Gold & Precious Metals

Everyone knows that gold (COMEX:GCZ13) and silver (COMEX:SIZ13) have value, but few people understand their real value. Some people say that the current price of gold and silver is too high after rising 12 years. Is that true? If we know the real value of gold and silver, we will have a clear answer to the question. In this article, I will decode the three main components of the value of gold and silver: Monetary value, commercial value and cultural value. Then we will know if it is worth to buy gold and silver at the current price and what to buy. This article is for all people no matter whether you own gold and silver or not.

Everyone knows that gold (COMEX:GCZ13) and silver (COMEX:SIZ13) have value, but few people understand their real value. Some people say that the current price of gold and silver is too high after rising 12 years. Is that true? If we know the real value of gold and silver, we will have a clear answer to the question. In this article, I will decode the three main components of the value of gold and silver: Monetary value, commercial value and cultural value. Then we will know if it is worth to buy gold and silver at the current price and what to buy. This article is for all people no matter whether you own gold and silver or not.

1. Gold and silver have monetary value

The principle to estimate the monetary value of gold and silver is based on the fact that gold and silver are money. Many people account paper currency as money. That is wrong. Paper currency is just a kind of fiat currency. “The average life expectancy for a fiat currency is twenty-seven years” (Chris Mack, president of Trade Placer). Gold and silver are real money and have been used as money for 5,000 years by all countries. You can easily learn the difference between money and currency on the internet. I don’t need to reiterate here. Just remember that a currency loses its purchasing power as the currency issuer, the central bank, prints more currency. But money (such as gold and silver) will never lose its purchasing power though it may fluctuate during some short periods. No one can print one ounce of gold or silver.

The method to estimate gold’s monetary value in a specific currency is that the money supply should be backed by the total gold reserve in that country. There is money supply data such as monetary base, M1, M2, M3 and gold reserve data such as central bank gold reserve, private gold reserve, tradable gold, aboveground gold and underground gold. Different money supply data should be paired to different gold reserve data (monetary base and central bank gold reserves are a pair, aboveground gold and M2 are another pair). The results derived by different pairs should be coincident or approximately the same value. I will use the monetary base and the gold reserve by the Fed as an example to estimate gold’s monetary value in USD. We know that the Fed reserves 261 million ounces of gold (World Gold Council) and the current monetary base is $3,398,930 millions in August, 2013 (FED). Therefore, the gold’s monetary value is $13,022 / ounce (3,398,930 / 261). There are some countries such as China and Canada who don’t have enough gold reserve at present to back their currencies. For those countries, we use the global total monetary base and total gold reserve by all central banks to estimate gold’s monetary value as a reference. Fortunately, the result is almost the same as the value we got in the USA. It is about 80,000 yuan / ounce in RMB or $13,000 / ounce in CAD.

Regarding silver’s monetary value, the result is terribly high, which few people can accept it today if we use the silver reserve to divide the monetary base. The reason why silver’s monetary value is higher than gold’s monetary value is that silver is rarer than gold for almost all kinds of reserve data. According to Silver Institute and CPM Group, current government stocks of silver are close to zero compared to 350 million ounces in 1970, more than 95% of silver dug by human beings has been consumed by industry. However, we can estimate silver’s monetary value with an alternative method by dividing gold’s monetary value by gold silver price ratio (GSPR). In another paper, The Beginning of the Silver Age, I discussed GSPR and suggest that it will reach the area between 9 and 16 in about five to ten years and will continue to go down in the long term. Let’s use the medium number of 12.5 as a possible GSPR, we can get the current monetary value of silver as $1,041 / ounce in USD and as 6,400 yuan / ounce in RMB.

2. Gold and silver have commercial and cultural value

The cultural value of gold and silver is really difficult to estimate because people with different cultures have different value standards. In addition, some items have added value beyond the materials. For example, a gold dish or chair used by a king or a hierarch, an amulet given by a relative, ancient silver coins and so on, all of them have added value and the value is hard to estimate. The commercial value of gold and silver is mainly decided by their supply and demand. It’s also hard to estimate the exact value. To make it easy, I will use statistical methods with historical data spanning 70 years to estimate the gold’s commercial and cultural value (GCCV) together in terms of monetary value.

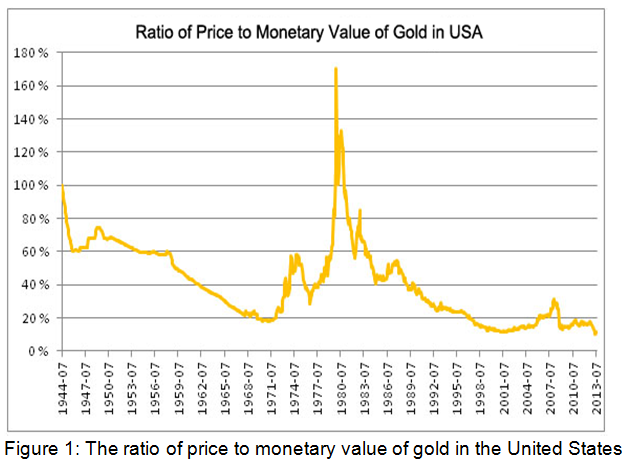

Using the historic data of monetary base and gold reserve in the United States, we can calculate gold’s monetary value in USD during the last 70 years after Bretton Wood System (July, 1944). Then we divide gold price by monetary value to get a chart of the ratio of price to monetary value of gold (RPMV-Gold) in the United States over the last 70 years as in Figure 1.

From figure 1, we can see that RPMV-Gold reached 170% in 1980. Most people in North America and west Europe then expected gold would be money again soon. The 70% more above its monetary value was the maximum RPMV-Gold. We also see that RPMV-Gold reached the bottom around 10% three times in 1999, 2008 and 2013. Few people in the world these days think that gold will be money again thanks to the government education all over the world. Now we have a range of GCCV from 10% to 70% of gold’s monetary value. With the same principle, we can figure out the range of silver’s commercial and cultural value (SCCV), it was between 2% and 60% of silver’s monetary value during the last 70 years. The ratio of price to monetary value of silver (RPMV-Silver) will be much higher than 60% in the future because of the coming silver shortage.

3. The value of gold and silver and the future price trend

Now that we have the monetary value and the statistical range of commercial and cultural value of gold and silver, we can figure out the current value of gold and silver. For gold, it is between $13,022 / ounce and $22,137 / ounce (monetary value plus maximum GCCV). For silver, we use the GSPR of 12.5 and current value of gold to estimate the value, it’s between $1,041 / ounce and $1,770 / ounce. All these values are just for reference and must be adjusted dynamically according to the money supply and gold reserve data.

The future price trend of gold and silver will be a movement from the current price to their actual value. Comparing the current price and the value of gold and silver, we know that the future price trend of gold and silver will definitely go up. Therefore, we should purchase gold and silver at the current price. The current RPMV-Gold around 10% is the third opportunity that the market gave us in 70 years and generally we cannot expect to get the opportunity more than three times. The door may close quickly very soon.

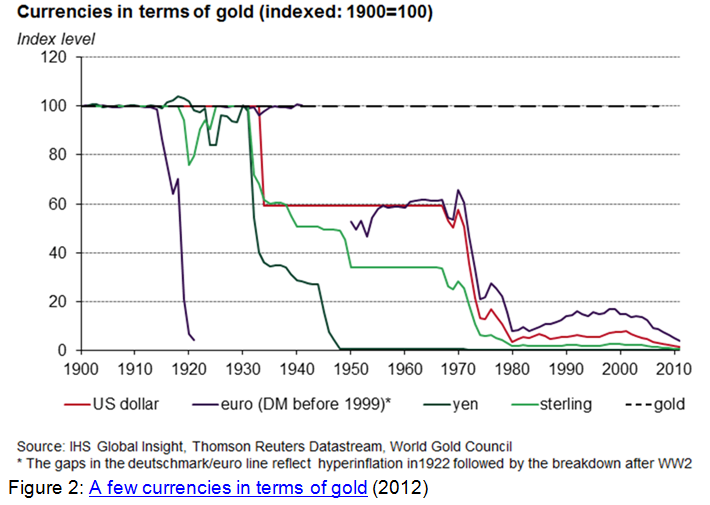

Some may argue that gold and silver will not be money again and their prices will never match their values. The problem with those opinions is that those people forget how long gold and silver have been used as money and how long the average life cycle of the fiat currency is. History told us unlimited times: Any fiat currency will eventually become useless paper. No fiat currency has lasted forever. Figure 2 shows the value changes of a few currencies in terms of gold from 1900 to 2012 (World Gold Council). We can see the value trend for all those currencies is going to zero. No matter whether or not gold and silver will be money again, one thing is for sure: All fiat currencies will eventually fail, but gold and silver will hold purchasing power forever. From this point of view, any price is a good price to buy gold and silver. However, you must be aware that if you purchase gold and silver at a price higher than their value, such as the price in January 1980, you may have a risk temporarily. But you will be the winner eventually if you own real gold or silver instead of the fiat currency. Some people measure stuff such as commodities, houses, stock indexes and workforce costs in gold and silver instead of paper currencies. That is an alternative method to value gold and silver.

4. Buy real gold and silver, not shadows

If we buy gold and silver at the current price $1,325 / ounce and $22.2 / ounce, we have an investment return of 9 folds for gold and 40+ folds for silver. It might not happen overnight except that the market will repeat January 30, 1934 again, it might last for a few years or decades until your current currency fails or a new gold standard system will be reassumed. The bottom line is that you should include gold and silver in your portfolio. History also tells us that silver usually moves in the same direction as gold. As long as gold price goes up, silver price will rise faster than gold price. If you believe that gold price will rise, you have no reason not to buy silver.

I recommend everyone buy some real gold or silver bullion such as bars, coins, U.S. Eagle, Canadian Maple, Chinese Panda, Australian Nugget, etc. Don’t buy the old coins or commemorative coins if the premium is too high because the high premium will lower your investment return. You can always choose the lower premium bullion to get a better investment return.

You can buy some other forms of gold and silver such as the ETF shares, a certificate by a bank or an organization, mining shares, futures contracts and options, but they are all shadows of gold and silver. Shadows are for trading, not for investment. It’s easy to understand that if you own shadows, you own nothing. There are some unexpected issues in owning shadows. First, some mining companies will finish digging out their underground gold and silver reserve someday; their shares may fall down sharply then. Second, banks may not have enough gold and silver in their vault at all. You might never get real gold and silver. There are rumors that many central banks sold out their gold reserve already or leased to commercial banks and have never bought it back again. I cannot imagine what will happen if that is true. Third, all ETFs are the same as bank certificates. Last, futures contracts and options are designed for arbitragers, speculators or traders, not for investors. If you are a serious investor and not a seasoned trader, you cannot use any leverage or loan to buy gold and silver. Otherwise, you may have trouble in a deep correction. Your own money is the only choice.

Conclusion

I often tell people to buy gold and silver bullion to protect their wealth with money history, inflation knowledge and the trend of paper currency. One month ago, a person challenged me with “The current gold price at $1,300/ounce is too high. I would buy gold at $35/ounce in 1971.” First, I told him: “It is worth to buy gold and silver if the price is under the value.” Then I spent 20 minutes expounding that the current price of gold was cheaper than the price at $35/ounce in 1971 if we compared the price with their monetary value (refer to figure 1).

There are a lot of catalysts for gold and silver prices to rise abruptly. They might be: The peak of global gold and silver production, world war, people get their real gold and silver from the banks or ETFs, short squeeze in the futures markets, some insolvent countries default, super inflation in some large countries, or the next time Chinese government publishes their gold reserve. Anything expected or unexpected can ignite an accelerating uptrend.

As a final reminder: The numbers I gave you in this paper are not the price targets. You must dynamically calculate the value and compare it with the price. If you unluckily purchased gold or silver at a relative high price, don’t complain, don’t worry, you will be determined about the uptrend of gold and silver after understanding their real value.

About the Author

With the S&P 500 (broad gage of U.S. stocks) up over 16% year-to-date and almost 31% since the beginning of 2012, it is fair to ask if broader North American markets should be considered overvalued. Anecdotally, it is certainly more difficult to identify striking value than it has been over the past several years – but not impossible as growth has picked up in select areas.

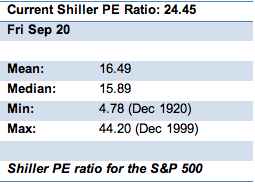

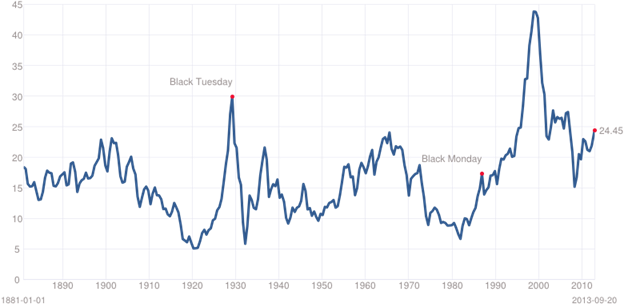

One such method which has proven successful in identifying market extremes (both over and undervalued) is the Shiller PE Ratio or cyclically adjusted price-to-earnings ratio, commonly known as CAPE. Developed by Yale economist Robert Shiller and built off the work of legendary value investors Benjamin Graham and David Dodd, CAPE is a valuation measure usually applied to broad equity markets. It is defined as price divided by the average of ten years of earnings, adjusted for inflation.

The central theme behind the CAPE is simple. Taking a multiple of one year’s earnings is misleading because stock markets naturally adjust when investors believe profits are cyclically high or cyclically low. Compare prices instead to the average of earnings over 10 years (Prof Shiller also corrects for inflation) and it becomes clearer whether stock markets are overvalued or undervalued.

For over a century, extremes in the CAPE have coincided with favourable times to buy and sell. By staying far above its long-term average during the rebound that followed the internet bust from 2003 to 2007, the CAPE also provided a warning that the rally was not to be trusted – ahead of the far worse crisis of 2007-09.

Prof Shiller and the CAPE (not the one some believe he wears) are sound the alarm once again, recently implying that the U.S. market is 62% overvalued and more expensive than any other big stock market.

Economics without debate is like politics without scandal. It’s not going to happen. It should be no surprise that the CAPE is under attack from another renowned economist, Jeremy Siegel, who contends that it is based on faulty data. Many on Wall Street discount CAPE, but most have a vested interest.

Prof Siegel of the University of Pennsylvania’s Wharton School has produced a new version of the CAPE, which he says corrects Prof Shiller’s mistakes. His version of the CAPE (again not the one his followers think he wears) suggests that the U.S. stock market is sending a different signal – stocks are cheap.

But there is plenty of reason to worry broadly about the economy including public (unfunded pension liabilities included) and private (consumer) debt. While U.S. consumer debt has been headed in the right direction, levels still remain historically high. U.S. unemployment is also a big concern.

Within Canada, our relative insulation from the great recession has unfortunately spared us a valuable lesson and consumer debt has not been paid down. In fact, Canadians are borrowing more, piling on consumer debt – credit cards, conventional bank loans, car loans and lines of credit. At some point this ends and a spending vacuum could limit growth.

Perhaps this partially justifies the S&P TSX Composite’s poor performance on a relative basis, being up a scant 3.3% and just 7.5% since the start of 2012. Slumping commodity prices (outside oil of late) are also a major contributor to the underperformance of the resource laden TSX.

So where does this epic tug-o-war leave us – which one of these statements is true?

“The stock market is overvalued.” “The stock market is undervalued.” Investors ask us these every day.

From our perspective, both statements are simplistic and most often irrelevant.

It is a market of stocks, not a stock market.

We do not recommend you buy “the market,” when you look to beat the market. Our clients create their Small-Cap Growth Stock Portfolios with discipline by purchasing 8-12 cash producing stocks over a 12-18 month period. Our holding periods are typically between 1-5 years and beyond.

Over that 1-5 year period, the broader market will have its ups when it is likely overvalued based on a number of metrics and downs when it may show as undervalued based on those same metrics. What is important to us and to you as a client is whether your 8-12 stocks are continuing to create shareholder value through a number of company specific metrics including cash flow increases, growth, a higher return of capital (dividends) and an improving balance sheet.

Outside of this, Mr. Market will create a great deal of “noise” on a day-to-day basis. Try not to pay too much attention – it will allow you to sleep far better each night.

|

KeyStone’s Latest Reports Section |

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair