Gold & Precious Metals

- The total amount of Silver ever mined would fit inside a Football Stadium.

- There are two major sources of yearly Silver production, recycled scrap and new metal production: 25% of yearly Silver production comes from recycling. 50% is mined as a byproduct of lucrative metals such as Gold, Copper and Zinc. with only 25% of yearly Silver production coming from primary Silver mines. This is changing with today’s high Silver prices many new Silver deposits have become economical to mine as a primary metal.

- Political and Economic conditions in areas where you can mine primary Silver has a large effect how much it costs to mine and correspondingly how much of it gets produced. In 2011 both increased Mexican electricity rates and increased Labor costs in Peru drove up the cost of Silver production.

Many more fact about Silver Supply and Demand beginning at the 1:30 mark of the 5 minute video below:

Ed Note: There is another video at Endeavour Silver’s website HERE called “The Silver Market and Inflation”. I could not find part 11 of “Supply and Demand”.

This group of stocks has paid reliable dividends for over 20 years. One of my favorites in this space has paid over 144 consecutive dividends and raised its payout for 37 straight years.

They’re the creme de la creme of the income universe. (Ed Note: The Tax friendly equivalent in Canadian Stocks, like Penn West Petroleum @ 8.33%, Sun Life Financial @ 7.11%, Enerplus @ 15.13% and TransAlta @ 7.18% are at S&P/TSX 60 best Dividend Yielding Stocks.)

Each one has increased its dividend every year for at least two decades… some sport track records with over 50 years of consecutive dividend increases.

All told, these stocks are some of the most reliable dividend payers on the planet.

I’m talking about the S&P 500 “Dividend Aristocrats” and their kissing cousins, the S&P “High Yield Dividend Aristocrats.”

In order to become a member of these elite groups, a company must not only pay a regular dividend, it must also enjoy a stellar track record of growing that dividend every year for at least 20 years.

With such stringent membership criteria, only about 70 U.S. companies make the grade. (Ed Note: Given the amount of money tied up in the Bond markets dwarfs the amount tied up in Stock markets, if investors start start looking for safe higher North American yields, those few high quality dividend stocks are going to be an attractive candidates. With the US 10 Year Treasury Note at hitting a low of 1.3908 % in the last 24 hours, and the equivalent Spanish 10 Year Bonds jumping to a new high of 7.52% on monday , its clear that fears of a wilting economy and Government finances can drive investors to look for something else to invest in besides government Bonds).

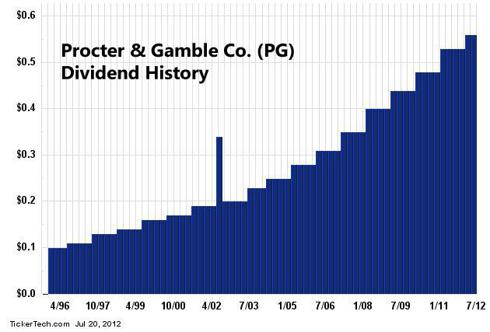

As you’d expect, a wide variety of industries are represented. You’ll find an overweighting of consumer staples such as Procter and Gamble (NYSE:PG)

and Kimberley Clark (NYSE: KMB), and a healthy chunk of electrical utilities, such as Consolidated Edison (NYSE: ED) and Northwest Natural Gas (NYSE: NWN).

But there’s one group that makes the list that you would probably never expect: insurance.

All together, six of some 70 aristocrats sell insurance. Even more interesting, five of these six companies are property and casualty insurers. The exception is Aflac, which is mainly a life insurer.

What is it about property and casualty insurers that allows them to keep increasing their dividends in good times and bad for at least a quarter of a century?

The answer surprised me. Here’s what I found out…

Today, insurance is usually life or non-life, also known as property and casualty.

Property insurance covers loss or damage to physical property, such as houses and cars. Casualty insurance covers the legal cost if the insured person were to cause someone else physical injury or damage another’s property. Liability insurance is a common example.

You might expect property and casualty insurers such as Dividend Aristocrat — RLI (NYSE: RLI ) — to be cash-flow machines… churning out streams of highly predictable earnings quarter after quarter.

Nothing is further from the truth.

Their earnings streams are notoriously volatile. Major unpredictable risks, such as natural disasters, have a huge impact on earnings.

So why do I like property and casualty companies then? As in all industries, some companies far outperform others. RLI is one of them — as measured by the combined ratio, the key industry metric of underwriting profit.

The combined ratio combines two metrics. It measures underwriting expenses as well as the amount paid out in claims, both as a percentage of net premiums earned.

A combined ratio of 100 means the company is breaking even on its underwriting activities. The lower the ratio, the higher the company’s underwriting profit.

In 2011, RLI’s combine ratio was an outstanding 78.4… Well below the industry average of 107. RLI has seen sixteen straight years of underwriting profitability, with an average combined ratio of 87 over the period.

And while property and casualty companies may break even or lose money on their underwriting activities, that is only part of their financial story.

These companies accumulate millions and even billions of dollars of investment capital, which provides investment income that makes a vital contribution to their per-share earnings.

For example, RLI earns investment income and realizes gains from a $1.9 billion portfolio, comprised 74% of high-quality debt with an average “AA” credit rating, and 26% in equity.

Given that the investment portfolio comprises the lion’s share of earnings, management’s decision on whether or not to realize capital gains or losses by selling investments can cause tremendous earnings volatility from year to year.

How can volatile earnings grow dividends?

First, insurance companies keep their payout ratio relatively low, so it can inch up the dividend regardless of earnings. RLI had a payout ratio of 25.0% of in 2009, 19.2% in 2010, and 19.5% in 2011.

Meanwhile, insurance companies keep building shareholders’ equity, which they can dip into on a temporary basis to supplement the dividend if there were a short-term earnings shortfall.

That’s one reason RLI has been able to pay a dividend for 144 consecutive quarters and raise its ordinary dividends for 37 consecutive years.

For the past two years, the insurer has also returned excess earnings to shareowners in the form of one-time special dividends. In 2010, the special December payout was $7 and in 2011 it was $5.

Over the past four quarters, the company paid out $1.14 in ordinary dividends. Factoring in last year’s special dividend, shares of RLI provide a remarkable yield of 9.8% at today’s price — an outstanding yield for a member of the “Dividend Aristocrats.”

Of course, as with every investment, there are risks to be considered. If management decides to break with its two-year policy of paying out a special dividend from excess capital, the stock would no longer be suitable as a high-yield income play.

But that said, many insurance companies have a surprisingly good track records when it comes to dividend payouts. If you’re looking for a high-yield stock with a reliable dividend track record, then an insurer like RLI may be suitable for you.

[Note: For more high-yield ideas, make sure to watch the latest presentation StreetAuthority’s research team recently put together. In it, they’ve identified 5 of the best income stocks for the next 12 months. To learn about these stocks, click here now.)

Good Investing!

![]()

Carla Pasternak’s Dividend Opportunities

P.S. — Don’t miss a single issue! Add our address, Research@DividendOpportunities.com, to your Address Book or Safe List. For instructions, go here.

Mark Leibovit has been bullish the Stock Market for awhile, and if you’ve been following his Platinum trading service, it certainly hasn’t hurt him to have been Bullish.

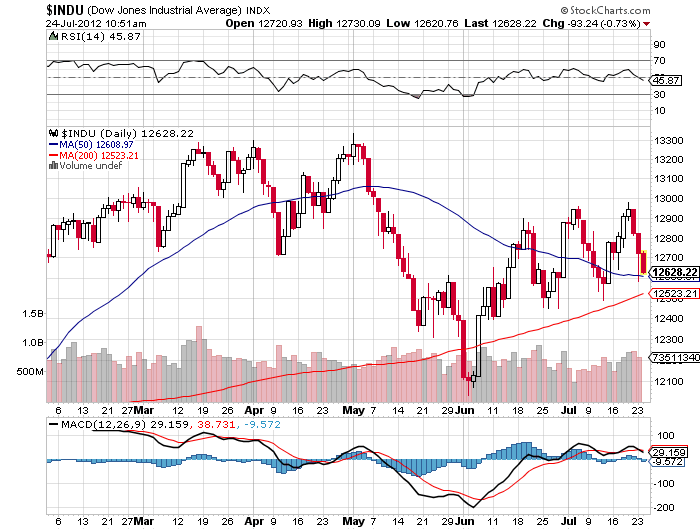

Now, that the S& P 500 has sold off 50 points from its recent high of 1380, Mark thinks we are at an crucial juncture. Specifically, the two previous 50 point selloffs from the June10th and July 3rd S&P 500 peaks have defined a clear line at 1330 (it touched 1329.24 today then rallied). If that line at 1330 is broken with authority he thinks that will signal that the S&P 500 is heading down more than double the previous corrections. Or another fat 63 points to the June 4th low of 1267 “and possibly well beyond” . No wonder he’s warning about a potential for a big decline. Just a quick glance around and you’ve got Ben Bernanke’s talking before Congress about the Fiscal Cliff the US is facing, while any one of 3 major European countries could plunge over a Fiscal Cliff in the blink of an eye. “We could be looking at another ‘Flash Crash‘ type scenario” – Mark Leibovit

(Mark continues below the chart).

A bit more from Mark on the market’s health:

“Volume increased to the downside yesterday and, as you know, Apple (AAPL) which has been long viewed as a surrogate for the current bull market disappointed the Street with last night’s earnings report. Earlier in the day, Tim (I don’t pay my taxes) Geithner put out a sound bite stating he’s optimistic the government won’t trip over the so-called “fiscal cliff” because, “I also think you’re seeing people show more realism about what is necessary” to avoid a fiscal crisis. The markets seemed to like this. Separately, the Wall Street Journal’s Jon Hilsenrath reported to have a source which says the Fed will act as soon as next week to stimulate the US economy. This was a surprise and was most likely the force that took stock indices well off there lows in late trading today”.

“We all know the truth. They only have one weapon. It’s called the printing press (or perhaps an electronic printing press that automatically moves newly created ‘money’ into the checking accounts of targeted banks or corporations). More and more printing could be ignored by the market which is far more powerful than any central government. To the best of my knowledge the European Central Bank does not have the equivalent of a Plunge Protection Team or an Exchange Stabilization Fund allowing them to manipulate European stock markets. And, even so, money printing has been secretly going on behind the scenes for months and yet the financial crisis in Europe and the debt burden of U.S. cities, states and the U.S. government itself continues to grow and grow. This is primarily due to the reduced level of revenue from a slowing economy and from businesses who are reluctant to expand in an uncertain political and tax environment. I fear we could be looking at another ‘Flash Crash’ type scenario. I hope I am wrong and the traditional ‘seasonal’ tendency for another rally try into the U.S. Presidential election is still an option. I hope this because I stuck my neck out with the ‘BULL’ call into the election – one that I made late last year! In truth, the rally could have ended on April 2 and we’re now headed into oblivion. For this reason, I have limited our exposure to the markets to a few selected trades in our Current Portfolio. As I told you yesterday, the overall picture doesn’t appear very rosy with Spain, Italy and possibly France next ready to go over a financial cliff and the potential to see both the U.S. Dollar Index and the Euro both trade at par (100) in coming months cannot be discounted in this kind of environment.”

In short, Mark is very cautious here, I imagine it’s because he’s thinking what Greg Weldon is thinking. That “Never has there been been a more critical fiscal or political situation. No one can really debate the fact that the fiscal future of the US hangs in the balance”

The one big factor we can be sure will move the markets powerfully is the Fed coming forth with QE3. Marks comments about the “Plunge Protection Team” and the “Exchange Stabilization Fund” underscore what Greg Weldon told Mike. “That when push comes to shove, and we stare into that deflationary abyss, every central banker in the world will choose to reflate no matter what the cost because they think that they can deal with reflation better. In their minds its preferable to the pain of deflation. That’s the bottom line.

It sure will be an interesting next week, if as Mark Leibovit say’s above “the Wall Street Journal’s Jon Hilsenrath reported to have a source which says the Fed will act as soon as next week to stimulate the US economy”.

Hang on to your hats! At the time of this writing its 12:38 am PST and the S&P September Futures are trading down 2.25 points or the equivalent of 1336 on the cash S&P 500.

Mark Leibovit’s Gold Letter, # 1 Gold Timer for 10 year period & #2 Gold Timer for 2011

IF YOU HAVE NOT SIGNED UP FOR THE LEIBOVIT VR GOLD LETTER, HERE IS YOUR CHANCE. HERE IS THE LINK: WWW.VRGOLDLETTER.COM. YOU GET A 50% DISCOUNT FOR THE FIRST MONTH.

VRTRADER.COM Trial Signup:

THE RENEWAL OF YOUR SUBSCRIPTION IS AUTOMATIC. YOUR CREDIT CARD WILL CONTINUE TO BE BILLED UNLESS YOU NOTIFY VRtrader.com SEVEN DAYS PRIOR TO SUBSCRIPTION EXPIRATION EITHER VIA EMAIL POSTING THE WORD ‘UNSUBSCRIBE’ IN THE SUBJECT BOX OR TELEPHONE US AT (928) 282-1275 OF CANCELLATION. NO REFUNDS ARE AVAILABLE ON SILVER, PLATINUM OR VR FORECASTER (ANNUAL FORECAST MODEL) SUBSCRIPTIONS.

Welcome and congratulations on choosing VRTrader.com as a source for your stock market commentary, information and analysis for the U.S. Stock Market. Needless to say we are very happy that you are joining us for AT LEAST the next 30 days days and look forward to providing you rewarding and inciteful information that will help you toward your goal of succeeding in the markets.

Here is the Special Trial Offer: Use this month to kick our tires. Pay 50% for the first 30 days (No refund) and sample our Silver or Platinum service and then decide what works best for you. If you aren’t 100% ready to move forward, simply email us to cancel one week before your 30 day 50% off trial subscription ends and it will be canceled and you will not be charged ANY FURTHER, no questions asked. Just send an email to mark.vrtrader@gmail.com” or call 928-282-1275 to cancel. You will receive an emailed confirmation of your cancellation at that time.

The 30 day trial is allowed one time only. By taking this 30 day 50% trial, you agree to be charged the full cost of the monthly Silver or Platinum service (choose one only) at the end of the 30 day trial subscription period, unless you cancel first. The regular Silver monthly rate is $49.40 and the Silver quarterly rate is $133.50. The regular Platinum monthly rate is $129.95 and the Platinum quarterly rate is $350.85. The special trial 50% off trial rates are listed below. Sign up today!

There are no refunds or pro-rata refunds offered at VRTrader.com for any subscription. You are being offered a 50% discount for trying our service for the first 30 days only!

THE WORLD IS HURTLING TOWARD A DAY IN WHICH MONEY WILL AGAIN BE BACKED BY GOLD OR OTHER HARD ASSETS. UNTIL, THIS ANALYST SEES PLENTY OF TROUBLE.

“Hear Me Now, Believe Me Later,” was the title of two separate and prescient pieces penned by Pomboy, an economist and founder of the MacroMavens research boutique. One, published in March 2006, foretold the disastrous costs of the housing bubble. The second, somewhat later, laid out the consequences of the bubble’s “financial echo.” Today, Pomboy predicts something more draconian: the demise of fiat money—currencies that aren’t backed by anything other than government decrees that they have value.

We checked in with her last week, as central banks around the globe weighed more easing and as Fed chief Ben Bernanke described to Congress the headwinds facing the U.S. economy, including the automatic tax increases and spending cuts set for year end, called the “fiscal cliff.” With the Fed being the biggest buyer of Treasuries, Pomboy thinks the 40-year-old fiat system will crack within five years.

Barron’s : What don’t investors anticipate today?

Pomboy: That the Fed will be a presence in the Treasury market for a long, long, long time. Some believe that, with another round of quantitative easing, we move forward, emerge from the morass, and the need for further intervention will dissipate. But the Fed is really the only natural buyer of Treasuries anymore. It will have to continue to monetize Treasury issuance at the same time all the other major developed economies—from the Bank of Japan to the Bank of England to the European Central Bank—are doing the same. Pursue that to its natural conclusion, and you see the inevitable demise of fiat money. To look at our policies and not be concerned about the risks to our currency would be dangerously naive.

One step at a time. When is the next round of QE?

….read her answer and much more HERE

U.S. Market – While I’m certainly not bullish I would caution anyone who is thinking about shorting the market on the assumption something more than a 5% -10% fall is in the cards. The economy sucks and the geopolitical problems around the world are very serious.

However (Dislike using this hedging word found in so many market forecasters vocabulary which include if, but, maybe….), a lot of bad stuff has been thrown at this market and it bends but doesn’t break. I suspect the FED is getting close to pushing on the string yet again and there’s going to come a time when the “Don’t Worry, Be Happy” crowd on Wall Street (who always says it’s a good time to invest) shall decide it’s time to shift some of the enormous capital in bonds into stocks. Here again, I don’t anticipate a surge upwards but shorting here is the one move I think is among the worse among the choices.

Gold – It may be hard to see with the naked eye, but gold has been building a base that I believe can lead to it taking out $1,650, which in my mind should signal the resumption of the climb in the “mother” of all gold bull markets. A seasonally favorable period for gold is just a few weeks away and if the perma-bears and gold haters (that’s basically 98% of the world) can’t get gold below $1,500 by then – it’s curtains for them (and I won’t be shedding a tear for them).

U.S. Dollar – It’s getting to the point where I would like to take a flyer on shorting Uncle Sam. I shall let you know if and when I do.

Bonds – I’m looking for the 10-yr. T-Bond to get down to a 1.25% yield. At that point I feel getting seriously short is all but certain.

Oil and Natural Gas – No change here.

Mining and Exploration Shares – The juniors are especially suggesting their wash-up is near complete. We actually started to see some bids come into the market late last week In case you forgot, a bid is where someone is actually willing to buy shares-lol).

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair