Energy & Commodities

Strengths

- The best performing precious metal for the week was pretty much a tie between gold, platinum and palladium with roughly a 0.50 percent gain. Following the launch of a U.S. missile strike on Syria this week, gold rallied to its highest level in nearly five months, reports Bloomberg. Bullion was pushed back above its 200-day moving average, a level that analysts use to predict whether further gains will continue or stall.

- Earlier in the week, the minutes from the Federal Reserve’s March meeting “boosted gold prices with the mention of the shrinking of the balance sheet,” said Jingyi Pan, a Singapore-based market strategist, reports Bloomberg. “This agenda could potentially conflict with the pace of rate hikes, therefore placing pressure on the dollar.” In addition, gold advanced after automobile manufacturers reported worse-than-expected U.S. sales for March.

- BullionVault’s Gold Investor Index, measuring the balance of buyers against sellers, rose to 54.2 in March from 51.8 in February, reports Bloomberg. “Political risk continues to drive private investor demand for gold,” Adrian Ash, head of research at BullionVault, said in a report.

Weaknesses

- The worst performing precious metal for the week was silver, with a fall of 1.30 percent. Late Friday CFTC data showed that money managers actually increased their bullish opinion on silver to the highest level in more than eight months. Profit taking, post the morning surge in precious metals prices, late Friday pulled silver into a loss for the week. Gold reserves in China’s central bank remained unchanged for the month of March, coming in at 59.24 million ounces, reports Bloomberg. This is the fifth straight month that gold reserves have remained unchanged.

- Despite Goldman Sachs encouraging investors to have “patience” for the commodity market in the wake of a waning price rally, inflows into ETFs linked to raw materials have significantly plunged in recent weeks, reports Bloomberg. Goldman believes the pace of economic growth in China will drive raw-materials consumption. In a similar fashion, RBC Mining & Material Equity Team cut its precious metals recommendation to underweight from market weight for the second quarter, reports Bloomberg. It upgraded bulk commodities to overweight from market weight and fertilizers to market weight from underweight.

- In Canaccord Genuity’s Precious Metals Note this week, the group says we may see potential NAV multiple compression in the sector. It notes margin compression, rising management compensation, declining IRR hurdle rates and rising operational and geopolitical risks as potential headwinds that could temper enthusiasm for gold producers.

Opportunities

- In its U.S. Economics report this week, Macquarie Research says that demographic forces are intensifying, as the share of population 75+ begins to rise. Because of this, the group says the economy is confronting two headwinds, or “double trouble”: 1) a closing of the output gap and the end of slack and 2) unprecedented demographic change that has accumulated over the past seven years is now intensifying. They believe the Fed Funds may normalize at 1.5 to 1.75 percent and the 10-year Treasury yield at around 2.3 percent, well below consensus of 3 percent for Fed Funds and 3.5 percent for 10-year yields. With CPI running at 2.7 percent, it is likely we will continue to see flat to negative real rates, thus supportive of gold. And in a note from BMI Research, the team says gold can be supported as the Fed is likely to raise rates only once more in 2017.

- The technical team from Desjardins says that the gold price (COMEX) has substantial potential upside. The team notes that total known ETF holdings of gold have increased around 2 million ounces year-to-date, implying a gold price of $1,310 per ounce. Similarly, Comex paper claims to physical gold continue to soar to 45:1, while deliverable gold has contracted by 50 percent since the start of the year.

- Zacks Investment Research highlights Klondex Mines in an article this week, calling the company an “off-the-radar potential winner” and saying it looks well positioned for a solid gain, but has been overlooked by investors lately. Klondex has seen estimates rise over the past month for the current fiscal year by about 22.2 percent, although that is not yet reflected in its price, as the stock lost 21.7 percent over the same time frame, Zacks writes. The company carries a Zacks Rank #2, a strong buy, further underscoring the potential for its outperformance. Another company with positive coverage this week is Rye Patch Gold, initiating a buy recommendation from George Topping from Industrial Alliance Securities. Topping predicts that Rye Patch will trade at 75 cents within a year, implying a potential 124 percent gain.

Threats

- The Senate voted along party lines on Thursday to change the Supreme Court’s longstanding rules and effectively eliminate the filibuster for Supreme Court nominees, reports Bloomberg. Now it will only require 51 votes, not 60, to bring a nominee up for a confirmation vote. The Senate confirmed on Friday Judge Neil Gorsuch as the new Supreme Court Justice, restoring the generally conservative majority. Some commentators noted that this may embolden President Trump to now pick even more judges for the bench that are more divisive, since a simple majority will be all that is needed to confirm. Similarly, Adam Posen, president of the Peterson Institute for International Economics, says that Trump is likely to pick a Fed chairman who is “very responsive to him.”

- In its Global Precious Metals Comment this week, UBS points out that European diesel share decline accelerated in March, supporting its view on platinum group metals (PGMs). Diesel share in the top five European auto markets declined, bringing the share of diesel vehicles to a multi-year low of 40.6 percent. The UBS Global Autos team expects this trend to accelerate further out, resulting in falling platinum demand.

- Goldman Sachs writes this week, that after five years of operating cost deflation, we expect costs to start responding to the 40 percent rebound in metal prices witnessed since January 2016. Once earnings tailwinds, we believe these core cost drivers should now start putting upward pressure on the full spectrum of global cost curves, Goldman continues. Additionally, the group notes that not all costs can be controlled, explaining that around 85 percent of the copper industry’s opex improvement was driven by what it considers to be “uncontrollable costs.”

Investing.com – Crude prices gave up some of the early gains in Asia on Monday with tensions on the Korean peninsula in focus along with the fallout from a missile strike by U.S. forces last week on a Syrian airbase that drew a sharp rebuke from major oil producers Iran and Russia.

Investing.com – Crude prices gave up some of the early gains in Asia on Monday with tensions on the Korean peninsula in focus along with the fallout from a missile strike by U.S. forces last week on a Syrian airbase that drew a sharp rebuke from major oil producers Iran and Russia.

On the ICE Futures Exchange in London, Brent oil for June delivery wrose 0.14% to $55.32 a barrel. Elsewhere, the U.S. West Texas Intermediate crude May contract rose 0.25% to $52.37 a barrel.

Last week, oil futures settled higher for the fourth session in a row on Friday, extending a rally to the strongest level in around a month after two U.S. destroyers based in the Eastern Mediterranean fired 59 Tomahawk cruise missiles at a Syrian air base, which the U.S. said was in retaliation to Bashar al-Assad’s alleged use of chemical weapons against his own people.

Oil pared some of the gains later in the session as concerns about a wider escalation in the region faded and U.S. economic data weighed on global markets.

But analysts said the initial knee-jerk reaction to the airstrike may have been overdone given Syria’s role as a very minor oil producer and after U.S. officials described the attack as a one-off event that would not lead to wider escalation.

Meanwhile, oil traders continued to focus on the ongoing rebound in U.S. shale production, which could derail efforts by other major producers to rebalance global oil supply and demand remained in focus.

Oilfield services provider Baker Hughes said late Friday that the number of active U.S. rigs drilling for oil rose by 10 last week, the 12th weekly increase in a row. That brought the total count to 672, the most since September 2015.

Earlier in the week, the U.S. Energy Information Administration said that crude oilinventories increased by 1.57 million barrels to yet another all-time high of 535.5 million.

It was the 13th weekly build in U.S. stockpiles in the past 15 weeks, feeding concerns about a global glut.

Market participants, however, remained optimistic that OPEC would extend its current deal with non-OPEC producers to cut output beyond June in an effort to rebalance the market. In November last year, OPEC and other producers, including Russia agreed to cut output by about 1.8 million barrels per day between January and June.

A joint committee of ministers from OPEC and non-OPEC oil producers will meet in late April to present its recommendation on the fate of the pact. A final decision on whether or not to extend the deal beyond June will be taken by the oil cartel on May 25.

Investors will keep an eye out for monthly reports from the Organization of Petroleum Exporting Counties and the International Energy Agency to gauge global supply and demand levels.

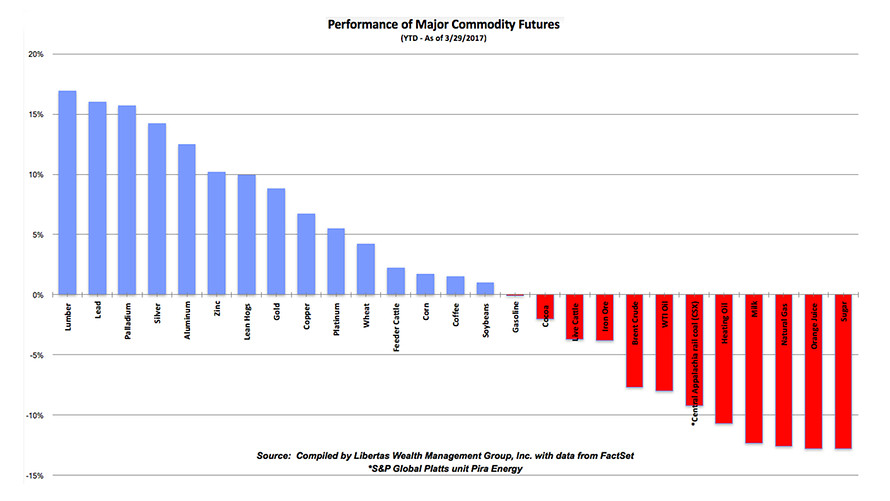

As the first quarter ends, losers outnumbered winners when it comes to commodities—undoubtedly much to the disappointment of those who expected the sector to build on last year’s bounce.

“The first quarter of 2017 has been disappointing, especially after last year’s brief, but promising rebound from a 5-year downtrend, as commodities just haven’t managed to gain any traction into the post-[U.S.] election year,” said Adam Koos, president of Libertas Wealth Management Group.

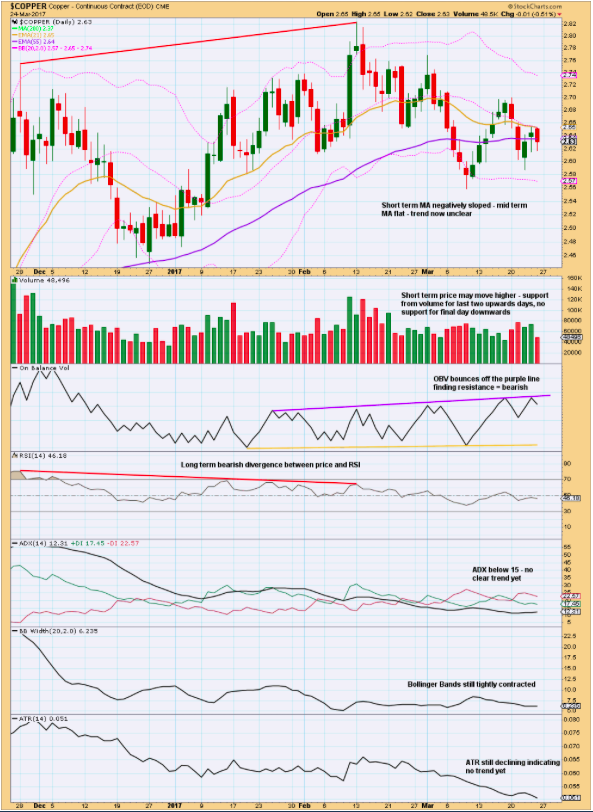

Trading Room will focus on classic technical analysis. Elliott wave analysis will be for support and for targets/invalidation points.

Copper (Spot)

TECHNICAL ANALYSIS

Notwithstanding that oil demand has increased for over 150 years, it will eventually stop increasing. If oil demand were to reach an actual peak, then the top might be easier to predict. As it stands, the forecast models of demand are likely predicting peak demand far later than it will be.

Notwithstanding that oil demand has increased for over 150 years, it will eventually stop increasing. If oil demand were to reach an actual peak, then the top might be easier to predict. As it stands, the forecast models of demand are likely predicting peak demand far later than it will be.

The so-called balance of supply and demand has always been a moving target, a race to the top in which the two run neck and neck. Imbalances result from out-of-step growth rates and not from movements away from a stationary balance. Perversely, imbalances breed further imbalances as the supply and demand components are provoked in opposite directions but with different timing, magnitudes and inertias. Without sufficient damping, the market has often overcompensated. Of course, there are also exogenous events like political turmoil, policy shifts, technological innovations and demographic changes which can unexpectedly and significantly alter not just the immediate balance but fundamentally shift the way supply and demand curves respond to price movements. The trends are plagued by inherent and irreducible irregularities.

Such a structural change has recently occurred. High prices persisted long enough for the industry in the U.S. to build a larger fleet of modern rigs and to learn how effectively to hydraulically fracture shale wells. It also persisted long enough for new efficiencies to incubate towards maturity, and the Paris accords promised to further reduce carbon emissions through policy changes. By the time that Saudi Arabia finally acted to protect not only its place among suppliers but also, and more importantly, the role of oil in the world economy. The backbone of shale supply in the U.S. was strong, and the seeds of lesser use were established. After these fundamental shifts, the rest of the world realized what Saudi Oil Minister Al-Naimi argued long ago and what Shell Oil has more recently asserted, namely that peak demand will occur long before peak supply.

To understand the trajectory of demand growth, we turn to econometric models like those published by the EIA and IEA. The central problem with long term supply and demand models is that they require assumptions about the many and interrelated responses to today’s prices. Though modeled responses may be tuned with low precision to relatively recent events and new realities, the actual response curves are poorly constrained and continue to evolve, in some cases at an accelerating pace. As the aphorism goes, all models are wrong, but some are useful.

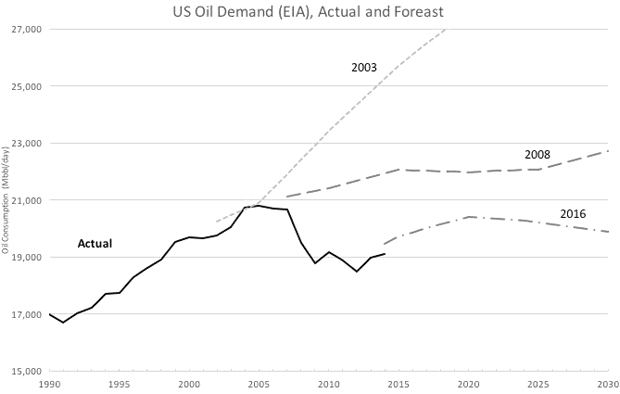

The EIA, IEA and other public econometric models call for global oil demand to continue growing through 2040, and the EIA even calls for renewed growth in the U.S. and OECD demand. The forecasts of growth in global demand rely upon increased use by developing countries, most importantly China and India. On the other hand, the United States has already seen demand decline for about 13 years. In fact it was the second to last of the world’s seven major developed countries to enter demand decline, and the entire OECD group of countries has, as a whole, seen shrinking demand since 2007. EIA data shows that 35 countries in all have already reached and descended from maximum oil demand. The experience of projected versus actual peak oil demand in the U.S. and OECD countries provides an empirical test and thus context to evaluate the current forecasts of growth and delayed maximum.

The following chart compares actual oil demand in the U.S. to several relevant demand forecasts of the EIA, all data coming from the EIA itself. U.S. demand reached a plateau for four years ending in 2007. Before, during, and even after the actual maximum demand, the models predicted decades of growth.

The next chart shows the same kind of comparison for the IEA’s models of OECD oil demand. Actual demand gently achieved its maximum in 2005. Even the alternative policy (lower demand) case in 2006 failed to capture the impending decline, but the reference cases adapted to the reality of declining demand much more quickly than did the EIA. Still the IEA over predicted the actual demand. Though not shown in charts, the EIA’s model of OECD demand growth and the IEA’s model of U.S. demand growth follow the same patterns. In short, these deeply technical and widely used referenced models missed badly the pivot point, the watershed of the object of analysis. For truly exculpatory reasons, the second and third order dynamics of reality were not captured by the models.

Rather than the theoretical calculation by such models, empirical observation of history is likely more informative when it comes to anticipating the timing of maximum demand. The graph below normalizes annual oil demand from the G7 countries with the U.S. shown in black, each normalized to its own year and volume of maximum demand. The scales show a 15 year window around the maximum annual consumption, and the pattern of the G7 is repeated in the OECD total and in most all of the 28 other countries.

The same data viewed on the scale of generations may resemble an alpine peak, but from the experience of living through it, demand does not peak. It sputters, surges and stalls as it rolls over from a slow incline into a slow decline. It is less a peak and more a crest of demand.

Sequential global demand forecasts over the last decade have projected slower growth, mostly now forecast at less than 1 percent, and sensitivity cases now allow for the possibility of substantial demand decline by 2040. Unfortunately, experience demonstrates that the crest will likely occur unexpectedly and sooner than predicted. And then our industry enters a whole new world as the moving balance of supply and demand turns into a race to the bottom.

By Dwayne Purvis for Oilprice.com

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair