Gold & Precious Metals

In yesterday’s alert we wrote that the reversal in the precious metals market should once again not be taken at its face value and that one should not overreact based on it as the size of the potential rally was limited. Well, it turned out that “limited rally” was an euphemism for a decline. Gold, silver and mining stocks declined once again despite the previous day’s reversal and gold stocks confirmed the breakdown below the key support line. The implications are strongly bearish. However, there’s something ever more bearish and much more profound.

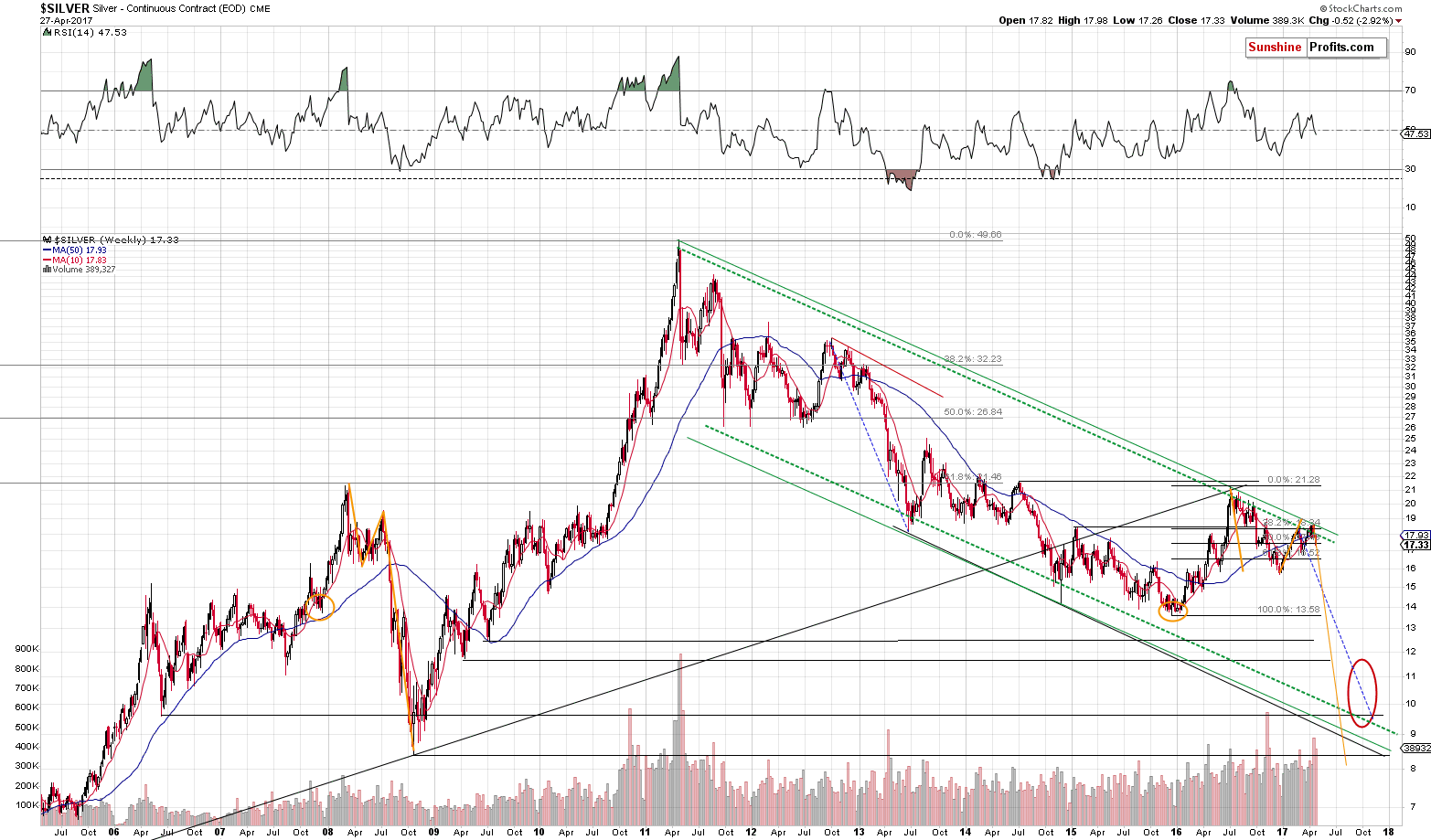

Let’s recall the situation in silver. A few weeks ago we wrote about silver’s move to the key resistance line and the huge importance of the invalidation of the breakdown below the line based on the weekly closing prices. Silver is now significantly below the resistance line, but the key question is if the decline is already over. Well, it seems that it’s far from being over and the analogy that we are going to discuss shows just how far it could be from being over.

History repeats itself – maybe not to the letter, but more or less – that’s the key principle of technical analysis. This principle is usually utilized by using chart patterns, but it goes beyond this – to self-similarity and fractal analysis. Long story short, if one manages to find a pattern that is a good reflection of a pattern from the past (either direct or on a proportional basis) then they could profit on the pattern’s continuation.

Based on the above paragraph and the title of this article, you may already suspect that there is a very important self-similar pattern in silver. Let’s take a closer look (charts courtesy of http://stockcharts.com).

Please focus on the parts of the chart that we marked with orange (in 2016-2017 and in 2007-2008). At first sight there’s nothing similar between what had happened in late 2007 and the first half of 2008 and what’s been taking place since December 2015. However, the more one starts to compare them, the more amazing it becomes.

First, let’s discuss the price moves.

Silver’s early 2008 rally started a bit below the $14 level and took place until the white metal moved above $21 (below $22, though). Then silver declined about $5.50 and then it rallied (which turned out to be its final rally before the big plunge) about $3.

Silver’s early 2016 rally started a bit below the $14 level and took place until the white metal moved above $21 (below $22, though). Then silver declined about $5.50 and then it rallied (which turned out to be its final rally before the big plunge) about $3.

That’s right, the price swings are almost identical not only in relative terms, but also in terms of the (almost) exact prices. What does the above suggest? That silver is likely to decline below $9. Yes, that’s quite extreme, so let’s “conservatively” say that it’s likely to decline to or below $10.

“C’mon that’s only the price analogy – what about time?” one could ask, and they would be correct. At least initially, because it is the price analogy that makes the above even more remarkable. The analogy in terms of time is proportional instead of being exact, but it’s still present and so are the implications.

The time between silver’s bottom in late 2007 and the 2008 top is more or less the same as the time between the 2008 top and the July 2008 top, which is also more or less the same as the time between the July 2008 top and the 2008 bottom.

The time between silver’s bottom in late 2015 and the 2016 top is more or less the same as the time between the 2016 top and the 2017 top, which… Is likely to be more or less the same as the time between the 2017 top and the (upcoming) 2017 bottom.

The existence of the above analogy not only confirms that the price analogy that we discussed earlier is valid, but it also points to early November as the (more or less) time target for the final bottom in silver. Interestingly, the above is in perfect tune with the red target ellipse that we drew based on other factors (long-term support levels and the similarity to the 2012 – 2013 decline). The above makes this price / time target combination even more reliable.

Still, is the above imminent? Does silver have to slide to or below $10? Of course not – the world changes and we should take every silver and gold price prediction with a healthy dose of skepticism and review the estimations when new developments emerge. The above does, however, make a very strong case for much lower silver prices in the coming months, as it confirms multiple signals coming from other parts of the precious metals sector and other markets.

For now, it appears that we are still in the “pennies to the upside, dollars to the downside” territory and short positions seem to be well justified from the risk to reward point of view. Naturally, the above could change in the coming days and we’ll keep our subscribers informed, but that’s what appears likely based on the data that we have right now. If you enjoyed reading our analysis, we encourage you to subscribe to our daily Gold & Silver Trading Alerts.

Thank you.

Sincerely,

Przemyslaw Radomski, CFA

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Listen to the Podcast Audio: Click Here

Listen to the Podcast Audio: Click Here

Mike Gleason: We are fortunate today to be joined again by Frank Holmes, CEO and Chief Investment Officer at US Global Investors. Mr. Holmes has received various honors in recent months including being named America’s Best Fund Manager for 2016 by The Mining Journal and received two more Lipper awards just last month in both the three year and five year precious metals equity funds categories.

He’s also the co-author of the book The Goldwatcher: Demystifying Gold Investing and is a regular guest on CNBC, Bloomberg, Fox Business, as well as right here on the Money Metals podcast. Frank, welcome back and thanks for joining us again. How are you today?

Frank Holmes: I’m well, thank you.

Mike Gleason: You mentioned back in January when we had you on right before Donald Trump’s inauguration that the first 100 days of his presidency would be a key on several fronts. Give us your thoughts on what these first 100 days have looked like. What have you gleaned from the last few months as you’ve been evaluating his policy decisions and the market’s reaction to those?

Frank Holmes: Well, I think it’s really difficult to grasp the difficulties of getting change in Washington. There’s just so many people that are addicted, from lobbyists to whatever on regulations and more rules and regulations. Regulations for taxation for every agency there is. It’s been much more difficult for him to tackle that than it was expected, and that’s recently showing up with interest rates falling back below and giving a negative interest rates, gold rallying from that. I think it’s hard for the average investor because something like 70% of the media is biased, and they’re pro-Democrat no matter what it is, and so you find the narrative from even so many business columns are wanting Trump to fail.

I find that really saddening because a great investor, the greatest in the world, Warren Buffett, who bet on Hillary Clinton and then when Trump won he said, “Well, I’m behind the President and if he does well we all do well, so that’s what I’m going to do,” and I’m more of a Buffett cheerleader in a thought process, so I think it confuses a lot of people that how difficult it is, and I think that to really read through his message, that he wants bilateral agreements, he wants to renegotiate agreements with the benefit to the middle class of America. I think that that’s very positive, but no matter what he does, we’re just getting skewed with a negative sentiment.

Government’s basically have two levers to manage the economy. One is monetary policy, the other is fiscal policy. Monetary policy is money supply and real interest rates. Fiscal policy is tax and spend and regulations are an indirect taxation on a sector of the economy. When it comes back, what we witnessed under Obama was an administration that was on steroids in every department on new regulations. It was a massive increase, and the only way to have economic growth with this massive increase in regulations which has always been a drag on the economy, is to have cheap money. Low interest rates, and to a point where they went negative. When I say negative, is that every month we get what’s called the “CPI number.” The CPI tells us what Consumer Producer Index of inflation is.

That inflation index is an important factor because if it’s 2% and the government wants you to buy their 10-year government bonds, and they’re only going to pay you 1.5%, you’ll say, “Well, that’s a bad deal. I’m going to lose half a percent every year for 10 years.” Whenever that happens, gold becomes a very attractive asset class, and so do companies that are paying dividends and have the capacity to raise dividends. That’s the other part where you see in the stock market rally for the past eight years predominately, and we’ve had negative interest rates. And you see gold fall and rise every time we’ve had this positive/negative.

For your listeners, every month the CPI number comes out, and you deduct that from whatever the government wants you to pay for their 5-year and 10-year government money, and the core relation is immense. Anytime they’re paying you more than the CPI number, gold falls. Anytime they’re paying you less, gold rises.

Mike Gleason: Yeah, very well put. It is obviously a big thing that we look at, and we’ll need to continue to look at. What are you expecting for that situation here going forward? Do you expect a negative real interest rate environment to persist here, Frank?

Frank Holmes: Yeah, I think that as long as you have this massive burden of regulations, you’re going to have to have cheap money. Raising interest rates right now is only going to hurt the economy, and there’s some parts that are already trying to show up with that. The concerns, stay away from auto parts. Automakers have a huge inventory, and a lot of the recent cars have been financed with basically junk paper, because a lot of people can’t qualify. It seems to be a very risky sector. So, what happens if that short term interest rates now, I remember I wouldn’t call and ask some car dealers locally, and if you want to use their services, it’s 4% for a car. If you can get one of the credit unions here, you can get it down to 2%, but a year ago it was one and a quarter.

Mike Gleason: Yeah, I think that as long as you have this massive burden of regulations, you’re going to have to have cheap money. Raising interest rates right now is only going to hurt the economy, and there’s some parts that are already trying to show up with that. The concerns, stay away from auto parts. Automakers have a huge inventory, and a lot of the recent cars have been financed with basically junk paper, because a lot of people can’t qualify. It seems to be a very risky sector. So, what happens if that short term interest rates now, I remember I wouldn’t call and ask some car dealers locally, and if you want to use their services, it’s 4% for a car. If you can get one of the credit unions here, you can get it down to 2%, but a year ago it was one and a quarter.

Frank Holmes: I was in London also and I had a lovely lunch with Nicholas Vardy. Very insightful. He’s a newsletter writer that went to Stanford and then did his law degree at Harvard, and was there when President Obama was there, and our new Supreme Court judge. So, he’s very insightful and talkative, and gave me lots of color, and whenever I travel to these places, I always ask the taxicab drivers what do they think, and the thoughts of Brexit, it was ubiquitous. Everyone was happy for Brexit to go through, and they felt that the unions have taken control of the government policies in Spain and Italy and France, have prevented young people from getting jobs, and the only place for opportunity is in the UK.

They can handle only 50,000 families a year and there’s 500,000 coming in a year. So, they feel that you can’t stop these socialist unelected officials, and they’d rather control their own destiny. So, I think the Brexit is an interesting event, and I think that probably the vote will still remain very strong, even though most of the media don’t want to see it happen, but I think it will. I saw when I was in Zurich the construction was booming, there’s lots of reservations on the regulatory world globally. They believe that globalization, the slow down of that took place 10 years ago with the difficulty of moving money, the proof of burden that your money is your money, and the paperwork that goes with it, that they will not open an account for any American taxpayer today.

Neither will Bermuda, I found out. So, you get this different idea that the ability to move freely with yourself or money around the world is becoming restricted, but more so the advent has been before building a wall between America and Mexico, all that drama that’s taken place is actually really showing up in the movement of capital. It’s much more difficult, and there are things I learned. They’re big believers in gold. They believe that this mismanagement of fiscal monetary policy, the French government, the socialist there was proposing a 100% income tax, basically taking people back to feudalism. Bizarre that he would think that, and I think what happens is that when you don’t get mainstream thinking, that is we want to have the streamline regulations, have taxes that are appropriate and accountable for what we’re spending the money for, whenever you get this excessive right wing or excessive left wing, you create volatility for investors.

That’s something that’s coming out of France. France is the second most important part of the Europe, when England’s gone. The other thing you need to realize is that England was the second biggest contributor to the EU budget, and that was offending a lot of the British taxpayers that not only were all these immigrants coming in because of the bad government policies of other countries, they were sending their tax followers out to build better places for France and Spain, and other countries. So, I think that the world is resetting. I think that’s positive, to get a rebalance there, and I think that we’re going to continue to live with low interest rates and suffer with these regulations until we get finally a breakthrough. And once we get a breakthrough, because whenever you get fiscal policy incentives, streamline regulations, create tax incentives, you get a much bigger bang for your dollar and growth in the economy.

That’s why when China started its revolution with Deng Xiaoping in 1978, they created seven tax free zones. You see that in San Antonio to get Toyota to build a car plant here a decade ago, it was to provide all these tax and training concessions, and it’s been a big windfall to us. So, it is so key and right now Washington’s in a stalemate of streamlining regulations.

Mike Gleason: Do you expect the bullishness for gold that you were seeing there in Europe to make its way here to the U.S.? I mean, since gold is really the anti-dollar, it seems that we need U.S. hedge funds and some hot money to come into the market in the Western world to really take it to the next level. Do you see that happening here, Frank? And what could possibly trigger the renewed appetite for precious metals among U.S. investors? Because retail demand is quite soft and it seems like most of the rest of the world are really the ones that are focusing on gold right now.

Frank Holmes: I think it’s not so much this conspiracy theory on gold and money and the dollar. I think it’s better to look at the imbalances that take place in an economy’s fiscal and monetary strategies. And whenever you get these imbalances, gold will perform exceptionally well during that process. It’s in America and it’s in many other countries in the world, of this monetary driving the equation, and not fiscal policy that’s driving the equation, except for more taxation and regulation. I just think that the U.S. still has this imbalance. Europe clearly has a much greater imbalance, and difficulty in this monetary/fiscal policy imbalance. And I think we’re going to mutter along with it.

You saw India has a surtax on gold imports and finally after all the currency debauchery that took place where they wiped out 86% of paper money. 86% of Indian money, paper money, was in 10’s and $5 bills. 86%. They said, “If you can’t show where you got that money from, then you lose 30% of the dollar value. You better run to the bank and show where that cash came from, to stop the corruption as they’re going through an election cycle. Well, that’s all done and immediately you saw a surge in gold prices. The demand that India’s getting back to, it was up 300% from a year ago. I think there’s other positive parts to take a look at that gold demand, the supply from around the world is just not growing the way paper money is growing. It’ll just be these continuous imbalances and you should have your exposure to gold and it should be 5-10%, and the magic is to rebalance.

So, when we get these incredible runs, you have to take some profits off the table because we will get these big corrections, in particular in the (gold) stock prices. I think the real shocker here in this first quarter is last year in the first quarter when gold jumped 6%, you had a massive move from 40-80% in gold stocks. This year, it’s a very modest increase of like 14% I think for the first quarter, and gold is up six and a half percent. The big part of that is this GDXJ rebalancing and it’s garnered, it’s almost 10% of all gold equity funds. Money’s not really going into the gold equity funds. They’re going into the gold ETF which has nothing, no thought process on taking stocks for values. It’s just market cap.

Now, they’re making a decision that they don’t want to have as much small cap because they could own too much of a company and they’ve been dumping, and it’s going to happen now over the next month, something like three billion dollars’ worth of the junior gold producers. These are disruptive in the capital markets. They make people skeptical, et cetera, but you know what? They provide an opportunity. If you can understand an index as doing this and all the regulations around that index and that’s what they say as the reason they have to do this, then it becomes your opportunity.

Mike Gleason: Obviously geopolitics are starting to flare up here as tensions between us, Syria, Russia, North Korea, and China are making headlines. Where does this all head and what investment class do you see being the primary beneficiary of all this global tension? Because it does feel like we’re in maybe the calm before the storm here, especially when you throw in everything that’s going to happen in Europe, with those key votes in the EU later this year. What are your thoughts there, Frank?

Frank Holmes: I think that dividend stocks and stocks that have the capacity to raise dividends are going to still do well. I really do. I think that gold is going to be… that there are so many great quality gold stocks, and I think that they’re going to do well. I think that MLPs are involved in the shipping of energy, not the processing of energy, they’re going to still do extremely well. I’m constructively bullish, it’s just I think we’re going to have more volatility. And volatility should be to your benefit. You should understand what that DNA of volatility, and let me help you with your listeners. When you do a rolling 12 month period for the past decade, it is a nonevent, that is 70% of the time gold can go plus or minus 20%. That’s the same thing with the S&P.

They’re both the same. They both have the same DNA of volatility. But gold stocks have a DNA of volatility which is two times that, that is 70% of the time, it’s a nonevent for them to go plus or minus 40%, and so is biotechnology, and so are other sectors of the economy that have a greater volatility to them. So, the magic is to understand that DNA of volatility, and every time you get a big sell off on the gold stocks, you want to be a buyer because the math is in your favor to rebound back to the mean. The same thing is with other asset classes, like technology, especially biotechnology, which has the same DNA volatility as gold stocks.

Emerging markets have the same volatility of gold stocks, and that’s another classic for your listeners. If you read New York Times, it always has negative news on emerging markets and Trump is bad because emerging markets, et cetera. Did you know that the Chindia ETF, which is basically China and India equally weighted ADRs, big cap stocks in that particular ETF, which represents 40% of the world’s population, was up two times what the S&P was last year? In the first quarter of 2017, its return was twice the S&P 500. So, emerging markets are actually doing well. When I look at our emerging European fund, the dividend yields on there are averaging like 4%. When I look at our global resource fund, the dividend yields there are like 3%.

I mean, I’m buying a real resource, I’m getting a dividend that’s growing, it’s growing at 3%. There’s still lots of M&A activity in the chemical industry, so there’s lots of places I’m actually constructively bullish on. If you believe of this other part, the whole theme on military spending, it’s 600 billion dollars. They’ve sold off here recently, but I think stocks like Boeing which is in our JETS ETF, is not only making all the airlines that you’re flying, but they also make a lot of components that’s for the military. That stock has been on a beautiful climb. When you look at the budget that’s going to go towards military spending, and technology towards the element of technology in defense spending, those stocks I think are going to do exceptionally well over the next five years.

Mike Gleason: Well gold and silver are off to a good start in 2017. We’ve talked earlier about negative real rates supporting prices, and some other potential market movers that could drive demand for the yellow metals specifically. As we begin to close here, what else if anything are you focusing on in terms of potential catalysts that may drive things for the rest of the year? And do you think there’s still some more upside in the metals?

Frank Holmes: Yeah. I think you’re going to see… I have to forecast what I thought the price of gold could do, and I said it can run to $1,500 this year. You have that probability on a rolling 12 month period. When I look at my quant models and I look at the fundamental factors around the world, it could easily do that. I’d also like to point out to all your listeners that every president in the ’90s, and we’ve seen in the past decade, starts off with a campaign that “China’s a currency manipulator,” until they get into power and they realize they’re really not manipulating the currency.

The New York Times is anti-China, they’re anti gold and they’re anti the Clintons, so it seems to be this pervasive, don’t get confused with all those headline news, and recognize that China, there’s a lot more in common with China’s leader with Trump than you would normally think, and the same thing is with the leader of India, Modi. These are three mavericks that the media liked to attack. They do things their own way, they go after corruption, they want to renegotiate deals, they all believe big in their own country. They’re very country centric. They want to trade with the rest of the world, but their priority is to be focused on their own domestic economy first. So, I think this is a really positive dynamic and I’m going to bet like Buffett, I’m being positive.

Mike Gleason: Well thanks for the fantastic insights as usual, Frank. It’s always great to hear your thoughts and we really appreciate your time once again. Now before we let you go, please tell our listeners a little bit more about your firm and your services and then also about your fantastic Frank Talk blog.

Frank Holmes: Well, thank you. Very kind, gentle worlds. I love it, and we do work very hard. We’ve done 88 awards in a competitive arena in the fund business on education. We have 40,000 readers in 180 countries, and I welcome to go to USFunds.com, and sign up for Frank Talk. I talk about my travels around the world, as we started off this conversation, and try to relate to investors my tacit knowledge along with my quant explicit models, to try to navigate through the world. So, please go to USFunds.com, we have the top performing gold funds, we have also, I love the short term tax refund called NEARX. It’s stable, $2 approximate price, and it’s much better than a money fund because of its higher coupon. Much higher. We have many different types of funds from China to Eastern Europe and domestic funds.

Mike Gleason: Well excellent stuff. Thanks again, Frank. Congratulations on picking up some more awards. Very well deserved, keep up the good work, and we’ll look forward to speaking with you again in the coming months. Take care.

Frank Holmes: Thank you once again, my friend. Cheers.

Mike Gleason: Well that will do it for this week. Thanks again to Frank Holmes, CEO of US Global Investors. The site is USFunds.com, and be sure to check that out, and also the previously mentioned Frank Talk blog, some of the best market commentary you will find anywhere on gold, the miners, the commodities as a whole, and many other topics related to the investment world. Again, you’ll find all that at USFunds.com.

Mike Gleason is a Director with Money Metals Exchange, a national precious metals dealer with over 50,000 customers. Gleason is a hard money advocate and a strong proponent of personal liberty, limited government and the Austrian School of Economics. A graduate of the University of Florida, Gleason has extensive experience in management, sales and logistics as well as precious metals investing. He also puts his longtime broadcasting background to good use, hosting a weekly precious metals podcast since 2011, a program listened to by tens of thousands each week.

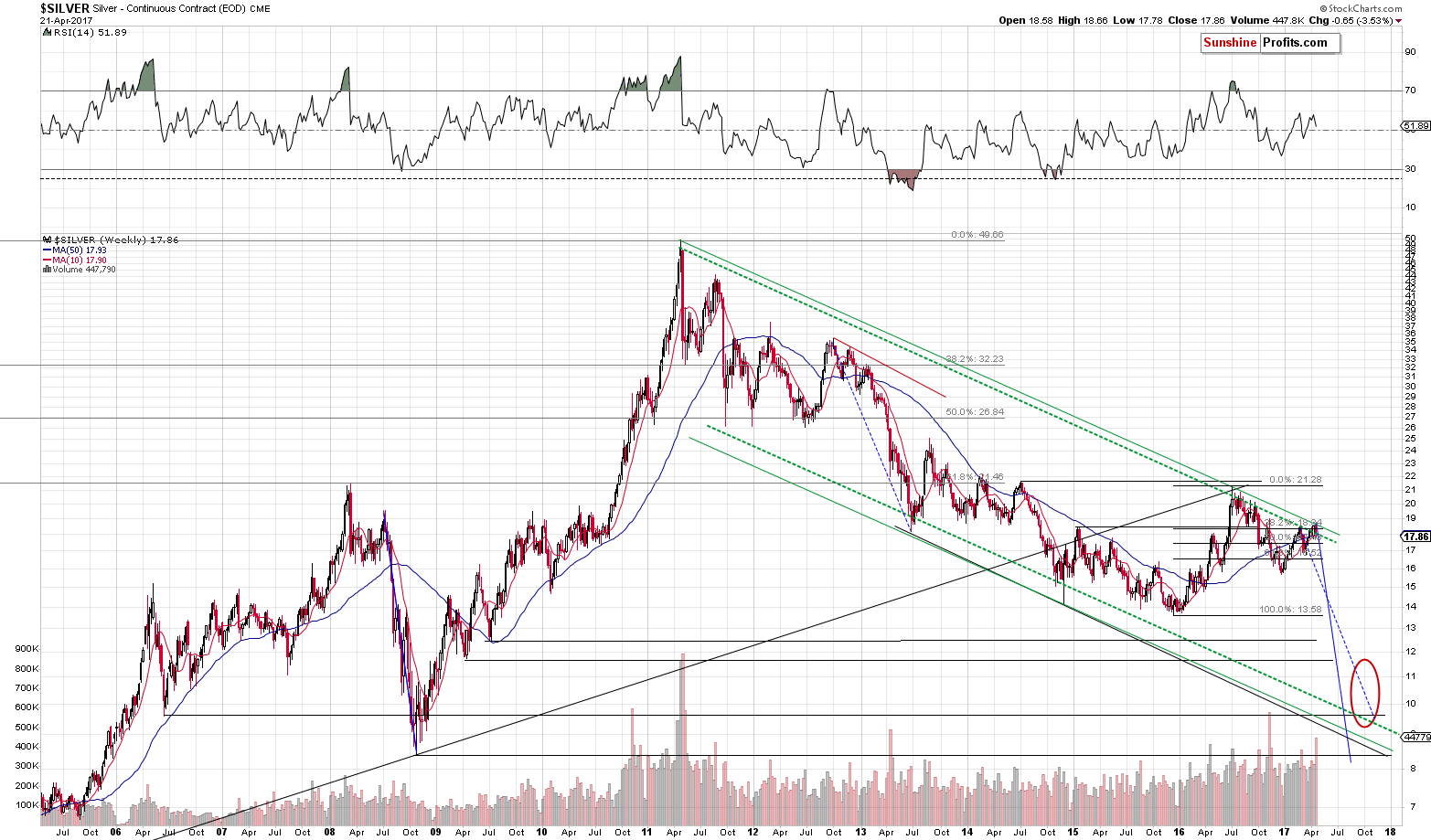

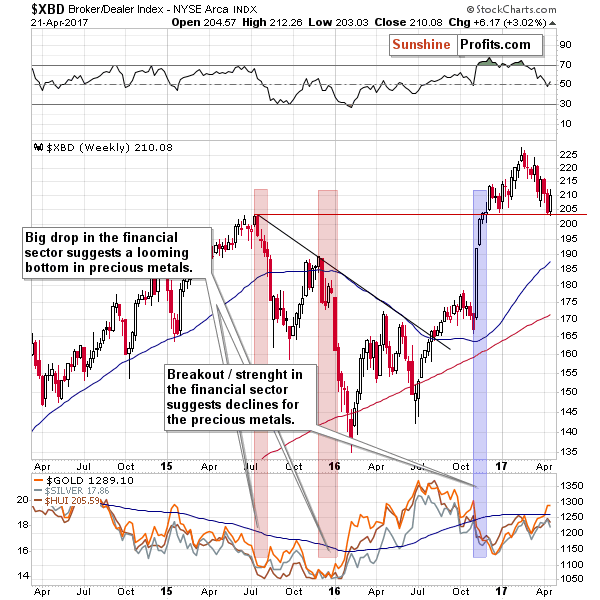

The most prominent action in the precious metals market that we saw last week, took place in silver – the white metal closed the week below the important long-term support/resistance line, thus invalidating the previous breakout. However, there’s more to the precious metals market than just the action in silver. In today’s free gold analysis, we discuss both the developments in silver and other factors.

Let’s start with silver itself (charts courtesy of http://stockcharts.com).

In Friday’s alert, we wrote the following:

(…) Still, if gold was to move higher (to $1,310 or so), then the above chart provides us with an analogous upside target – the upper, long-term green line (based on the same major tops as the lower line, but drawn through intra-day tops). It’s currently at about $18.70 – just 10 cents above this week’s high. So, the upside is quite limited.

Silver has indeed moved lower after it reached the upper of the declining, long-term, green resistance lines. The lower one (based on weekly closes) is currently at about $18, so if silver manages to close the week below it (which seems likely), the previous breakout will be invalidated and it would likely trigger another powerful decline. For now, the fact that the upper resistance line held, continues to have bearish implications – the upside is very limited and the downside is huge.

It didn’t take long for silver to slide below $18 – it did so a few hours after we posted the above and it’s been trading below it since that time. At the moment of writing these words, silver is at $17.92, so the odds are that it will indeed close the week below $18.

The volume on which silver declined was significant as well, so the implications are definitely bearish.

Naturally, if silver’s signals are not confirmed by other markets, one shouldn’t rely on them, but this time they are. In addition to multiple factors that we discussed in the previous alerts, we would like to emphasize that the breakdown in mining stocks was not invalidated yesterday.

The invalidation of the breakdown is now a clear fact. It’s no longer bearish, somewhat bearish, or a bit bearish – it’s very bearish. It’s been confirmed by the weekly closing price, and since the support/resistance line is based on the same kind of prices, the invalidation of the breakout is meaningful and clearly bearish.

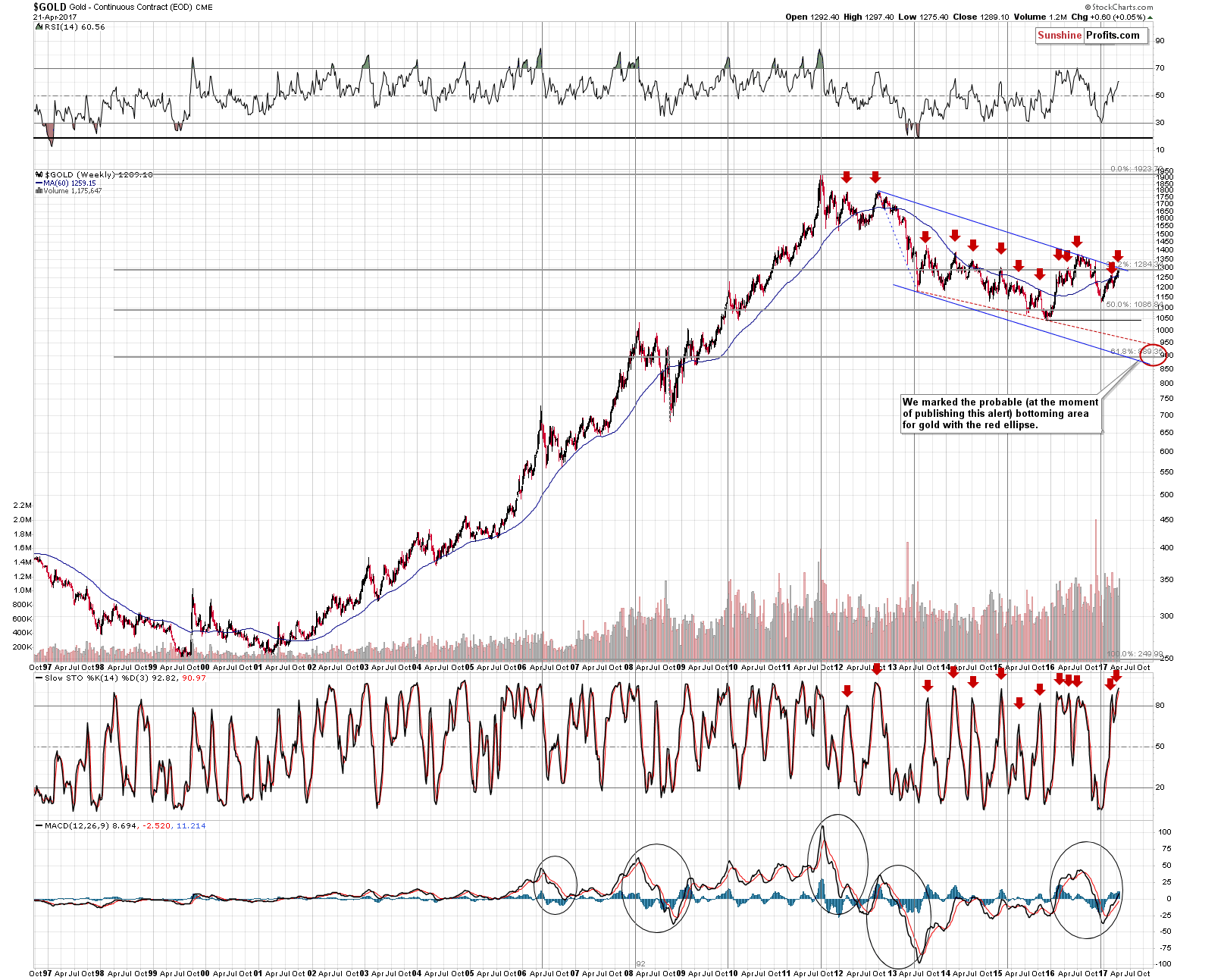

The long-term gold chart confirms the above bearish comments. The yellow metal moved to the declining long-term resistance line and then declined once again. There was no breakout, so the trend remains down.

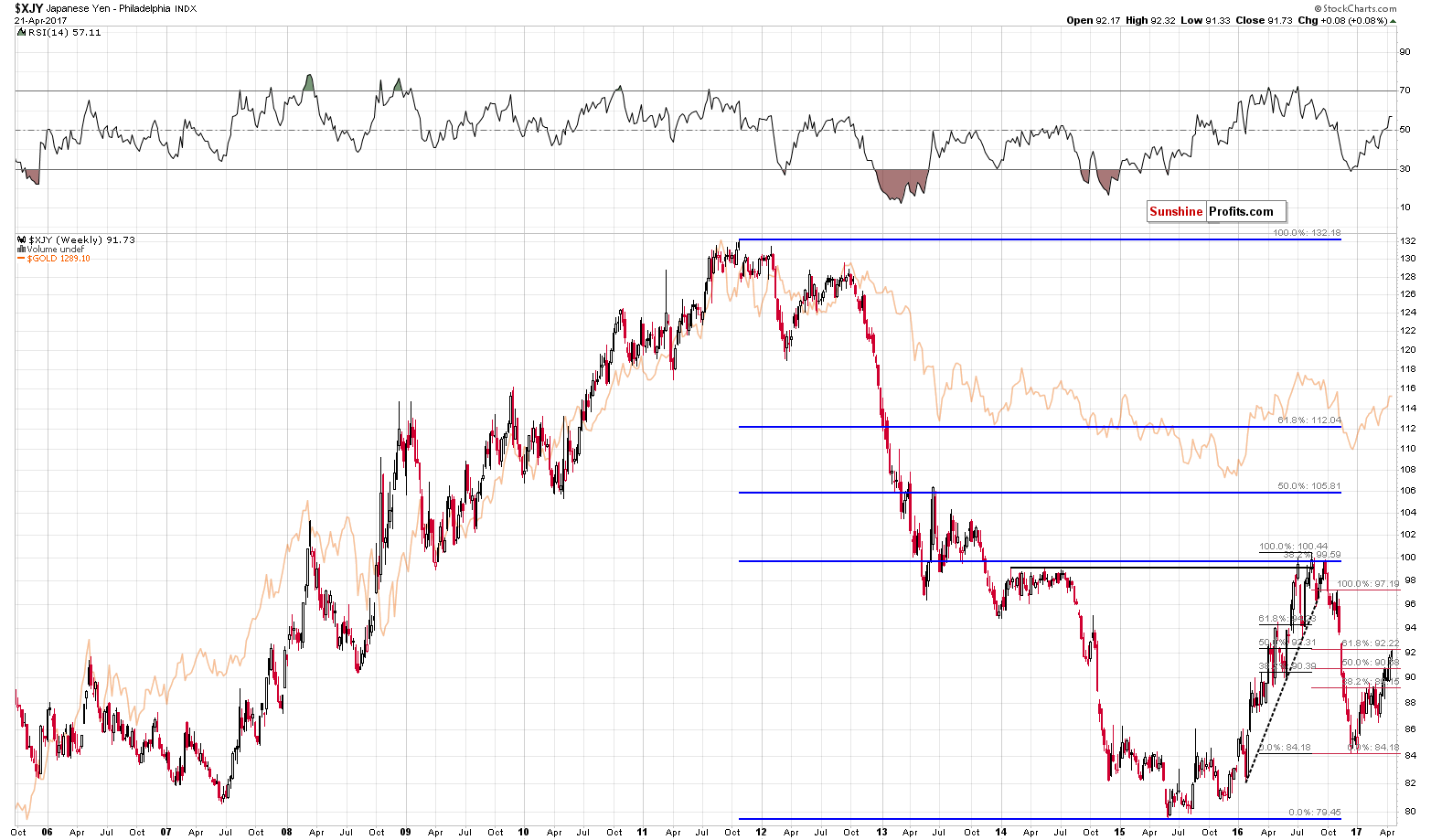

The Japanese yen which is closely linked to the price of gold, also moved to its critical resistance level (further supported by the zigzag corrective pattern) and thus it’s likely to have reversed its recent direction and decline in the coming days – and so is gold.

The financials were more clear as far as their signals are concerned. They too moved to an important level, but their bounce after reaching it was very visible. That’s a major medium-term development. This description is particularly important as the precious metals sector tends to react to major (!) moves in financial stocks (moving in the opposite way). Since the major move up is now (given the confirmation of the breakout above the 2015 high) likely for the financial stocks, a major move lower is likely for the precious metals sector.

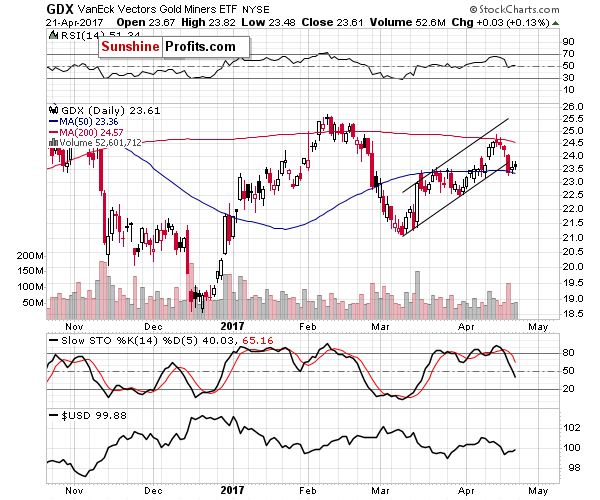

Let’s take a look at the short-term mining stock chart that appears to be leading gold once again (miners moved ahead of gold in the past months).

Gold and silver stocks confirmed the breakdown below the rising short-term support line by closing below it for 3 consecutive trading days, moving back to it without invaliding it and by closing the week below it. The volume on which Thursday’s and Friday’s upswing materialized was low, which also confirms that the move lower is the current true direction and the upswings should be treated as corrections.

Summing up, the precious metals market appears to be starting to decline even despite the lack of direct reasons to do so and that’s a particularly bearish situation. Precious metals had all the reasons to rally – tensions regarding North Korea, the unresolved situation regarding the U.S. airstrike in Syria and tensions before the elections in France… And it didn’t do anything substantial. Silver declined and miners have not only broken below the rising support line, but they also confirmed the aforementioned breakdown. This, plus other factors discussed previously support the expectation of lower precious metals prices in the coming weeks. Naturally, the above could change in the coming days and we’ll keep our subscribers informed, but that’s what appears likely based on the data that we have right now. If you enjoyed reading our analysis, we encourage you to subscribe to our daily Gold & Silver Trading Alerts.

Thank you.

Sincerely,

Przemyslaw Radomski, CFA

Founder, Editor-in-chief, Gold & Silver Fund Manager

APRIL 21, 2017, 10:40 AM

The first round of presidential elections in France is held on Sunday. What can we expect from that event and how can it affect the gold market?

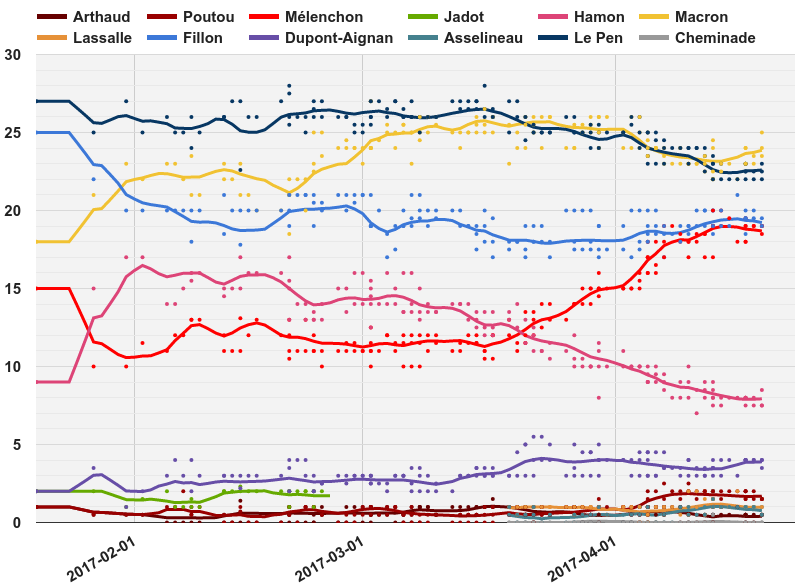

In the recent edition of the Market Overview, we wrote that centrist Emmanuel Macron and nationalistic Marine Le Pen were expected to move on the next round. However, the situation has complicated a bit since then. As you can see on the chart below, actually four candidates have pretty good chances to advance to the next round. It’s because both hard-left Jean-Luc Melenchon and conservative Francois Fillon have gained momentum recently.

Chart 1: Opinion polls for the first round of voting (smoothed 14-day weighted moving average) updated daily from Wikipedia.

It’s good news for the gold market, as it means higher uncertainty. Now, Marine Le Pen is not the only terrifying candidate in town. Jean-Luc Melenchon’s economic program is similarly frightening for the financial markets. For example, he proposed to impose a 100 percent tax on those who earn above €400,000. Yup, you guessed, he is a commie and a fan of Hugo Chavez.

The consensus is that Macron and Le Pen will move on to the next round. Therefore, if this scenario realizes, the markets should not be affected significantly. And since Macron is expected to beat Le Pen in the run-off, there may be a relief rally in the French bonds and the euro. The safe-haven demand for gold should decline then, but a weakening dollar would support the yellow metal.

Macron and Fillon would be the best for the financial markets, as both candidates are from the mainstream, so radical changes would probably not happen. It would be the worst scenario for safe havens, but the best for the euro.

Other scenarios are much more interesting. Fillon and Le Pen would go much more neck and neck than Macron and Le Pen. Higher uncertainty should support the safe-haven demand for the gold market. Melenchon and Fillon would be even more fascinating, as the former is expected to beat the latter in the second round. The vision of a communistic president in France could encourage investors to buy some gold. But probably the best scenario for gold would be a run-off between Melenchon and Le Pen. It would be like a duel between Sanders and Trump, only squared. Such a scenario could trigger some financial panic and boost safe-haven demand for gold.

The bottom line is that there is the first round of the French elections this weekend. The outcome of the election is uncertain, since four candidates have chances to move on to the run-off. If Macron advances on Sunday, he is the most likely to win in the run-off, no matter who he faces. We could see then a relief in risky markets and a decline in gold prices. But if he fails, then any outcome is possible. In this scenario, investors should expect rising uncertainty which should provide additional support for the price of gold. The most market-unfriendly outcome would clearly be a face-off between far-right Le Pen and far-left Melenchon. The risk appetite could soften then, which may boost the safe-haven demand for gold (although the likely appreciation of the U.S. dollar may limit the gains). Will this happen? Given a tarnished reputation of polls and a wild surge in Melenchon’s odds, only time will say. Stay tuned!

French Elections and Gold @ 7:18 am Friday April 21st

In the previous edition of the Market Overview, we analyzed the potential impact of the European elections on the gold market. As the Dutch elections are behind us, let’s see how the Wilders’ defeat affected the markets and the political outlook for France, where people will vote for the president on April 23.

Investors reacted positively to the outcome of the Dutch election, relieved that populists did not win. European stocks and the euro rose, while the France-Germany 10-year bond yield spread declined after the elections. This is because Wilders’ failure is considered to indicate that “the wrong kind of populism” is losing momentum.

Although Wilders lost, it does not mean that all risks vanished and the threat of protectionism has gone. Actually, the triumphant party won fewer seats in the last parliament, while Wilders got more than the last time (the same applies to Marine Le Pen, who is much more popular than her father, the founder of the National Front). And Dutch voters are still flirting with populism – they are just more dispersed, as people also voted for other right-wing parties. Moreover, other parties, including the ruling People’s Party for Freedom and Democracy, adopted a more right-wing tone during the campaign, as the prime minister’s decisive approach toward Turkish diplomats showed. Let’s face it: Wilders is the second force in the country now, so he would definitely influence the domestic politics. In a sense, a populist party did not win, but populist ideas were pushed to the mainstream political agenda instead.

Therefore, it is too early to state that Le Pen is set to fail. Importantly, her odds of winning in the run-off increased after the Dutch elections. As a reminder, according to the polls conducted before the presidential television debate, she will win in the first round of voting, but lose in the run-off. Her odds of winning in the second round are 40 percent with Macron and 45 percent with Fillon, but as Emmanuel Macron is believed to have won the debate, the chances of Le Pen fell slightly. The French election is a different kettle of fish, as there are only few candidates (the run-off is between the two contenders who get the most votes in the first round of the elections), while the parliamentary election in the Netherlands was between 28 parties. If the political scene in the Netherlands was not so fragmented, Wilders could win. Another issue is that French economy is performing worse than the Dutch (the unemployment rate is twice as high, while the GDP growth is half of the Netherlands). Hence, although the probability of Le Pen’s victory is not high (in the second round, voters are likely to build a coalition against her), we believe that her chances did not change significantly after the outcome of the Dutch elections. In other words, investors should not extrapolate trends between the Netherlands and France. The presidential election in the latter remains one of the major risks for the euro area.

Thus, investors are nervous ahead of the French elections, and we could see a short-term volatility in European assets and the euro; we could also observe some inflows into gold, the ultimate safe-haven asset. For example, the euro was up 0.6 percent to a six-week high after the French presidential debate, while the French interest rate premium over Germany declined. According to the polls, centrist Emmanuel Macron won the debate, which eased the political risks to the EU from Le Pen. The price of gold rose together with the euro. It shows that investors started to take into account the political uncertainty in Europe after trading solely on expectations of the Fed’s and Trump’s actions. It also indicates that the exchange rate channel is more important for the yellow metal than the uncertainty channel.

However, long-term investors should not overstate the impact of that election on the gold market. As the chart below shows, the price of gold actually declined before the Dutch elections, while the euro gained against the U.S. dollar.

Chart 1: The price of gold and the EUR/USD exchange rate in 2017.

It implies that macroeconomic factors and central banks’ actions may be more important drivers for the currency exchange rates and the price of gold in the long-term. Surely, the French election is much more important than the Dutch, given the size of the French economy and the key role of the country in the EU, but even the surprising and really disrupting Brexit vote caused only a short-term rally in gold prices. Hence, the EUR/USD exchange rate and the price of gold may be strongly affected by the prospects of the election in the short-run, but their impact may not be long lasting.

If you enjoyed the above analysis and would you like to know more about the impact of the current macroeconomic trends and political uncertainty on the gold market, we invite you to read the April Market Overview report. If you’re interested in the detailed price analysis and price projections with targets, we invite you to sign up for our Gold & Silver Trading Alerts. If you’re not ready to subscribe at this time, we invite you to sign up for our gold newsletter and stay up-to-date with our latest free articles. It’s free and you can unsubscribe anytime.

Thank you.

Arkadiusz Sieron

Sunshine Profits‘ Gold News Monitor and Market Overview Editor

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair