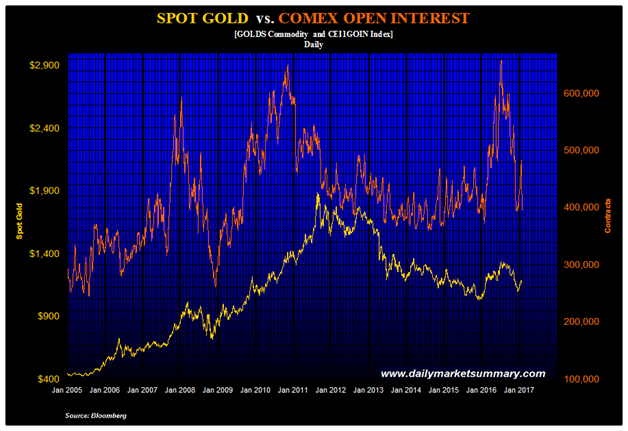

Last week we thought that we had seen the bottom in the gold correction. More evidence of that came Monday with the release of Friday trading data from COMEX. Last week, as the gold price began to fall towards its 50 day moving average where corrections usually end or breakdowns can begin, COMEX Speculators blew an enormous number of contracts out the window.

At the close last Monday, the Open Interest on COMEX was 483,408 contracts, a total which had grown quickly as the gold price advanced from the December low of $1124. At the Friday close, the Open Interest had fallen to just 395,599 contracts, a reduction of an enormous 87,809 contracts or 18.1% in just four trading days. Clearly, a large number of players panicked and liquidated BUT the price never even touched the 50 dma at $1178.

What happened? Was it fear of this week’s Fed meeting (statement this Wednesday)? Or the employment report this coming Friday? We don’t know. But it was the fastest, most aggressive liquidation we have seen in years. And it did not break gold. We think that’s likely bullish.

Related Articles

Want to read more Gold Report articles like this? Sign up for our free e-newsletter, and you’ll learn when new articles have been published. To see a list of recent articles and interviews with industry analysts and commentators, visit our Streetwise Interviews page.

Disclosures:

1) Statements and opinions expressed are the opinions of Rudi Fronk and Jim Anthony and not of Streetwise Reports or its officers. The authors are wholly responsible for the validity of the statements. Streetwise Reports was not involved in any aspect of the content preparation. The authors were not paid by Streetwise Reports LLC for this article. Streetwise Reports was not paid by the authors to publish or syndicate this article.

2) Seabridge Gold is a sponsor of Streetwise Reports. Streetwise Reports does not accept stock in exchange for its services. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

3) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

4) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their families are prohibited from making purchases and/or sales of those securities in the open market or otherwise during the up-to-four-week interval from the time of the interview/article until after it publishes.

Chart provided by the authors.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}