Bonds & Interest Rates

Most of you reading this expect inflation in the years ahead, right? Well, I don’t. In fact, I am firmly in the deflation camp.

Just think about it. What has happened after every major

We got deflation in prices… every time.

This time around, with the latest bubble peaking in 2007/08, the outcome will be exactly the same. There is deflation ahead. Expect it. Prepare for it.

But the bubble-bust cycle that history has allowed us to see is not the only reason I’m so certain we’re heading for deflation and a great crash ahead. I have other, irrefutable evidence…

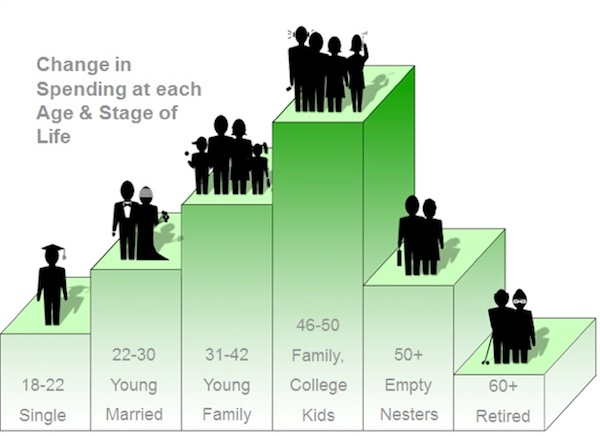

For one, there is the most powerful economic force on Earth: demographics. More specifically, the power of the number 46. You see, that’s the age at which the average household peaks in spending.

When the average kid is born, the average parent is 28. They buy their first home when they’re 31… after they had those kids. When the kids age into nasty teenagers, the parents buy a bigger house so they can have space. They do this between the ages of 37 and 42. Their mortgage debt peaks at age 41. And like I said, their spending peaks at around 46.

From cradle to grave, people do predictable things… and we can see these trends clearly in different sectors of our economy, from housing to investing, borrowing and spending, decades in advance.

This demographic cycle made the crash in the ’30s and the slowdown in the ’70s unavoidable. Now it is happening again… with the biggest generation in history – the Baby Boomers.

Consumer spending makes up more than two-thirds of our gross domestic product (GDP). So knowing when people are going to spend more or less is an incredibly powerful tool to have. It tells you, with uncanny accuracy, when economies will grow or slow.

Why Deflation Is the Endgame

Think of it this way: the government is hellbent on inflating. It’s doing so by creating debt through its quantitative easing programs (just for starters). But what’s the private sector doing? It’s deflating.

And the private sector is definitely the elephant in the room. How much private debt did we have at the top of the bubble? $42 trillion. How much public debt did we have back then? $14 trillion.

That looks like a no-brainer to me. Private outweighs public three to one. And the private sector is deleveraging as fast as it can, just like what happened in the 1870s and 1930s. History shows us that the private sector always ends up winning the inflation-deflation fight.

Now, I will concede that this is an unprecedented time. Today governments around the world have both the tools and the determination to fight deflation. And they are desperate to keep it at bay because they know how nasty it is (they, too, are students of history).

How bad is it? Think of deflation like what your body would do with bad sushi. It would flush it out as fast as possible. That’s what our system is trying to do with all the debt we accumulated during the boom years. It’s what the system did in the 1930s. Back then we went from almost 200% debt-to-GDP to just 50% in three years. It hurt like hell. The government doesn’t want this painful deleveraging.

The problem is, the longer the government tries to fight this bad sushi, the sicklier the system becomes. I know this because it’s what happened to Japan…

Japan’s bubble peaked in the ’80s. When the unavoidable deleveraging process began, the country did everything in its power to stop it. How is Japan doing today, 20 years after its crash? It is still at rock bottom. Its stock market is still down 75%.

Japan has gone through everything we’ll go through in the next few years. Does Japan have an inflation problem? That’s a rhetorical question. Did its central bank stimulate frantically? Also a rhetorical question.

Think of it another way: what is the biggest single cost of living today? Is it gold? Oil? Food? It’s none of these. It is housing. And what is housing doing? Dropping like a rock. It can’t muster a bounce, despite the lowest mortgage rates in history and the strongest stimulus programs anywhere… ever.

The Fed is fighting deflation purposely. It will fail.

Why the Fed Will Fail in All Its Efforts

There is simply no way the Fed can win the battle it’s currently waging against deflation, because there are 76 million Baby Boomers who increasingly want to save, not spend. Old people don’t buy houses!

At the top of the housing boom in recent years, we had the typical upper-middle-class family living in a 4,000-square-foot McMansion. About ten years from now, what will they do? They’ll downsize to a 2,000-square-foot townhouse. What do they need all those bedrooms for? The kids are gone. They don’t visit anymore. Ten years after that, where are they? They’re in 200-square-foot nursing home. Ten years later, where are they? They’re in a 20-square-foot grave plot.

That’s the future of real estate. That’s why real estate has not bounced in Japan after 21 years. That’s why it won’t bounce here in the US either. For every young couple that gets married, has babies, and buys a house, there’s an older couple moving into a nursing home or dying.

I watch this same demographic force move through and affect every other sector of the economy. The tool I use to do so is my Spending Wave. This is a 46-year leading indicator with a predictable peak in spending of the average household.

Here’s how it works: the red background in the chart above is the Dow, adjusted for inflation. The blue line is the spending wave, including immigration-adjusted births and lagged by 46 years to indicate peak spending. If you ask me, that correlation is striking.

The Baby Boom birth index above started to rise in 1937. It continued to rise until 1961 before it fell. Add 46 to 1937, and you get a boom that starts in 1983. Add 46 to 61, and you get a boom that ends in 2007.

Today demographics matters more than ever because of the 76 million Baby Boomers moving through the economy. That’s why I don’t watch governments until they start reacting in desperation. Then I adjust my forecasts accordingly.

Don’t Hold Your Breath for the Echo Boomer Generation

But all this talk about Baby Boomers inevitably births the question: “Surely the Echo Boom generation is coming up right behind their parents. They’ll fill the holes, right?”

Let me make this clear. If I hear one more nutcase on CNBC say, “The Echo Boom generation is bigger than the Baby Boom,” I might go ballistic. They are wrong. The Echo Boomer generation is NOT bigger than the Baby Boom generation. In fact, it’s the first generation in history that’s not larger than its predecessor is, even when accounting for immigrants.

It’s not all doom and gloom, though. We will see another boom around 2020-23. But for now, all the Western countries will slow, thanks to the downward demographic trend sweeping the world. Some are slowing faster than others are. For example, Japan is slowing the fastest (it actually committed demographic kamikaze, but that’s a discussion for another day). Southern Europe is next along in its decline. Eastern Europe, Russia, and Asia are following quickly behind.

Which brings me back to my point: there is no threat of serious inflation ahead. Rather, deflation is the order of the day. The Fed thinks it can prevent a crash by getting people to spend. To that I say, “Good luck.” Old people don’t spend money. They bribe the grandkids, and they go on cruises where they just stuff themselves with food and booze.

Do you know how to tell if you’re buying a car from an older person? It’s going to be ten years old and have only 40,000 miles on it. They drive 4,000 miles a year. They just go down the street to get a Starbucks coffee and a newspaper. Then they go back home. How do you know you’re buying a car from a soccer mom? It’s driven 20,000 miles a year, carting the kids around all day… to school, soccer practice, whatever. This is the power of demographics.

So let me tell you what causes inflation. It’s young people. Young people cause inflation. They cost everything and produce nothing. That’s inflation in people terms.

Why did we have high inflation in the ’70s? Because Baby Boomers were in school, drinking, spending their parents’ money. While this was going on, we experienced the lowest-productivity decade in the last century.

Do you remember the 1970s? We had worsening recessions as the old Bob Hope generation began to save more while the Baby Boomers entered the economy en masse… at great expense. It costs a lot of money to incorporate young people, raise them, and put them into the workforce.

Then suddenly, in the early ’80s, like some political genius did something brilliant, the economy started growing like crazy, and inflation fell. You know what that was? That was the largest generation in history transitioning en masse from being expensive, rebellious, young people to highly productive yuppies with young new families. It was the move from cocaine to Rogaine.

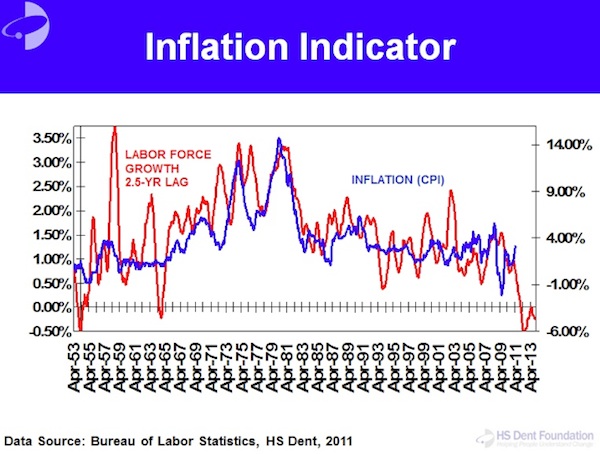

The correlation between labor force growth and inflation is crystal clear…

When lots of young people come into the labor force, it’s inflationary. When lots of old people move out of the labor force and into retirement, it’s deflationary. Right now, where is the highest inflation in the world? It’s in emerging countries. Do they have more old people or young people? They have more young people.

We saw it in the 1970s, we see it in emerging markets, and we’ll see it ahead as the Baby Boomers head off into the sunset. First, there was inflation. Ahead is deflation. No doubt about it.

Harry Dent, the editor of Boom & Bust, has put together a free report for John Mauldin’s readers, called: Survive and Prosper in This Winter Season: Take These Steps Now… Before Dow 3,300 Arrives. You can access this free report by clicking on this link:http://www.boomandbustinvestor.com/reports/current/BoomandBustInvestor_WinterSeason.pdf

While we have written about Silver here and there, we have not covered it publicly in over a year. The market made an obvious cyclical top last spring and the tremendous gains from late 2008 into 2011 would need to be corrected and digested. From May to July the market tested its lows successfully and formed support. The recent advance confirmed the lows and confirms that we are likely in a new cyclical bull market. Based on the technicals, Silver and silver stocks continue to show tremendous long-term potential.

Below is a chart of our growth producer index which features 10 growth-oriented producers and is weighted somewhat by market capitalization. The market had a rip-roaring advance which lasted a total of 27 months. The correction lasted about 14 months (a 50% time retracement) and retraced about 50% in price. As you can see from the circles, the low occurred in May and was retested multiple times over the summer.

The long-term technical outlook for silver producers is potentially nothing short of super bullish. We say potentially because nothing is certain in this business. The market has formed a textbook cup and handle pattern. Note that the beginning of the handle is higher than the start of the cup. In other words, this shows more strength than a typical pattern in which those two points are equal or in which the start of the handle is lower than the start of the cup.

Moreover, we can visually see that the correction in a long-term sense was relatively mild. Mathematically speaking it was dramatic (about 50% in percentage terms) but much less dramatic than 2007-2008 (90%) and less dramatic than 2004 (60%). A smaller correction can be a sign of a market building internal strength for the next impulsive advance.

The super bullish outcome would be driven by Silver making a run at and eventually surpassing $50/oz. The equities are closer to their all-time highs and will likely break to new highs before Silver clears $50/oz. Certainly, the “super bullish outcome” is predicated on Silver breaking through $50/oz.

We know a few things. First, we are in a new cyclical bull market. Second, we are moving closer to the beginning of the bubble phase in this bull market. Third, in a bull move, Silver acts like Gold on steroids. It’s clear from the charts that Silver and silver stocks are in position for a potentially spectacular move over the next three to five years. We believe that the silver stocks can break to new highs in the next 12 months and that Silver won’t be far behind. The bubble phase is certainly several years away but these charts illustrate the potential for massive breakouts which would generate the momentum that leads into a bubble.

In the meantime, Silver and the silver stocks have rebounded strongly. Similar to the gold stocks, we see an upcoming pause or pullback in silver stocks over the next month. October is typically a weak month. Many stocks have rebounded substantially and with strong momentum. A pause or correction in October stands between gold and silver miners and a retest of old highs in the winter. A correction would also mark a great buying opportunity ahead of much higher prices. If you’d be interested in professional guidance in uncovering the producers and explorers poised to outperform then we invite you to learn more about our service.

Good Luck!

Jordan Roy-Byrne, CMT

Jordan@TheDailyGold.com

Crude oil prices hit a four-month high this week on the back of rising tensions in the Middle East and North Africa and the unfortunate murder of the U.S. ambassador to Libya. Added impetus on the upside was given to oil by the announcement of more money printing (QE3) by the Federal Reserve which said it would launch an open-ended commitment to purchase $40 billion of mortgage-backed securities monthly. The global benchmark for oil, Brent crude oil, jumped to about $117 a barrel. It maintained its roughly $18 premium to U.S.-based WTI crude oil which was trading at $100 a barrel on a couple days ago. Non-futures investors can easily participate in the oil market through the use of exchange traded funds. The ETF which tracks Brent crude oil futures is the United States Brent Oil Fund (NYSE: BNO) and the ETF which tracks WTI crude oil futures is the United States Oil Fund(NYSE: USO). The real story behind the story in the oil market, however, is the ongoing Arab Spring which is sweeping throughout the Middle East and North Africa, pushing aside some regimes and threatening others. The countries whose governments, such as Saudi Arabia and the other Gulf states, feel threatened by popular uprisings are where investors should put their focus. Saudi Arabia in particular is key because it accounts for more three-quarters of the world’s spare oil production capacity. So it is very important to note that the kingdom is no longer a price ‘dove’ in OPEC as it has been for decades. It has joined Iran, Venezuela and others in being a price ‘hawk’. The reason behind the change in attitude is simple…Arab Spring. Like its neighbors in the Gulf region, Saudi Arabia has gone on a public spending spree to appease its restless citizens. It has sharply increased outlays on subsidies for items like food, fuel and housing in an attempt to appease its citizens. In 2011, the kingdom raised its domestic spending by $129 billion – the equivalent of more than half its oil revenues. Much of this increased spending will go toward upgrading the country’s infrastructure. Take electricity, for example. Saudi Arabia has revealed plans to spend more than $100 billion dollars on power plants and distribution networks by 2020. The kingdom has also set a goal to electrify 500,000 new homes that are being built in an attempt to mollify political unrest among its population of 27 million people. This spending spree led the International Monetary Fund and other analysts to estimate that the kingdom and other Gulf countries need oil to be selling between $80 and $85 a barrel in order for the governments to balance their budgets. This is up, in Saudi Arabia’s case, from a mere $25 a barrel a few short years ago! Unfortunately for oil consumers, this trend looks set to continue in years ahead. According to the Institute of International Finance, by 2015 the Saudi government will only be able to balance its budget if oil prices are at $115 a barrel if current spending trends remain in place. So in effect, with the Arab Spring forcing governments to spend more on their citizens, it has put a floor under the price of oil. OPEC will do everything in its power to keep the price above the budget breakeven points for governments in the Gulf region. Keep up to speed on the oil and precious metals markets with my free newsletter: www.GoldAndOilGuy.com Chris Vermeulen

If legendary investor Jim Rogers is right, not only is Recession 2013unavoidable, it’s going to be a doozy.

In recent interviews, Rogers has been predicting a 2013 recession, bowled over by a potential blowout in Europe and unsustainable spending by the US government.

“Be very worried about 2013 and be very worried about 2014, because that’s when the next slowdown comes,” Rogers told Reuters.

And while Rogers sees no true safe havens out there, a few investments can provide some comfort – specifically, commodities in the form of agriculture, gold, and silver.

Rogers’ statements usually get lots of attention, mainly because he has an uncanny tendency to be right.

Together with George Soros, he founded the Quantum Fund in the 1970s and posted returns of 4,200% over 10 years. Rogers retired in 1980 at the age of 37, but remains active as a private investor.

Back in 1999, Rogers recommended gold when it was trading at $252 and silver at $4.

We all know what happened after that.

Here’s the Jim Rogers take on the economy and how to survive Recession 2013.

Elections Will End Good Times

Rogers sees the coming elections as the end of a joy ride for both Europe and the United States.

“President Obama wants to get reelected. German Chancellor Angela Merkel wants to get reelected,” Rogers said. That means they’ll both be spending lots of public money to keep voters happy until the elections are over.

The ECB’s controversial decision to purchase unlimited quantities of bonds from struggling Eurozone members indicates Merkel is ready to pull out all the stops to save the euro – and her job.

In fact, Merkel has made a sharp about face and now wants to stop Athens from leaving the euro zone at all costs.

“For [Merkel], it is essential to avoid the consequences of a Grexit before national elections next year,” influential German news magazine Der Spiegel said recently.

But the EU rescue will “absolutely not” work, Rogers says. He expects the Greeks to be the first to exit the EU.

What’s more, Greece will be merely the first domino to fall.

“You have got countries that are essentially bankrupt. The solution to too much debt is not more. I suspect that the euro will not survive,” he said.

Eventually the entire EU may be restructured with a core group of countries like Finland, the Netherlands, and Austria joining Germany and perhaps France in a new monetary union.

…..read page 2 HERE

For all the analysis of the US ‘fiscal cliff’, eurozone sovereign debt crisis, Japan’s lost decades and China’s stalling economy, the biggest threat to global financial markets this autumn is the danger of a sudden strike on Iranian nuclear installations by Israel, most probably before the US presidential election.

The fear then is that Iran would attempt to close the Strait of Hormuz, the vital oil artery of the global economy with 18 million barrels of oil passing through this 34-kilometre wide stretch of sea.

At present there is an armada of ships from 25 nations conducting a mine sweeping exercise in the Straits, including three of the most powerful US aircraft carriers, each with more planes than the entire Iranian airforce.

Unpredictable consequences

Military experts are in no doubt who would win but wars are very unpredictable. The US over-ran Iraq in three weeks in 2003 but failed to adequately plan the occupation leaving the country highly unstable and in a virtual state of civil war.

Stock markets hit rock bottom in the spring of 2003 just before the invasion of Iraq and the Second Gulf War. That was the point of maximum uncertainty. Remember some then thought Saddam Hussein had weapons of mass destruction and nobody could be entirely sure.

This autumn many global stock markets have recovered to almost pre-global financial crisis levels, mostly without a full recovery in economic output. Arguably they are ripe for a fall.

As in 2003 the countdown to military action in the Gulf is just the sort of thing to put fear back into the markets. The most immediate impact is already being felt in the price of crude. Oil prices are at levels today that have tipped better global economies into recession.

Oil price impact

If Israel insists on making its attack on Iran then the price of crude will soar to levels beyond the peak of $147 a barrel in July 2008 that brought on the global financial crisis of that autumn after the failure of Lehman Brothers.

The stock market response will be to discount another major recession with very much lower share prices across the board. Hopefully whatever happens in this military action will not be anything like the worst case scenario and the bounce back for financial markets will be equally vigorous.

However, if you want to isolate the biggest threat to global financial markets this autumn it has to be an Israel-Iran conflict, something that the money printing of global central banks can do nothing to influence or contain.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair