Gold & Precious Metals

The movie “The Big Short” features Michael Burry. His statement from Zerohedge:

The movie “The Big Short” features Michael Burry. His statement from Zerohedge:

“It seems the world is headed toward negative real interest rates on a global scale. This is toxic. Interest rates are used to price risk, and so in the current environment, the risk pricing mechanism is broken.”

Repeat: “THE RISK PRICING MECHANISM IS BROKEN.”

What risks could be mispriced? A few come to mind.

- The world is saturated in debt – over $200 Trillion. Does anyone expect that debt to be repaid? What are the risks when over $200 Trillion in debt can be counted as an asset ONLY if that massive and increasing debt can be rolled over and replaced with say $300 Trillion in debt? What are the risks this exponentially increasing debt nonsense will be acknowledged for what it is – a train wreck in progress?

- The US stock market looks like it is rolling over, just as it did 7+ years ago in 2008, and 15 years ago in 2000, and 1994, and 1987. What are the risks that the S&P 500 is overvalued, that the P/E and a dozen other measures are overvalued, and the stock market will correct/crash? Think back to 2008, 2000, 1994, and 1987. Read: Tread Lightly – 2016 Technical Outlook.

- People and countries in the Middle East are not playing nice with each other. Regardless of whether the problems are religious, a 2,000 year feud, outside interference, control over gas and oil pipelines, or foreign policy stupidity, the region appears ripe for turmoil and more violence. Have risks been properly assessed? What happens if WWIII is born out of the fires of Middle East hatred, energy markets, and political posturing? Has that risk been properly priced into bond markets with negative yields, or stock markets with historically high P/E ratios, or crude oil prices at multi-year lows?

- Silver (paper) prices have been crushed by nearly five years of paper selling, derivatives, central bank manipulations, support for stock and bond markets, and more. Have the risks of financial turmoil, economic catastrophe, and escalating war been properly priced into paper COMEX silver prices?

- Actual physical gold has left the vaults in the western world and moved east into private and public vaults in Russia, India, and China. Have the risks of paper gold defaults (cash settlement) been priced into the COMEX paper price of gold? What if much of the gold supposedly vaulted in London, New York, and Fort Knox has mysteriously been replaced by “IOU gold” paper promises? Have the risks of missing gold and increasing demand for real physical gold been properly priced into the paper gold market?

- What is the risk of nuclear confrontation between Russia and the US? If we believe the bond markets, the risk is exceptionally low, since the prices of money (interest rates), are at multi-decade or perhaps multi-century lows. Have the risks of major war, or nuclear war, been mispriced in the bond market?

But looking on the silly side of a broken risk pricing mechanism … (SARCASM ALERT)

- Wall Street financial firms are doing “God’s Work” here on earth and will take care of the rest of us.

- Social Security recipients will receive no cost of living increase in 2016 because, per the Social Security Administration, “The law does not permit an increase in benefits when there is no increase in the cost of living.” Good to know there has been no increase in the cost of living during 2015! Apparently the Obamacare price INCREASES in premiums and deductibles compensated for other price increases…. (reminder – sarcasm alert).

- The Presidential race is heating up, but good things might happen in a single party political system masquerading as a two party process. Vote for the least offensive candidate and tell yourself there is a difference, not in the candidates, but in the policies that will be implemented.

- But don’t worry, be happy, trust debt based fiat currencies with no intrinsic value, and spend, spend, spend, because “deficits don’t matter.” Frankly, what could go wrong? Remember – sarcasm alert!

Silver thrives, paper dies! That mantra will serve us well in 2016 and 2017 since paper silver prices are currently very low compared to ratios to the US national debt, the S&P 500 Index, total global debt, fiscal and monetary silliness, and political stupidity (graphs not shown). If risk has been mispriced because the “risk pricing mechanism is broken” as Michael Burry says, then we should expect a volatile and traumatic year in 2016 as risk pricing adjusts.

Rig for stormy weather, expect surprises, markets regressing to the mean, pricing mechanisms failing, political systems collapsing, and Middle-East politics exploding. There will be blood and trauma. Do not trust the supposed value of paper assets and find security in real assets such as silver and gold bars and coins stored outside the financial system.

Silver thrives, paper dies!

Gary Christenson

The Deviant Investor

Who says gold lost its appeal as a safe haven asset?

After five straight positive trading sessions last week, the yellow metal climbed above $1,100, its highest level in nine weeks, on a weaker U.S. dollar.. The rally proves that gold still retains its status as a safe haven among investors, who were motivated by a rocky Chinese stock market, North Korea’s announcement that it detonated a hydrogen bomb last Wednesday and rising tensions between Saudi Arabia and Iran.

Here in the U.S., gold finished 2015 down 10.42 percent, its third straight negative year. Until the new year, sentiment appeared poor, and many gold bulls were finding it hard to stay optimistic.

But after the price jump last week, large exchange-traded gold funds saw massive inflows, confirming a shift in investors’ attitude toward the precious metal.

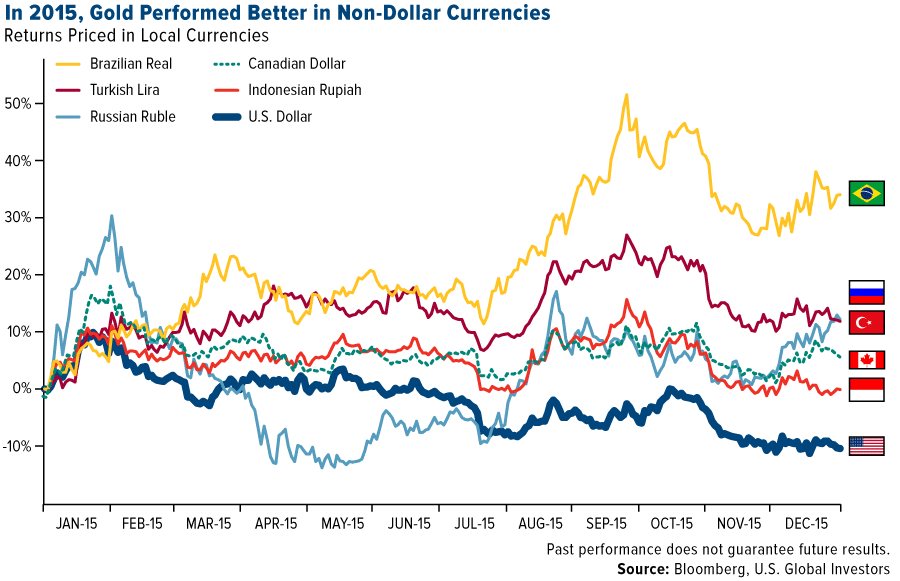

It’s worth remembering that about 90 percent of physical demand comes from outside the U.S., mostly in emerging markets such as China and India. In many non-dollar economies, buyers are actually seeing either a steady or even rising gold price. The metal is up in Russia, Peru, South Africa, Canada, Mexico, Brazil and many more.

Note the differences in returns between gold priced in U.S. dollars and gold priced in the Brazilian real, Turkish lira, Canadian dollar, Russian ruble and Indonesian rupiah.

Gold demand in China was very robust last year. A record 2,596.4 tonnes of the yellow metal, or a whopping

80 percent of total global output for 2015, were withdrawn from the Shanghai Gold Exchange. As for the Chinese central bank, it reported adding 19 more tonnes in December, bringing the total to over 1,762 tonnes. Precious metals commentator Lawrie Williams points out, though, that China’s total reserve figure is widely believed to be “hugely understated,” meaning the central bank might very well have much more than we’re being told.

Forget Interest Rates—Real Rates Are the Key Drivers of Gold

Despite all the talk of rising interest rates in connection to gold, they’re not a dominant driver of prices. Sure, rising nominal rates have tended to make the metal less attractive, since it doesn’t pay an income, but the larger driver by far are real interest rates. When real rates drop into negative territory, gold has historically done well.

As a reminder, real rates, important for the Fear Trade, are what you get when you subtract the consumer price index (CPI), or inflation, from the 10-year Treasury yield. As of January 6, the 10-year yield was 2.18 percent, while the 12-month CPI for November—December data will be released later this month—came in at a barely-there 0.50 percent. Real rates, therefore, are running at a positive 1.68 percent, which is a headwind for gold.

That’s why we need inflation to pick up, because then gold would be more likely to rally.

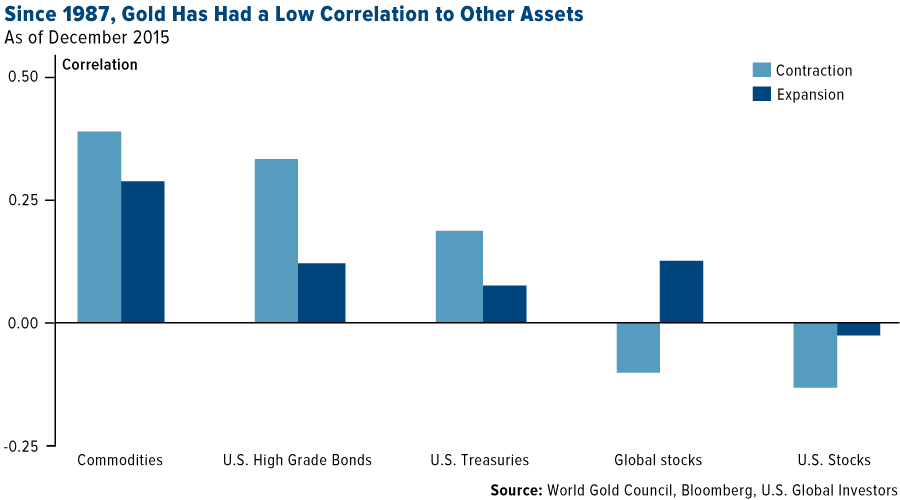

Regardless, the World Gold Council (WGC) writes in its 2016 outlook that gold’s role as a diversifier remains “particularly relevant”:

Research shows that, over the long run, holding 2 percent to 10 percent of an investor’s portfolio in gold can improve portfolio performance.

The reason for this is that gold has tended to have a low correlation to many other asset classes, making it a valuable diversifier. During economic contractions, for example, gold’s correlation to stocks actually decreased, according to data between 1987 and 2015.

For the last three years, gold has disappointed many because other investments, specifically equities, have seen such huge gains. But with global markets hitting turbulence, the yellow metal is looking more attractive as insurance against the currency wars.

I always recommend 10 percent in gold: 5 percent in gold stocks or an actively-managed gold fund, 5 percent in bullion and/or jewelry. It’s also important to rebalance every year.

This should be the case in both good times and bad, whether gold is rising or falling. As highly influential investment expert Ray Dalio said last year: “If you don’t own gold, you know neither history nor economics.”

USGI Among the First to Discuss the Significance of PMI as a Forward-Looking Indicator

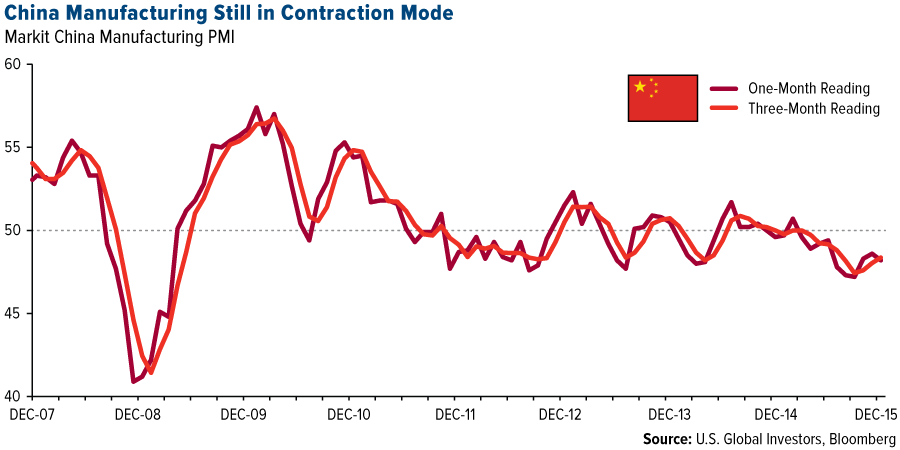

Aside from real interest rates, gold prices are being challenged by weak manufacturing data around the world. China’s purchasing managers’ index (PMI) fell to 48.2 last month, down 0.4 points from the November reading. The Asian giant’s manufacturing sector spent a majority of 2015 in contraction mode, managing to rise above the key 50.0 level only once last year, in February.

Although fears of a Chinese slowdown are real, they’re largely overdone. Consulting firm McKinsey & Company’s Gordon Orr calls these fears a distraction, writing that “the country’s economy is still massive—as are its potentional opportunities.”

Something to keep in mind is that China recently approved a new five-year plan, its 13th since 1953. Although we won’t know exactly what’s in it until March, we do know that these plans have been good for economic growth in the past. It’s likely that interest rates will be trimmed even more to stimulate business, with more funding diverted to infrastructure and “green” initiatives.

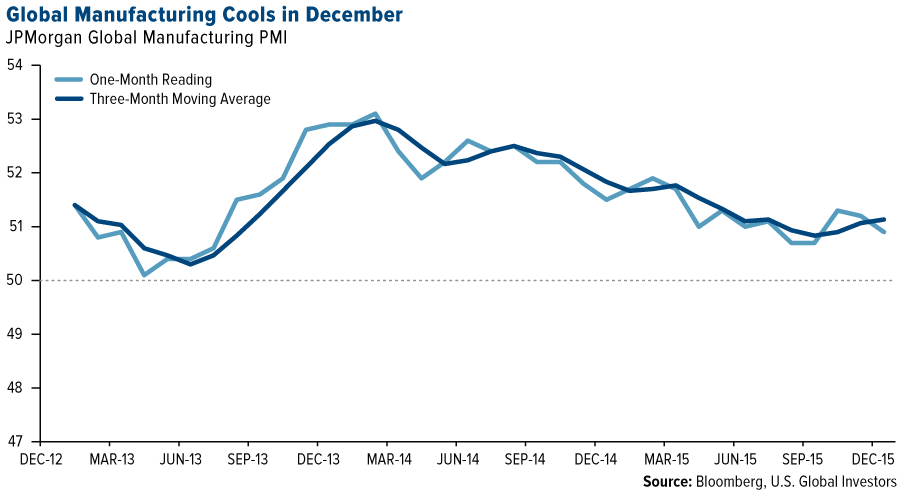

Manufacturing around the world showed signs of deterioration in December as well. The JP Morgan Global Manufacturing PMI declined to 50.9 from 51.2 in November. The sector is still in expansion mode, but just barely.

The reading also fell below its three-month moving average in December, which, as I’ve shown many times before, can have a huge effect on materials and energy three to six months out.

We were one of the earliest investment firms to monitor this important economic indicator closely and bring it into public, everyday discourse. (From what I can find, the first time we wrote about it was in January 2009, as it applied—wouldn’t you know?—to China.) Today, I hear and read about the PMI on the radio and in newspapers as often as I do more common economic indicators such as GDP and unemployment rates.

That’s a testament to the sort of cutting-edge analysis we do and pride ourselves on here at U.S. Global Investors.

Looking Ahead in the New Year

Until we see global synchronized growth with rising PMIs, we remain cautious going forward. A constant source of hope is the Trans-Pacific Partnership (TPP), which, when ratified sometime this year, will eliminate 18,000 tariffs for 25 percent of global trade.

We also anticipate more stimulus programs this year around the world. Lately we’ve experienced strong fiscal drag as more and more regulations and taxes impede progress that not even cheap money has been able to offset. A 2014 report by the National Association of Manufacturers (NAM) revealed that federal regulations in the U.S. alone cost businesses more than $2 trillion a year. To ignite growth, G20 nations should commit themselves to cutting red tape.

A good model for such a task is Canada’s “One-for-One Rule,” introduced in April 2012 during former Prime Minister Stephen Harper’s administration. The rule mandates that when a new or amended regulation is introduced, another must be removed.

However it’s accomplished, regulatory burdens placed on businesses must be reduced.

For more in-depth analysis, consider subscribing to our award-winning newsletter, the Investor Alert.

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor. By clicking the link(s) above, you will be directed to a third-party website(s). U.S. Global Investors does not endorse all information supplied by this/these website(s) and is not responsible for its/their content.

The Caixin China Report on General Manufacturing is based on data compiled from monthly replies to questionnaires sent to purchasing executives in over 420 manufacturing companies. The J.P. Morgan Global Purchasing Manager’s Index is an indicator of the economic health of the global manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment.

The article references the investment theory of an investment as insurance against a separate market event that could negatively affect performance of an investment. The reference does not guarantee performance or a safeguard from loss of principal by investing in that asset.

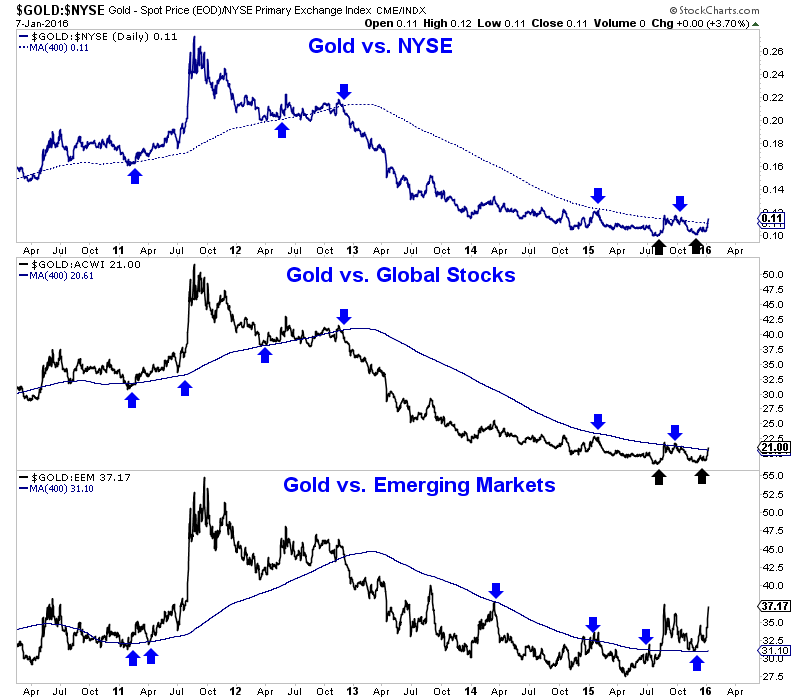

It has been a strong start to 2016 in precious metals, today notwithstanding. Gold was able to break above daily resistance at $1080 to $1090 while miners climbed higher until Friday’s reversal. Rather than focus on the nominal gains I want to turn our attention to Gold’s performance against other markets and asset classes. It is starting to turn in Gold’s favor and that is imperative if the precious metals bear market is to end in 2016.

We plot Gold against various equity markets in the chart below. These are daily line charts that include the 400-day moving average. Note how the moving average has been an excellent indicator of trend. At the bottom of the chart, we see that Gold last year broke its downtrend against emerging markets. The ratio is holding well above the moving average and nearing a test of its two year high. Gold against the NYSE and global equities is more interesting. The two ratios appear to have bottomed and are in the process of transitioning from downtrends to uptrends. It may take a few months or longer but we expect it to happen this year.

Gold vs. Equities

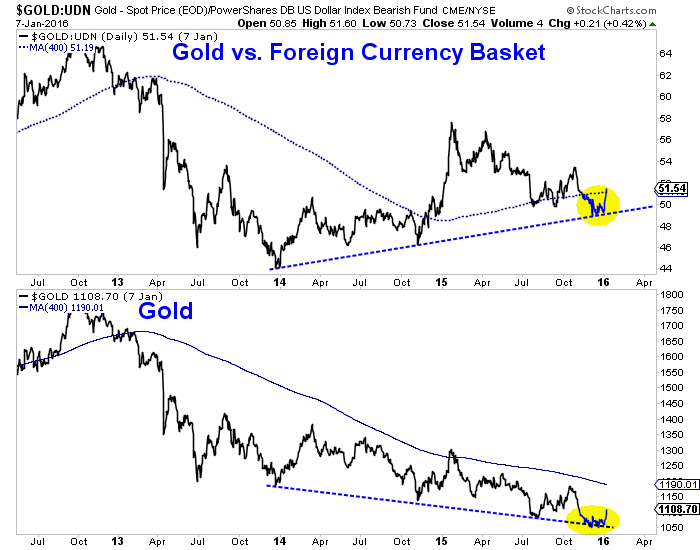

Gold’s relative strength is also apparent in the context of foreign currencies. We plot Gold against foreign currencies (FC) and Gold in US$ below. Although Gold/FC recently lost its 400-dma it rebounded after testing trendline support. Gold/FC has made higher lows over the past two years while Gold has made lower lows. This is not a total surprise given how Gold/FC has led Gold at key sector bottoms dating back to 2008, 2005 and 2001.

Gold vs. Foreign Currencies

Gold’s performance against other asset classes such as equities and currencies gives us additional insight to its current and future trend. We continue to expect the US$ to strengthen and Gold to have another leg down before its bear market ends. Gold’s performance against equities and foreign currencies can help us decipher the size and scope of Gold’s next leg down. If Gold is breaking out relative to stocks and holding strong against foreign currencies amid a nominal decline then Gold is gaining underlying strength and will be in position to rebound substantially when its nominal decline ends.

As for the short-term, we have rally targets of $1120 and $1130 to $1140 for Gold. Despite the strong decline in miners today we feel the group (GDX, GDXJ) has minimum upside targets at the 200-day moving averages. We intend to hedge our long positions when we feel the downside risk is increasing and we hope to be buyers in the event of sub $1000 Gold.

Jordan Roy-Byrne, CMT

Today’s videos and charts (double click to enlarge):

Bonds, Dollar, & US Stock Market Video Analysis

Gold & Silver Bullion Video Analysis

Key Precious Metal ETFs Video Analysis

Trader Time Swing Trades Video Analysis

Individual Precious Metal Stocks Video Analysis

Thanks,

Morris

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair