up 1.26 mmbbl/d, or 22 percent from a year ago.

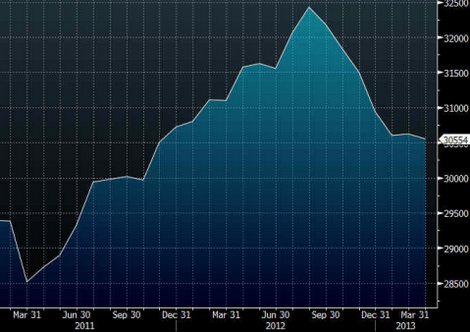

In turn, OPEC has had to cut back its output to keep the market in balance. The cartel’s output fell to 30.55 mmbbl/d in March, the lowest level since November 2011 and nearly 2 million barrels per day below the most recent peak set in August 2012. The reduction in OPEC’s output—and consequent increase in OPEC’s spare capacity—has created a buffer against supply disruptions. Oil prices typically perform poorly during periods of high OPEC spare capacity.

OPEC Crude Production

BRENT

WTI

Bottom Line: The correction in oil prices may continue as Brent falls to $100. A break below that level exposes much lower levels near $87. WTI is set to continue its outperformance, but may decline if Brent falls significantly from here.

…..read more HERE

As I was researching, and writing, this past weekend’s weekly newsletter entitled “The Bernanke Factor” what really struck me was the universal belief by the majority of analysts, economists and commentators, that there is currently “no evidence” of an asset bubble. This idea was further confirmed by Bernanke’s testimony last week where he explicitly stated:

I don’t see much evidence of an equity bubble.

His prepared statement also touched on the same:

Another potential cost that the Committee takes very seriously is the possibility that very low interest rates, if maintained for a considerable time, could impair financial stability. For example, portfolio managers dissatisfied with low returns may ‘reach for yield’ by taking on more credit risk, duration risk, or leverage…Although a long period of low rates could encourage excessive risk-taking, and continued close attention to such developments is certainly warranted, to this point we do not see the potential costs of the increased risk-taking in some financial markets as outweighing the benefits of promoting a stronger economic recovery and more-rapid job creation.

The common theme between Bernanke’s comments, and the majority of analysts and economists, is corporate profitability. As Neil Irwin recently penned:

But there’s good evidence pointing to this [an equity bubble] not being the case. The key thing to know is that American businesses have spent the last four years becoming much more profitable.

However, looking at corporate profitability in a vacuum can be a bit misleading. Today, there are contributing factors to corporate profitability that did not exist previously, such as the change to FASB Rule 157, which changed mark-to-market accounting, the excessive use of loan-loss reserves and other accounting gimmickry. Regardless, what is more important than the level of profits is the relative growth trend of those profits. The chart below shows top line sales versus reported and operating earnings. The last two major market peaks have coincided with earnings topping, and beginning to weaken, much like we are seeing currently.

While the level of corporate profitability is certainly important – corporate profits are more of a reflection of the issues that have historically led to asset bubbles. Increases in leverage, speculative investing and the push for yield, as identified in Bernanke’s testimony, are more attributable to historic asset bubbles from the peak in 1929, the technology bubble in 2000 or the housing bubble in 2008. For example, the housing bubble that started in 2003, which was built around excess credit and leverage as homes were turned into ATM’s – led to a surge in corporate profitability and economic growth. However, the growth of corporate profitability did little to deter what happened next.

Following The Sign Posts

So, instead of corporate profitability, which is already showing signs of stress, we should be focusing on the areas identified by Mr. Bernanke in his recent testimony: leverage, speculative risk taking, and the reach for yield. These data points could provide much needed clues as to where, as investors, we are in the current cycle and what the potential risks are that lie ahead.

Sign Post #1 – Leverage

The downfall of all investors is ultimately “greed.” Greed can be measured not only emotionally by looking at bullish versus bearish sentiment indexes but, more importantly, how much leverage investors are taking on. The chart below is the amount of margin debt by investors overlaid against their relative positive or negative net credit balances.

With both margin debt and negative net credit balances reaching levels not seen since the peak of the last cyclical bull market cycle it should raise some concerns about sustainability currently. It is the unwinding of this leverage that is critically dangerous in the market as the acceleration of “margin calls” lead to a vicious downward spiral. While this chart does not mean that a massive market correction is imminent – it does suggest that leverage, and speculative risk taking, are likely much further along than currently recognized.

Sign Post #2 – High Yield Chase

When investors have little, or no, fear of losing money in the market they begin to seek the things with the greatest returns. Over the last few years the chase for yield, due to Bernanke’s consistent push to suppress interest rates, has driven investors into taking on additional credit risk to increase incomes. The chart below is the BofA Merrill High Yield (aka Junk Bond) Index.

The chart shows that, as opposed to Bernanke’s statement, investors are rapidly taking on excessive credit risk, which is driving down yields. With those yields now at historic lows there is little margin for error either in the credit markets or the economy.

Sign Post #3 – Reduced Translation Into Economic Growth

While Bernanke is hoping for stronger economic growth in the near future his real concern has been the effect of diminishing returns on each monetary program.

Since Q4 of 2008, the real economy has grown from $12,883.5 billion to $13,656.8 billion as of Q4 2012. This is a total of $773.3 billion in growth over the last four years or $193 billion per year or roughly about a 1.5% growth rate. During this same period, the Fed has injected roughly $5 for each dollar’s worth of economic growth. This could hardly be considered a great return on investment.

As opposed to Bernanke’s statement that increased risk-taking are okay as long as such risks are outweighed by “the benefits of promoting a stronger economic recovery and more-rapid job creation,” it appears that such a progression is not the case. As we have seen with virtually every indicator – economic activity peaked in 2010. Since then, even with the input of global stimulus, the rate of economic growth has weakened, as shown in the chart below.

Risks Of Recession Have Increased

With Q4-2012 GDP running at statistically zero – the impact of the payroll tax hike (effectively about a $125 billion hit to consumers), higher gasoline and energy costs, and the impact of further cuts to government spending due to the sequester, put an already weakening economic growth trend at further risk.

Don’t misunderstand me. As I wrote at the end of February in “Get Ready For A Run To All-Time Highs”– it is certainly conceivable that the S&P 500 (SPY) could attain all-time highs by this summer. The speculative appetite combined with the Fed’s liquidity is a powerful combination in the short term. However, the increase in speculative risks combined with excess leverage leave the markets vulnerable to a sizable correction at some point in the future.

The only missing ingredient for such a correction currently is simply a catalyst to put “fear” into an overly complacent marketplace. There is currently no shortage of catalysts to pick from whether it is further fiscal policy missteps stemming from the upcoming “Debt Ceiling”debate, a resurgence of the eurozone crisis, or an unexpected shock from an area yet to be on our radar.

In the long term, it will ultimately be the fundamentals that drive the markets. Currently, the deterioration in the growth rate of earnings, and economic strength, are not supportive of the speculative rise in asset prices or leverage. The idea of whether, or not, the Federal Reserve- along with virtually every other central bank in the world- are inflating the next asset bubble is of significant importance to investors who can ill afford to once again lose a large chunk of their net worth.

It is all reminiscent of the market peak of 1929 when Dr. Irving Fisher uttered his now famous words: “Stocks have now reached a permanently high plateau.” The clamoring of voices that the bull market is just beginning is telling much the same story. History is replete with market crashes that occurred just as the mainstream belief made heretics out of anyone who dared to contradict the bullish bias.

Does an asset bubble currently exist? Ask anyone and they will tell you“NO.” However, maybe it is exactly that tacit denial which might just be an indication of its existence.

- Company: Streettalk Advisors

- Blog: The Daily X-Change

When I was a kid, I used to watch the World Wrestling Federation religiously.

I couldn’t wait for the show to air at 4 o’clock on Saturday afternoons…

My favorite wrestler was Rowdy Roddy Piper. He wasn’t exceptionally gifted as an athlete, but man, he was a great entertainer. My favorite quote from him is: “Just when you think you know the answer, I change the question.”

That phrase can be applied to the current state of the American oil and gas industry.

It’s changing at an exponential rate. Here’s what I mean…

I want you to take a good, long look at this picture:

What you see are well pads, leveled and cleared to make way for drilling equipment.

My untrained eye tells me there are at least 100 pads being prepared in this photo. And this is just a snapshot of a much bigger picture.

Oil drillers are gearing up for an absolute bonanza here. And if they hit paydirt, this region of the globe could become one of the most prolific oil-producing regions the world over.

So, where was this photo taken?

Believe it or not, it’s in our own backyard.

It’s the Permian Basin in West Texas.

As I told you last month in an article published in Energy and Capital, the Permian has been a cradle of oil drilling since 1921, producing 32 billion barrels to date.

However, experts forecast that with the discovery of the Cline Shale within the Permian — coupled with the application of multi-well pad drilling — the Permian has the ability to produce another 32 billion barrels. Or even more.

The March 2013 cover of National Geographic says it all:

No offense to National Geographic, but we scooped them seven years ago.

The fracking boom started in earnest in 2008, but it’s just starting to heat up…

Last month the EIA published new numbers for U.S. oil production for the month of January 2013. The EIA report showed Texas produced an average of 2.26 million barrels per day (bpd) in January, the highest daily output for Texas since 1986. (I was a junior in high school that year… now my oldest son is the same age. That’show long ago it was.)

At that production rate, Texas alone produced more oil than OPEC members Algeria, Libya, Angola, Ecuador, Nigeria, and Qatar — and it’s closing in fast on Kuwait, Venezuela, and the UAE.

But even this fact doesn’t represent how dramatic and swift the reversal of fortune has been for the Texas oil industry…

You see, Texas oil production increased by 30% in January from a year earlier — and by 75% from two years ago. In fact, oil production in Texas has achieved a clean double in the last three years!

Texas is literally booming. And the positive effects are being felt everywhere. The state added over 80,000 jobs in the month of February.

This trend is accelerating at light speed, and it’s having an impact not just in the States, but globally. According to CNBC this past Monday:

Without fanfare, China passed the United States in December to become the world’s leading importer of oil-the first time in nearly 40 years that the U.S. didn’t own that dubious distinction. That same month, North Dakota, Ohio and Pennsylvania together produced 1.5 million barrels of oil a day–more than Iran exported.

As those data points demonstrate, a dramatic shift is occurring in how energy is being produced and consumed around the world-one that could lead to far-reaching changes in the geopolitical order.

U.S. policy makers, intelligence analysts and other experts are just beginning to grapple with the ramifications of such a change, which could bring with it both great benefits for the U.S. and potentially dangerous consequences, including the risk of upheaval in countries and regions heavily dependent on oil exports.

Most agree the U.S. would be the big winner, in position to reshape its foreign policy and boost its global influence.

Like I’ve said before, technology and innovation always win the day.

And multi-well pad drilling is a game changer.

Because oil and gas companies can drill 8 to 24 (sometimes more than 50) wells from a single pad site, more oil and gas are accessible from a single drill rig, reducing time and costs.

Just how is this playing out in the real world?

The United States is producing more natural gas today with less than 400 drill rigs than it did in 2008, when there were over 1,600 drill rigs in operation in the United States. This is the drilling equivalent of Moore’s Law.

But here’s the deal: There’s no sign that it’s about to stop any time soon…

Multi-well pad drilling is becoming the new normal. Here’s how we’re playing it.

Forever wealth,

Brian Hicks

Brian is a founding member and President of Angel Publishing and investment director for the income and dividend newsletter The Wealth Advisory. He writes about general investment strategies for Wealth Daily and Energy and Capital. Known as the “original bull on America,” Brian is also the author of Profit from the Peak: The End of Oil and the Greatest Investment Event of the Century, published in 2008. In addition to writing about the economy, investments and politics, Brian is also a frequent guest on CNBC, Bloomberg, Fox, and countless radio shows. For more on Brian, take a look at his editor’s page.

All financial eyes should be focused on the BOJ (Bank of Japan) right now. Money managers are calling this week’s BOJ meeting, the most important one in many years.

All financial eyes should be focused on the BOJ (Bank of Japan) right now. Money managers are calling this week’s BOJ meeting, the most important one in many years.

- It’s likely to be a key factor in determining the next big move for the price of gold.

- Key market players expect Governor Kuroda to imitate Ben Bernanke’s actions, and begin buying longer maturity bonds, and more of them,with electronically printed yen.

- If Kuroda disappoints the market, the yen could rally, and the Nikkei could tumble. If the yen rallied against the dollar, gold might rally too, simply because it trades mainly in dollars.

- On the other hand, if the market believes Kuroda’s actions are a great first step in reversing Japanese deflation, gold could also rally. In the big picture, Kuroda seems to be creating a “win win” situation for gold.

- The man formerly known as “Mr. Yen”, Eisuke Sakakibara, former vice finance minister of Japan, thinks Kuroda will fail to reverse deflation.

- I don’t believe Kuroda will fail, but I believe most money managers are drastically underestimating the amount of money printing that is needed to get the job done.

- Kuroda has said he will do “whatever it takes” to get the Japanese inflation rate up to 2%. Cost push inflation (CPI) will likely be the horrific consequence of doing “whatever it takes”.

- Japan is the 3rd largest economy in the world, far larger than Germany, which is number 4. CPI could devastate Japanese savers. Worse, because Japan is such a large economy, CPI could spread around the world, and I think it will.

- The only good news about CPI is that it could push the gold price well above $2000, and push your gold stocks to new highs. Right now, I don’t think you need any more good news than that!

- Until CPI becomes a dominant theme in the eyes of professional money managers, a rising T-bond price will continue to be bullish for gold. Quantitative easing, and the resulting expansion of the Fed’s balance sheet, is the main driver of gold market liquidity flows.

- Please click here now. You are looking at the daily chart of the T-bond. The good news, for gold market investors, is that there is an upside breakout attempt in play, today. Note the key HSR (horizontal support & resistance) in the 145 area.

- Having said that, please note the position of my “stokeillator” (14,7,7 Stochastics series), at the bottom of the chart. The red lead line has risen to about 90. A crossover sell signal seems imminent, but I’m hoping that any sell-off creates the right shoulder of a bullish double-headed inverse h&s pattern.

- It’s very common, technically speaking, for the price of an asset to rise a bit above a key HSR line, before overbought oscillators “work” to pull it back down, and that may be the case here with the T-bond.

- The technical set-up of this bond chart is similar to that of gold. Pleaseclick here now. That’s the daily gold chart, and you can see that a crossover sell signal for my stokeillator is clearly in play.

- It’s difficult for gold to rally strongly, when technical oscillators are overbought and flashing sell signals. A light sell-off now, or a sideways “drift”, could be just what is needed to begin a much larger rally of $200-$300 an ounce. I think that is exactly what is in the cards now, for gold.

- Note the important HSR at about $1620. If the T-bond can surge above 145, gold should burst above $1620.

- For a closer look at the gold price, please click here now. That’s the hourly gold chart. Note the rough rectangular pattern, defined by the two black trend lines. The target is about $1575.

- Oscillators are like the tides of the ocean, or a person’s breathing pattern. Fighting the natural tendency of gold to rise and fall in a small way, as oscillators move up and down, is not a good idea.

- The situation in the Korean peninsula is potentially a big driver of higher gold prices, but that too, seems to be in sync with my stokeillator; tensions are building, but North Korea has not physically moved any significant number of troops, and that’s needed to raise the tension level. A major rise in tensions seems imminent, but it’s not quite here yet.

- Gold stocks may need a little more “rest time”, too. Please click here now. Double-click to enlarge. You are viewing the BMO Junior Golds Index ETF daily chart. Note the “waterfall” action of the technical indicators.

- That’s not a giant sell signal. It’s simply the cycle of “gold stocks life”.

- While you wait for cost push inflation to become a dominant theme in markets around the world, gold stocks will rise and fall in a small way, like the tide comes in and goes out. A tidal wave of price is coming, but investors need to wait for it, with patience. If you are bored, from waiting for “the big one”, you may want to check out my intraday gold trading service. Send me an email at stewart@gutrader.com, and I’ll send you the details. Thanks.

- GDXJ has a similar look to the BMO ETF. Please click here now . Double-click to enlarge. This is the daily chart. Volume declined during the recent rally, and now most technical indicators are rolling over, suggesting a little weakness is possible. Oscillators don’t create tidal waves, though. Fundamentals do. The fundamentals will create a tidal wave for gold, and these technical oscillators & indicators are telling you that the price of gold needs to breathe, in and out, like a person does. Let the gold price breathe naturally, and you’ll find the price action much less stressful!

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Apr 2, 2013

Stewart Thomson

Graceland Updates

website: www.gracelandupdates.com

email for questions: stewart@gracelandupdates.com

email to request the free reports: freereports@gracelandupdates.com

Graceland Updates Subscription Service: Note we are privacy oriented. We accept cheques. And credit cards thru PayPal only on our website.

For your protection we don’t see your credit card information. Only PayPal does. Subscribe via major credit cards at Graceland Updates – or make checks payable to: “Stewart Thomson” Mail to: Stewart Thomson / 1276 Lakeview Drive / Oakville, Ontario L6H 2M8 / Canada

Stewart Thomson is a retired Merrill Lynch broker. Stewart writes the Graceland Updates daily between 4am-7am. They are sent out around 8am. The newsletter is attractively priced and the format is a unique numbered point form; giving clarity to each point and saving valuable reading time.

Risks, Disclaimers, Legal

Stewart Thomson is no longer an investment advisor. The information provided by Stewart and Graceland Updates is for general information purposes only. Before taking any action on any investment, it is imperative that you consult with multiple properly licensed, experienced and qualifed investment advisors and get numerous opinions before taking any action. Your minimum risk on any investment in the world is 100% loss of all your money. You may be taking or preparing to take leveraged positions in investments and not know it, exposing yourself to unlimited risks. This is highly concerning if you are an invetor in any derivatives products. There is an approx $700 trillion OTC Derivatives Iceberg with a tiny portion written off officially. The bottom line:

Are You Prepared?

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair