Gold & Precious Metals

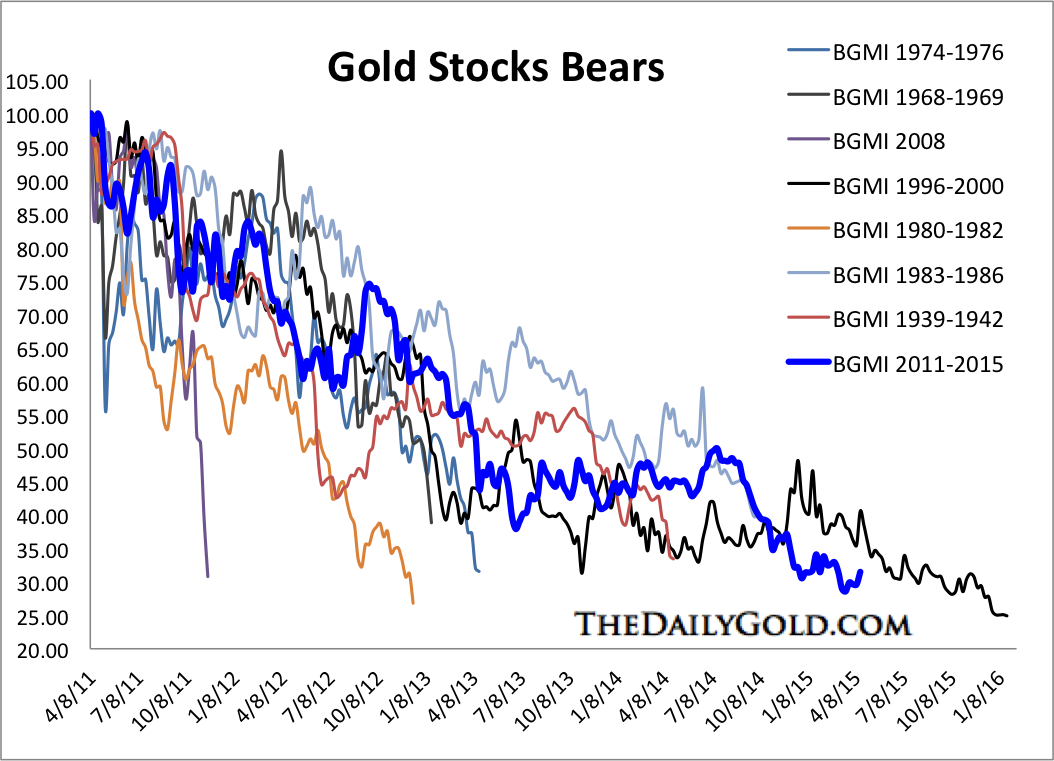

Everyone knows that this has been a devastating bear market for the gold mining sector. If you have followed our work you know that it is the second worst cyclical bear market in at least 80 years. Obviously, gold mining stocks have been crushed. Then they became cheaper, then cheaper and then really cheap. Yet, we may not realize just how cheap this sector has become both in nominal and relative terms.

Below we plot the Barron’s Gold Mining Index (BGMI) against Gold. The BGMI dates back to 1938. The ratio recently touched its lowest level in at least 77 years! There might not be anyone alive today who has seen gold stocks this cheap relative to Gold.

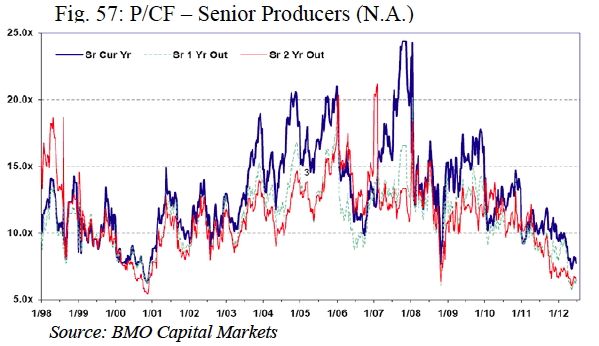

The next chart plots the price to cash flow valuation for senior gold miners. Twice in the past two years it touched a low of about 5. According to data from BMO, this is even lower than during the secular bottom of 2000 when senior miners traded at 6x-7x cash flow.

Gold stocks are also historically cheap relative to book value. A year or so ago I posted a chart from Datastream, a product of Thomson Reuters that showed gold stocks trading at their lowest book value since at least 1980. You can view that here. Here is another chart which shows the price to book ratio for the 10 largest miners. It is unsourced but shows price to book value at the lowest levels since at least 1993.

These spectacularly low valuations have resulted from arguably the second worst bear market ever. The updated bear analog chart is below.

{kind=link}

{kind=link}

{kind=link}

Could gold mining stocks get even cheaper in the weeks or months ahead? It is certainly possible, but only in the scenario of Gold trading to new lows. Even in that scenario, there is no guarantee that the various gold miner indices will make new lows.

While we lack data that precedes 1980, my guess is gold mining stocks relative to cash flow and book value are trading at valuations not seen since 1960 (a secular bottom) or even earlier. In the year 2000 the gold stocks were at the end of their worst cyclical bear market in history (and worst secular bear) and were trading at a 24-year low! Valuations recently surpassed (to the downside) where they were at that epic low.

In any event, the gold mining sector is primed for what should be a spectacular recovery. A big rise in margins/earnings and valuations is the one two punch that causes markets to rally substantially following a major bottom. Margins are starting to recover as evidenced by Newmont Mining’s earnings report. Miners have worked to cut costs and are now getting a boost from lower energy prices and weak local currencies. The only thing left is for metals prices to turnaround. Consider learning more about our premium service including our current favorite junior miners which we expect to outperform in the second half of 2015.

Jordan Roy-Byrne, CMT

Over the next few years as debt, currencies and countries start to fall apart individuals will be looking to place their money where it will hold its value and buying power during times of extreme uncertainty.

If you eliminate fiat currencies which are created out of this air and are nothing more than a credit we are left with precious metals and stones. As much as we have evolved over time, we could be valuing things like gold, silver, platinum, and precious stones more so than our currency.

Let’s face it, currencies are swinging in value 20-50% regularly and while most people do not realize it their buying power often is not as strong as it was. Would you rather hold a large portion of your capital in say the EURO which is falling like a rock in value costing you thousands of dollars a month, or would gold and silver which rises in value as your currency falls be a smarter decision?

Do not get me wrong, I am not trying to be a doom and gloom analyst. And I hope to be wrong, but with so many things pointing to an extreme global change it only makes sense to add some protection in the event something drastic does happen.

With the average fiat reserve currency since 1400 lasting between 80-105 years. With the dollar becoming the reserve currency in 1920 the odds point to the dollar being dropped within 3-5 years.

Gold Price Chart & Long Term Bullish Patterns

Review Of the 1970-80’s Gold & Bubble

The chart below shows the price of gold, silver, the typical price bubble, and phased of the market which happens in all asset types at some point in their life cycle.

The red line shows the average market participants emotional state. Yellow line is the price of gold, and the grey line in silver.

Current Gold & Silver Bubble – Priceless

Priceless Gold Conclusion:

What does all this mean? It means money is going to move out of dying currencies and into physical assets like gold, and silver.

There are three different forecasting models for gold I have created. Depending how things play out in the next couple years the low target is $5,000 oz, and highest is $12,000 oz.

Starting to accumulate physical gold and silver as a long term investment and as insurance for your portfolio is critical. Small denominations are best because when prices sky rocket it will be tough to sell/trade a $12,000 oz gold bar compared to a gram of gold that will be worth $450, or better yet an ounce of silver worth $150.

With that said my key focus is on trading for income and growth through the use of exchange traded funds. And if precious metals are about to start another bull market there will be big gains in gold stocks which I will be trading.

Chris Vermeulen

My new book explains how to protect your capital in detail.

Learn to trade, and get my trades live: www.TheGoldAndOilGuy.com

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

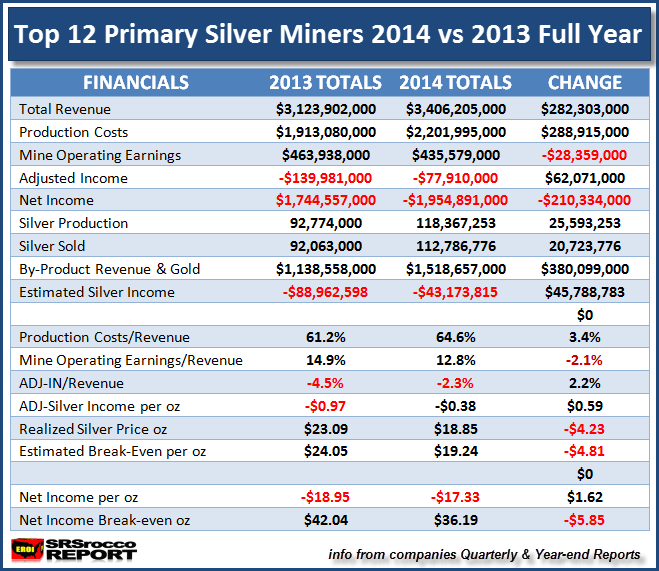

With the last remaining company finally releasing their year-end results, my top primary silver miners lost a combined $1.9 billion in net income in 2014. Two-thirds of the group reported significant write-downs (impairments), while the two of the largest companies suffered the highest losses.

Even though the group experienced record net losses, seven of the twelve actually enjoyed positive adjusted income. Let me explain. Companies report net income and adjusted income. Net income includes various items such as impairments, losses (or gains) on derivatives, hedges, investments or financial exchange losses (gains), and etc.

While these financial items are apart of their profit and loss statement, I like to focus on their adjusted income which removes these items in order to get a better idea of how successful they are at MINING SILVER. As I mentioned before, two of the largest silver producers in the group suffered huge net income losses due to large impairments, but their adjusted income wasn’t as bad.

For example, Coeur stated the largest net income loss of the group at $1.15 billion while Pan American Silver came in second at $545 million in the red. However, the adjusted income for Coeur was -$112 million compared to Pan American Silver at -$20.8 million. Coeur’s large adjusted loss for the year, awarded them with the third highest estimated break-even of the group at $22.38. Which means, Coeur lost an estimated $3.51 for each ounce of silver they sold at an average price of $18.87 in 2014.

Here is the combined financial data for the top 12 primary silver miners in my group:

As we can see from the table above, the group sold nearly 21 million oz (Moz) more silver in 2014 than 2013, but their total revenue only increased $282 million from $3.1 billion to $3.4 billion. Basically, the group sold 23% more silver in 2014 and was awarded with a paltry 8% increase in total revenue.

The major reason the group’s total silver production and sales increased so much in 2014 was due to Tahoe Resources Escobal mine reaching full year commercial status. Tahoe’s Escobal mine produced over 20 Moz of silver in 2014, but only sold 18.1 Moz. Tahoe is the lowest cost producer of the group even though Hecla likes to brag it has one of the lowest cash costs. CASH COST accounting is not a GAAP (Generally Accepted Accounting Principle) and I believe is totally useless in determining the overall profitability of a mining company.

You will also notice the group’s total production costs increased $288 million, year over year. This was due to the addition of Tahoe Resources $127 million in production costs along with the group adding a few newly acquired primary gold mines as well as cost increases from higher silver production from the other members.

I would like to point out just how much by-product (and gold) revenue the group reported in 2014:

The total group’s by-product and gold metal sales in 2014 were $1.5 billion of the total $3.4 billion in revenue. Thus, the group’s by-product and gold metal sales accounted for 44% of total revenue. That’s a lot of copper, zinc, lead and gold.

CASH COST ACCOUNTING: Needs To Be Thrown Out The Window

I brought this subject up to prove to the precious metal investor that by-product sales are not CREDITS as the industry lists them on their balance sheet when they calculate their cash costs. To arrive at a CASH COST figure, the company deducts their by-product credits from the cost. What a silly and stupid waste of time.

Can you imagine the losses the individual companies and the group would have suffered if they did not include their by-product sales in their balance sheets? We must remember a CREDIT is a FREEBIE. When you go to the store and you have a CREDIT on your account, that’s a freebie. On the other hand, the mining companies need every bit of their by-product revenue to fortify their balance sheets.

Sure, some of the revenue comes from a few primary gold mines, but the majority is a by-product of mining silver. This isn’t a CREDIT, it’s a DAMN necessity… LOL.

If we were to deduct $1.3 billion of the supposed by-product credits from the total revenue, how would that impact their bottom line?? Instead of the group suffering a total adjusted loss of $77 million, it would be a whopping $1.37 billion (add $77 million to $1.3 billion). Now, I used $1.3 billion of by-product revenue instead of the full $1.5 billion shown above because I deducted a conservative $200 million of primary gold sales from their primary gold mines.

Again, for a company to actually list a CREDIT, it wouldn’t need that income or revenue to be profitable. Which means, if by-product metal sales were actually CREDITS, then the company would be profitable without them. As we can see, this is not the case.

I am quite surprised that Jeff Christian’s CPM Group still uses the worthless CASH COST metric in their annual Silver Yearbooks. CPM Group sort of bragged in their 2014 Silver Yearbook that the primary silver miners cash cost fell to $9.68 in 2013 compared to $10.01 in 2012.

Unfortunately, there still seems to be a good percentage of precious metals investors (new and old) who believe it costs $10 to produce silver. There isn’t one company in my group that has an estimated breakeven anywhere near $10. The lowest is Tahoe at $13.70 with most in the $17-22 range.

Here is the highlighted estimated breakeven for the group taken from the table above. In 2014, the top 12 primary silver miners lowered their estimated breakeven to $19.24 down from $24.05 in 2013. Even though group was able to lower costs which in turn lowered their estimated breakeven ($4.81 an oz) compared to 2013, the average realized price they received for silver ($4.23 an oz) declined significantly as well.

According to my formula, the group suffered a net loss of $0.39 for every ounce of silver they sold in 2014. How high would the group’s losses be if we didn’t include their by-product metal sales? Let’s be really conservative and subtract $1 billion of by-product metal sales and see how that would impact the loss per ounce:

$1 billion divided by 112.7 Moz of silver sold = -$8.87 an ounce

Without adding the supposed BY-PRODUCT CREDITS of a conservative $1 billion, the group would have lost another $8.87 on each ounce of silver sold. Thus, the breakeven for the group would have jumped to ($19.24 + $8.87) $28.11. If the primary silver mining industry received $18+ an ounce for the silver they produced in 2014, without their by-product revenue, they would be in REAL TROUBLE.

This is exactly how CPM Group gets away with publishing a primary silver mining industry $10 cash cost. By the industry deducting all of its by-product metal sales (credits), it can show a very low CASH COST which has nothing to do with profitability. So why does the industry continue to publish this worthless metric? That’s a good question.

How Much Lower Can The Group’s Breakeven Go?

I would imagine we will continue to see a drop in the group’s breakeven over the next several quarters. Because the price of oil is now half of what it was in 2014, this should finally make its way through the cost structure in the primary silver mining industry. However, I don’t see that much of an overall decline in the group’s breakeven for producing silver.

If the estimated breakeven for the group was $19.24 in 2014, I don’t see it falling too much below $18 this year. I believe the primary silver mining companies have done as much as they can to cut costs and there really isn’t a lot of wiggle room left.

Furthermore, even if the group’s break even was to fall to say $17.50, the average price of silver is now trading at $15.90. Thus, the primary silver miners as a group would still be losing money. This is quite a shame because these mining companies are the few entities in the world actually producing WEALTH or a STORE OF WEALTH, while the Commercial and Central Banks continue to rob, steal and loot wealth from the public.

PRIMARY SILVER MINERS: Few Bright Spots In The Future

Some readers may interpret my breakeven analysis on the primary silver miners as being bearish or critical. While I like to point out the facts as I see them, I believe the primary silver mining industry will be one of the FEW BRIGHT SPOTS in the future. This will be due to the negative ramifications of the peak and decline of global unconventional oil production on most paper and physical assets. As investors flee increasingly worthless paper assets in the future and into the primary silver miners, their share prices will explode higher.

I will be publishing PAID REPORTS on various aspects of the silver industry and market. One will focus on the top 12 primary silver miners in my group analyzing which companies are the best candidates to consider owning when we finally get the MAD RUSH IN GOLD & SILVER.

Please check back for new articles and updates at the SRSrocco Report. You can also follow us at Twitter

Gold & Silver Trading Alert originally sent to subscribers on April 20, 2015, 7:59 AM

Briefly: In our opinion, a speculative short position (half) in gold, silver and mining stocks is justified from the risk/reward point of view.

The situation in the precious metals market is quite specific at this time. We have gold moving higher on low volume and moving lower on increased volume (which is bearish), but during the last few weeks miners have outperformed gold which seems to indicate strength. One of the signals that help to decide what the outlook really is comes from silver stocks.

Before we move to silver miners, let’s take a look at gold and silver (charts courtesy of http://stockcharts.com).

As mentioned above, the price of gold moved back and forth and the corresponding action in volume was

bearish. Volume very often confirms the direction in which the market is going and it allows to differentiate between true rallies (that are likely to be followed by even bigger rallies) and corrections (that are likely to be followed by declines). In this case, we saw the latter type of action.

Gold is after a confirmed breakdown below the rising support line and after reaching the 50% retracement based on the February – March decline, so it’s been likely to decline and the price-volume action makes this even more likely.

Silver’s bearish outlook also remains unchanged as the price didn’t do much on Friday. Silver tried to move above the previously broken black support/resistance line, but was only able to move to it on an intra-day basis and decline shortly thereafter.

Yesterday’s price action in mining stocks (the GDX ETF includes both gold stocks and silver stocks) might seem surprising to those who believed that miners would soar right after the breakout as miners refused to rally even despite the gold’s rally on Friday. That’s a bearish sign.

Have we just seen another top? Based on the Nov. 2014 highs being reached – yes. However, we wouldn’t rule out a move to the $21 level as such a move would make the head-and-shoulders patternmore symmetrical. Please note that we don’t have to see this type of move for the pattern to have bearish implications – the pattern doesn’t have to be perfectly symmetrical and a top (right shoulder of the pattern) at exactly the previous top (left shoulder of the pattern) would very much make it meaningful anyway.

Our previous comments about the head-and-shoulders pattern’s implications for mining stocks remain up-to-date:

The red resistance lines that you can see on the chart are based on the possible head-and-shoulders pattern. If we see a move to the Nov. high or even to the $21 level but without a visible breakout above them and then see a decline, the implications will be very bearish. If we don’t see such upswings and miners decline before these levels are reached (which seems likely), then the implications will be very bearish anyway, because the head-and-shoulders pattern will continue to be formed. If it is completed, the decline following the breakdown below $17 could take the GDX ETF below $13.

What about the silver stocks?

Silver stocks formed bearish head-and-shoulders patterns a few times previously. In each case, these patterns resulted in much lower values of silver stocks and the rest of the precious metals sector. What’s particularly interesting about these patterns is that the right shoulder was quite often (2 out of 3 cases) smaller than the left one. Consequently, a move higher here is not required for the right shoulder of the current head-and-shoulders to form. In fact, it’s top could be already behind us.

All in all, the thing that silver stocks tell us is that we can really see a move lower right away, without another small upswing (hence, exiting the small short positions at this time seems premature).

Furthermore, let’s not forget that the silver to gold ratio has recently moved sharply higher, causing the RSI Indicator based on it to become overbought. In EACH case that we saw this development a major decline followed (at times we had to wait for it a few weeks, but it ultimately happened without a bigger rally before it). We have not seen a major decline so far, so the bearish implications remain in place.

The gold to oil ratio closed the week well below its 2011 high, and – because of the size of the move and the weekly close – we consider the breakdown to be confirmed. The implications are bearish and our previous comments remain up-to-date:

We think that there’s nobody in the precious metals market that needs to be convinced that the 2011 top was a major event. However, it was not only major in gold itself, but also in the case of its ratios, including the gold to oil ratio.

This ratio peaked in 2011 as well and it was not until this year that it was broken. The initial move lower in the ratio earlier this year and a rebound from the 2011 high proved that this is indeed a major support/resistance level. This important level was just broken yesterday in a very profound way.

The gold to oil ratio moves in tune with gold, so such a major breakdown in this ratio has bearish implications for gold as well.

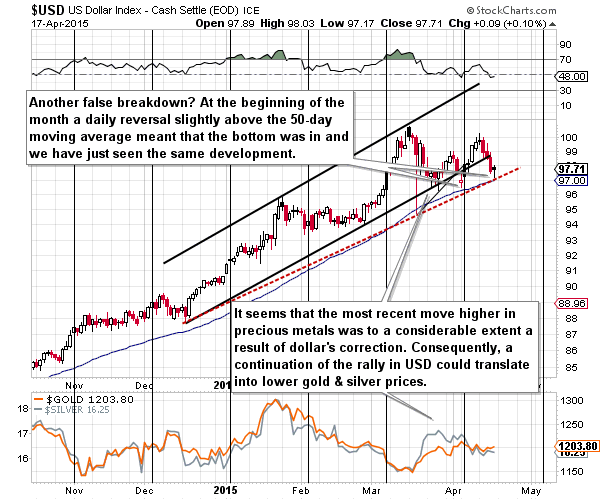

The USD Index declined on Friday, but only initially – it came back up in the following part of the session. Will the USD decline based on the breakdown below the rising trend channel? It’s possible, but it’s not very likely. Please note that this line was invalidated a few times in the past and in each previous case the USD rallied back above it.

Moreover, the 50-day moving average provides support (just like it was the case in mid-March and early April) and so does the red dashed support line based on the December and March lows. Consequently, the outlook did not deteriorate significantly – we can still see much higher USD values in the coming days and weeks.

Summing up, even though it seems that the situation in the precious metals market is improving based on last week’s strength in mining stocks, we think that this is not the case – in fact, the opposite might be taking place. The strength in miners was no longer present on Friday and practically no other market or ratio (i.a. gold, silver, silver to gold ratio, gold to oil ratio, silver stocks, USD Index) is confirming it. While we could see some more strength in miners, it’s not likely to be significant and – more importantly – we don’t have to see more strength for the bearish head-and-shoulders pattern to be completed. The right shoulder has already been formed (it’s after the right shoulder’s highest point) in the case of gold and silver and it seems that it’s about to be formed in the case of mining stocks. The implications are very bearish and it seems that exiting small short positions in the precious metals sector at this time would be premature. If we see an invalidation thereof, we’ll close the positions, but it seems more likely that we will see a bearish confirmation, which will likely result in increasing the size of the short position.

We will keep you – our subscribers – updated.

To summarize:

Trading capital (our opinion): Short (half position) position in gold, silver and mining stocks is justified from the risk/reward perspective with the following stop-loss orders and initial (!) target prices:

- Gold: initial target price: $1,115; stop-loss: $1,253, initial target price for the DGLD ETN: $87.00; stop loss for the DGLD ETN $63.78

- Silver: initial target price: $15.10; stop-loss: $17.63, initial target price for the DSLV ETN: $67.81; stop loss for DSLV ETN $44.97

- Mining stocks (price levels for the GDX ETN): initial target price: $16.63; stop-loss: $21.83, initial target price for the DUST ETN: $23.59; stop loss for the DUST ETN $12.23

In case one wants to bet on lower junior mining stocks’ prices, here are the stop-loss details and initial target prices:

- GDXJ: initial target price: $21.17; stop-loss: $27.31

- JDST: initial target price: $14.35; stop-loss: $6.18

Long-term capital (our opinion): No positions

Insurance capital (our opinion): Full position

Please note that a full position doesn’t mean using all of the capital for a given trade. You will find details on our thoughts on gold portfolio structuring in the Key Insights section on our website.

As a reminder – “initial target price” means exactly that – an “initial” one, it’s not a price level at which we suggest closing positions. If this becomes the case (like it did in the previous trade) we will refer to these levels as levels of exit orders (exactly as we’ve done previously). Stop-loss levels, however, are naturally not “initial”, but something that, in our opinion, might be entered as an order.

Since it is impossible to synchronize target prices and stop-loss levels for all the ETFs and ETNs with the main markets that we provide these levels for (gold, silver and mining stocks – the GDX ETF), the stop-loss levels and target prices for other ETNs and ETF (among other: UGLD, DGLD, USLV, DSLV, NUGT, DUST, JNUG, JDST) are provided as supplementary, and not as “final”. This means that if a stop-loss or a target level is reached for any of the “additional instruments” (DGLD for instance), but not for the “main instrument” (gold in this case), we will view positions in both gold and DGLD as still open and the stop-loss for DGLD would have to be moved lower. On the other hand, if gold moves to a stop-loss level but DGLD doesn’t, then we will view both positions (in gold and DGLD) as closed. In other words, since it’s not possible to be 100% certain that each related instrument moves to a given level when the underlying instrument does, we can’t provide levels that would be binding. The levels that we do provide are our best estimate of the levels that will correspond to the levels in the underlying assets, but it will be the underlying assets that one will need to focus on regarding the sings pointing to closing a given position or keeping it open. We might adjust the levels in the “additional instruments” without adjusting the levels in the “main instruments”, which will simply mean that we have improved our estimation of these levels, not that we changed our outlook on the markets. We are already working on a tool that would update these levels on a daily basis for the most popular ETFs, ETNs and individual mining stocks.

Our preferred ways to invest in and to trade gold along with the reasoning can be found in the how to buy gold section. Additionally, our preferred ETFs and ETNs can be found in our Gold & Silver ETF Ranking.

As always, we’ll keep you – our subscribers – updated should our views on the market change. We will continue to send out Gold & Silver Trading Alerts on each trading day and we will send additional Alerts whenever appropriate.

The trading position presented above is the netted version of positions based on subjective signals (opinion) from your Editor, and the Tools and Indicators.

As a reminder, Gold & Silver Trading Alerts are posted before or on each trading day (we usually post them before the opening bell, but we don’t promise doing that each day). If there’s anything urgent, we will send you an additional small alert before posting the main one.

=====

Latest Free Trading Alerts:

Bitcoin Trading Alert: Bitcoin in Deadlock

Bitcoin went up both yesterday and on the day before. This could have looked like the end of the decline but we were rather cautious about that yesterday. Has anything changed since then?

=====

Hand-picked precious-metals-related links:

Gold below $1,200 on steadier dollar; eyes on Greece, China

=====

In other news:

US, Ukraine Start Military Training, Defying Russian Fury

Greece Flashes Warning Signals About Its Debt

=====

Thank you.

Sincerely,

Przemyslaw Radomski, CFA

Founder, Editor-in-chief

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair