Stocks & Equities

Roblox, the kids gaming app that surged in popularity during the pandemic, soared in its market debut on the New York Stock Exchange on Wednesday. The company’s stock closed at $69.50 apiece, giving the company a market cap of $38.26 billion.

Roblox went public through a direct listing, following the lead of other tech companies including Spotify, Slack and Palantir. Instead of raising fresh capital in exchange for new shares, Roblox allowed existing shareholders to sell immediately, without being subject to a lockup period.

Shares began trading at $64.50, which represented a 43% increase from a private financing round in January, when the company sold shares for $45. The NYSE set a reference price on Tuesday of $45, though no stock changed hands at those levels. The reference price tends to reflect private market trading and does not indicate where a stock will open.

Each week Josef Schachter will give you his insights into global events, price forecasts and the fundamentals of the energy sector. Josef offers a twice monthly Black Gold newsletter covering the general energy market and 27 energy and energy service companies with regular updates. He holds quarterly subscriber webinars and provides Action BUY and SELL Alerts for paid subscribers. Learn more.

EIA Weekly Data: The EIA data on Wednesday March 10th was clearly bearish for prices as both crude inventories rose and US production recovered meaningfully. Commercial Crude Inventories rose by 13.8Mb last week following a record build of 21.6Mb last week. The forecast this week was for a build of 816Kb. US production recovered, rising 900Kb/d in just one week, to 10.9Mb/d,but remains 2.1Mb/d below last year’s 13.0Mb/d of production. In the coming weeks this could recover another 1.1Mb/d to reach 12.0Mb/d as rig activity remains strong and some more weather related production shut-ins come back on line. Private operators are driving the growth in production at the current time as large public companies are under pressure to pay down debt and provide shareholder returns. Private companies see the less competitive landscape as attractive to build their companies. For example private company DoublePoint Energy is running more rigs than energy giant Chevron. In specific basins private companies have large footprints. In Haynesville 74% of rigs are operated by private companies, in the Eagle Ford 38% and in the Midland basin 41%.

Refinery Utilization recovered to 69.0% from 56.0% but remains below last year’s 86.4%. Overall Commercial Inventories are 46.6Mb above last year or up by 10.3% to 498.4Mb. This is the build problem we have been warning about. Inventories will continue to build until we start the summer driving season. Total Product consumed fell by 88Kb/d to 18.67Mb/d. Gasoline Demand was the one bright spot rising by 578Kb/d to 8.73Mb/d as driving picked up with better weather driving conditions. Gasoline inventories fell as a result by 11.9Mb. Jet Fuel consumption fell by 436Kb/d to 849Kb/d. Overall US consumption of all products is 15% below a year ago, gasoline demand down by 8% and Jet Fuel demand down by 46%. Inventories at Cushing rose 500Kb to 48.8Mb and are up from 37.9Mb a year ago.

Baker Hughes Rig Data: The data for the week ended March 5th showed the US rig count up by one rig (five rigs up in the prior week). Canada had a decline of 22 rigs (nine rigs lower last week) as we have ended the winter drilling season and break up season has started. Canadian activity is 31% below last year when 203 rigs were working. In the US there were 403 rigs active, but that is down 49% from 793 rigs working a year ago. The US oil rig count rose by one rig. The Permian saw an increase of three rigs to 211 rigs working and activity is 49% below last year’s level of 415 rigs working. The rig count for oil in Canada fell by 12 rigs to 80 rigs working and is down 40% from 134 rigs working last year. The natural gas rig count fell by 10 rigs to 61 rigs active and is down from 69 rigs working at this time last year.

Conclusion:

Crude oil prices spiked up over the last week by nearly US$9/b to US$67.98/b as the Saudis held back from returning their shut in production (original cutback was for the two months of February and March with a 1.0Mb/d cut) that they were expected to bring back on in April. In addition the market was expecting a 500Kb/d increase from other OPEC+ members with Russia getting the largest allocation. Except for Russia and Kazakhstan all members rolled over their quotas. Russia received an increase of 130Kb/d and Kazakhstan an increase of 20Kb/d. So this approach was well received by oil markets and oil prices jumped. However, just this week the US added back 900Kb/d and with the addition of production by Russia alone, you have fully offset the Saudi quota move. In the coming weeks we expect to see further US production additions and if there is OPEC cheating as is likely, world inventories will grow in Q2/21 and prices will have reason to retreat meaningfully. Today WTI is down due to the big inventory build and is trading at US$63.43/b, down $0.58/b on the day. OPEC’s next meeting is on April 1st to discuss production levels for May.

Iran in the meantime is selling more oil into China and has plans to increase sales to India in the coming months as they see the Biden administration wanting a nuclear deal and willing to ignore Iran’s cheating on sanctions. The buyers love the lower prices that Iran is offering and as well payment terms are very generous with refiners not paying for the crude until after it is processed. Iran had been shipping 306Kb/d in 2020 but this has risen to 600Kb/d in January 2021 and to 850Kb/d in February according to Reuters and Chinese customs data.

Technically the support level for WTI crude is US$59.24/b now. Energy and energy service stocks are overbought and have been chased by hot momentum money and quarterly window dressing as we near the end of Q1/21. We remain in the bear camp now. The most vulnerable companies are energy and energy service companies with high debt loads, high operating costs, declining production, current balance sheet debt maturities of some materiality within the next 12 months and those that produce heavier crude barrels. Results for many companies for Q4/20 have been released and were not strong enough to justify current lofty stock price levels. If crude prices retreat these stocks could get battered.

We have had a SELL signal since January 14, 2021. Subscribers of our regular SER service were notified of this on January 14, 2021 and were informed of 14 stocks and the prices at which we think they should be harvested. We sent out a second SELL Alert on February 5th and added four additional ideas for harvesting. The next two-three months could see significant downside for the energy sector. The topping process for the general stock market is ongoing and some surprise event will prick this bubble.

Energy Stock Market: The S&P/TSX Energy Index now trades at 123 and is part of a lengthy, extended, and broadening topping process. The S&P/TSX Energy Index is likely to fall substantially in the coming months. A breach of 107.66 should initiate the sharp decline.

I will be on MoneyTalks radio on the Corus (Global) network with Michael Campbell on Saturday March 20th at 10AM MT. If interested in our discussion on the risks in the general stock market and the energy market specifically, please listen in.

If you want to listen to our February 25th webinar in the archive please go to our subscriber page and become a subscriber. For new subscribers, the quarterly choice gives you three months to see if the product meets your needs.

Subscribe to the Schachter Energy Report and receive access to our two monthly reports, all archived Webinars, Action Alerts, TOP PICK recommendations when the next BUY or SELL signal occurs, as well as our Quality Scoring System review of the 27 companies that we cover. We go over the markets in much more detail and highlight individual companies’ financial results in our reports. If you are interested in the energy industry this should be of interest to you.

To get access to our research go to https://bit.ly/34iKcRt to subscribe.

Commodities trader Mercuria Energy Group Ltd. struck a deal last summer to buy $36 million of copper from a Turkish supplier. But when the cargoes started arriving in China, all it found were containers full of painted rocks.

The saga unfolds like a gangland thriller, with the Swiss trading house saying it’s been the victim of cargo fraud. Before its journey from a port near Istanbul to China even began, about 6,000 tons of blister copper in more than 300 containers were switched with jagged paving stones, spray-painted to resemble the semi-refined metal.

The bizarre case highlights commodity traders’ vulnerability to fraud, even when security and inspection controls are in place. In 2014 and 2015, Mercuria took provisions to cover potential losses after metal contained in a warehouse in the Chinese port of Qingdao was seized by authorities as part of fraud investigation

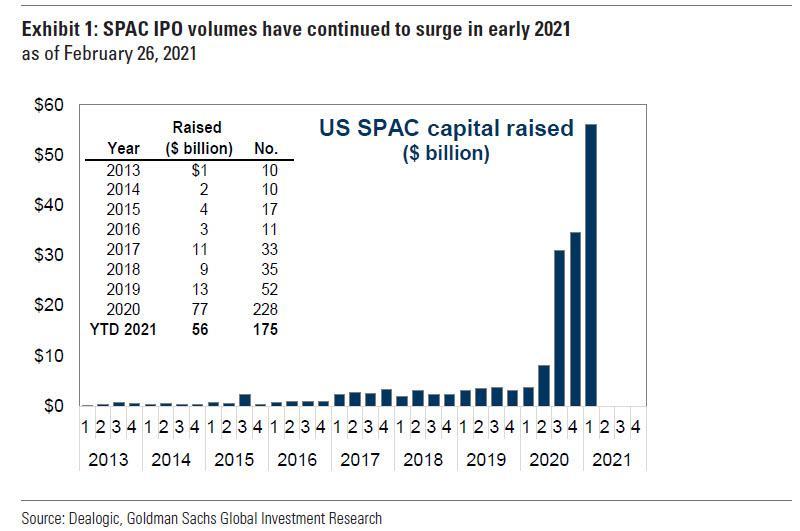

When we look back at the COVID-19 era, there’s little doubt that the SPAC boom that dominated financial headlines last year will be remembered as a shining example of what happens when the Fed steps up to monetize trillions of dollars in federal government stimulus, while millions of scared and desperate Americans scramble to parlay one free paycheck into two.

A few days ago, Chamath Palihapitiya, “the King of SPACs” whose leadership in the Virgin Galactic deal arguably makes him one of the progenitors of the contemporary bubble, warned that there will be even more pain ahead for SPAC investors, especially if bond yields continue to rise (which, as we have explained, they likely will, especially if Senators Sherrod Brown and Elizabeth Warren get their way).

“The SPAC market has taken a real beating…if you have one or two more months of this where all of a sudden bonds look better…you’ll have a bunch of busted IPOs or mergers.”

To borrow a phrase form Palihapitiya, SPACs “took a beating” during the Nasdaq drawdown that started last month.

Yet, as issuance volume explodes…

…the SEC has decided to issue a rare public alert about the sector, warning investors to think twice before investing their hard-earned money in shares of a SPAC, especially when celebrity pitchmen or women are attached to the deal. The notice cautions investors not to make investment decisions “solely based on celebrity involvement”.

Most importantly, the notice explained to readers how the economic interests of SPAC sponsors sometimes differ from those of their customers, as sponsors will typically get in on deals at more favorable terms.

The agency also offered readers a walk-through of how SPACs work, including explaining what a “warrant” is, the standard $10 debut trading price, and the typical two-year timeframe (SPACs usually promise investors they will close a deal within 2 years).

Read the full notice below:

The SEC’s Office of Investor Education and Advocacy (OIEA) cautions investors not to make investment decisions related to SPACs based solely on celebrity involvement.

Celebrities, from movie stars to professional athletes, can be found on TV, radio, and social media endorsing a wide variety of products and services. Sometimes they are even involved in investment opportunities such as special purpose acquisition companies, or SPACs, as sponsors or investors. Those celebrities may even be well-known professional investors.

However, celebrity involvement in a SPAC does not mean that the investment in a particular SPAC or SPACs generally is appropriate for all investors. Celebrities, like anyone else, can be lured into participating in a risky investment or may be better able to sustain the risk of loss. It is never a good idea to invest in a SPAC just because someone famous sponsors or invests in it or says it is a good investment.

SPACs have become a popular vehicle for transitioning a private company to a publicly traded one. A SPAC is a blank check company with no operations that offers securities for cash through an initial public offering (IPO). SPACs then have a specified period of time—typically two years—to identify and merge with a private operating company. This business combination is often used as an alternative means of taking the acquired company public, rather than through a traditional IPO.

Special purpose acquisition companies (SPACs). To learn more about SPACs and what to consider before investing in a SPAC, see our Investor Bulletin about what you need to know.

However, SPAC transactions differ from traditional IPOs and have distinct risks associated with them. For example, sponsors may have conflicts of interest so their economic interests in the SPAC may differ from shareholders. Investors should carefully consider these risks. In addition, while SPACs often are structured similarly, each SPAC may have its own unique features, and it is important for investors to understand the specific features of any SPAC under consideration.

Differing economic interests. SPAC sponsors generally acquire equity in the SPAC at more favorable terms than investors in the IPO or subsequent investors on the open market. As a result, the sponsors will benefit more than investors from the SPAC’s completion of a business combination and may have an incentive to complete a transaction on terms that may be less favorable to you. To learn more, see our Investor Bulletin.

Even if a celebrity is involved in a SPAC, investing in one may not be a good idea for you. Before investing, always do your research, including these three steps:

- Check out the background, including registration or license status, of anyone recommending a SPAC, using the search tool on Investor.gov;

- Learn about the SPAC sponsors’ backgrounds, experience, and financial incentives, how the SPAC is structured, the securities that are being offered, the risks associated with an investment in the SPAC, plans for a business combination, and other shareholder rights by carefully reading any prospectus which may be available through the SEC’s EDGAR database; and

- Consider the investment’s potential costs, risks, and benefits in light of your own investment goals, risk tolerance, investment horizon, net worth, existing investments and assets, debt, and tax considerations.

Never invest in a SPAC based solely on a celebrity’s involvement or based solely on other information you receive through social media, investment newsletters, online advertisements, email, investment research websites, internet chat rooms, direct mail, newspapers, magazines, television, or radio.

* * *

Is this too little, too late for the SEC? After all, the SPAC craze has already reached a surreal, permanently high plateau where 5 new SPACs price ever single day so far in 2021, and that YTD, 144 SPACs have gone public raising a total of $44 billion.

Shut Up ‘n Play Yer Guitar

Last week I was sent a video clip of hard rock legend and former Deep Purple and Rainbow guitarist Ritchie Blackmore giving an interview with the ‘cool cats’ of Russia Today. Resplendently syrup-ed, his monologue to a politely nodding interviewer flowed thus:

“We all have to look within. I think a lot about death. More than life. Because we are going towards death. And I think death is very important. I think it’s going to happen to all of us. Most of us. Not all. Some of us might get away with it. It’s what Bob Dylan said. Bob Dylan came up to me once and he said: ‘Hey – who the hell are you?’. And I kind of admired him for that.”

Pure Spinal Tap! My point today is yet again that much of what we read and see in terms of geopolitical and market analysis can sound deep – but it’s nonsense wrapped around elements of the painfully obvious.

Chinese stocks slumped again because the PBOC introduced a policy that *must*, if followed, induce a huge slowdown in future economic activity – or “pulling back stimulus gradually”, as Bloomberg describes shifting liquidity growth of 35% y/y to 8-9%. Then the same stocks went up because ‘the National Team bought them’. So what the economy and asset prices do are to remain two unrelated factors entirely: because it’s one thing not to have enough fiscal stimulus, and hence low rates, and hence high equity multiples; but China is going to *delever* its bubbles and ensure they don’t burst. Good luck with that.

Another narrative not being discussed: the underlying signal that the US and China seem incapable of *both* managing to put their foot on the fiscal accelerator at the same time. Up until now it’s been all China: now it’s going to be all the US. (Chinese CPI and PPI today saw the former rise from -0.3% to -0.2% y/y and the latter jump from 0.3% to 1.7%: so input prices are rising and sales prices are falling – time to scale back borrowing? US CPI is out later today.)

That lack of willingness to coordinate, or perhaps ability given the problems if 50% of world GDP stimulates in tandem(?), has serious implications for markets and geopolitics. Instead, we get the press ‘scoop’ that China wants to meet with the US in Alaska to “reset relations”: perhaps because someone from the White House can see China from there?

Take off the syrup, and ask from which of the two possible sides this story came; and who would want the narrative out there; and to what end. Journalists, like the Russian who sat listening to Ritchie Blackmore pontificate about evading death, seem to have lost that art: but the RT/RB example was no more ridiculous than the New York Times salivating about ‘secret’ US plans to attack Russian cyber facilities. So secret it’s a good job no Russians can read the US press and find out about them there: Эти жалкие одноязычные русские шпионы!

But back to Anchorage and its handy view of China: is a relations reset compatible with the same Bloomberg coverage today(!) talking about China firing an anti-aircraft carrier missile in the South China Sea to send “an unmistakable message”, according to a top US admiral testifying in Congress? With the 6.8% y/y increase in Chinese defence spending? With Xi Jinping telling the PLA to “be prepared to respond in uncertain times”? With recent hawkish statements made by Secretary of State Blinken? With plans from both the US and China for tech supremacy? Or with building up a foreign policy “Quad”, which continues apace?

Perhaps, yes: as a necessary de-escalation, some might say; and look at what is happening with the US and Iran despite what Iranian-backed actors are doing in the region, others would add. However, good luck getting anything past Congress.

Now back to the fiscal: the US is going one way and China the other – what does that tell us about how well the globe can handle any real Building Back Better? Is US fiscal stimulus going to buy Chinese green goods, which they will have too many of for local demand if their own economy is slowing down? How do we manage the relationship between these two as at least partial decoupling becomes a domestic political priority? We need Bob Dylan-style questioning here. But expect lots of Russia Today style nodding, or Spinal Tap analysis instead.

Meanwhile, from the big picture to the small, and despite the USD having a down day for the most part vs. G10 FX Tuesday, the meme is still rapidly shifting to “America is back” in terms of higher long-end rates, and hence a bid for the buck against emerging markets in particular. Moreover, the OECD has just released their updated global GDP forecast in which they see world growth 1% higher than previously seen, and the US bouncing to 6.5% in 2021 – though Europe will lag behind yet again: who can VDL blame for that one? Well, we had a few months of Spinal Tap dollar bearishness at least – even if higher yields pushing the USD up are themselves Tap-py.

Recall the great line from Tap bassist Derek Smalls (who looks the spitting image of Blackmore today): “We’re very lucky in the band in that we have two visionaries, David and Nigel, they’re like poets, like Shelley and Byron. They’re two distinct types of visionaries, it’s like fire and ice, basically. I feel my role in the band is to be somewhere in the middle of that, kind of like lukewarm water.” There is no such middle role in a K-shaped US economy, where fiscal stimulus is too much for some and not enough for others: so yields will shoot up and ultimately crash down again, and the USD will likely do the same – unless and until we get Fed yield curve control that is. Watch those stage pyrotechnics play out in awe.

The very small(s) picture is of the RBA belatedly reminding markets it might be able to set up a committee to include ‘whatever it takes’ on the agenda, but it will require a qualified majority vote that then goes to a special commission for review in a plenary session. In short, Governor Lowe verbally defended the yield curve control policy and reminded us he isn’t about to raise rates. This worked in regards to the 3-year: but on an underlying level arguably because parts of the global market can still react to what the PBOC said it is going to do. At least Lowe can be happy about what AUD has been doing, yesterday aside: but again that’s about what the US government says it’s going to do, not the RBA.

As Frank Zappa would have put it: Shut Up ‘n Play Yer Guitar. (An album whose tracks include “Five-five-FIVE”; “Hog Heaven”, “Treacherous Cretins”, and “Soup ‘n old clothes”, all of which sound like potential Bloomberg, Russia Today, or New York Times headlines.)

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair