Energy & Commodities

The value of the crude oil production alone is worth a staggering $1.7 trillion each year. Add downstream fuels and other services to that, and oil is a money-making machine.

Both companies and governments take advantage of this resource wealth. More of the world’s largest companies work in the oil patch than any other industry. At the same, entire government regimes are kept intact thanks to oil revenues.

The only problem when an industry becomes this lucrative?

Eventually, everybody wants a piece of the pie – and they’ll do anything to get their share.

THE BLACK MARKET IN FUEL THEFT

Today’s infographic comes from Eurocontrol Technics Group, and it highlights the global problem of fuel theft.

While pipeline theft in places like Nigeria and Mexico are the most famous images associated with the theft of hydrocarbons, the problem is actually far more broad and systematic in nature.

Fuel theft impacts operations at the upstream, midstream, and downstream levels, and it is so entrenched that even politicians, military personnel, and police are complicit in illegal activities. Sometimes, involvement can be traced all the way up to top government officials.

E&Y estimates this to be a $133 billion issue, but it’s also likely that numbers around fuel theft are understated due to deep-rooted corruption and government involvement.

HOW FUEL THEFT ACTUALLY HAPPENS

Billions of dollars per year of government and corporate revenues are lost due to the following activities:

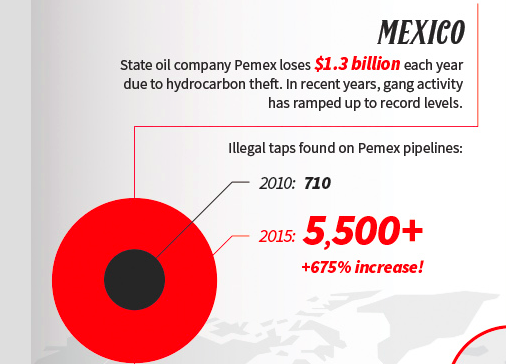

Tapping Pipelines: By installing illicit taps, thieves can divert oil or other refined products from pipelines. Mexican drug gangs, for example, can earn $90,000 in just seven minutes from illegal pipeline tapping.

Illegal Bunkering: Oil acquired by thieves is pumped to small barges, which are then sent to sea to deliver the product to tankers. In Nigeria, for example, the Niger Delta’s infamous labyrinth of creeks is the perfect place for bunkering to go undetected.

Ship-to-Ship Transfers:

This involves the transfer of illegal fuel to a more reputable ship, which can be passed off as legitimate imports. For example, refined crude from Libya gets transferred from ship-to-ship in the middle of the Mediterranean, to be illegally imported into the EU.

Armed Theft (Piracy):

This involves using the threat of violence to command a truck or ship and steal its cargo. Even though Hollywood has made Somalia famous for its pirates, it is the Gulf of Guinea near Nigeria that ships need to be worried about. In the last few years, there have been hundreds of attacks.

Bribing Corrupt Officials:

In some countries – as long as the right person gets a cut of profits, authorities will turn a blind eye to hydrocarbon theft. In fact, E&Y says an astonishing 57.1% of all fraud in the oil an gas sector relates to corruption schemes.

Smuggling and Laundering:

Smuggling oil products into another jurisdiction can help to enable a profitable and less traceable sale. ISIS is famous for this – they can’t sell oil to international markets directly, so they smuggle oil to Turkey, where it sells it at a discount.

Adulteration:

Adulteration is a sneaky process in which unwanted additives are put in oil or refined products, but sold at full price. In Tanzania, for example, adding cheap kerosene and lubricants to gasoline or diesel is an easy way to increase profit margins, while remaining undetected.

THE IMPLICATIONS OF FUEL THEFT

The impact of fuel theft on people and the economy is significant and wide-ranging:

Loss of corporate profits: Companies in oil and gas can lose billions of dollars from fuel theft. Case in point: Mexico’s national oil company (Pemex) is estimated to lose $1.3 billion per year as a result of illegal pipeline tapping by gangs.

Loss of government revenues: Governments receive royalties from oil production, as well as tax money from finished products like gasoline. In Ireland, the government claims it loses €150 to €250 million in revenues per year from fuel adulteration. Meanwhile, one World Bank official pegged the Nigerian government’s total losses from oil revenues stolen (or misspent) at $400 billion since 1960.

Funds terrorism: ISIS and other terrorist groups have used hydrocarbon theft and sales as a means to sustain operations. At one point, ISIS was making $50 million per month from selling oil.

Funds cartels and organized crime: The Zetas cartel in Mexico controls nearly 40% of the fuel theft market, raking in millions each year.

Environmental damage: Not only does fuel theft cost corporations and governments severely, but there is also an environmental impact to be considered. Fuel spills, blown pipelines, and engine damage (from adulterated fuel) are all huge issues.

Leads to higher gas prices: Unfortunately, all of the above losses eventually translate into higher prices for end-customers.

HOW TO STOP FUEL THEFT?

There are two methods that authorities have been using to slow down and eventually eliminate fuel theft.

Fuel dyes are used to color petroleum products a specific tint, so as to allow for easy identification and prevent fraud. However, some dyes can be replicated by criminals – such as those in Ireland who “launder” the fuel.

Molecular markers, which are used in tiny concentrations of just a few parts per million, are invisible and can also be used to identify fuels.

In Tanzania, the initiation of a fuel marking program using molecular markers led to significant increases of imported petrol and diesel for the local market, and a decrease of kerosene.

At the retail level, product meeting quality standards increased from 19% in 2007 to 91% in 2013. Ultimately, this resulted in an increase of tax revenue of $300 million between 2010 and 2014.

While diamond industry experts warn that demand is expected to outstrip supply as early as 2019, the largest mines keep producing the coveted rocks at full steam.

Here are last year’s top 10 diamond mines in terms of output and value, based on data compiled by expert Paul Zimnisky.

(Image courtesy of De Beers Group.)

1. Jwaneng, Botswana

Produced 11,975,000 carats, worth $2,347 million

Jwaneng, the richest diamond mine in the world, is located in south-central Botswana in the Naledi river valley of the Kalahari. It’s 2 kilometres across at its widest point and patrolled by colossal 300-tonne trucks that labour up the terraced slopes.

Nicknamed “the Prince of Mines”, Jwaneng was opened in 1982, as the diamond trade helped Botswana go from being one of the world’s poorest countries to one of Africa’s wealthiest.

Sunrise at Yubileyny open-pit. (Image by Ruslan Akhmetsaphin | ALROSA.)

2. Jubilee, Russia Produced 9,231,000 carats, worth $1,431 million

Belonging to ALROSA, the world’s top diamond miner by output in carats, the Jubilee mine (also known as Yubileinaya), has been in production since 1989. It’s among the world’s biggest diamond mines by area.

Image courtesy of Diamond Producers Association

3. International, Russia

Produced 3,948,000 carats, worth $829 million

Also known as Internatsionalny, this underground mine has been in operations since 1999. ALROSA estimates the deposit will run out of diamonds by 2022.

Image courtesy of Diamond Producers Association

4. Orapa, Botswana

Produced 7,931,000 carats, worth $753 million

The Orapa mine is the ninth largest diamond mine in the world by reserve and the world’s largest mine by area. It has been in production since 1971. It’s owned by Debswana, a joint venture of De Beers and the Botswana Government.

Currently Orapa is mining at a depth of 250 metres and is expected to reach 450 metres by 2026.

Aerial view of Debmarine’s Debmar Atlantic vessel, which mines diamonds off the coast of Namibia. (Image courtesy of Diamond Producers Association)

5. Debmarine, Namibia

Produced 1,169,000 carats, worth $585 million

De Beers’ Debmarine uses a fleet of five specialized marine mining vessels to screen material recovered from the ocean floor.

These deposits are then airlifted by helicopter for further processing on shore. It’s Namibia’s largest diamond producer, accounting for 70% of the country’s output of these stones.

(Image courtesy of Wenco)

6. Catoca, Angola

Produced 6,700,000 carats*, worth $570 million

This diamond mine is the world’s fourth largest. It’s owned by a consortium of international mining interests, with Endiama (the state mining company of Angola) having a majority stake.

* = Figure not officially confirmed

(Image courtesy of ALROSA)

7. Nyurbinskaya, Russia

Produced 5,001,000 carats, worth $565 million

The Nyurba Mining and Processing Division (MPD) is one of the youngest enterprises of ALROSA. It operates at the Nakyn ore field, which includes the Nyurbinskya and Botuobinsky open-pits, and two same-name alluvial placers.

The impressive Diavik. (Image: Rio Tinto.)

8. Diavik, Canada

Produced 6,658,000 carats, worth $539 million.

Operated by Rio Tinto, which owns 60% of the mine, Diavik began production in 2003 and has an annual output of some 6-7 million carats of predominantly large, white gem-quality diamonds. It’s Canada’s largest diamond mine in terms of carat production. Dominion Diamond owns the remaining 40%.

Aerial view of the Ekati mine, 300 kilometres northeast of Yellowknife. (Image: Dominion Diamond Corporation)

9. Ekati, Canada

Produced 5,200,000 carats, worth $463 million

The Ekati Diamond Mine (named after the Tlicho word meaning “fat lake”) is Canada’s first surface and underground diamond mine. Located about 300km north-east of Yellowknife, near Lac de Gras in Canada’s North-West Territories, is run by Dominion Diamond Corporation (DDC).

(Image courtesy of ALROSA)

10. Mir, Russia

Produced 3,191,000 carats $463 million

Although open pit mining at this operation ended in 2004, ALROSA built a series of underground tunnels, which have continued to yield high-quality rough diamonds. The remaining pit is so huge it creates a vortex potentially strong enough to suck helicopters into its depths.

By Cecilia Jamasmie via Mining.com

WTI and Brent continued to tumble on Thursday, dropping to their lowest levels since the announcement of the OPEC deal back in November. Brent actually dipped below $49 per barrel, raising fears of another downturn. Both WTI and Brent were off by nearly 4 percent during midday trading on Thursday.

WTI and Brent continued to tumble on Thursday, dropping to their lowest levels since the announcement of the OPEC deal back in November. Brent actually dipped below $49 per barrel, raising fears of another downturn. Both WTI and Brent were off by nearly 4 percent during midday trading on Thursday.

Oil traders have been patient, hoping that despite the rapid rebound in U.S. shale production, the OPEC cuts would take a substantial volume of oil off the market and correct the supply/demand imbalance. But it has been a painful and protracted process.

U.S. crude oil inventories hit a record high of 535 million barrels as recently as the end of March. Several consecutive weeks of drawdowns in April again raised hopes that the market is heading towards balance, but the most recent data release from the EIA on May 3 disappointed yet again, and it was apparently the last straw for some. Market analysts predicted a drop in oil inventories by about 2.3 million barrels, but the EIA said stocks only fell by 930,000 barrels. WTI sank to $46 per barrel and Brent fell into the $40s for the first time in 2017.

…related:

Total SA’s chief energy economist, Joel Couse, forecasted that EVs will make up 15 to 30 percent of global new vehicle sales by 2030.

Total SA’s chief energy economist, Joel Couse, forecasted that EVs will make up 15 to 30 percent of global new vehicle sales by 2030.

Oil demand for transportation fuel see its “demand will flatten out,” after 2030, “Maybe even decline.” Couse said speaking this week at the Bloomberg New Energy Finance conference in New York.

Colin McKerracher, head of advanced transport analysis at Bloomberg New Energy Finance, sees Couse’s forecast as the highest EV sales margin yet to be forecasted by a major company in the oil sector.

“That’s big,” McKerracher said. “That’s by far the most aggressive we’ve seen by any of the majors.”

Royal Dutch Shell Plc sees a similar trend with oil demand in transportation flattening out in the near future. Chief Executive Officer Ben van Beurden said in March that oil demand may peak in the late 2020s. In November during an interview, Shell CFO Simon Henry said that demand is expected to peak in about five years.

Shell and Total SA have been looking to diversify their energy assets through hydrogen as a transport fuel. In January, both companies joined a global hydrogen council that included Toyota, Liquide SA, and Linde AG. The companies will be investing about $10.7 billion in hydrogen products over the next five years.

Like hydrogen fuel cell vehicles, electric vehicles have major walls to climb to find mass adoption in vehicle sales and infrastructure. One barrier is the cost of owning an electric vehicle versus a cheaper, comparable gasoline-engine vehicle. The battery pack in an EV can be quite expensive, making up half the cost of the car, according to BNEF.

Backers of EVs point to two trends fast approaching the market; with one being the longer range, 200-plus-miles per charge EVs coming to market like the Chevy Bolt and Tesla Model 3. The higher-priced versions of the Tesla Model S and Model X are thought to be a sign of it, with consumers willing to finance or lease one of these EVs to gain access to more power and longer range.

Automaker are feeling pressed by strict emissions reduction rules in Europe and China, with other markets like the U.S., Japan, and South Korea having similar standards.

Auto Shanghai has been a showcase for existing and startup automakers launching several EVs to the China market, with some of them ending up overseas.

It’s helping that lithium ion battery prices are dropping about 20 percent year, as automakers spend billions on electrifying their vehicle lineups. Volkswagen wants to see at least 25 percent of its vehicles sold in 2025 to be EVs. Toyota is moving toward selling zero fossil-fuel powered vehicles by 2050.

Another sign that the Total SA report carries some weight is the diverse and broad portfolio of EVs that automakers till be rolling out on the market soon.

“By 2020 there will be over 120 different models of EV across the spectrum,” said Michael Liebreich, founder of Bloomberg New Energy Finance. “These are great cars. They will make the internal combustion equivalent look old fashioned.”

Electric cars only make up about 1 percent of global vehicle sales, so making it to 30 percent in the short-term future would be a huge leap. Analysts point to a few market forces that need to be addressed before that technology takes off in sales. Among those issues are pre-incentive prices coming down, distance per charge going up beyond 300 miles, and the fast charging infrastructure becoming pervasive and cost competitive to gas pumps.

As we get ready to kickoff what promises to be a wild week of trading, today the man who has become legendary for his predictions on QE, historic moves in currencies, spoke with King World News about what is going to come as a massive shock to people.

“This Is The New Normal!”

Egon von Greyerz: “This is the new normal”! That is what a professional advisor stated at a recent family office in London after I had outlined the risks due to the credit and asset bubbles. This is what is so frightening about any top in such an extreme economic cycle. Peak optimism and peak asset prices go hand in hand. I did not experience the 1929 crash or the depression, but a few quotes from that remarkable period of time expresses the typical euphoria at a market peak.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair