Gold & Precious Metals

There’s a plausible path to $10,000 an ounce gold. And it doesn’t require a breakdown in civil society…

Speculators see central bankers as modern-day superheroes, able to push markets around with a single phrase. In the minds of most investors, Ben Bernanke, Mario Draghi and Masaaki Shirakawa might as well be wearing tights, masks and capes. These superhero central bankers continuously swoop down into the financial markets to defend them from downticks…and to insure that they always deliver capital gains.

The reality, of course, is that these superheroes are frauds. They have no superpowers…other than the power of mass delusion. The powers of Mario Draghi and the other central bankers in Europe are waning. Excess debt is like kryptonite: Each new wave of printing has less impact on markets. As the popular phrase goes: “This is a solvency problem, not a liquidity problem.”

In other words, new money supply cannot restore health to sick loans and government bonds. The only way to restore solvency to the system is to deflate the economy or slash the amount of debt in the system through mass bankruptcy.

Or is there another way? Is there a “reset button” that central bankers can push (with the approval of political leaders) that would restore balance to the system?

We know central bankers would never want to deflate the economy or crash the value of debt, which would destroy the banking system. So how about inflating the money supply to dilute the value of debt? All in one fell swoop?

Right now, central bankers are diluting the value of debt very slowly by pushing interest rates below the rate of inflation. Some call this “financial repression.” It’s an unspoken policy that has many negative consequences. What is an alternative, since all attempts to “fix” the current system with more borrowing and printing are failing?

How about the classical gold standard, which stands out as the least flawed of all the systems we’ve tried. Each nation could choose to peg its local currency to gold at a price that allows for enough growth in bank reserves to greatly reduce the burden of public- and private-sector debts.

Re-pegging a currency like the US dollar to gold at the current price (about $1,550) has its pitfalls. Most notably, it would not deleverage an overleveraged banking system. But re-pegging the dollar to something like $10,000 an ounce might do the trick.

Hedge fund managers Lee Quaintance and Paul Brodsky from QB Asset Management wrote a fascinating outline on the potential reintroduction of gold into the monetary system, while simultaneously implementing what one might consider a debt jubilee. I recommend reading the entire outline. Zero Hedge posted it at this link. QB explains the mechanics of how it could work in the US:

|

This path would weaken the economy-sapping effects of debt created since President Nixon closed the gold window. It would transform a debt-based currency into an asset-backed currency. No longer would one ask the unpleasant question “What backs the dollar?” and come away with even more questions (and a headache). Right now, the dollar is backed by Treasuries held on the Fed’s balance sheet, which are in turn backed by dollars, which are in turn backed by faith in fiat money — i.e., nothing!

QB’s monetization scenario would impose losses on certain parties as the reset button is hit, but unlike most of the policy prescriptions we’ve seen lately, it seems to solve more problems than it creates. Most notably, politicians could argue that this reset would involve “migration of value, in real terms, from leveraged assets to unleveraged goods, services and assets.” Wage earners would be winners relative to asset owners, because “stable to higher nominal asset prices would require even higher nominal wage and consumable pricing looking forward.”

This scenario argues for holding some shares in producers of physical commodities (especially gold miners), even if it feels like we’re in a deflationary environment. A gold standard, after a one- time debt monetization, would make for a more-balanced, efficient global economy less prone to violent booms and busts.

As an added bonus: Central bankers would no longer be viewed as superheroes! Just meager servants, pegging the money supply to gold and letting the free market determine the price of money. After all, when in history has central planning worked better over time than the free market?

We can hope the central bankers of the world stumble their way to a solution like that proposed by QB Asset Management before they inflict even more damage to the foundation of the global economy. Unfortunately, conditions may have to get much worse in financial markets, banking systems and economies before such “outside the box” ideas are considered. A defensive portfolio with exposure to gold and other real assets seems like the right mix in today’s environment.

Regards,

Dan Amoss

for The Daily Reckoning

Editor’s Note: We like it when things make sense, fellow reckoner. And at a time when those in charge of the world’s money seem to have little of it themselves, we’re increasingly happy to have gold on our side. As Dan points out above, there are numerous reasons why a gold-backed currency simply makes sense, and after seeing this presentation, we can tell he’s in good company.

Click here to discover a long-lost gold “bible” penned by none other than Congressman Ron Paul…and how you can snag a copy for yourself.

——————————————————-

Here at The Daily Reckoning, we value your questions and comments. If you would like to send us a few thoughts of your own, please address them to your managing editor at joel@dailyreckoning.com” title=”joel@dailyreckoning.com” target=”_blank”>joel@dailyreckoning.com

By now, everyone has seen the chart of Homestake Mining and its bull market run from 1924 through 1935. Hence, there is no need to repost it. In this editorial, Frank Barbera shows a handful of charts of gold stocks and gold stock indices during the Depression era. US Gold producers apparently bottomed in 1929 while the Financial Times Gold Index bottomed in 1931. The time to buy the gold stocks was when deflation set in. More recently, the time to buy gold stocks and physical (Gold or Silver) has coincided with fears of deflation.

Below is a chart that that shows the Google search volume for “deflation.” Predictably, there is a big spike at the end of 2008. There is also a mini-spike in 2010. Unfortunately Google doesn’t have search data pre-2004. Policy makers had a fear of deflation during 2002 and 2003.

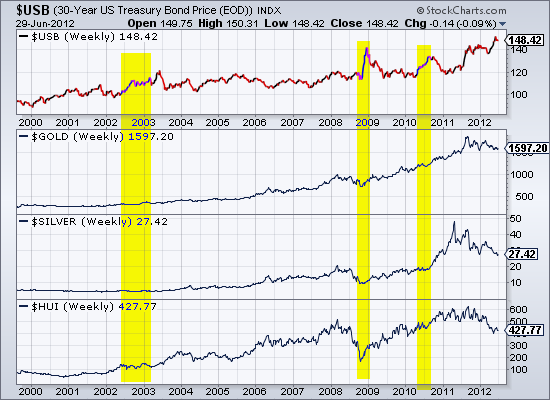

Below we plot Bonds, Gold, Silver and the HUI Gold Bugs index. We highlight the periods in which deflation fears emerged. That would be 2002-2003, October 2008 and briefly in the spring of 2010. All of course were buying opportunities within the bull market in precious metals. Note that the peak in Bonds in 2005 coincided with a major bottom in precious metals.

So why does the onset of or fear of deflation act as a catalyst for the precious metals sector?

….read more HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair