Timing & trends

“Mario Draghi and Ben Bernanke have willingly opened the floodgates and allowed their respective printing presses run 24/7. No surprise here. This is all Central Bankers know how to do and it had been forecast by many (myself included).”

“My Annual Forecast Model (below) along with Equityclock.com’s ‘seasonal’ studies all pointed to the time band from mid-summer forward as being friendly to the metals. So, for now, we need to sit back and enjoy it!”

“Depending on which forecast chart you look it, it is clear we’re overall headed higher. However, there is theoretical ‘cyclical’ risk of a pullback both here in September and again in October. Use pullbacks to establish or to add to current positions if you don’t feel you allocation to the metals is great enough.”

Quote & Chart above from Mark Leibovit’s Hot off the Press Sept. 14th 25 page VR Gold Letter . IF YOU HAVE NOT SIGNED UP FOR THE LEIBOVIT VR GOLD LETTER, HERE IS YOUR CHANCE. HERE IS THE LINK: WWW.VRGOLDLETTER.COM. YOU GET A 50% DISCOUNT FOR THE FIRST MONTH.

Miners Catching Up To Metals — Huge Run

Coming?

Gold bugs are a generally happy bunch this week. But they’d be a lot happier if precious metals mining stocks kept up with the metals themselves. Since early 2011 the largest gold miners have underperformed gold by about 40%, while the junior miners have done even worse (I’m talking to you, Great Basin).

Thanks to this divergence between the metals and the miners, it was possible to clearly understand the monetary destruction endemic in the developed world, conclude that gold and silver were the places to be, make a decisive bet on this thesis — and still end up losing money.

There are two possible conclusions to draw from this: Either mining as a business has changed fundamentally and will be unprofitable forever – in which case we should just own physical metal and forget about paper proxies. Or the past couple of years were one of those inexplicable divergences from established relationships that produce huge gains when they snap back to normal.

The past month has offered a taste of what the second possibility might look like. The chart below shows that the big miners (represented by the GDX gold miner ETF, red line) have outperformed gold itself (the GLD bullion ETF, blue area) since July. But the two-year gap, like I said, is about 40%, so parity is still a long way off.

Now that the miners have some momentum, it wouldn’t be surprising if they made up this ground in no time at all.

Above by DollarCollapse.com managed by John Rubino, co-author, with GoldMoney’s James Turk

Perspective on the current Dow rally

The Dow made another post-financial crisis rally high Thursday on the news that the Fed will embark on a third round of quantitative easing (a.k.a. QE3). To provide some perspective on the current Dow rally, all major market rallies of the last 112 years are plotted on today’s chart. Each dot represents a major stock market rally as measured by the Dow — with a rally being defined as an advance that followed a 15% correction (i.e. a major correction). As today’s chart illustrates, the Dow has begun a major rally 28 times over the past 112 years which equates to an average of one rally every four years. Also, most major rallies (78%) resulted in a gain of between 30% and 150% (29.8% to 150.5% to be exact) and lasted between 200 and 800 trading days (9.5 months to 3.2 years) — highlighted in today’s chart with a light blue shaded box. As it stands right now, the current Dow rally (hollow red dot labeled you are here) which began in October 2011 (since it followed a 16.8% correction), would be classified as well below average in both duration and magnitude.

Notes:

Where’s the Dow headed? The answer may surprise you. Find out right now with the exclusive & Barron’s recommended charts of Chart of the Day Plus.

Quote

“Rather than stimulating a real recovery by focusing on a strong dollar and market interest rates, the Fed’s announcement today shows a disastrous detachment from reality on the part of our central bank.”

– Ron Paul

(Ed Note: Jack Crooks is this weeks Money Talks Guest)

Of Interest

- Troika could give Greece more time for reforms (Telegraph)

- Era of ‘jobs-targeting’ begins as Fed launches QE3 (Telegraph)

Commentary

The Federal Reserve was set-up to disappoint; but they didn’t. And why would they have? Bernanke’s received more than a few pats on the back for his decisions to date:

“QE has made a massive difference,” said Tim Congdon from International Monetary Research. “If they had not done it we would have gone into another Great Depression.”

There were high expectations for Fed action yesterday. They delivered mostly at those expectations, except for one thing – they put no end-date on their operations. Twist … to infinity and beyond.

And that may be the difference maker.

We’d seen several indicators and pieces of analysis to suggest Fed expectations were priced in. That may be true; and the price action yesterday (following the announcement) and this morning may be a blow-off squeeze of sorts. In the recent history of QE and Twisting, the rumors and expectations in the months leading up to the actual action have created the environment for risk assets to rally. These assets, however, have sold off in the periods after the actual action. It is the classic “buy the rumor, sell the news” dynamic.

Action

As of now, that dynamic seems to make the most sense. The market is ripe for a downturn. But once that downturn runs its course (maybe lasting a month or so), there is little reason right now to expect anything but an extended uptrend for risk assets. Certainly this unlimited monetary accommodation will juice up inflation expectations and liquidity, justifying investments in commodities and stocks.

But what about the fundamentals? The Fed’s comments suggest there is nothing horribly worrisome about US growth potential, barring continued pressure on jobs. So has our fundamental analysis been horribly misguided? We don’t think so. Actually, recent Fed action seems to validate our pessimism. But our expectations for price action have been off target. Looking ahead, we are considering ways to hedge current bearish positioning. And unless a real crisis in confidence materializes soon, it will likely make sense to adopt a bullish stance on the markets. Stay tuned.

The Federal Reserve fulfilled expectations of more stimulus for the faltering economy, taking aim now at driving down mortgage rates until an improvement in unemployment that the central bank says will be a problem for several years. Ben Bernanke recently spoke of the benefits of “non-traditional policies”

The US central bank has announced it will resume its policy of pumping more money into the economy via so-called quantitative easing. The Federal Reserve said it will “increase policy accommodation by purchasing additional agency mortgage-backed securities at a pace of $40bn per month”. Interest rates in the US have been close to zero for several years now.

The purchases will be open-ended, meaning that they will continue until the Fed is satisfied that economic conditions, primarily in unemployment, improve.

“The committee is concerned that, without further policy accommodation, economic growth might not be strong enough to generate sustained improvement in labour market conditions,” said the Fed, led by chairman Ben Bernanke

The stock market, which had been slightly positive prior to the decision surged while bond yields, particularly farther out on the curve, jumped higher.

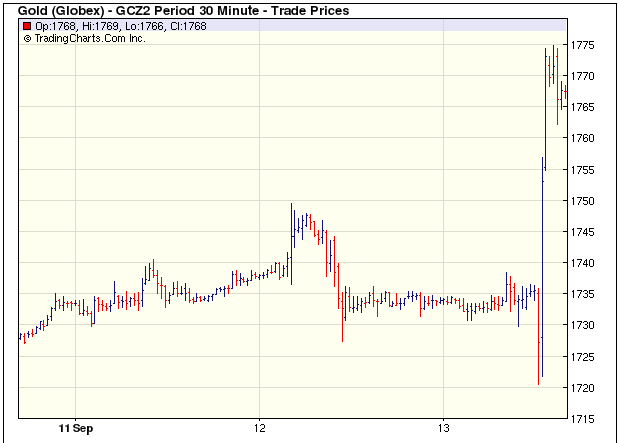

(Ed Note: Chart below taken at 12.45 pm PST)

Gold and other metals gained at least 1 percent across the board while the dollar slid against most global currencies. (Ed Note: Gold chart taken at 12:58 PST)

“There’s strong hints that they’ll do Treasurys next,” Joe LaVorgna, chief economist at Deutsche Bank Advisors, said in a phone interview from London. “They’re pulling out all the stops to try to get this economy to gain some traction and, most important, to get unemployment down.” (Ed Note: It would seem that investors are thinking the Fed will act next on Treasurys as T-Notes rallied back to their pre-announcement levels. Chart taken at 1.06 pm PST)

…read more:

Fed’s Stimulus Move Ignites Wall Street

Fed Bets Big in New Push To Rescue Economy

Federal Reserve to buy more debt to boost US Economy

The nation is approaching the “fiscal cliff.” This is a negative for the market. On January 13, Congress will have to vote on whether to increase the national debt, which is now over $16 trillion and counting. Fiscal cliff and debt ceiling are both momentous decisions for Congress, problems that they’d rather not face.

The stock market also has its problems. Last week the Industrial Average closed above its May 1st peak — the Industrial move was not confirmed by the Transports. This leaves the stock market in limbo, and it leaves investors in a quandary. My choice for an investment position is — gold coins (bullion) and GLD and enough cash to pay your bills. If the Fed acts to stimulate the economy, it would be bullish for gold. If the nation goes over the fiscal cliff, such an emergency would probably be bullish for gold. If Congress fails to raise the debt limit, it should be bullish for gold (another emergency).

If absolutely nothing happens, the prevailing forces of deflation will kick in, and that would be bearish for all commodities and probably bearish for gold. But wait — if the whole scene turns deflationary, that would be a situation that Bernanke would not tolerate (the Fed is terrified of deflation), and Bernanke would almost surely flood the system with truck loads of fiat money — that would be bearish for the dollar and bullish for gold.

Big picture — emerging nations are slowing down. China’s economy is slowing, Europe is in recession, employment in the US has stalled and unemployment remands high. In the face of this, the world forces of deflation are continuing. The US could now be suffering long-term structural damage, as the Fed has feared.

This all militates toward Fed action, but many question whether Fed action will do much good. The European Central Bank unveiled a bond-buying program last Thursday, and China announced major infrastructure projects last week.

The Fed can bull the markets, but it can’t directly create jobs. During the Great Depression, the government created jobs through its alphabet agencies such as the CCC and the WPA. I wouldn’t be surprised if the current government chooses that path again. In the meantime, the stock and bond markets are in a quandary. The trend, if there a trend– where is it?

Below, the US dollar is looking bearish and has just broken below both moving averages. A cheaper dollar is bullish for gold.

Is world commerce slowing down? You wouldn’t know it from ‘Dr. Copper,’ which is busting out from a good base and is now above both MAs.

Below is a chart I’m keeping an eye on. It’s the YIELD on the bellwether 10-year T-note. I think we’ve seen the low on this critical note. As bond yields rise, it’s going to put competitive pressure on stocks, which is one reason why I’m still very conservative. This is no time to be a wild man in the stock market. With the chart below imbedded in my thinking, I now advise more cash and less gold in the mix.

As my friend, Bob Prechter once said, ‘There’s nothing wrong with cash — it gives you time to think.’ The only question in my mind is — is it better to have your currency in paper, or is it better to have it in gold, better known as real tangible money? Personally, I trust gold more than I trust paper, but that’s just me and hard experience.”

To subscribe to Richard Russell’s Dow Theory Letters CLICK HERE.

Letters are published and mailed every three weeks. We offer a TRIAL (two consecutive up-to-date issues) for $1.00 (same price that was originally charged in 1958). Trials, please one time only. Mail your $1.00 check to: Dow Theory Letters, PO Box 1759, La Jolla, CA 92038 (annual cost of a subscription is $300, tax deductible if ordered through your business).

IMPORTANT: As an added plus for subscribers, the latest Primary Trend Index (PTI) figure for the day will be posted on our web site — posting will take place a few hours after the close of the market. Also included will be Russell’s comments and observations on the day’s action along with critical market data. Each subscriber will be issued a private user name and password for entrance to the members area of the website.

Investors Intelligence is the organization that monitors almost ALL market letters and then releases their widely-followed “percentage of bullish or bearish advisory services.” This is what Investors Intelligence says about Richard Russell’s Dow Theory Letters: “Richard Russell is by far the most interesting writer of all the services we get.” Feb. 19, 1999.

Below are two of the most widely read articles published by Dow Theory Letters over the past 40 years. Request for these pieces have been received from dozens of organizations. Click on the titles to read the articles.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair