Gold & Precious Metals

Knowing that it’s very likely that Gold and Silver have bottomed, we feel it is time to look at the charts and assess what may or may not be in store over the next year or two.

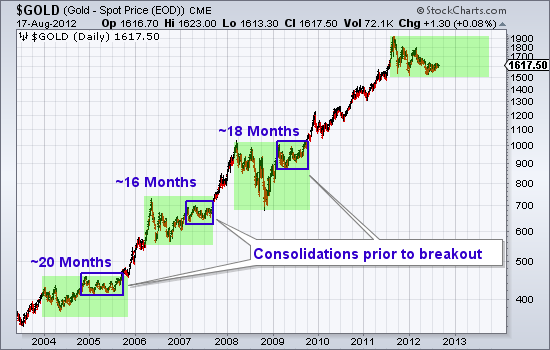

Gold has consistently made impulsive advances that were digested by multi-quarter corrections and eventually followed by a breakout and new impulsive advance. Following the last major breakout in late 2009, Gold enjoyed an extended impulsive advance that lasted two years. Previous impulsive advances lasted less than a year. Gold, having bottomed, remains well entrenched in another consolidation that is 12 months old. As we can see from the chart, previous consolidations lasted 16 to 20 months.

It is important to note that previously Gold, within a year was able to rally back near the recent impulsive high. In other words, Gold is currently in a much weaker state relative to past consolidations. Gold will need to rally back to $1800 or $1900 and that would be followed by a multi-month consolidation that would lead to a breakout. Conservatively speaking, over the next 12 months we could see a rally back to $1900 and a final consolidation.

Meanwhile, Silver continues to consolidate and digest the two and a half year advance from $8 to $49. Predictions of $60 or $70 Silver are absurd and fail to account for the lengthy consolidation that is needed to reduce supply and position the market for not only a retest of $50 but an actual breakout. Silver is a commodity with real world supply and demand dynamics. It will be a while before producers won’t sell for $35-$36 and before buyers consider $35 a bargain. That being said, the near and medium term outlook is quite compelling. Longer-term, the market is in a giant cup and handle pattern (dating back to the high in 1980) and this correction and consolidation is the handle. A powerful breakout past $50 in, say 2014, could push Silver towards its bubble phase.

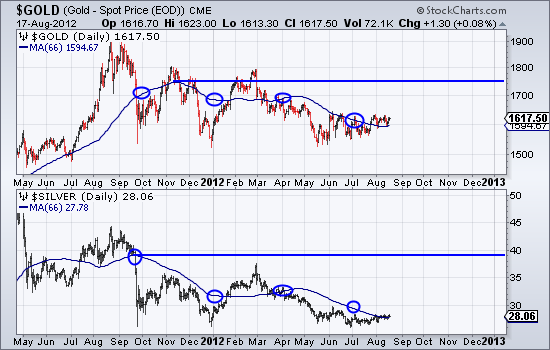

The fact that Gold and Silver are unlikely to break to new highs anytime soon hardly deters me in my bullish enthusiasm for select gold and silver stocks. Key word being select. I’m not bullish on every mining company but I digress. In the chart below I use a 66-day moving average to plot an average quarterly Gold and Silver price. I also circle the moving average at the end of quarters.

Note that the quarterly high prices for Gold and Silver are roughly $1750 and $39 and far off from the 2011 highs. The quarterly averages are starting to turn up. Well run companies with production increases could very well move to new highs when Gold returns to $1750 and Silver moves past $35. We do think most of the Gold and Silver shares can breakout to new highs ahead of the metals. In other words, the mining shares at large will ultimately challenge for a breakout ahead of Gold and Silver reaching new all time highs. If you’d be interested in ourprofessional guidance and uncovering the producers and explorers poised for biggains, then we invite you to learn more about our service.

Good Luck!

Jordan Roy-Byrne, CMT

Market Notes

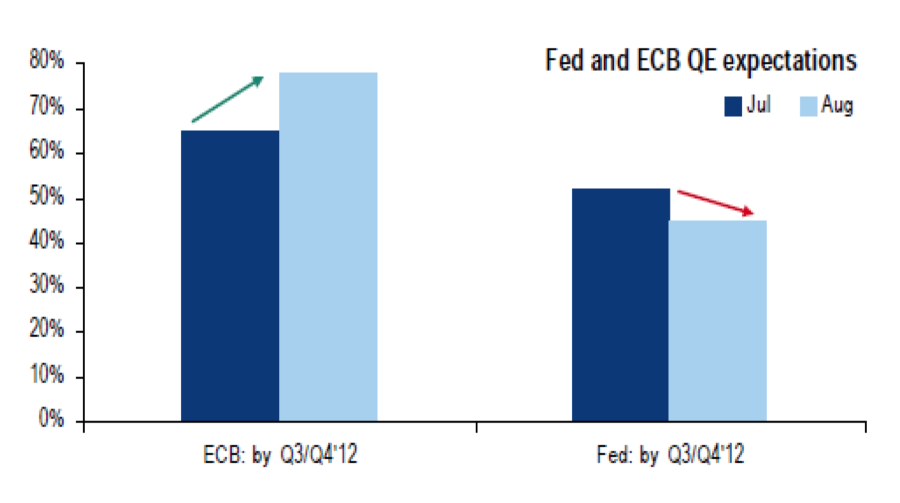

- Recent Merrill Lynch Fund Managers Survey showed that 8 out of 10 fund managers expect ECB to engage into QE engage into QE by the end of the year, while 5 out of 10 expect Fed to re-start QE. Also to note was that managers increased equity exposure to overweight, increased exposure to commodities from underweight to neutral and finally decreased exposure in both cash and bonds.

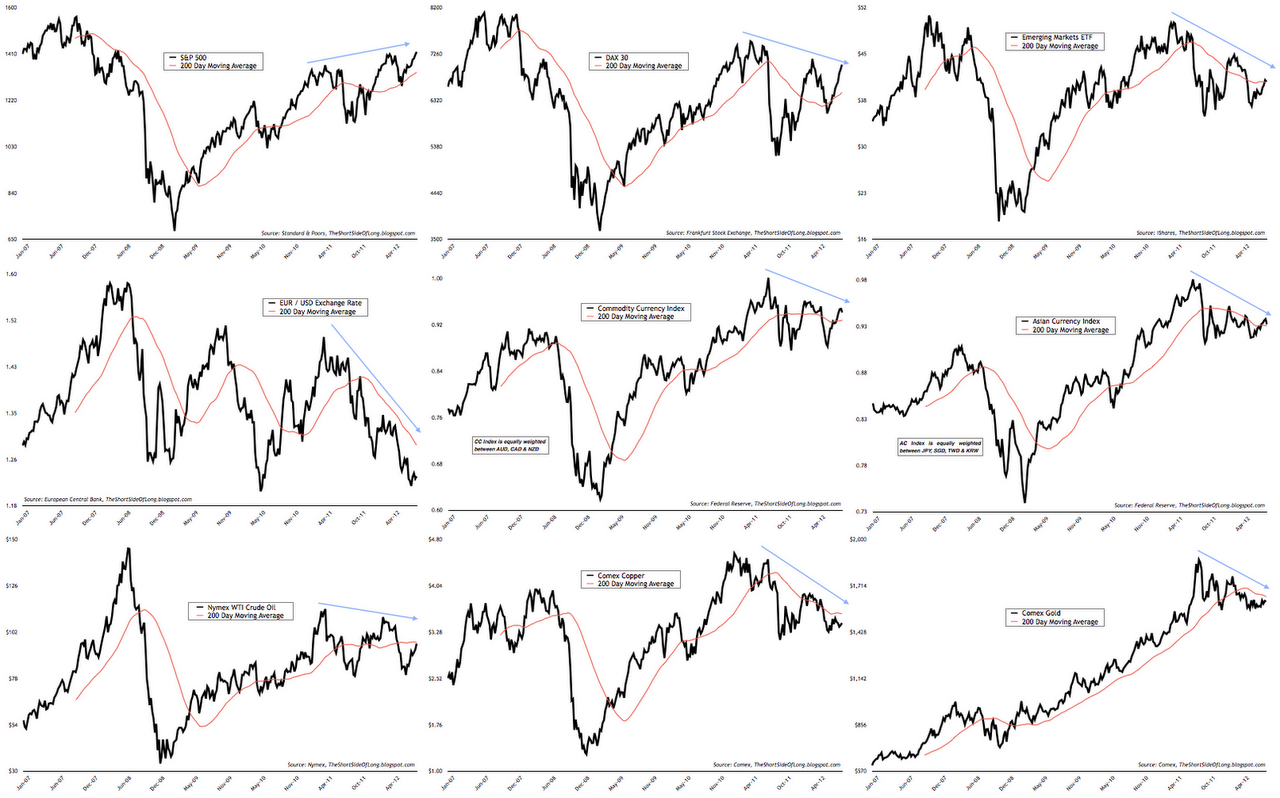

- Bulls well and truly dominate the media space (CNBC, Bloomberg). That is usually what happens when US equities rise for six straight weeks and EU equities rise for 11 straight weeks. NYSE 10 day TRIN breadth measure has now become extremely low and joins other indicators like the VIX in signalling maximum complacency.

- Treasury Inflation Protection securities (TIPs) have done amazingly well in recent years. We have seen a very strong correlation with the overall business cycle since early 2009. TIPs have tracked the improvement in equity prices, industrial production and weekly jobless claims perfectly. Fast forward to today and we see TIPs breaking down. What is the message for other risk assets?

- Global risk appetite is usually best represented by the Aussie Yen exchange rate cross. Australian central bank is seen as a super hawkish inflation fighter during economic upturns, while capital naturally finds its way into Japanese Yen during downturns as a safe haven – a perfect risk on / risk off barometer. Aussie Yen cross continues to send a warning signal for other risk assets

{kind=link}

![]()

You cannot expect to do well in the market if you look at investing in a normal way. By definition, being average is doing what most other people do and since investing is largely a psychological game, doing what other people do is only natural. Average results come from normal people acting in normal ways.

To beat the market, you have to be different.

Not necessarily in a straight jacket bouncing off padded walls different, just a little off.

Here are 10 things that may help you be a better investor, some ways to think differently from the crowd in that pursuit to achieve market dominance.

1. Do not think about making money, think about losing money – the first step toward success is accepting that losing is part of trading. You will not be right all of the time, you cannot always trade your way out of a bad situation. There will be times when you simply have to walk away with a loss. The key is to keeping the losses small and manageable. When the market proves you wrong, take the loss.

2. Do not think you can average down to win – it is a logical idea, add more to a losing position with the expectation that the market must eventually go your way. Many times this strategy will work but, when it does not work, the loss may be insurmountable. The market does not eventually have to go your way.

3. Do not think that your success is entitled – you may make a great trade, pick a really great stock and have a feeling like you really have the market figured out. Forget your gloating, no one ever has the market figured out. We must always remember that we have to work as smart for the next trade as we did for the last.

4. Do not think that talent is required – making money in any trading endeavor is a small part technical skill and a big part emotional management. Learn to limit losses, let winners run and be selective with what you trade. Emotional mastery is more important than stock picking skill.

5. Do not think that you can tell the market what to do – the market does not care about you, it does not know that you want to make a profit. You are the slave, the market is your master. Be obedient and do what the market tells you to.

6. Do not think you are competing against other traders – trading success comes to those who overcome themselves, it is you and your persistent desire to break trading rules that is the ultimate adversary. What others are doing is of little consequence, only you can react to the market and achieve your success.

7. Do not think that Fear and Greed can ever be positive – in life, fear can keep us from harm, greed can give us the motivation to work hard. In the market, these two emotional forces will lead to losses. If your decisions are governed by either or both you will most certainly find that your money escapes you.

8. Do not think you will remember everything you learn – every trade provides a lesson, some valuable education on what to do and what not to do. However, it is likely that your lessons will contradict one another and lead you to forget many of them. Write down the knowledge that you accumulate, return to this trading journal so that you can retain some value from the lessons taught by the market. Remember, the market is cruel, it gives the test first and the lesson after.

9. Do not think that being right will lead to profits – you may be exactly right about what the fundamentals are and what they are worth. However, timing is everything, if your expectations for the future are ill timed, you may find yourself losing more than you can tolerate. Remember, the market can be wrong longer than you can be liquid.

10. Do not think you can overcome the laws of probability – traders tend to be gamblers when they face a loss and risk averse when the have a potential for gain. They would rather lock in a sure profit and gamble against a probable loss even if the expected value of doing so is irrational. Trading is a probability game, each decision should be made on the basis of the best expected value and not what feels best

I am on vacation this week so there is no Market Minutes video. Back to normal next week.

![]()

- Get the Stockscore on any of over 20,000 North American stocks.

- Background on the theories used by Stockscores.

- Strategies that can help you find new opportunities.

- Scan the market using extensive filter criteria.

- Build a portfolio of stocks and view a slide show of their charts.

- See which sectors are leading the market, and their components.

If you’ve been following my newsletter, you’re familiar by now with my friend George Friedman and the geopolitical analysis company he founded, Stratfor. And if you’ve read any of George’s work, you know that his entire methodology is based on the premise that the actions of leaders and nations are predictable. George starts with the constraints – what can they notdo, assuming they’re rational actors – and moves forward from there. It’s this methodology that allowed him to – in all seriousness and probably with an impressive amount of accuracy – write a book titled The Next 100 Years.

I’ve always encouraged my readers to keep up with George’s work at Stratfor. His expertise is not in investing, but the understanding of global politics he provides is essential for any global investor. That said, this week George set his sights on the world of investing with a rather harsh accusation: that investors today lack both imagination and an understanding of political economy.

It’s always uncomfortable, to say the least, when good thinkers turn a critical eye on your own profession. I don’t necessarily agree with George’s conclusions, but I respect him enough to give his ideas some careful consideration and share them with my readers. After all, my basic premise with Outside the Box is that there is little to gain by reading only the work of those with whom we agree.

If George’s piece makes you think, I recommend you check out Stratfor. They offer a substantial discount on subscriptions to OTB readers, plus a complimentary copy of the aforementioned book, The Next 100 Years, for new subscribers. <<Click here to access the offer.>>

Your not so unimaginative analyst,

John Mauldin, Editor

Outside the Box

Louis M. Bacon is the head of Moore Capital Management, one of the largest and most influential hedge funds in the world. Last week, he announced that he was returning one quarter of his largest fund, about $2 billion, to his investors. The reason he gave to The New York Times was that he had found it difficult to invest given the impossibility of predicting the European situation. He was quoted as saying, “The political involvement is so extreme – we have not seen this since the postwar era. What they are doing is trying to thwart natural

The purpose of hedge funds is to make money, and what Bacon essentially said was that it is impossible to make money when there is heavy political involvement, because political involvement introduces unpredictability in the market. Therefore, prudent investment becomes impossible. Hedge funds have become critical to global capital allocation because their actions influence other important actors, and their unwillingness to invest and trade has significant implications for capital availability. If others follow Moore Capital’s lead, as they will, there will be greater difficulty in raising the capital needed to address the problem of Europe.

But more interesting is the reasoning. In Bacon’s remarks, there is the idea that political decisions are unpredictable, or less predictable than economic decisions. Instead of seeing German Chancellor Merkel as a prisoner of non-market forces that constrain her actions, conventional investors seem to feel that Europe is now subject to Merkel’s whims. I would argue that political decisions are predictable and that Merkel is not making decisions as much as reflecting the impersonal forces that drive her. If you understand those impersonal forces, it is possible to predict political behaviors, as you can market behaviors. Neither is an exact science, but properly done, neither is impossible.

Political Economy

In order to do this, you must begin with two insights. The first is that politics and the

There are times when politics leave such laws unchanged and times when politics intrude. The last generation has been a unique time in which the prosperity of the markets allowed the legal structure to remain generally unchanged. After 2008, that stability was no longer possible. But active political involvement in the markets is actually the norm, not the exception. Contemporary investors have taken a dramatic exception – the last generation – and lacking a historical sense have mistaken it for the norm. This explains the inability of contemporary investors to cope with things that prior generations constantly faced.

The second insight is the recognition that thinkers such as Adam Smith and David Ricardo, who modern investors so admire, understood this perfectly. They never used the term “economics” by itself, but only in conjunction with politics; they called it political economy. The term “economy” didn’t stand by itself until the 1880s when a group called the Marginalists sought to mathematize economics and cast it free from politics as a stand-alone social science discipline. The quantification of economics and finance led to a belief – never held by men like Smith – that there was an independent sphere of economics where politics didn’t intrude and that mathematics allowed markets to be predictable, if only politics wouldn’t interfere.

Given that politics and economics could never be separated, the mathematics were never quite as predictive as one would have thought. The hyper-quantification of market analysis, oblivious to overriding political considerations, exacerbated market swings. Economists and financiers focused on the numbers instead of the political consequences of the numbers and the political redefinitions of the rules of corporate actors, which the political system had invented in the first place.

The world is not unpredictable, and neither is Europe nor Germany. The matter at hand is neither what politicians say they want to do nor what they secretly wish to do. Indeed, it is not in understanding what they will do. Rather, the key to predicting the political process is understanding constraints – the things they can’t do. Investors’ view that markets are made unpredictable by politics misses two points. First, there has not been a market independent of politics since the corporation was invented. Second, politics and economics are both human endeavors, and both therefore have a degree of predictability.

The European Union was created for political reasons. Economic considerations were a means to an end, and that end was to stop the wars that had torn Europe apart in the first half of the 20th century. The key was linking Germany and France in an unbreakable alliance based on the promise of economic prosperity. Anyone who doesn’t understand the political origins of the European Union and focuses only on its economic intent fails to understand how it works and can be taken by surprise by the actions of its politicians.

Postwar Europe evolved with Germany resuming its prewar role as a massive exporting power. For the Germans, the early versions of European unification became the foundation to the solution of the German problem, which was that Germany’s productive capacity outstripped its ability to consume. Germany had to export in order to sustain its economy, and any barriers to free trade threatened German interests. The creation of a free trade zone in Europe was the fundamental imperative, and the more nations that free trade zone encompassed, the more markets were available to Germany. Therefore, Germany was aggressive in expanding the free trade zone.

Germany was also a great supporter of Europewide standards in areas such as employment policy, environmental policy and so on. These policies protect larger German companies, which are able to absorb the costs, from entrepreneurial competition from the rest of Europe. Raising the cost of entry into the marketplace was an important part of Germany’s strategy.

Finally, Germany was a champion of the euro, a single currency controlled by a single bank over which Germany had influence in proportion to its importance. The single currency, with its focus on avoiding inflation, protected German creditors against European countries inflating their way out of debt. The debt was denominated in euros, the European Central Bank controlled the value of the euro, and European countries inside and outside the eurozone were trapped in this monetary policy.

So long as there was prosperity, the underlying problems of the system were hidden. But the 2008 crisis revealed the problems. First, most European countries had significant negative balances of trade with Germany. Second, European monetary policy focused on protecting the interests of Germany and, to a lesser extent, France. The regulatory regime created systemic rigidity, which protected existing large corporations.

Merkel’s policy under these circumstances was imposed on her by reality. Germany was utterly dependent on its exports, and its exports in Europe were critical. She had to make certain that the free trade zone remained intact. Secondarily, she had to minimize the cost to Germany of stabilizing the system by shifting it onto other countries. She also had to convince her countrymen that the crisis was due to profligate Southern Europeans and that she would not permit them to take advantage of Germans. The truth was that the crisis was caused by Germany’s using the trading system to flood markets with its goods, its limiting competition through regulations, and that for every euro carelessly borrowed, a euro was carelessly lent. Like a good politician, Merkel created the myth of the crafty Greek fooling the trusting Deutsche Bank examiner.

The rhetoric notwithstanding, Merkel’s decision-making was clear. First, under no circumstances could she permit any country to leave the free trade zone of the European Union. Once that began she could not predict where it would end, save that it might end in German catastrophe. Second, for economic and political reasons she had to be as aggressive as possible with defaulting borrowers. But she could never be so aggressive as to cause them to decide that default and withdrawal made more sense than remaining in the system.

Merkel was not making decisions; she was acting out a script that had been written into the structure of the European Union and the German economy. Merkel would create crises that would shore up her domestic position, posture for the best conceivable deal without forcing withdrawal, and in the end either craft a deal that was not enforced or simply capitulate, putting the problem off until the next meeting of whatever group.

In the end, the Germans would have to absorb the cost of the crisis. Merkel, of course, knew that. She attempted to extract a new European structure in return for Germany’s inevitable capitulation to Europe. Merkel understood that Europe, and one of the foundations of European prosperity, was cracking. Her solution was to propose a new structure in which European countries accepted Brussels’ oversight of their domestic budgets as part of a systemic solution by the Germans. Some countries outright rejected this proposal, while others agreed, knowing it would never be implemented. Merkel’s attempt to recoup by creating an even more powerful European apparatus was bound to fail for two reasons. First and most important, giving up sovereignty is not something nations do easily – especially not European nations and not to what was effectively a German structure. Second, the rest of Europe knew that it didn’t have to give in because in the end Germany would either underwrite the solution (by far the most likely outcome) or the free trade zone would shatter.

If we understand the obvious, then Merkel’s actions were completely understandable. Germany needed the European Union more than any other country because of its trade dependency. Germany could not allow the union to devolve into disconnected nations. Therefore, Germany would constantly bluff and back off. The entire Greek drama was the exemplar of this. It was Merkel who was trapped and, being trapped, she was predictable.

The euro question was interesting because it intersected the banking system. But in focusing on the euro, investors failed to understand that it was a secondary issue. The European Union was a political institution and European unity came first. The lenders were far more concerned about the fate of their loans than the borrowers were. And whatever the shadow play of the European Central Bank, they would wind up doing the least they could do to avert default – but they would avert default. The euro might have been what investors traded, but it was not what the game was about. The game was about the free trade zone and Franco-German unity. Merkel was not making decisions based on the euro, but on other more pressing considerations.

Modern Trading

The investors’ problem is that they mistake the period between 1991 and 2008 as the norm and keep waiting for it to return. I saw it as a freakish period that could survive only until the next major financial crisis – and there always is one. While the unusual period was under way, political and trade issues subsided under the balm of prosperity. During that time, the internal cycles and shifts of the European financial system operated with minimal external turbulence, and for those schooled in profiting from these financial eddies, it was a good time to trade.

Once the 2008 crisis hit external factors that were always there but quiescent became more overt. The internal workings of the financial system became dependent on external forces. We were in the world of political economy, and the political became like a tidal wave, making the trading cycles and opportunities that traders depended on since 1991 irrelevant. And so, having lost money in 2008, they could never find their footing again. They now lived in a world where Merkel was more important than a sharp trader.

Actually, Merkel was not more important than the trader. They were both trapped within constraints about which they could do nothing. But if those constraints were understood, Merkel’s behavior could be predicted. The real problem for the hedge funds was not that they didn’t understand what they were doing, but the manner in which they had traded in the past simply no longer worked. Even understanding and predicting what political leaders will do is of no value if you insist on a trading model built for a world that no longer exists.

What is called high velocity trading, constantly trading on the infinitesimal movements of a calm but predictable environment, doesn’t work during a political tidal wave. And investors of the last generation do not know how to trade in a tidal wave. When we recall the two world wars and the Cold War, we see that this was the norm for the century and that fortunes were made. But the latest generation of investors wants to control risk rather than take advantage of new realities.

However we feel about the performance of the financial community since 2007, there must be a system of capital allocation. That can be operated by the state, but there is empirical evidence that the state isn’t very good at making investment decisions. But then, the performance of the financial community has been equally unacceptable, with more than its share of mendacity to boot. The argument for private capital allocation may be theoretically powerful, but the fact is that the empirical validation of the private model hasn’t been there for several years.

A strong argument can be made – corruption and stupidity aside – that the real problem has been a failure of imagination. We have re-entered an era in which political factors will dominate economic decisions. This has been the norm for a very long time, and traders who wait for the old era to return will be disappointed. Politics can be predicted if you understand the constraints under which a politician such as Merkel acts and don’t believe that it is simply random decisions. But to do that, you have to return to Adam Smith and recall the title of his greatest work, The Wealth of Nations. Note that Smith was writing about nations, about politics and economics – about political economy.

John Mauldin is president of Millennium Wave Advisors, LLC, a registered investment advisor. All material presented herein is believed to be reliable but we cannot attest to its accuracy. Investment recommendations may change and readers are urged to check with their investment counselors before making any investment decisions.

Opinions expressed in these reports may change without prior notice. John Mauldin and/or the staffs at Millennium Wave Advisors, LLC and InvestorsInsight Publishing, Inc. (InvestorsInsight) may or may not have investments in any funds, programs or companies cited above.

PAST RESULTS ARE NOT INDICATIVE OF FUTURE RESULTS. THERE IS RISK OF LOSS AS WELL AS THE OPPORTUNITY FOR GAIN WHEN INVESTING IN MANAGED FUNDS. WHEN CONSIDERING ALTERNATIVE INVESTMENTS, INCLUDING HEDGE FUNDS, YOU SHOULD CONSIDER VARIOUS RISKS INCLUDING THE FACT THAT SOME PRODUCTS: OFTEN ENGAGE IN LEVERAGING AND OTHER SPECULATIVE INVESTMENT PRACTICES THAT MAY INCREASE THE RISK OF INVESTMENT LOSS, CAN BE ILLIQUID, ARE NOT REQUIRED TO PROVIDE PERIODIC PRICING OR VALUATION INFORMATION TO INVESTORS, MAY INVOLVE COMPLEX TAX STRUCTURES AND DELAYS IN DISTRIBUTING IMPORTANT TAX INFORMATION, ARE NOT SUBJECT TO THE SAME REGULATORY REQUIREMENTS AS MUTUAL FUNDS, OFTEN CHARGE HIGH FEES, AND IN MANY CASES THE UNDERLYING INVESTMENTS ARE NOT TRANSPARENT AND ARE KNOWN ONLY TO THE INVESTMENT MANAGER.

Communications from InvestorsInsight are intended solely for informational purposes. Statements made by various authors, advertisers, sponsors and other contributors do not necessarily reflect the opinions of InvestorsInsight, and should not be construed as an endorsement by InvestorsInsight, either expressed or implied. InvestorsInsight is not responsible for typographic errors or other inaccuracies in the content. We believe the information contained herein to be accurate and reliable. However, errors may occasionally occur. Therefore, all information and materials are provided “AS IS” without any warranty of any kind. Past results are not indicative of future results.

Posted 08-17-2012 1:00 by John Mauldin

What? You’re not happy with the market? It could be worse. You could have loaded up on the Facebook IPO at 44, and today the dog is selling at 19.07. But I’m not sure I feel sorry for Zuckerberg. After all (sniff) he’s no longer one of the five richest tech-lords. Now there is talk that he should be removed as CEO, because he’s too immature.

Fred Hickey, my vote as the top expert in tech, thinks the tech bubble has popped, and that tech is now in a secular bear market. I agree with him, only because I can’t really work my iPhone (I claim it’s not really user-friendly), and because I think playing with Facebook is a royal pain.

Hickey, by the way, is a huge fan of gold and the gold mining stocks. But don’t get me wrong about tech, I love Amazon and Google, and I love the Internet. I think the Net has changed the world. It allows almost everyone on earth to know what’s going on in the rest of the world, and we know that “the truth will set you free.” Every dictator loathes and fears the Internet, because the Net allows people to know what’s going on. Why even North Korea is showing signs of crumbling, not only because of the Internet — but because their newest boy dictator was educated in Switzerland.

Yesterday, the Dow almost made it to its May 1st peak, but at the close they sold the Dow off. The Transports still have a way to go before they can close above 5285.97. What will I do if both D-J Averages do close above their May peaks? In that case, the facts will have changed, and I’ll change with them. There’s nothing stupider in this business than an analyst who dreams up a scenario and who sticks with his scenario no matter what. I often have a scenario, and as long as the markets go in harmony with my scenario, I’ll stick with it, but when the facts change I revise or jettison my scenario — to do otherwise would be idiotic.

I may appear fussy in my insistence that the two D-J Averages close above their May peaks, but whether they do or do not could be unbelievably important.

….read mor from 84 Year Old Richard Russell HERE

The following is an excerpt from Richard Russell’s Dow Theory Letters

Two days ago, amid all the low volume and sluggishness, the Transports gave us just a hint of something hopeful. It was a breakout of the declining trendline, as you can see on the chart. The Transports have been the laggers all year, and it seemed as though if the Industrials closed above their May peak, the Transports would not confirm. Now with this little upside breakout, the Transports are giving us a ray of hope. Maybe, just maybe, the Transports will add on a few more point, and get in the game.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair