Energy & Commodities

Industrial demand for Silver to average 483 mn oz from 2012 to 2014 – SILVER INSTITUTE

Industrial demand for Silver to average 483 mn oz from 2012 to 2014 – SILVER INSTITUTE

“Silver helps make today’s interconnected lifestyle possible and is a vital component of virtually every automobile, cell and smartphone, computer and laptop, appliance and electronic device we use. Further, silver’s antibacterial properties are finding new uses in textiles, medical instruments and hospital equipment, providing an effective tool in combatting infection and bacteria.”

Industry’s widening use of silver is expected to average more than 483 million ounces (Moz.) from 2012 to 2014, a level 53 percent greater than the average annual industrial fabrication demand of 313.4 Moz from 1992-2001.

Speaking last week at the annual Prospectors & Developers Association of Canada convention in Toronto, Michael DiRienzo, Executive Director of the Silver Institute, said that demand for silver is broadening in many directions.

….read more HERE

Ed Note: Some older articles on Silver becoming Extinct:

According to the U.S. Geological Society: “Silver will be the first element in the periodic table that will become extinct.”

Canada is getting into the Big leagues of Energy Production according the a recent report from the Fraser Institute.

In short, Canada has “pretty much vast untapped potential for Economic benefits to Canadians by continuing along this path of increased energy production and trade” says Ken Green of the Fraser Institute. According to this report, Canada is well on its way to becoming a Superproducer of energy with its vast new reserves of Oil from unconventional sources like the Oil Sands, new reserves of Natural Gas from Fracking shale reserves, as well as our existing supplies of power generated by Hydro Electricity.

The price of natural gas is coming down dramatically in North America due to the vast new supplies of shale gas coming online.

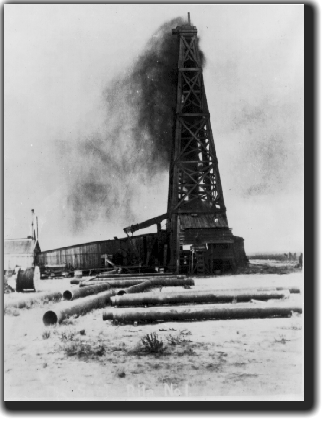

At around 6 o’clock on the morning of May 28, 1923, an oil well named after the patron saint of the impossible blew.

The well sprayed oil over the top of the derrick and covered a 250-yard area around the site…

This is an actual picture of it:

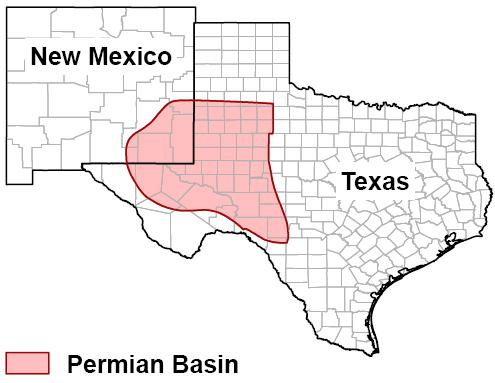

On that morning, the Permian oil boom in Texas was born.

The name of the well was Santa Rita No. 1.

According to official state records in Texas, between 1917 and 1919, more than 5,000 drilling permits were issued for the Permian Basin. However, no exploration occurred… until August 23, 1921, when — just four hours before its permit was set to expire — the Santa Rita No. 1 was spudded.

Drilling continued for almost two years at the drill site before they struck the gusher.

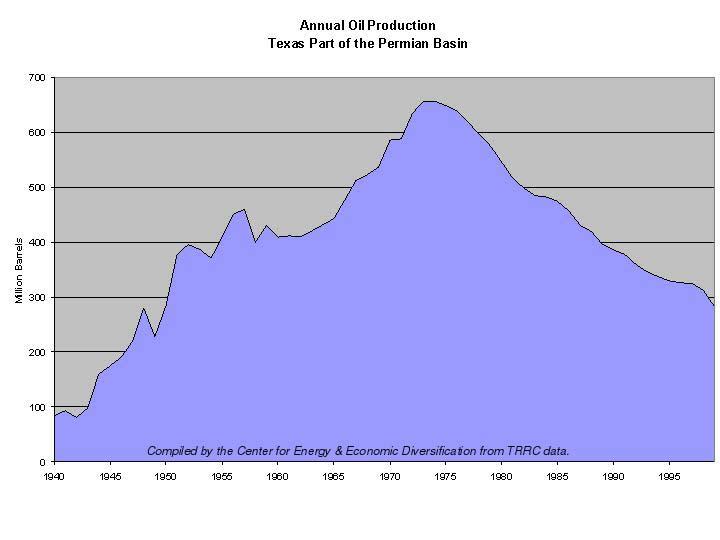

For the next 50 years, the legendary Permian Basin dominated the world.

It has pumped out 35 billion barrels since Santa Rita No. 1 started spewing.

The field peaked in production between 1973 and 1974, as predicted by Shell geologist M. King Hubbert.

At its height, the Permian was pumping out over 1.7 million barrels per day.

When the Permian peaked, it marked the end of American oil domination and ushered in OPEC. And for the next 40 years, OPEC would have a stranglehold on the world’s energy economy.

But that was that was four decades ago.

A lot of things have changed — and quite dramatically…

Thanks to the revolution in hydraulic fracturing, the Permian is expected to regain its stature in the global oil market. It is set to become the king.

Oil and gas companies are rushing into West Texas like army ants. And it’s easy to see why.

“That would be the equivalent of 10 Eagle Ford shales stacked on top of each other. It’s 17 Bakkens placed on top of one another.”

That’s how a new American shale play is being described. That’s how big it is.

The industry-respected, Houston-based Hart Energy Magazine says: “There’s just oil all over the place,” and estimates the field could produce more than 1.65 million barrels of oil per day within seven years.

At that daily production, this single oilfield would produce nearly four times more oil than OPEC member Ecuador. It would represent 66% of all of Mexico’s oil production (at its current rate)!

It’s a modern-day black gold rush. And it’s the hottest play in America — hotter than California’s Monterey… hotter than Texas’ Eagle Ford… and even hotter than North Dakota’s booming Bakken.

In fact, as you read this, the field I’m talking about has over 400 drill rigs currently operating in it. To give you an idea of how much that is, it accounts for 10% of all drilling rigs currently in operation on the planet.

I’m talking about the revived Permian Basin in Texas — and the Cline Shale that lies within it.

If you haven’t heard of the Cline Shale, it is a monster: Lying roughly 1.8 miles below the surface of the Permian, the Cline runs about 140 miles from north to south and 70 miles wide. So it’s approximately 9,800 square miles in size.

Devon Energy was one of the first companies in the Cline Shale. A recent study from Devon estimated the Cline Shale contains 3.6 million barrels of recoverable oil per square mile.

Let’s do the math on that one: 9,800 sq. miles x 3,600,000 = 35 billion barrels of oil.

That’s a gross resource value of $3 trillion at today’s WTI price of $91 per barrel.

It’s a resource treasure for the United States, plain and simple. With Devon’s estimate of 3.6 million barrels per square mile, it exceeds the Bakken and Eagle Ford by nearly 50%.

The Eagle Ford pay zone is 20 to 35 feet thick; the Bakken is 10 to 25 feet thick… but the Cline is estimated to be anywhere from 200 to 550 feet thick. It’s enormous.

And the Cline resides inside the legendary, prolific Permian Basin, which to date has pumped out some 35 billion barrels of oil from multiple pay zones.

Drillers are going back for the oil that’s been left behind.

And they’re finding more and more formations within the Permian…

That’s why the play is the hottest in the world right now.

With the price of oil spurring activity, the Permian rig count has increased nearly 339% since April 2009, from 92 to 404 at the end of January.

Get ready to make money off of this play. It’s going to go great guns for decades.

Forever wealth,

![]()

Brian Hicks

Brian is a founding member and President of Angel Publishing and investment director for the income and dividend newsletter The Wealth Advisory. He writes about general investment strategies for Wealth Daily, Energy & Capital, and the H & L Market Report. Known as the “original bull on America,” Brian is also the author of Profit from the Peak: The End of Oil and the Greatest Investment Event of the Century, published in 2008. In addition to writing about the economy, investments and politics, Brian is also a frequent guest on CNBC, Bloomberg, Fox, and countless radio shows. For more on Brian, take a look at his editor’s page.

A new idea for value investors. Our long time friend and contributor Michael Williams was one of the keynote technical speakers at the recent Prospectors & Developers Conference – the world’s largest mining and mineral industry event. He made the case for significant future demand and low supply for Zinc. Of interest to our MoneyTalks audience is his argument that Zinc could be THE place for contrarian investors looking for an early entry point.

A new idea for value investors. Our long time friend and contributor Michael Williams was one of the keynote technical speakers at the recent Prospectors & Developers Conference – the world’s largest mining and mineral industry event. He made the case for significant future demand and low supply for Zinc. Of interest to our MoneyTalks audience is his argument that Zinc could be THE place for contrarian investors looking for an early entry point.

Michael was kind enough to share this private presentation with MoneyTalks.

U.S. Stock Market – I’ve no desire to not look a gift horse in the mouth after refraining from taking bearish stances on the U.S. stock market since March of 2009. While I continue to suggest the most likely path I envision going forward was depicted in the chart above, you will note that it allows for the market to still see another 10% or so rise before a vicious bear market decline takes hold. That’s why after making a new, all-time high, I’ve suggested a scale-up sell approach as a prudent approach for those who own general U.S. equities (and instead used companies whose majority of business is derived outside the United States).

U.S. Bonds – Worse investment for the next decade.

U.S. Dollar – For the 1% or so of high-risk speculators who can truly afford the financial risks and mental anguish of future’s trading, the 83 – 84 area on the U.S. Dollar Index to me looks like an area to establish a short position.

Gold – While Friday’s hunch proved correct, it won’t matter much unless we can get above $1,600 and stay there. If and when we do, then I think the overwhelming number of bears can capsize their boat and we could see an abandon ship cry go out. Remember, gold is hated by most who work in the financial arena and much of the media that reports on it, so stop looking for them to throw you any bone on how the bear trade may be going bad.

Mining and Exploration Stocks – Another week of not going down is needed to stem the free fall. Gold rising above $1,600 can be a much needed added boost. Don’t lose sight that there’s going to be a wall of selling for quite some time as its almost a universal position now among retail investors to get out and never come back to junior resource stocks. Volume will need to come in before price movement can advance.

Grandich Client Companies

Alderon Iron Ore – I had a chance to speak with Mark Morabito this weekend before he left for a multi-week trip to Asia. As of Saturday, he knew of no reason why the final check from strategic partner HBIS wouldn’t be coming by weeks end. His comment to me was “… if I thought there was going to be a problem, I wouldn’t be off to Asia. I can tell you that part of my trip is to speak about our relationship with HBIS going forward, meet with potential new partners via an additional off-take agreement and institutional investors…”

Donner Metals – Good news continues to flow from DON during the worse junior resource market in my 30 years in and around the financial arena. DON is looking forward to building on its success and I hope to have a Q & A with one of its senior management about this in the not-too-distant future.

Excelsior Mining – Mark Morabito asked that I be a little patient as he hopes one or more possibilities MIN is working on can bear fruit soon. What choice do we really have anyway?

Geologix Explorations – A critical report is due out shortly. The anticipation is it can show GIX to be a holder of a very viable project with strong upside potential. Stay tuned.

Oromin Explorations – I had an update from OLE at weeks-end and this is the gist of what I came away with:

- The main goal is to conclude a purchase of the company.

- If for some reason a sale of the project isn’t doable, many parties have expressed serious interest in supporting OLE going into production

- The jv partners of OLE are all willing to accept equity in any sale

- OLE management did the loan deal versus an equity financing because it believes it can successfully conclude a purchase of its main asset and such a loan was a better choice for shareholders. They believe it won’t become a problem if they aren’t sold and need to employ other strategic strategies

- They have engaged outside firms to assist with investor relations

Given what has happened in the junior resource market, I, along with other OLE shareholders can’t be thrilled to see a 40%+ drop in the share price. However, I believe it’s not because of anything just at the feet of OLE but a market in general reality.

It’s important to appreciate that as crazy as it may sound, the debacle in the junior market may have led to OLE to stand out more than before. It’s evident that early to late stage exploration companies are going to have a tough go at it for a while. But how many construction ready 3-5 million ounces (with potential for more), hi-grade deposits are available today? Knowing how the financing and institutional segment of the industry works, I suspect they will greatly narrow the focus of what they will put their money in for the foreseeable future and I believe OLE is among the very few type of deals that still look viable in their eyes.

Because I receive more emails about OLE than all other clients combined, I like to save time by again suggesting you avoid basing your decisions on something you read on a chat forum. I will never begin to understand how someone claiming to be a shareholder but spends their entire time on one of these forums complaining about the company remains a shareholder. What possible motive do they have when there’s an easy remedy for them – SELL!

People ask me how do you know when to sell? When you couldn’t first buy today what you currently own, who then do you expect to do so and to keep doing so until you get back to where you started? Hope is a wonderful mental strategy but a lousy investment one.

Precipitate Gold – As I noted since I began working for them, I pull a little extra in hoping this is the exception to the rule in junior resource stocks. In the short time I’ve been associated with it, nothing has suggested it can’t be.

Ridgemont Iron Ore – Back to square one so don’t expect anything. I’ve a two million share buy order in at a penny so I can average down my cost and bet on Morabito finding a new avenue for the company. It will be a long haul even if he can.

Sunridge Gold – Simply put, when you look at what now appears to be its sixth deposit, the worth of such deposits versus the current market valuation, it literally makes no sense. But given the country they operate in and the state of the industry, one can at least try to understand such a low valuation. This may change despite all of this when their key study is out by the end of April.

Timmins Gold – Like so many other emerging producers, it got thrown out with the bath water. IMHO, it may become a takeover target down at these levels.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair