Gold & Precious Metals

EB: With more monetary easing by central banks around the world – where do you think valuation will be skewed? Which stock markets are going to be most prone to ‘bubble-like’ characteristics?

MARC FABER : Given that given that zero interest rates are in the US in nominal terms and if I take say a more realistic view of cost of living increases. Last week, NY taxi prices went up 19%. If I consider that, I think that US stocks may for the time-being actually rally but I have doubts that they will rally above the highs at 1422 we saw in April of this year on the S&P.

I think that it’s possible that the US may rally as the whole world thinks that the US has natural gas and there will be a re-industrialisation in America. The mood amongst international investors is that the US is the least bad choice.

I’ve always said if you give me the choice to buy a 10 year treasury at the yield of 1.5% or Johnson&Johnson, I’d rather buy Johnson&Johnson with a ten-year view. But as I said, if I look at all the options that I now have, I can see that European stocks are now terribly depressed.

I still own Asian shares and again the reason I own them is we have next to zero deposit rates and my portfolio of Asian shares has an average yield of say 5-6%. If I look at my investments, I think that they might go down 30% but I don’t think there will be massive dividend cuts – some here and there but not across the entire portfolio.

I still keep a lot of cash because if the markets drop another 30% – which I hope they will do – I will then invest in equities. – in citywire

The U.S. Dollar Index added 0.17 (0.21%) last week. Intermediate trend is up. Support is at 81.16 and resistance is at 84.10. The Dollar remains above its 200 day moving average and below its 20 and 50 day moving averages. Short term momentum indicators are trending down.

Ed Note: Don’s Monday Site is well worth visiting HERE

Economic News This Week

July Producer Prices to be released on Tuesday at 8:30 AM EDT is expected to increase 0.2% versus a gain of 0.1% in June. Core PPI is expected to increase 0.2% versus a gain of 0.2% in June.

July Retail Sales to be released on Tuesday at 8:30 AM EDT are expected to increase 0.3% versus a drop of 0.5% in June. Ex autos, July Retail Sales are expected to improve 0.4% versus a decline of 0.4% in June.

The August Empire State Manufacturing Index to be released on Wednesday at 8:30 AM EDT is expected to slip to 7.2 from 7.4 in July.

July Consumer Prices to be released on Wednesday at 8:30 AM EDT are expected to increase 0.2% versus no change in June.

July Industrial Production to be released on Wednesday at 9:15 AM EDT is expected to increase 0.5% versus a gain of 0.4% in June. July Capacity Utilization is expected to increase to 79.2 from 78.9 in June.

July Housing Starts to be released on Thursday at 8:30 AM EDT are expected to slip to 752,000 from 760,000 in June.

August Philadelphia Fed to be released on Thursday at 10:00 AM EDT is expected to improve to -4.0 from -12.9 in July.

August Michigan Consumer Sentiment to be released on Friday at 9:55 AM EDT is expected to slip to 72.2 from 72.3 in July.

July Leading Indicators to be released on Friday at 10:00 AM EDT are expected to increase 0.2% versus a 0.3% decline in June.

The Euro fell 0.87 (0.70%) last week. Intermediate trend is down. Support is at 120.42. The Euro remains below its 50 and 200 day moving averages and above is 20 day moving average. Short term momentum indicators are trending higher.

The Canadian Dollar added 1.03 cents U.S. (1.03%) last week. Intermediate trend is neutral. Support is at 95.76 and resistance is at 102.05. The Canuck Buck remains above its 20, 50 and 200 day moving averages. Short term momentum indicators are overbought, but have yet to show signs of peaking.

The Japanese Yen added 0.45 (0.35%) last week. Intermediate trend is down. Support is at 124.12 and resistance is at 128.77. The Yen remains above its 20, 50 and 200 day moving averages. Short term momentum indicators are trending down.

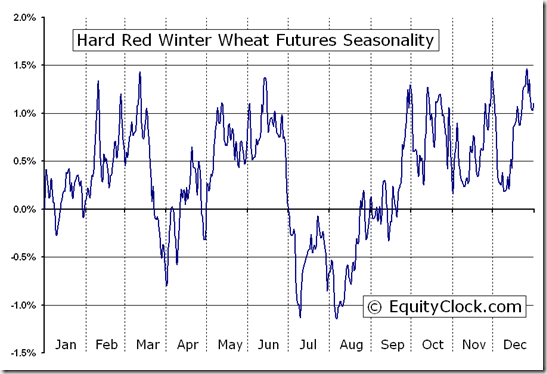

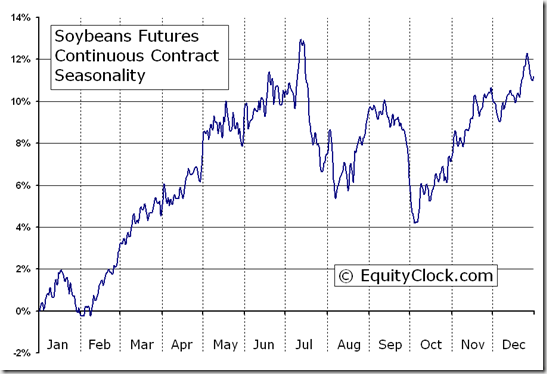

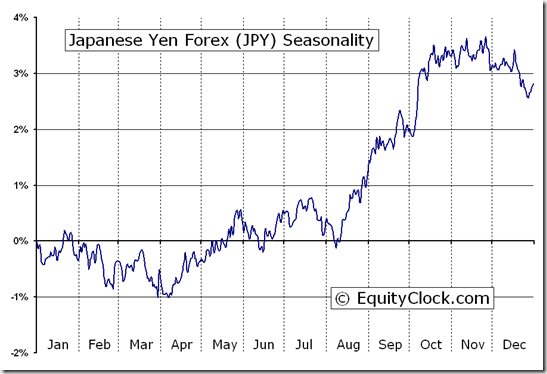

Seasonality refers to particular time frames when stocks/sectors/indices are subjected to and influenced by recurring tendencies that produce patterns that are apparent in the investment valuation. Tendencies can range from weather events (temperature in winter vs. summer, probability of inclement conditions, etc.) to calendar events (quarterly reporting expectations, announcements, etc.). The key is that the tendency is recurring and provides a sustainable probability of performing in a manner consistent to previous results.

Identified below are the periods of seasonal strength for each market segment, as identified by Brooke Thackray. Each bar will indicate a buy and sell date based upon the optimal holding period for each market sector/index.

Two weeks ago I told you that August would see dramatic trending moves, and that we wouldn’t have to wait long for them to unfold.

Well, they’re here NOW. Nearly all markets are pressing extreme resistance levels in what most traders and investors believe are breakouts.

They see a surge in gold, and think it’s going to march to new record highs well-above $2,000 an ounce.

They see a modest rally in silver, and think they should load up the truck, expecting silver to surge to $50 and higher.

They see a rally in oil, and figure that all must be well with the global economy and that higher energy prices are a fait accompli.

They see grain prices surging, and figure rampant inflation will soon hit food prices.

And they see the Dow Industrials hanging in there nicely above the 13,000 level — and expect a new bull market in stocks.

Mind you, ALL of the above WILL happen.

- Gold will soar to at least $5,000 an ounce.

- Silver to well over $100 an ounce.

- Oil to new record highs near $200 a barrel.

- Inflation surging.

- And the Dow Industrials will soar in a new bull market, to at least 21,000, if not much higher.

But none of that is in the cards for right now. It’s not time. The moves I mention above WILL happen, but not for at least another six months, give or take.

Instead, nearly all markets will soon turn back down, taking with them the most-optimistic of investors precisely at the wrong time.

You see, all markets have one underlying rule that always seems to govern their broad behavior: At market extremes, inflict the most amount of damage upon the most investors. Take them to the woodshed and spit them out like sawdust; then go find another group of investors and start the shredding process all over again.

Don’t get me wrong. That doesn’t mean you can’t make money in the markets. It does, however, mean that you must always keep your guard up … and more importantly, know when to be a trend-follower versus a contrarian.

And right now, it is my humble, 34 years of experience that’s telling me it’s time to be a contrarian.

Not just my gut, but also all of my technical and cyclical indicators.

For one thing, though gold seems to be pressing higher and could move even higher in the short term — as I recently pointed out — gold would have to close above $1,727.70 to prove me wrong and turn the short- and intermediate-term trends back to bullish.

I see very little chance of that happening and, instead, I sense that gold is about to inflict a lot of damage on the majority of investors and stage a stunning collapse.

Silver is about to do the same. While it could press a bit higher, silver would have to close above $30.71 to reverse the short- and intermediate-term trends. Short of that, silver will pummel a lot of the investors who are now venturing in to buy “the devil’s metal.”

Oil, too, is about to hurt a lot of investors and traders. While it’s managed to rally to the $94 level, it also is on the verge of turning back down — taking with it all those investors who think energy prices have nowhere to go right now but up.

Grain prices are topping as well. So is inflation in the short term.

And the Dow Industrials — though clearly showing their propensity to begin a new bull market — are getting very toppy.

Momentum indicators are slowing. The number of advancing stocks versus those declining is beginning to wane quite dramatically. And the Dow Transports have thus far entirely refused to confirm the rally in the Dow and the S&P 500, creating a hugely BEARISH non-confirmation.

I would love to tell you that new bull markets are here in all of the above, but they’re not. Each and every one of the above markets needs more time to form the foundation for their next bull legs higher.

They need to back-and-fill support areas on their charts. And most importantly, they need to take the majority of investors out to the woodshed for a shredding. Then, and only then, will they have a chance to begin anew.

Ironic, but once those declines occur, you’ll find almost everyone will become a giant bear. Precisely near the bottom of the corrections.

Nearly everyone but me. Because when that happens …

When you see gold fall below at $1,500 …

When you silver fall at least below $23 …

When you see oil plummet like there’s no tomorrow …

And you see the Dow Industrials melting in a 2008-style plunge …

I’ll be backing up the truck and telling you to buy almost everything with both hands.

What are the chances I’m completely wrong in my analysis? I’d rate them as very low, say around 10%.

And if it turns out I am wrong, I don’t have a problem with it. With gold ultimately heading to over $5,000 … silver to over $100 … oil to near $200 … and the Dow Industrials to at least 21,000 …

There will be plenty of money to be made.

Bottom line: For now, dis-inflation still has the upper hand in most markets. There’s still too much bad debt in the world that hasn’t been dealt with.

And the Federal Reserve and the European Central Bank will NOT act until the pain is too much to bear. That pain is on the horizon, so in the interim, just make sure you’re out of harm’s way.

I repeat my advice of two weeks ago:

If you’re an investor with an eye to the long term, continue to preserve your ammo and hedge the positions that, for whatever reason, you can’t get out of. The time will come to add to your long positions — but it’s not here yet.

If you’re a short-term trader, don’t be frustrated by the recent choppy markets, or any short-term losses you may have experienced. Stay the course.

Best wishes,

Larry

P.S. I’m hard at work on the next issue of my Real Wealth Report, which publishes on Friday. To be among the first to find out how I’m planning to fully seize profit potential in the markets for the rest of the year, be sure you’re signed up to get your copy. Activate your risk-free trial subscription bysimply clicking here now!

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair