Timing & trends

Knowing that it’s very likely that Gold and Silver have bottomed, we feel it is time to look at the charts and assess what may or may not be in store over the next year or two.

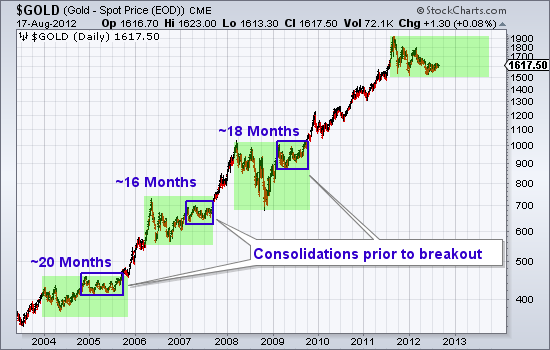

Gold has consistently made impulsive advances that were digested by multi-quarter corrections and eventually followed by a breakout and new impulsive advance. Following the last major breakout in late 2009, Gold enjoyed an extended impulsive advance that lasted two years. Previous impulsive advances lasted less than a year. Gold, having bottomed, remains well entrenched in another consolidation that is 12 months old. As we can see from the chart, previous consolidations lasted 16 to 20 months.

It is important to note that previously Gold, within a year was able to rally back near the recent impulsive high. In other words, Gold is currently in a much weaker state relative to past consolidations. Gold will need to rally back to $1800 or $1900 and that would be followed by a multi-month consolidation that would lead to a breakout. Conservatively speaking, over the next 12 months we could see a rally back to $1900 and a final consolidation.

Meanwhile, Silver continues to consolidate and digest the two and a half year advance from $8 to $49. Predictions of $60 or $70 Silver are absurd and fail to account for the lengthy consolidation that is needed to reduce supply and position the market for not only a retest of $50 but an actual breakout. Silver is a commodity with real world supply and demand dynamics. It will be a while before producers won’t sell for $35-$36 and before buyers consider $35 a bargain. That being said, the near and medium term outlook is quite compelling. Longer-term, the market is in a giant cup and handle pattern (dating back to the high in 1980) and this correction and consolidation is the handle. A powerful breakout past $50 in, say 2014, could push Silver towards its bubble phase.

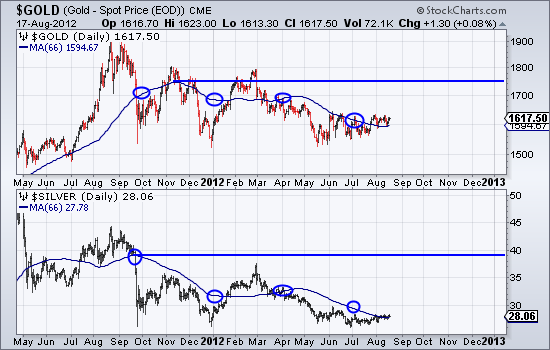

The fact that Gold and Silver are unlikely to break to new highs anytime soon hardly deters me in my bullish enthusiasm for select gold and silver stocks. Key word being select. I’m not bullish on every mining company but I digress. In the chart below I use a 66-day moving average to plot an average quarterly Gold and Silver price. I also circle the moving average at the end of quarters.

Note that the quarterly high prices for Gold and Silver are roughly $1750 and $39 and far off from the 2011 highs. The quarterly averages are starting to turn up. Well run companies with production increases could very well move to new highs when Gold returns to $1750 and Silver moves past $35. We do think most of the Gold and Silver shares can breakout to new highs ahead of the metals. In other words, the mining shares at large will ultimately challenge for a breakout ahead of Gold and Silver reaching new all time highs. If you’d be interested in our professional guidance and uncovering the producers and explorers poised for big gains, then we invite you to learn more about our service.

Good Luck!

Jordan Roy-Byrne, CMT

Jordan@TheDailyGold.com“>Jordan@TheDailyGold.com

One of the top stories in the financial markets in 2012 has to be the stagnation in the price of gold at around $1600 an ounce, which is down approximately 17% from its peak at $1920.30. Those bullish on the yellow metal have been disappointed in gold’s performance while those bearish on the shiny metal have reveled in its stagnation, saying that gold’s status as a safe haven is over.

What is behind gold’s sluggish performance in 2012? There are several reasons, but one of the key fundamental reasons has been the lack of demand from traditionally the largest buyer of gold on the planet – India (although China will surpass it this year). India bought only 181.3 tons in the second quarter of 2012, a 2-year low, according to the London-based World Gold Council.

There are several factors at play as to why Indian demand for gold has fallen. One reason is the sharp drop in the value of its currency, the rupee, which is down by 25% versus the U.S. dollar this year. This decline has kept gold prices high in relative terms while the actual dollar value of gold was falling. Perhaps even more important has been the ‘war’ declared on gold by its central bank which has blamed all of the country’s economic ills on Indian citizens’ traditional buying of gold. In an attempt to slow down gold and silver imports, the Indian government has imposed new taxes on the purchase of these precious metals.

But even though demand for the precious metal is way down in India, the situation still offers hope for gold bulls. Why? Because we’ve been here before – in 2009 to be exact. In early 2009, the Indian economy and rupee tanked. Gold demand almost completely dried up. According to precious metals consultancy GFMS, Indian demand for gold in the first quarter of 2009 collapsed by 77%. For the full year GFMS said Indian consumption dropped by 19%.

Now with the Indian economy slowing to its weakest growth rate in nearly a decade and the rupee falling, we are seeing a replay of 2009. The monsoon season has been poor, hitting farmers – among the biggest buyers of gold – hard. Gold prices have hit a record high in rupee terms, and India is expected to purchase, as forecast by the World Gold Council, only 750 tons of gold, down 25% from 2011 levels. Meanwhile, the WGC forecasts that China will buy 850 tons of gold this year.

Investors should pay heed to the clues that recent history is giving us. The drop in Indian demand is simply a cyclical phenomenon due to the lousy state of the Indian economy. It will recover eventually. And when it does, look out for the fireworks from renewed Indian demand for gold added to the Chinese demand. In 2010, as pent-up demand for gold was unleashed, Indian gold consumption soared 74% to a record high of 1,006 tons according to GFMS.

Gold bulls surely hope we see something similar in 2013 and that is exactly what I talked about last week based around gold miner stocks and also what Dave Banister’s recent gold forecast was about at TheMarketTrendForecast.com sees in 2013.

Gold Chart Showing 2009 Collapse and Outcome and Current Gold Price Analysis:

Gold Trading & Investing Conclusion:

In short, gold and gold stocks have a lot of work to do before they truly breakout into the next major leg higher. I feel we are nearing that point and they may have bottomed already. Starting a small long position to scale in I think is a safe play. But I would only add more once the trend actually turns up and shows strength in terms of price and volume action.

If you would like to get my weekly analysis on precious metals and the board market be sure to join my free newsletter at www.TheGoldAndOilGuy.com

Chris Vermeulen

Choppy, sideways and range-bound — at this point, investors are probably well-accustomed to hearing silver described that way. Silver market action has been largely lackluster of late, and some market participants may be growing nostalgic. Although the white metal has not broken out in either direction, there was an interesting development in its price action this week. On Monday, Tuesday and Wednesday, silver’s closing New York spot price was exactly the same: $27.83.

Hedge funds are the least bullish on silver in four years, according to Bloomberg, and speculative bets for higher prices have been cut by 72 percent since February

Silver appears to encounter resistance in the range of $28.30 to $28.40. There is solid resistance at the July high of $28.44. A close above this level could allow for an upside breakout.

….read the whole article HERE

Market psychology: One of my all-time favorite market quotes is from the 1987 movie Wall Street wherein Gordon Gekko declares that, “Money itself isn’t lost or made, its simply transferred from one perception to another.” Well perceptions have certainly changed…three months ago the market was very worried that the European financial crisis would spin out of control with contagion hitting all global markets…now fear is greatly reduced…especially since Draghi made his famous, “Whatever it takes,” statement on July 26…and that change in perception has shown up across asset classes.

Stocks: since the Key Turn Date and Key Weekly Reversal of June 4 theDJI has closed higher 9 out of 11 weeks, is up 1175 points (~10%) and closed this week at its highest weekly close since 2007. Since Draghi’s comments the major North American stock indices have risen ~5%, the German DAX is up ~11%, the UK FTSE is up ~7%, while Spanish and Italian stock indices are up ~25%!

VIX: the “fear” index, closed this past week at a 5 year low down ~50% from its June 4 Key Turn Date.

US and CAD interest rates: have risen sharply across the curve since Draghi’s comments while Spanish and Italian bond yields have fallen sharply.

Gold: implied volatility is near its lowest point of the past10 years…gold has been trading in a narrower and narrower range over the past 4 months…breakout ahead?

Crude: WTI hit a low of $78 on June 28…it’s now $96 up ~23%…Iran/Israel fears?

TSE: up 200 points on the week, up 755 (~6.5%) points since the June 4 lows.

Apple: hit a new all-time-high this week (up ~13% since Draghi’s statement) with a market cap of over $600 Billion. To put that market cap in perspective….it’s ~$200 Billion more than 2nd place Exxon, it’s double the market cap of third place Microsoft…double the combined market cap of Canada’s top 5 banks.

Royal Bank: closed at a 3 month high up ~16% from the June 4 lows…the broad US Bank Share Index is up ~15% from the June 4 lows.

CAD: is up over 5 cents from its June 4 lows at a 3 month high above 101.

Volume: share trading volume has been on a declining trend for the past few years and 2012 is on track to register the lowest annual volume in 15 years. This past week appears to be the lowest weekly volume in years…and it felt like it…summer doldrums in spades! (As an aside…the declining trading volumes and low interest rates are a double-whammy hitting the stock brokerage business…brokerage firms are losing money…expect consolidation across the industry.) If there is an Achilles heel to the recent stock market gains it may be that the rally has been on very light volume.

Money is mobile: Prices change as perceptions change…and as perceptions change money moves from one place to another…it moves from the center to the periphery…and back…from the “old reliable” to the exotic…and back…from low beta to high beta…and back…from New York to emerging markets…and back…from low yields to high yields…and back. A change in perceptions shows up across asset classes…in some sooner than others…in some more dramatically than others…by watching how these asset classes move relative to one another you can get a sense of how market perceptions are changing…you can find trading opportunities that “go with the flow.”

Trading: my theme for the past several weeks has been that, “this market wants to go higher.” I will maintain long positions in

“We see no reason why this gold trend cannot perform as well as the last bull market in gold between 1970 and 1980.” A replication of that move, “will take gold to $6,300.”

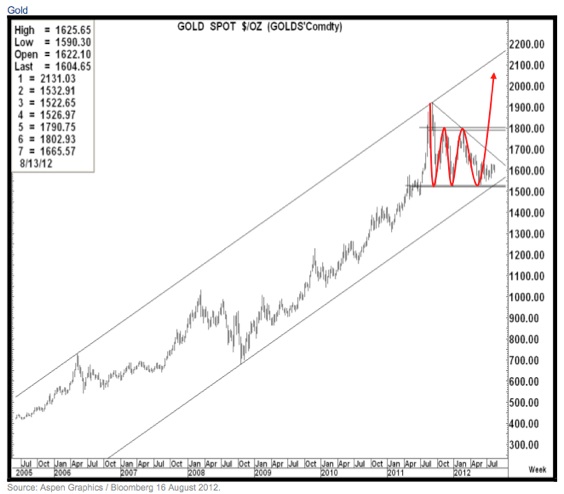

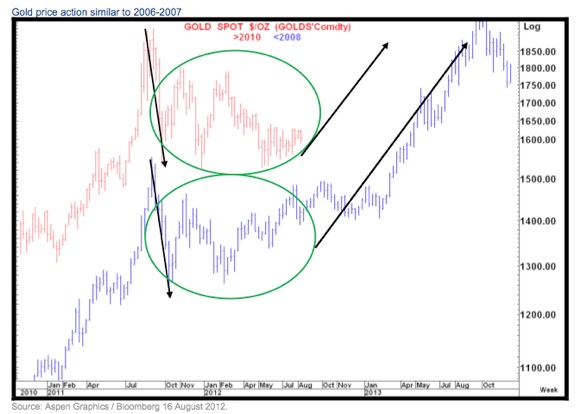

“The longer gold consolidates, the more we believe it sets up the platform, like 2006/2007, for the move higher. Certainly if we start to get a move up through $1,640 to $1,650, it looks to us like the upside move is finally starting, particularly if we can push through that $1,790 level. When the move kicks in, we think it will be a very quick move to the topside. When we look at the move in 2006/2007, if we follow that trajectory it should take gold up towards $2,400″.

More from Tom Fitzpatrick’s latest report:

“Gold still remains above the supports in the $1,520 area which the market has tested three times over the past year. The parallel of the trend across the highs also comes in here (currently at $1,532). The first resistance level to watch is $1,665 which is the trend line down from the highs and a rally through there would amount to at least a short term bullish break (see chart below).

Important resistance above there is at $1,790-$1,802 which marks the double (or triple) bottom neckline and a breach of that opens the way for new trend highs (see chart below). The price action here reminds us of what was seen in 2006 after Gold corrected down from $730 to $542 (a more aggressive correction then in percentage terms than the one seen since last year’s high). The market spent a long time consolidating but ultimately rallied to new trend highs in the second half of 2007 (as the credit and banking crisis worsened).

New highs (for gold) in 2013 (if we follow the pattern below)?

Brent (see chart below) has continued to push higher this week and is above the resistance area around $113 where we saw the previous rising trend line (which became resistance) and the 61.8% Fibonacci retracement of the fall from the Feb high.

A weekly close above here would suggest higher levels towards $119 (76.4% Fibonacci retracement) and possibly the trend highs again at $127-$128. The real concern here is that a breach of $127-$128 would be a major break opening the way for the 2008 high at $147.50 which is $31 (26%) above current levels.

Having seen the ‘shaky’ US (fundamentals) and keeping in mind that Europe is still in severe economic turmoil in addition to a slowdown elsewhere (especially China), it is difficult to see a rally in Crude of this magnitude coming from a demand side dynamic. We therefore have to entertain the idea that either Brent will not rally back to $147 or that a supply shock may take it there.

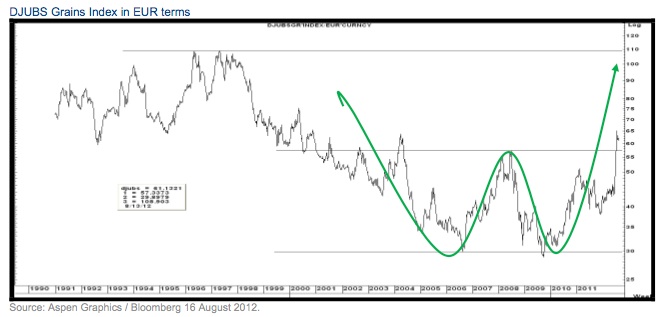

Grains

The minimum target on this double bottom (linear) would be a move towards 85 with a percentage change target suggesting as high as 108- Close to the major peaks posted in 1996-1996 (see chart below).

Overall:

We see the danger of further gains in Oil (particularly Brent) possibly by as much as $30+. Food prices have risen aggressively and there are few, if any, indications of a turn in trend. Economic commodities such as metals continue to look weak with breaks already having taken place on the LME Index and Aluminum and key support levels on sight for copper.

Bottom line:

1. What we have to pay for is rising in price.

2. What we choose to pay for is falling in price reflecting stresses on the consumer and businesses alike. This is not a positive dynamic in a very uncertain environment.

3. Over time the outperformer will be a “currency” rather than a commodity (Gold) as major central banks react to the first two and the economic stresses associated with the dynamics there.

The most concerning charts here are those on Oil which we fear will break higher and ultimately create a negative feedback loop that could at some stage become a negative backdrop for equities. Europe will suffer most given their economic fragility and currency weakness.”

Fitzpatrick also told King World News, “If we were to repeat the 1970 to 1980 move, in percentage terms, that would put a target as high as $6,300, which I mentioned earlier. However, that incorporated a surge late in the trend in ‘79’-’80, which included a Russian invasion of Afghanistan. Absent that move, the trend seen at that time would still give us a move on gold to $3,400.”

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair