Stocks & Equities

The latest monetary easing by the European Central Bank (ECB) and Federal Reserve has given financial markets on both sides of the Atlantic a positive lift. But the global cheer did not extend to China as stocks in Shanghai continue to slide.

In fact, many emerging stock markets have been under-performing, as I pointed out in a previous Money and Markets column. And the trend hasn’t improved much for some, including China, in spite of a pickup in global capital flows into the region.

But all emerging markets are not created equal. While some are high-profile laggards, others are beginning to outperform.

This highlights the fact that not all emerging markets are moving up or down together these days. It also underscores the importance of doing your homework to uncover the hidden opportunities in emerging markets.

[Editor’s note: To help you uncover these opportunities, Mike has a FREE special report where he gives you his five tried-and-true rules for global ETF trading. Click here to read it now.]

China: No Sign of a Bottom Yet

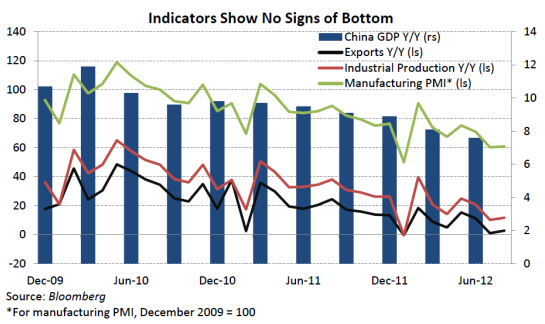

China, the emerging market poster-child, has continued to underperform almost all major global stock markets in 2012. The Shanghai Composite index is now down 36 percent from its 2009 peak — a period in which the S&P 500 Index soared 44 percent.

The reason: China suffers from self-inflicted economic wounds. Its past reliance on an export-led growth model was fine … when the global economy was going strong. But as you can see in the chart below, China’s trade volumes are shrinking, and the global economy is forecast to expand just 2.1 percent in 2012.

Years of over-investment in China has led to a glut of unused industrial capacity and a real estate bubble, souring investor confidence. On top of that, according to the World Trade Organization (WTO), global trade volume expanded just 5 percent last year, down from 13.8 percent in 2010, and is expected to slow further to just 3.7 percent this year.

The result: China’s industrial output growth in August fell to the lowest level in three years. The People’s Bank of China is cutting interest rates, the same as many other central banks around the world. But investors worry that further easing may only inflate property values without doing much for the real economy … that sounds familiar.

Unfortunately, there is not much evidence pointing to a turnaround for China’s economy anytime soon.

Some Good News in

Select Emerging Markets

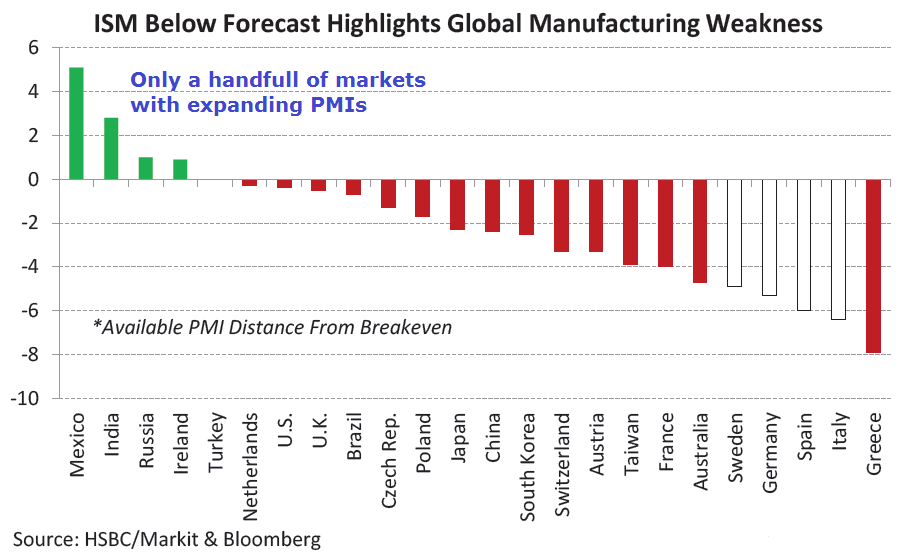

Of course China is certainly not alone in experiencing a manufacturing slowdown as a result of the downshift in global growth — it’s just more apparent for their export-led economy.

A recent survey of global manufacturing purchasing managers index (PMI) readings by Bloomberg finds 20 out of 24 countries are showing contraction in their manufacturing sector. The countries that still have expanding PMI’s include: Mexico, India, Russia, and Ireland.

India, for example, is much less reliant on export growth than its neighbor China. And its economy should expand 6 percent this year — certainly in the top-tier among global GDP growth. Global investors have noticed …

Net equity inflows from foreign investors have surged $12.5 billion so far this year, equal to 10.9 percent of India’s total stock market value.

It’s no surprise that India’s stock market has been one of the better emerging market performers … up nearly 20 percent year-to-date and tops among the big-four BRIC markets.

The Bright Spot in Europe

In Europe, where many stock markets, both emerging and developed, have been crushed this year by the European debt crisis, Russia has been a bright spot with its equity market up 12 percent this year. Granted, its economy remains closely linked with commodity prices, particularly energy. But Russia’s economy should grow 3.7 percent this year.

And Russia’s recent entry into the WTO could provide the same kind of boost to its economy as it did for China over a decade ago. Plus, Russian stocks are among the world’s biggest bargains, trading at less than six times earnings today.

Bottom line: Despite the ongoing and high profile underperformance of markets like China, not all emerging markets are lagging, and several are beginning to take the lead in performance. That’s why global investors must differentiate between the fundamentals of each market — evaluating them one country at a time.

Good investing,

Mike Burnick

About Money and Markets

For more information and archived issues, visit http://www.moneyandmarkets.com

Money and Markets is a free daily investment newsletter published by Weiss Research, Inc. This publication does not provide individual, customized investment or trading advice. All information is based upon data whose accuracy is deemed reliable, but not guaranteed. Performance returns cited are derived from our best estimates, but hypothetical as we do not track actual prices of customer purchases and sales. We cannot guarantee the accuracy of third party advertisements or sponsors, and these ads do not necessarily express the viewpoints of Money and Markets or its editors.

Mac Slavo: If you think the Federal Reserve’s quantitative easing will only affect the U.S. dollar, think again. Now that the United

Moreover, because everyone is joining the fray, all of that extra money will make its way into key resource stocks and commodities, adding further upside price pressure to essential goods like food and fuel.

It’s a race to the bottom, and the losers are the 99.9% of us who aren’t being kept in the loop.

Quantitative easing is really another word for currency wars. A weak U.S. currency puts continued pressure on the Japanese Yen, the Chinese Yuan, the South Korean Won, the Australian dollar and other currencies.

Cheap money also fuels speculation and this money quickly drifts into commodity markets and the ETFs that help propel commodity market speculation. This is inflationary for food prices.

The lower the U.S. dollar the greater the intensity of currency wars.The break below the key uptrend line on the Dollar Index chart was an early warning of the third round of quantitative easing (QE3).

The most important question now is to use the chart to examine the potential downside limits of a QE3 weakened U.S. dollar.

The weekly close below this uptrend line was the first signal of a major change in the trend direction. It came before the announcement of QE3, last week.

The third significant feature is historical support near 74.5. This is the upper edge of a consolidation band between 73.5 and 74.5. This is the downside target for the Dollar Index following a fall below 79.

This target can be reached very rapidly over three to four weeks. A rapid collapse of the U.S. dollar puts immediate pressure on other dollar-linked currencies.

There is a very low probability the U.S. dollar will resume its uptrend. The move below the value of the uptrend line and a fall below 79 confirm thata new downtrend has developed.

The weakness in the U.S. Dollar will hurt export dependent economies and companies.

There are two ways this may end – neither of which is going to be good for the average Joe:

- The Fed et. al. continue to print, so much so that prices for food, gas, utilities and other key commodities that are linked to US dollar movements will rise exponentially. This rise in prices will accelerate the pressure on consumers as more jobs are lost in an ever progressing, self reinforcing economic death spiral. The pressure of rising prices, even though the Dow Jones may reach 20,000 or 50,000 points, will be so great that American consumers simply won’t be able to pay their bills or put food on the table.

- The Fed and their brethren around the world won’t be able to print fast enough to maintain stable financial markets, leading to stock market crashes in Europe, Japan, China and the United States, which then leads to a shift of capital to US Treasury bonds, ironically strengthening the dollar. A weak US economy that isn’t creating jobs and is adding tens of thousands of people to an already overburdened social safety net every week will eventually lead to confidence being lost in the US government’s ability to repay its debts. As we noted in 2012 Predictions of a Mad Tin Foilist, the end result will be a currency crisis, or de facto default by way of hyperinflating away our debt.

Both scenarios are virtually the same, as both will end with complete and utter destruction of Americans’ wealth.

Despite the mainstream notion that inflation is under control and most of the money is sitting on the sidelines with banks, all we need to do is look at the price increases for consumers since private and public bailouts begin in late 2008. Gas has doubled. Food is up over 25%. Electricity costs and the cost of just about every other non-debt based asset has steadily risen.

This is not going to stop.

While timelines remain elusive because of never ending government intervention into financial markets and economies, the policies being instituted by central banks around the world can only lead to continued degradation of paper currencies and the rise in prices of all goods linked to those currencies.

In January of 2010 we suggested a strategy of buying physical commodities at today’s lower prices and consuming those commodities at tomorrow’s higher prices. The trend for fiat paper money and physical assets has not changed and is, in fact, more pronounced now than ever before.

The US dollar is being systematically weakened until it no longer exists as a viable means of exchange. When this happens you’d better be prepared to operate in a society where traditional money is replaced with mechanisms of exchange like precious metals, food, critical supplies and production skills.

You can begin taking simple steps to prepare now. The collapse of the existing global paradigm is accelerating and if you’re not ready for it the price you’ll pay will be severe.

Related Tickers: SPDR Gold Trust (NYSEARCA:GLD), iShares Silver Trust (NYSEARCA:SLV), Ultra Silver

Quotable

From February 2010:

“Shorting Treasuries is a ‘no brainer…every single human being should have that trade.’”

Nassim Taleb

LOL…hoisted on the horns of a Black Swan petard were you Mr. Taleb?

Commentary & Analysis

Guru Follies

The newsletter crowd, to which I plead guilty, loves to tell you scary stories that often seem to be missing an important element—facts. Let’s take a short stroll down memory lane and review the latest stories from the gurus.

1. Always a favorite, the US dollar is going to get killed. This one is back on the front burner thanks to QE3. Of course, the fact that the dollar didn’t get killed by QE1 or QE2 seems not to matter. It is QE3 that will surely do the dirty deed this time. The newsletter gurus seem to lose sight of one very important axiom of price, it is this: If supply increases, but demand for the increased supply increases even more, price doesn’t collapse; it tends to rise (cateris paribus). The demand for dollar liquidity in a world where the European banking system is desperately deleveraging and many in the private world are doing the same likely means the world reserve currency remains supported.

2. Inflation will soar. This is one of my favorites, as the newsletter crowd remains stark-raving loony over this one despite the facts. After all, this inflation call is simple…more money means more inflation. Slam dunk! But we haven’t seen inflation as defined by the newsletter crowd. We have seen some commodity prices surge on investment liquidity and supply problems, granted. As I have shared with you many times before, if money doesn’t make it into the real economy to be used by real people to bid up the prices of real goods, it isn’t inflation in the normal sense we think of when we say “inflation.” But if we say there has been a massive inflation in financial assets; that would make sense. That’s because much of the money the Fed has created has leaked into financial assets. We can say there has been asset inflation driven by the financial economy. We can say that overall there has been a decline in the purchasing power of global fiat currencies as we view the price of gold. But this is different and more easily deflated.

3. There is a massive bond bubble out there just waiting to pop. I believe we are on our third fear-mongering bond bubble theme since QE started…it could be more, I really have lost track of this favorite scare story. And of course with QE3 fresh in the minds of newsletter buyers, this bubble story is hot again. The flimsy logic behind a bond bubble is the idea that money has moved into bonds irrationally, for some speculative gains and all these investors just don’t understand that hyper-inflation is just around the corner. And if you hold US bonds, you are really in trouble because QE3 is the straw that has broken the greenback’s back and that will add to the pain for bonds. Let us consider some real reasons why bonds are loved and why they could remain loved for a very long time: a. Global demographics – As people get older their portfolio tends to shift toward what they perceive is less volatile and more safe investments such as fixed income.

b. Secular change in consumption patterns – The credit crunch really was a sea change I think. Massive personal balance sheet overleverage, coupled with the decline in the biggest personal asset—real estate—seems to have triggered a sea change in both real consumption and attitude toward future consumption. This means more savings. More savings tends to mean more money in fixed income net…net.

i. The knock-on effect of a change in global consumption/increased savings is the catalyst for rebalancing the current account deficit nations with the current account surplus nations. It is especially bad news for those with export-dominated growth models who will take the brunt of the adjustment domestically…and we know who you are: China, Germany, and Japan…

c. Massive global debt levels equals below capacity future growth. Below capacity future growth will tend to push down the expected return from growth assets—stocks—relative to fixed income. And slower growth is usually accompanied by lower future inflation expectations. And lower future inflation expectations are usually discounted into the current yield for fixed income. Thus, bonds will tend to remain supported.

d. Risk bid. If I am right that the Eurozone crisis is far from over, and that China will likely experience either a hard landing or lead to a major negative growth surprise, the idea of a major risk bid of global money running for safe haven is still a high probability. And safe haven money flows into…you guessed it…fixed income.

e. Historical parallels. This from Hoisington Research, a fixed income investment management firm based in Houston who has been more right on bonds and interest rates for the last five years than anyone I have seen….

“Long-term Treasury bond yields are an excellent barometer of economic activity. If business conditions are better than normal and improving, exerting upward pressure on inflation, long-term interest rates will be high and rising. In contrary situations, long yields are likely to be low and falling. Also, if debt is elevated relative to GDP, and a rising portion of this debt is utilized for either counterproductive or unproductive investments, then long-term Treasury bond yields should be depressed since an environment of poor aggregate demand would exist. Importantly, both low long rates and the stagnant economic growth are symptoms of the excessive indebtedness and/or low quality debt usage.”

We know that debt levels in the industrialized world are in the ozone and still rising. Now take a look at what yields did historically during three similar crisis periods—Japan 1989, United States 1873, and United States 1929–when debt levels were much lower globally than they are now.

Back to Hoisington:

“In the aftermath of all these debt-induced panics, long-term Treasury bond yields declined, respectively, from 3.5%, 3.6% and 5.5 % to the extremely low levels of 2% or less in all three cases (Chart above). The average low in interest rates in these cases occurred almost fourteen years after their respective panic years with an average of 2% (Table below). The dispersion around the average was small, with the time after the panic year ranging between twelve years and sixteen years. The low in bond yields was between 1.6% and 2.1%, on an average yearly basis. Amazingly, twenty years after each of these panic years, long-term yields were still very depressed, with the average yield of just 2.5%. Thus, all these episodes, including Japan’s, produced highly similar and long lasting interest rate patterns. The two U.S. situations occurred in far different times with vastly different structures than exist in today’s economy. One episode occurred under the Fed’s guidance and the other before the Fed was created. Sadly, there is no evidence that suggests controlling excessive indebtedness worked better with, than without, the Fed. The relevant point to take from this analysis is that U.S. economic conditions beginning in 2008 were caused by the same conditions that existed in these above mentioned panic years. Therefore, history suggests that over-indebtedness and its resultant slowing of economic activity supports the proposition that a prolonged move to very depressed levels of long-term government yields is probable.”

Now, you may want to sell this bond market here based on the view it is a bubble. But before you do, let me share an anecdote. I remember it vividly. The recently deceased renowned global strategist, Barton Biggs, who spent most of his years toiling away at Morgan Stanley and was a rock-star when global strategists played those roles, made a bond bubble call back in the mid-1990’s. He said that shorting the Japanese government bond market was the “trade of a lifetime.” Well, maybe. Unfortunately Mr. Biggs didn’t live long enough to see that trade work out.

Webinar Announcement: I edit two currency trading newsletters for Weiss Research. I am doing a free webinar on Thursday, September 20th, at 12:00 p.m. ET, covering key global macro themes and my view on the direction of the dollar and other major pairs as we head into 2013. I invite you to attend and encourage your questions during the event.

The webinar is free. All we ask is that you seriously consider becoming a Member of one of our services offered by Weiss Research.

Please click here to register.

Thank you.

Jack Crooks

Black Swan

www.blackswantrading.com

Ed Note: The Godfather of newsletter writers, Richard Russell, had some absolutely extraordinary thoughts about life, the markets and gold. Here is what Russell had to say: “Most of the people in the world suffer from fear, anxiety, anger, guilt, bitterness, resentment, sorrow, depression, and various other emotions which can mar their lives. The majority of these emotions are holdovers from damaged or traumatic infancies.”

“I was brought up in the early 1920s. In those days parents were taught by doctors to feed infants by the clock, not when the infant was famished and screaming with hunger. In those days, infants were not tended and comforted when they needed warmth and attention. They were often tended by nurses and allowed to “cry themselves out,” thus leaving parents with plenty of free time of their own.

I had damaged parents, which affected me very negatively. My mother’s mother died in childbirth when my mom was two years old. So my mom grew up without a mother, and as a result, she knew nothing about mothering. My father’s father (my grandfather) committed suicide when my dad was 8 years old. As a result, my poor father was anxious, fearful, and nervous all his life.

Unfortunately, I absorbed the fears and anxieties of my parents, who had done the best they could, based on what they knew at the time. I grew up during the Depression, believing or feeling that the world was a harsh and unsafe place. As a result, I think I developed an extreme sensitivity to danger in the world and in the stock market. Interestingly, I think I kept my subscribers OUT of every bear market since the 1950s.

Let me go a bit further into my family history. My grandfather owned the biggest jewelry store in Charleston. He killed himself when he lost all his money in the awful panic of late 1902.

My dad’s half-brother (my uncle Irving) jumped out of the window of a New York hotel when the stock market crashed in 1929. Irving had a lot of stock in the family-owned City Stores. Irv was a playboy, and he lived entirely off his dividends. When City Stores cut its dividend in 1929, it was too much for Irving — so he killed himself.

With that sordid history, it’s kind of ironic that I ended up writing about the stock market. Strange, indeed, or is it?

December gold closed yesterday at 1770.60. If I was in GLD, I’d be fretting. But if I was solely in bullion coins, I wouldn’t give gold’s action a second thought. The reason I say this is because buying GLD is a trade, and holding gold coins is a move that theoretically is forever. For instance, if I had GLD, at some point I’d sell it, and hopefully show a profit.

But I don’t know when I’d ever sell the bullion coins. Sell them for what? For Fed-created fiat paper? Actually, I’d probably gift the coins to my kids, on the basis that it would be an easy transfer of wealth, much as some women gift their diamond engagement rings to their daughters.

Below is the US dollar as per yesterday’s close. The dollar has broken below both MAs, and is sitting on support, which is around 78 3/4. RSI shows the dollar over-sold, but MACD allows for a further decline. Thank the Fed’s massive money-creation project for this chart, but what the heck, a cheaper dollar helps our exports.

But a cheaper dollar is also inflationary. Marc Faber states that the Fed is destroying the world with its wild printing, and I can tell you that Mr. Faber is really angry.

Awhile back, the “surest” way to make money was to short the Euro. When too many traders get on one side of an item (in this case, the short side), this is what can happen. A strong Euro means a weak dollar, and a weak dollar translates into higher gold. But we must be careful, because the Euro is in the overbought zone of RSI, and a lot of its strength may be coming from short covering.

INTERESTED IN SUBSCRIBING? GO HERE

Russell began publishing Dow Theory Letters in 1958, and he has been writing the Letters ever since (never once having skipped a Letter). Dow Theory Letters is the oldest service continuously written by one person in the business.

Russell gained wide recognition via a series of over 30 Dow Theory and technical articles that he wrote for Barron’s during the late-’50s through the ’90s. Through Barron’s and via word of mouth, he gained a wide following. Russell was the first (in 1960) to recommend gold stocks. He called the top of the 1949-’66 bull market. And almost to the day he called the bottom of the great 1972-’74 bear market, and the beginning of the great bull market which started in December 1974.

The Letters, published every three weeks, cover the US stock market, foreign markets, bonds, precious metals, commodities, economics –plus Russell’s widely-followed comments and observations and stock market philosophy.

In 1989 Russell took over Julian Snyder’s well-known advisory service, “International Moneyline”, a service which Mr. Synder ran from Switzerland. Then, in 1998 Russell took over the Zweig Forecast from famed market analyst, Martin Zweig. Russell has written articles and been quoted in such publications as Bloomberg magazine, Barron’s, Time, Newsweek, Money Magazine, the Wall Street Journal, the New York Times, Reuters, and others. Subscribers to Dow Theory Letters number over 12,000, hailing from all 50 states and dozens of overseas counties.

A native New Yorker (born in 1924) Russell has lived through depressions and booms, through good times and bad, through war and peace. He was educated at Rutgers and received his BA at NYU. Russell flew as a combat bombardier on B-25 Mitchell Bombers with the 12th Air Force during World War II.

One of the favorite features of the Letter is Russell’s daily Primary Trend Index (PTI), which is a proprietary index which has been included in the Letters since 1971. The PTI has been an amazingly accurate and useful guide to the trend of the market, and it often actually differs with Russell’s opinions. But Russell always defers to his PTI. Says Russell, “The PTI is a lot smarter than I am. It’s a great ego-deflator, as far as I’m concerned, and I’ve learned never to fight it.”

Letters are published and mailed every three weeks. We offer a TRIAL (two consecutive up-to-date issues) for $1.00 (same price that was originally charged in 1958). Trials, please one time only. Mail your $1.00 check to: Dow Theory Letters, PO Box 1759, La Jolla, CA 92038 (annual cost of a subscription is $300, tax deductible if ordered through your business).

IMPORTANT: As an added plus for subscribers, the latest Primary Trend Index (PTI) figure for the day will be posted on our web site — posting will take place a few hours after the close of the market. Also included will be Russell’s comments and observations on the day’s action along with critical market data. Each subscriber will be issued a private user name and password for entrance to the members area of the website.

Investors Intelligence is the organization that monitors almost ALL market letters and then releases their widely-followed “percentage of bullish or bearish advisory services.” This is what Investors Intelligence says about Richard Russell’s Dow Theory Letters: “Richard Russell is by far the most interesting writer of all the services we get.” Feb. 19, 1999.

Below are two of the most widely read articles published by Dow Theory Letters over the past 40 years. Request for these pieces have been received from dozens of organizations. Click on the titles to read the articles.

“Rich Man, Poor Man (The Power of Compounding)“

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair