Gold & Precious Metals

THE GOLD STANDARD: Although it may be unrealistically optimistic, I believe my paraphrase of a Churchill quote:

“Central Bankers will eventually do the right thing and return to a gold standard after they have exhausted all other alternatives.”

While central bankers are exhausting all other alternatives, I worry about the collateral damage to 90% of the population who are not first in line on the fiat money gravy train that benefits the financial and political elite.

Clearly, central bankers will return to a gold standard only if forced by a financial implosion, economic collapse or equivalent disaster. Hence, the powers-that-be will do whatever is necessary to conceal the sovereign debt bubble, hide the insolvency of sovereign governments, and extend and pretend regarding the value of bonds, equities, and fiat paper currencies.

THE GOOD: Gold is and has been real money for 5,000 years.

THE BAD: Gold prices will benefit from the following items. (This is a long and incomplete list.)

- Greek bankruptcy and their inevitable exit from the Euro zone: Such an exit will confirm bad debts, weaken or destroy the banks that made the loans, and damage confidence in fiat currencies, ever-increasing debt, and sovereign debt collateral.

- Euro, Yen, Dollar collapse: Can a major world currency collapse in value without damaging confidence in all other fiat currencies? People will have more confidence in gold and will lose confidence in fiat currencies.

- Baltic Dry Index has hit new all-time lows. Global economic activity is weakening. Will central banks do nothing as the world economy weakens or will they continue the global QE to infinity to stimulate the global economy? Of course central banks will print currencies.

- Price of oil has collapsed. The same arguments apply as with the Baltic Dry Index.

- Central bank creation of currencies: QE to infinity! Maybe it will prolong the current system or perhaps a deflationary collapse will occur regardless. Would you rather own gold, or sovereign bonds backed by insolvent governments that can repay their debts only because central banks create new currency and monetize their debt?

- Cooked statistics: Who still believes the GDP, unemployment, retail sales or real estate sales numbers in the US?

- Ukraine conflict: Expect this growing conflict to damage European stability, increase military budgets, and substantially increase debt and financial risk.

- Syria and the Middle East: Expect more military spending, debt, bond monetization, and currency in circulation.

- “No boots on the ground,” except in the Middle East, Asia, Africa, Europe, and South America. However, I know of no plan to invade Antarctica. Swell! And you can trust that the economies of Europe and the US are humming along nicely, employment is robust, the people are happy, banks are solvent, politicians are truthful, and this is the best of all possible worlds.

THE TRULY UGLY:

- COMEX default or shutdown: What if the COMEX can’t deliver gold or silver and is forced to cash settle futures contracts. It could happen, perhaps soon since a huge quantity of gold has been shipped from western vaults to Asia. Paper gold is not real gold and that realization will be devastating to global confidence if the COMEX defaults on gold or silver delivery.

- LBMA shutdown: Same as a COMEX shutdown. See above.

- Global reset and financial collapse: We don’t want to think about the ramifications, the inevitable blame-game, false flag diversions, escalating wars and human suffering that will result from an economic collapse.

- Global credit collapse: Most economic transactions are based on credit. A global credit collapse probably would collapse global financial and economic systems, including the delivery of food and fuel. See above. Again, the consequences will be truly ugly.

President Nixon separated gold from the dollar (temporarily) on August 15, 1971. Currency in circulation and debt have subsequently increased exponentially. The purchasing power of fiat currencies has similarly decreased. The exponential price increase is gold mirrors the devaluation of the dollar. See the graph below. I discuss this in my book, “Gold Value and Gold Prices From 1971 – 2021.”

CONCLUSIONS:

- The global financial system is vulnerable and dangerously fragile. If it were safe and healthy, why would Europe continue to “throw good money after bad” with more bailouts to Greece and other countries? Ask yourself if Italy, Spain, Japan and the US are materially different.

- A vulnerable and dangerous financial system that is increasingly leveraged is a bubble in search of a pin. Accidents happen! Protect yourself and insure your assets with gold and silver.

- The Baltic Dry Index and the price of crude oil are telling us that global demand and economic strength are faltering. Expect more central bank intervention, bond monetization, and “money printing.” If sovereign debt is a dangerous bubble now, what will it be after another year or two of massive printing and stimulus?

- Various wars and boots on the ground: Wars are inflationary. More war creates more debt, more “money printing” and higher prices for commodities and the cost of living. The S&P, sovereign debt prices, and politician approval ratings probably will not benefit from more wars, a higher cost of living, and declining living standards. Protect yourself. Gold prices will rise.

- Gold has been real money for 5,000 years. Dollars, Euros, Yen, and other unbacked fiat currencies have been printed to excess for decades. Bet on gold prices rising.

Gary Christenson

The Deviant Investor

Precious Metals have had an interesting week. Both Silver and the gold stocks rebounded off their 50-day moving averages only to do a 180 the following day. Meanwhile Gold has given back most of its January gains. In this missive we consider the near term outlook for Gold and the gold stocks.

In the chart below we plot Gold and Gold priced in foreign currencies (Gold/FC) which is essentially the inverse of the US$ index. Gold put in a strong rebound, rallying over $150/oz from November through January. That was also its strongest rally in real terms in several years. As we can see, Gold/FC drove that rally as its driving the current decline (to some degree). Gold/FC has a bit more downside to go to reach support. The fact that Gold could not hold above $1240 tells us that Gold will need more time before it can retest trendline resistance. However, Gold’s strength against foreign currencies is a major character change that wasn’t in place during 2013-2014.

Gold & Gold priced in Foreign Currencies

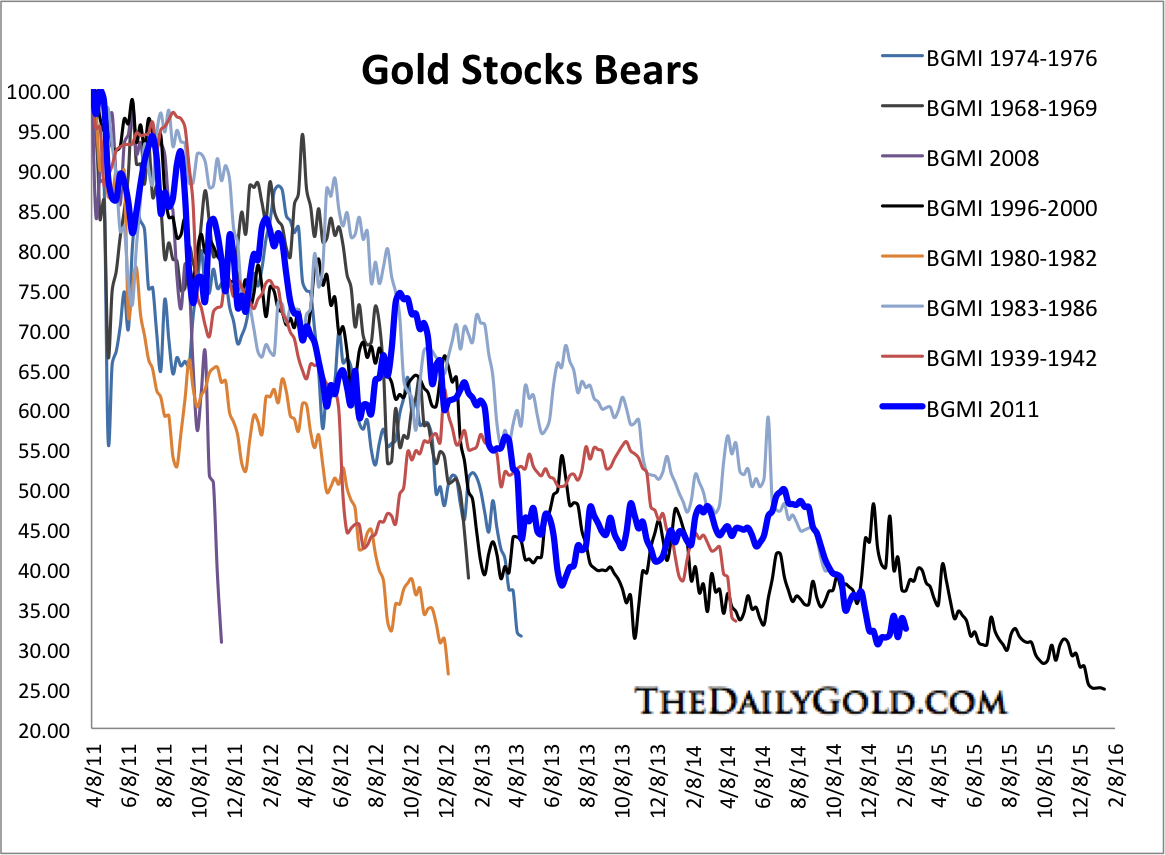

Turning to the stocks, let’s start with the bears analog chart. We use weekly data from the Barron’s Gold Mining Index which dates back to 1938. Back in December we noted that gold stocks were likely at their second most oversold point in history. The most oversold point was the months and weeks prior to the bottom in 2000. Markets can do anything in the short term but this chart makes a strong case that miners are extremely ripe for a new bull market.

Gold Stocks Bear Markets

Next is a chart of GDX and our Top 40 Index. Both formed a strong double bottom at the end of 2014 and both will need to surpass their 400-day moving averages to be in a new bull market. The miners formed the recent low amid an extreme oversold condition. After a strong rebound, resistance has come into play. The range between strong support and strong resistance is getting smaller.

GDX & Top 40 Index

The trend for precious metals can be considered neutral or range-bound with a current bearish bias. After strong rebounds, Gold and gold shares are backing off from resistance. They aren’t yet ready to make major breakouts to lift them into bull markets. This is bearish but there have been key bullish developments in recent months which should caution bears. Both Gold and gold shares performed well amid a very strong US$ which signals a major change. Gold companies are benefitting from the collapse in energy prices and weak currencies within the jurisdictions they operate.

Because gold companies can benefit from lower energy costs and weaker foreign currencies, it’s quite possible that they could be the first, ahead of Gold to break into new bull market territory. Market heavyweights such as Jeff Gundlach and Jim Rogers may sense that as they recently became investors in the miners. A new bull market lies ahead sooner rather than later but investors and traders need to maintain their discipline and patience.

Good Luck!

Jordan Roy-Byrne, CMT

A lot of investors want to know why I am not screaming from the rooftops, “Buy Gold!”

The reason is simple: Gold has not bottomed yet, not by a long shot.

So why am I so confident gold has not bottomed (ditto for silver), especially when all is not well with the world?

After all, in addition to the Ukraine crisis, which is not over, tensions are rising dramatically all over the world.

My answer is simple: It’s not yet time for gold and silver to take off to the upside. Quite the contrary, they have more work to do on the downside.

Look, every market has its time and place in the sun. And every market has its false rallies. That’s why timing is so critically important.

The pause in gold and silver’s long-term

bull markets is not yet over

In contrast to important tops in any market, important bottoms take time to complete. That’s especially true with the precious metals.

Gold and silver have more backing and filling to do. They have lots of investors they still need to chew up and spit out. Especially the most recent buyers and pundits urging investors to buy.

In fact, gold and silver will not bottom until most investors have turned outright bearish on them.

In fact, gold and silver will not bottom until most investors have turned outright bearish on them.

That’s one of the reasons why gold and silver took a nice nose-dive last week. It cast out recent buyers. And though there may be one or two more bounces higher — sucking in even more naïve analysts and investors …

Gold is destined to fall below $1,000 … and silver to near $12.50 in the months ahead.

Mining shares, even penny miners, will be sliced in half again.

Keep in mind that for a market to bottom, it must hit long-term support levels at the right time. When price and time converge together, then you have an important bottom.

We have none of that yet, in gold, silver, any precious metal, or the mining sector. And though yes, one or two more bounces higher can easily form, the most important thing for you to know right now is that a new sell signal is rapidly approaching.

You can see it here on this chart that I have for you.

A chart based on a composite of all the reliable cycles affecting gold’s trading. Over two billion computations of those cycles and what they say for the future of gold.

As you can clearly see, though one or two more small rallies remain possible, this model is showing a very strong timing sell signal for Feb. 26, just eight days from now.

And take a look at the decline it’s forecasting. It’s quite a whopper. A potential waterfall decline that would last into late May, where gold would have a chance to finally bottom, around the week of May 21.

Then there would be a bounce, and a sort of double-bottom formation heading into late June, before gold’s new bull market actually materializes.

The long-term bull market would then take back over.

But the bottom line is this: The bear market in the precious metals is not yet over, and anyone telling you that it is, either has a hidden agenda, or simply can’t see the writing on the wall (or both).

Ditto for mining shares, no matter how big or small they may be, no matter how cheap they may seem.

So what will drive gold into its final bottom?

It’s simple and it boils down to two chief reasons:

1. As I mentioned above, there are too many premature bulls in the market. They’re still trying to buy and get everyone else to buy, and that in itself is a sign gold has not bottomed.

Gold will bottom when the investors and analysts screaming “buy now” are bloodied.

2. Deflation is reigning supreme now. It’s almost everywhere. Blanketing Europe. Even some sectors in China and Asia. Even here in the U.S. And in virtually all commodity markets.

All this, despite the most massive money printing in the history of civilization!

So much for all that hyperinflation talk!

Best wishes,

Larry

– See more at: http://www.swingtradingdaily.com/2015/02/18/no-way-has-gold-bottomed/#sthash.ggRYF84u.dpuf

The TSX-Venture has begun exhibiting some constructive signs during the past couple of months after a brutal 70%+ decline from the 2011 peak….

….continue reading HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair