Energy & Commodities

For every 10 percent increase in global food prices there is a 100 percent increase in anti-government protests, according to a recent report from the International Monetary Fund. Looking at recent price increases in global ag commodities — up about 20 percent so far this year — it’s no wonder there are Arab Fall flare ups (this time directed at America) breaking out across the globe. According to the IMF, a 20 percent increase in foodstuffs should triple the levels of unrest, and that seems to be precisely what’s happening.

The chaos caused by food inflation and hunger back in 2011 was heartwarmingly marketed by propagandists as democratization. Remember the French Revolution and “let them eat cake.” The causa proxima was food inflation, not stupid remarks or films. I hypothesize: Food Price Index + FAO Hunger Index = Riots, Civil Wars and Revolutions.

The United Nations’ Food and Agriculture Organization also offers a Global Hunger Index that measures levels of food stress around the world. According to the 2011 index, a hunger level above 30 is considered extremely alarming, 20 to 29 is alarming and 10 to 19 is serious.

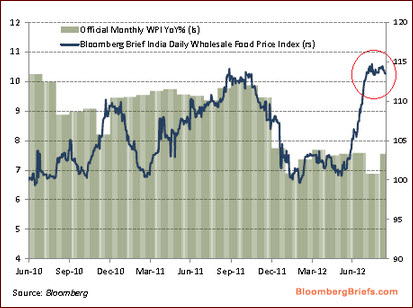

Among the countries to watch is Nigeria with a level of 16. About 10 percent of U.S. oil imports come from Nigeria, and it’s the sweet oil variety that can’t be substituted if disrupted. In 2011, Yemen, which is in open disorder and a completely failed state, had a hunger index of 25. Angola, another oil producer, had a hunger index of 27 and considered be in the “extremely alarming” category. Cameroon, a small African oil producer, had a score of 18. That country was severely impacted by food riots during the 2008 commodity bubble. Both Bangladesh and India were ranked 24. Both countries were impacted this year by a poor monsoon period, which normally brings much-needed rain for crops. Trouble spot Pakistan is 21.

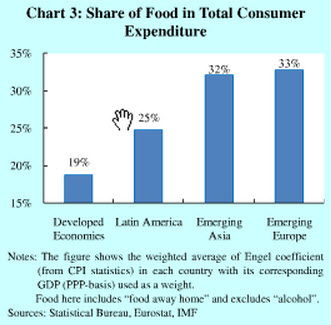

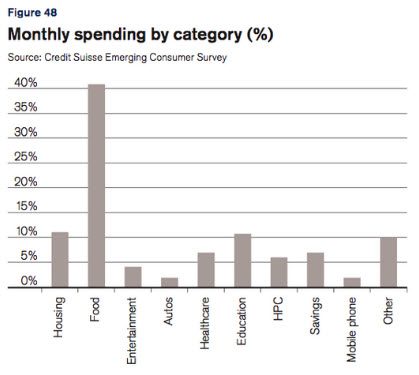

Obviously, not all countries are in high-hunger-index situations, but most of the world is spending a larger percentage of income on food. This includes 48 million Americans qualifying for food stamps. A 35 percent pop in prices for people already paying 30 percent of their income on food has the effect of triggering civil unrest.

Egypt is the world’s largest wheat importer, bringing in 60 percent of what it consumes from varied global sources. Egypt also imports 40 percent of its food and is highly vulnerable to rationing and steep prices. On average, Egyptians use 42 percent of their income on food. Watch wheat prices carefully. It is showing new signs of another lift off since the Fed’s open-opended QE announcement.

A new quantitative easing program is oppressive in a strong food-inflation environment. It also aggravates the effect of the drought and encourages speculators to pile into commodities that are already facing rationing. The Bank of Japan released a report that examines the financialization of commodities. With some big players effectively substituting foodstuffs and other commodities for near-zero-percent returns at the bank, the heightened interest in these commodities goes far beyond normal economic demand. It is key to understanding the impact of both QE and Zero Interest Rate Policy (ZIRP). The end result of the monetary experiment is a massive misallocation of capital, resulting in global hunger and social-political instability. Indeed, this is Ben Bernanke’s ultimate gesture to global food consumers.

For additional analysis on this topic and related trades, subscribers go to Russ Winter’s Actionable. The subscription fee is $69 per quarter and helps support Russ’s work on your behalf. Click here for more information or to subscribe.

Source: Wall Street Examiner

THE FIRST is a set of gold-rimmed eyeglasses. Further on, there is a pocket watch stopped at 11:14. Then there is a brown leather suitcase, somewhat worse for the wear. There are stacks of white dishes and racks of dark green bottles. Another display shows brass plumbing fixtures and a gray, steel wrench. And at another stop along the walk one sees a copper and glass engine thermometer. There is a jade rosary, and a man’s boulder hat, of all things, in remarkably fine condition, considering… And a pair of woman’s shoes, made of black leather. Not one shoe, but a pair, recovered from the sea floor beneath 12,000 feet of cold North Atlantic water.

Then there are the coins and paper currency. Gold coins, silver coins, copper. British, American, French. This was real money back then, from a gold standard era. And the paper notes also tell a tale. They are a collection of official British and American treasury promissory notes, and a remarkable amount of scrip from private banks, redeemable in precious metal.

Every note has an annotation at some spot or another, promising to pay to the bearer some quantity of gold or silver. “One Dollar Silver Note,” from a bank in New England, redeemable in an ounce of silver from that institution. Or a “Two Dollar Silver Certificate,” to be paid on demand by the Treasury of the United States of America in, not surprisingly, two ounces of silver. Or “Ten Gold Dollars,” half an ounce of yellow metal in 1912, promised by and intended to be paid to the bearer from the precious gold assets of the Government of the United States.

These artifact paper notes, recovered against all odds from their watery grave, still retain a certain sense of dignity. They do not declare mightily and officiously that they are “legal tender for all debts, public and private.” They do not have to… The notes represent a solemn promise by the issuer that, in return for a person lending a sum of honest money to the bank or government, the issuer of the note will repay an equal sum of precious metal at a time and place of mutual convenience. There is, it seems, a sense of financial humility, respect and national or corporate duty to these documents.

The Titanic exhibit explains that within about two years of the ship sinking, the British and American governments changed the methods by which they permitted currency to be issued. The exhibit does not go into detail, which is understandable. This is a display of artifacts from a sunken ship, not an exposition on monetary history. But it is interesting that the curators would mention it at all.

In late 1913 the US government enacted the Federal Reserve Act, which removed the power to issue monetary notes from private banks and the US Treasury, and gave that power to the newly established Federal Reserve, or the American central bank. And in 1914, Great Britain’s central bank, the Bank of England, went off the gold standard shortly after Britain entered into what became the Great War, now known as World War I.

For the 100 years before this time, the respective values of the British and US currency had held more-or-less steady, excepting a period of inflation during the American Civil War. But after 1914 the value of the respective currencies was set by… well, by a monetary system, for lack of a better term, run by each nation’s respective central bankers.

The idea was to have an “elastic currency,” meaning a currency base that could expand to meet the needs of a dynamic and growing economy, or in the case of Britain, to fight a war that the nation could not afford.

In the ninety or so years since those monetary milestones of 1913 and 1914, both the British pound and the US dollar have lost about 98% of their value due to inflation of the national monetary supplies. That sure makes for one heck of an “elastic currency”, eh?

But because this monetary debasement has happened so slowly — year by year, decade by decade, generation by generation — this decline of the value of national currency has seemed almost a natural phenomenon, an immutable law of nature. This is the way that monetary theory is taught in all of the best schools, and is how all modern monetary systems work, right?

Typically the politicians have demanded, and people have grown to accept, “a little bit” of inflation fostered by the central bank as the price of progress. Except that “a little bit” of inflation over a long time is actually “a lot” of inflation.

Over the long term, the nominal savings of one generation are reduced, in the aggregate, to a pittance. This matters quite a bit when one goes to retire a generation or so after going to work. And in an inflationary environment, valuations of capital become meaningless over the long term, absent using statistical guesses to determine deflation factors.

Keep in mind that savings create capital, and inflation destroys savings, hence destroys capital.

From the standpoint of ethics, it would seem that the people who run the Federal Reserve and the Bank of England have a responsibility to their respective citizens to maintain a stable value to their currencies, and not to destroy that value over time. It would seem that the managers of a nation’s currency have a duty to maintain monetary standards, and not to wreck savings and impoverish one generation to benefit another. It would seem so, but apparently this is not how the monetary system works.

By way of comparison, this ethical duty to maintain standards is much the same as the duty of the principals of the White Star Line to design and build a fine ship, appropriate to the hazards of oceanic crossings. And this is much as Captain E.J. Smith had a duty to train his crew and sail his vessel along a track that would bring her safely into the port of destination. But on the night that the Titanic sank, there was a failure of duty by the Captain to sail a safe course, even after an ice warning was received over the radio. And the iceberg, scraping the rivet heads off the steel plating of the Titanic and permitting the sea to flood the ship through hundreds of small penetrations, revealed a flaw in construction. And the sinking revealed the failure of White Star Line fundamentally to design a proper ship, with lifeboats sufficient to the need of passengers and crew in a time of peril.

As fate would have it, J. Bruce Ismay, one of the directors of the White Star Line, survived the Titanic’s sinking by leaping into one of the last lifeboats that dropped from the doomed vessel into the freezing ocean. Later on, Director Ismay was greatly criticized from almost every quarter, because he survived the sinking when over 1,500 others did not. One of the most trenchant critiques of Ismay came from Admiral Alfred Thayer Mahan, the great historian, strategist and sea power visionary of the US Navy, who reviewed Ismay’s retreat to the lifeboats and his abandonment of hundreds to death by freezing and drowning, and wrote:

“We should be careful not to pervert standards. Witness the talk that the result is due to ‘the system.’ What is a system, except that which individuals have made it and keep it? Whatever weakens the sense of individual responsibility is harmful, and so likewise is all condonation of failure of the individual to meet his responsibility.”

What will the central bankers say in their own defense when the dollar, or the pound, vanishes like the Titanic beneath the sea? Will they simply shrug their shoulders and blame “the monetary system”? What will they say to those doomed souls who are the victims of their failure, and whose lives, communities, nations and cultures are shattered? What will they say as the wreckage of their monetary system slips away and rains down, like the artifacts from the Titanic landing on the dark abyssal plain far below?

Read more: A Titanic Disaster http://dailyreckoning.com/a-titanic-disaster/#ixzz26pwyhDwZ

Regards,

Byron King,

for The Daily Reckoning

Byron King is the managing editor of Outstanding Investments and Energy & Scarcity Investor. He is a Harvard-trained geologist who has traveled to every U.S. state and territory and six of the seven continents. He has conducted site visits to mineral deposits in 26 countries and deep-water oil fields in five oceans. This provides him with a unique perspective on the myriad of investment opportunities in energy and mineral exploration. He has been interviewed by dozens of major print and broadcast media outlets including The Financial Times, The Guardian, The Washington Post, MSN Money, MarketWatch, Fox Business News, and PBS Newshour.

Special Video Presentation: Urgent Message About Your Net Worth The single, solution-packed book that could… literally… mean the difference between growing wealthy or suffering an ugly, vicious decline in your net worth. Discover how to claim a FREE copy of this book, right here.

»» Equities rallied, and the U.S. dollar and government bonds sold off following an aggressive monetary stimulus from the Fed. (page 2)

»» One of the final hurdles for a bailout of troubled European sovereigns was cleared as a German Court declined to interfere. (pages 2-3)

»» Global economic data remains generally lackluster but at least appears to have stabilized. (page 4)

»» We’ve upgraded our equity recommendation on Continental European stocks to neutral, and we’ve upgraded Asia (ex Japan) stocks to overweight. (pages 2-3)

»» Global Roundup: Updates from the U.S., Canada, Europe, and Asia. (pages 3-4)

Downside risk exceeds upside potential in equity markets during the next five weeks. The recent breakout by the S&P 500 Index implies that depth of the downside risk is less than previous. Selected seasonal trades continue on the upside (gold, energy, software) and downside (transportation). However, many of these seasonal trades reach the end of their period of seasonal strength this month. September is a month of transition. Trade accordingly.

Last week we certainly had some game-changing events, with the German court ruling in favor of the European Stability Mechanism … Europe going ahead with yet more bailouts … and, perhaps more staggering, Fed Chairman Ben Bernanke committing the Federal Reserve to buying $40 billion worth of mortgage-backed securities each month on an open-ended, unending basis until employment improves.

These are possibly game-changing fundamentals for the markets.

They’re entirely consistent with my longer-term views of monetization of debt, commoditization of not just commodities but stocks as well, and monetization of paper money (or fiat currencies) by levitating and re-flating financial assets and tangible assets much higher over the longer term.

So with that in mind, we’re going to take a look at some weekly charts.

Although there have been some game-changing events in the last week or so, they have confirmed my longer-term views on longer-term bull markets in commodities and stocks.

However, I am not convinced that the recent rallies are the beginning of those long-term breakouts. So let’s take a look at this weekly chart of gold.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair