Gold & Precious Metals

The outperformance of gold as an asset class is what keeps investors flocking to the metal. Yes there have been volatile periods when price has sparked lower, but overall gold has consistently outperformed both stocks and bonds over the past 12 years. As the increase in liquidity at the hands of the Fed has kept both stocks and bonds afloat, their appeal has been illusionary as the chart below (courtesy of Datastream, Ertse Group Research) shows.

The left-hand scale shows the ratio of the MSCI World equity index to gold, while the right hand scale shows the ratio of a total return index of 10 year treasury bond to gold. When the ratio’s are falling, gold is outperforming. This means that the relative strength in gold is still present as both ratios are setting lower highs and lower lows which is the very definition of a downtrend. Holding physical gold should be encouraged until a significant reversal in this trend becomes apparent. As long as the government continues to pile up debt, this trend should continue.

So how does the government try to solve the current debt situation? By issuing more debt, of course!

Ed Note: Another Item from Mark’s 19 Page VR Gold Letter which you can read more about HERE:

Egon von Greyerz of Matterhorn Asset Management gold King World News, “The printing of money will lead to collapsing currencies, and investors buying gold at any price.” He added that “the paper markets will not be trusted” because “there is a distrust in the government’s ability to govern, and there’s a distrust in the financial system. We will continue to have failures like Lehman, MF Global and PFG. They will be much bigger and people will start to realize the banking system is not safe.” “So people will rush into physical gold. I see gold reaching $3,500 to $5,000 in the next 12 to 18 months. Within 3 years, I see the gold price reaching at least $10,000.” More specifically, he believes “silver will outperform gold. It looks like the upward correction in the gold/silver ratio is finishing here, which means that silver will start going up a lot faster than gold in the next few months. I don’t think it will be long before silver goes back to $50, and in the next 12 to 18 months we will be well above $50. In a world where most assets will rot, it’s critical to hold assets that won’t decay and that is gold and silver. And they have to be held in physical form.”

Ed Note: As you might know Mark Leibovit is one of Michael Campbell’s favorite analysts and here’s a good reason why. I get all of Mark’s services, and one thing stood out glaringly in his VR Trader Platinum service. Of the 31 recommended stocks that Mark has liquidated since June 4th/2012 81% of them were closed at a profit. The 6 that were closed at a loss, the losses were very smalll, specifically -.12 cents, -8 cents, -7 cents, -.30 cents , – 2 cents and a “big” -$1.25 on a $39 stock. Moreover of the 8 stocks Mark is currently long, only one is showing a loss at today’s close of – 6 cents.

This newsletter is a publication dedicated to the education of stock traders. The newsletter is an information service only. The information provided herein is not to be construed as an offer to buy or sell securities of any kind. The newsletter picks are not to be considered a recommendation of any stock but an information resource to aid the investor in making an informed decision regarding trading in stocks. It is possible at this or some subsequent date, the editors and staff of VRTrader.com may own, buy or sell securities presented. All investors should consult a qualified professional before trading in any security. The information provided has been obtained from sources deemed reliable but is not guaranteed as to accuracy or completeness. VRTrader.com staff makes every effort to provide timely information to its subscribers but cannot guarantee specific delivery times due to factors beyond our control.

VRTrader.com

P.O. Box 1451

Sedona, AZ 86339

Phone: 928-282-1275

Fax: 623-243-4174

To change or initiate a subscription. click here

Pundits may have closed the book on the so-called nuclear renaissance, but the story is far from over. In this exclusive interview with The Energy Report, Gold Stock Trades Editor Jeb Handwerger names the “sleeping beauties” quietly proving their worth. A new generation of nuclear energy must be part of a diversified happy ending, Handwerger says, but by that time, merger and acquisition activity may have already rewarded the investors who believed in a brighter future.

OMPANIES MENTIONED: AREVA – ATHABASCA URANIUM INC. – BABCOCK & WILCOX CO. – BHP BILLITON LTD. – CAMECO CORP. – DENISON MINES CORP. – EUROPEAN URANIUM RESOURCES LTD. – EXELON CORP. – FISSION ENERGY CORP. – FLUOR CORP. – GENERAL ELECTRIC CO. – RIO TINTO PLC – THE SHAW GROUP INC. – U3O8 CORP. – UEX CORP. –UR-ENERGY INC. – URANERZ ENERGY CORP. –URANIUM ENERGY CORP. – URANIUM ONE INC.

The Energy Report: Jeb, at the turn of 2012 you were bullish on junior uranium mining stocks. It’s halfway through the year and a lot of these stocks have still underperformed. Is this the result of continued economic fallout after the Fukushima nuclear disaster, or perhaps a consequence of the availability of cheap natural gas?

Jeb Handwerger: We had a really difficult year for uranium equities in the aftermath of both Fukushima and the end of QE2. The whole resource sector went, and uranium was hit extra hard. Cameco Corp. (CCO:TSX; CCJ:NYSE) and Uranium One Inc. (UUU:TSX) declined more than 50%.

However, we are beginning to see a notable improvement in the supply-and-demand fundamentals with more institutional investor interest in uranium. Year-to-date, Cameco is up close to 21%, making a higher low than in late 2011 and holding the 200-day moving average. It seems that the bottom we predicted in uranium miners in late 2011 is still holding. Compare that to the gold miners’ ETF (GDX:NYSE), which is down 17% and to the rare earths ETF (REMX), which is down about 12%. The uranium ETF is down only 10%. That shows me that uranium miners are relatively strong in a weak, panic-driven natural resource market where investors are hoarding cash and treasuries.

TER: So what’s breathing life into the uranium sector now?

JH: In 2011, nuclear energy had a lot of competitors from alternative energy sources such as solar, wind and natural gas. Since then, the challenges for each of these sources have become more apparent and the entire energy sector has undergone an outright selloff. A lot of articles have talked about cheap natural gas taking the place of nuclear. What the pundits don’t say is that natural gas has plenty of its own issues, ranging from the environmental downsides of hydraulic fracturing to greenhouse gas emissions. Furthermore, service stations and natural gas liquefaction plants must be set up along the chain of supply from mine to consumer. Major costs are involved and there is no assurance that the price of natural gas will remain at these low levels. Plus, some parts of the world don’t have abundant natural gas. The cost of liquefying it and shipping it can be extravagant. Japan, for instance, tried importing natural gas, but eventually gave up and recently reactivated nuclear plants amid growing fears of power outages affecting industry.

The short position in nuclear miners has increased even as money is being directed toward construction of new nuclear power plants globally. The shorts use the stories of cheap natural gas to depress the uranium sector. This means uranium miners may even have additional upside because of the large short position that may soon have to run for cover in the event of a turnaround. We have seen short covering rallies before in the uranium miners. In the summer of 2010, after QE2 was announced, the sector experienced major gains. The same was true in 2007/2008 before the credit crisis. We saw a huge exponential move. These moves came out of nowhere and were very powerful, with miners moving up 10–20% a day.

We must not tar nuclear energy with the broad brush of the entire resource sector malaise. Construction of new nuclear plants proceeds steadily and the media is not emphasizing that. The U.S., for the first time in three decades, announced the approval of plans for nuclear reactors in Georgia and South Carolina. Even Japan is reactivating nuclear reactors. India and China are moving full speed ahead, and this alone will require an additional 40 million pounds (40 Mlb) of uranium annually by the end of this decade. We must remember that the underperformance right now in junior uranium miners is transient. Nuclear power is here to stay. All energy sources have their own sets of cost and environmental issues. No one source can fulfill everyone’s needs for the next 30 years. Nuclear will always be part of the long-term energy mix, and when the market turns, long-term uranium investors have the potential to experience exponential profits.

TER: Japan’s Fukushima Nuclear Accident Independent Investigation Commission published its report on the 2011 accident. It largely blamed the Tokyo Electric Power Co. operators for administration and operational failures. What did these findings mean for the future of nuclear power in Japan and around the world?

JH: Many countries are still stuck with the old, 40-year-old nuclear reactors, which is what Fukushima was. A renaissance has since occurred in nuclear engineering. The next generation of reactors has a fraction of the risks involved with the old reactors. That is what is being built in China, India and Russia. Even Saudi Arabia has 16 plants under serious consideration. Four are in the works in the United States.

TER: Given that more than 500 new reactors are in some phase of the building pipeline right now, how attractive are investments in the engineering and contracting firms that design and build reactors?

JH: Investors are looking into the companies that build the reactors. The Shaw Group Inc. (SHAW:NYSE) is building the South Carolina reactors. Babcock & Wilcox Co. (BWC:NYSE) used to build nuclear submarines, but has also moved into small modular nuclear reactors. Fluor Corp. (FLR:NYSE) and General Electric Co. (GE:NYSE) are other names with exposure to nuclear power. One can also look at utilities like Exelon Corp. (EXC:NYSE) who are major players in nuclear power generation in the United States.

TER: If this is where the increased demand for uranium will come from, what about the supply? The large producers will probably deliver, but will the explorers eventually benefit as they find the fuel for the future? From an investment point of view, what is the best way to capitalize on this coming trend? Is it through the big companies or the juniors?

JH: To answer that, I think we need to take a look at what happened in 2011. One of the biggest deals was that Hathor Exploration, which owned the Roughrider deposit up in the Athabasca Basin, was bought up for multiples by the giant Rio Tinto Plc (RIO:NYSE; RIO:ASX; RIO:LSE; RTPPF:OTCPK). Rio Tinto’s stock price did not move nearly as much as Hathor’s price. Hathor received over $11/lb uranium. If you are looking to leverage the sector, a good way to play it might be to find a suitable candidate for the major uranium miners, many of which are trading at one-tenth of that value right now. Cameco and Rio Tinto have expressed ongoing interest in further acquisitions of juniors. That is why we are specifically looking at areas that are in mining-friendly jurisdictions where the majors are going to be looking to develop economic resources. The undervaluation of quality uranium miners is creating a possible once-in-a-lifetime buying opportunity.

TER: Do you see other buying opportunities in the Athabasca Basin?

JH: Following the Hathor buyout, we expect even more consolidation in the Athabasca Basin. When a company that large sinks $650 million into an area, we don’t think that’s the end. It is just the beginning. Rio Tinto will want to build resources and consolidate its position. We also think Cameco and possibly BHP Billiton Ltd. (BHP:NYSE; BHPLF:OTCPK) is going to try to build a larger position in the basin. Target candidates include Denison Mines Corp. (DML:TSX; DNN:NYSE.A). It has the Wheeler River deposit, which is one of the best undeveloped projects in the basin. UEX Corp. (UEX:TSX) has a large resource base in the basin and is already 22% owned by Cameco. Fission Energy Corp. (FIS:TSX.V; FSSIF:OTCQX) has the J Zone, which is pretty much a continuation of the Roughrider deposit.

Athabasca Uranium Inc. (UAX:TSX.V; ATURF:OTCQX) is an early-stage company in the area, but it has some great prospects at Keefe Lake. Athabasca has an interesting team with Dr. Zoltan Hajnal from the University of Saskatchewan, who is an expert at using seismic data for uranium exploration. He did this successfully for Hathor. He is a world-class seismic expert and he has joined Athabasca’s advisory board, along with Kim Goheen, who recently retired as CFO for Cameco. The company also came out with spring drilling program results that showed some very promising early-stage success using that seismic data. The second half of 2012/2013 may be interesting.

TER: Could Athabasca Uranium or any of these be standalone projects, or are they mainly acquisitions targets?

JH: In time, there won’t be many juniors in the Athabasca Basin. The high-quality ones will be a part of Rio Tinto or Cameco. The same thing will happen in the U.S., where we follow three juniors who are currently very active. Uranium Energy Corp. (UEC:NYSE.A), Ur-Energy Inc. (URE:TSX; URG:NYSE.A) and Uranerz Energy Corp. (URZ:TSX; URZ:NYSE.A) are going to be U.S. producers who are part of the solution to the U.S. supply crisis. Just under 20% of U.S power comes from nuclear reactors, however more than 95% of the uranium is imported. The U.S. used to be one of the largest uranium exporters. Now it produces less than 4 Mlb of uranium.

As part of a plan to meet that demand, in the near term Uranerz, could be a takeover target for Cameco or Uranium One. It already has a processing agreement with Cameco and an off-take agreement with Exelon Corp. Uranerz has an incredible land package right between the two majors in the Powder River Basin, which has been producing uranium for five decades. The company employs in-situ mining, which also has many benefits over conventional mining when it comes to environmental issues and costs.

TER: How soon might a takeover happen? Is there some catalyst in the wings?

JH: You just never know when it’s going to happen, although I do know it will be sooner rather than later. I think as we get closer to 2013 there’s going to be more pressure. Over the next 6-18 months a huge amount of consolidation could come to the industry.

TER: Has the market already priced in these takeovers?

JH: No, no, no. Uranerz is trading near three-year lows. Investors have a chance to get into these companies on historic lows.

In South America, a company I like is U3O8 Corp. (UWE:TSX.V; OTCQX:UWEFF) in Colombia, Guyana and Argentina. The main project is Berlin in Colombia. The company has shown incredible resource growth during the past year. It has increased the Indicated and Inferred resource sevenfold, from 7.1 Mlb to 47.6 Mlb, and it has only documented the three southern kilometers (km) of a 10.5 km mineralized trend. The Berlin deposit is also home to phosphate and vanadium and has shown some very positive metallurgical recoveries. U3O8 is rapidly growing and derisking its resources in South American countries that are mining friendly. I understand the company will be completing a PEA in the second half of 2012. The company thinks it can potentially grow this asset in the near term to 40–50 Mlb uranium.

U308 already has a strong cash position with institutional support. What is really interesting is that the phosphate, vanadium and rare earths may pay the way with the uranium as pure profit. That is what we are looking for in the second half of the year from this company.

TER: U308 Corp is trading at $0.33 right now. How much could it go up from there?

JH: Right now, U3O8 is priced at about $0.77/lb uranium; Hathor was bought out for $11/lb and Mantra for $10/lb. That is almost a potential tenfold increase. As the project is derisked in the second half of the year, the stock should get to at least a comparable value to some of its current competitors, at over $1/lb.

TER: Are you looking at any uranium companies in Europe?

JH: Yes. We have one that we really like in Slovakia called European Uranium Resources Ltd. (EUU:TSX.V; TGP:FSE). First of all, it has a great management team. Plus, Europe is the largest user of nuclear power per capita. There is only one operating uranium mine in Slovakia at the moment and that is rapidly depleting. European Uranium Resources is really Europe’s next answer for uranium production. The deposit may be one of the lowest-cost uranium mines in the world. The prefeasibility study is very impressive from an environmental and economic perspective. The real momentous catalyst is if the company can sign an off-take agreement with the Slovakian government, with a surplus going to other EU nations.

AREVA (AREVA:EPA), the third-largest uranium producer in the world, already took a 10% position at approximately $0.35 a share and is on the European Uranium board giving technical expertise. The company is now trading at three-year lows of $0.22 per share. This may be a real undervalued situation in Europe.

Overall, Europe and the Americas are much better mining pictures than Africa and Australia right now. Rising resource nationalism in Africa and rising costs in Australia make these other stories much more attractive.

TER: So, is the overarching story mergers and acquisitions?

JH: I think so. There is going to be a dramatic change of landscape in the uranium sector. As the high-quality juniors come closer to production, they’ll be taken over by the majors. We saw the beginnings of that in 2011 and we will see it continue. One needs patience and fortitude and the ability to go against the consensus.

TER: Thank you for your time and your insights, Jeb.

JH: Thank you.

Gold Stock Trades Editor Jeb Handwerger is a stock analyst and best-selling writer who’s syndicated internationally and known throughout the financial industry for accurate, in depth and timely analysis of the general markets, particularly as they relate to the rare earths, precious metals and, nuclear sectors. He studied engineering and mathematics and received his undergraduate degree from University of Buffalo and a masters degree from Nova Southeastern the University in Fort Lauderdale. Teaching technical analysis to professionals in South Florida for some seven years, Handwerger began a daily newsletter that grew to become Gold Stock Trades: Mining for Winners in Any Market, with thousands of readers from more than 40 nations who are interested in the North American resource markets. Click here to subscribe to his free newsletter.

Want to read more exclusive Energy Report interviews like this? Sign up for our free e-newsletter, and you’ll learn when new articles have been published. To see a list of recent interviews with industry analysts and commentators, visit our Exclusive Interviews page.

The most important chart in the market might be the chasm between commodities and stocks, as per the chart below. Either the former must rally or the latter will decline. The famous and very rich Jim Rogers said in an interview yesterday:

“the investing game is simple these days. I do believe I could count on one hand the number of times I’ve been presented with an investment opportunity that guarantees success no matter what direction the economy takes.” Rogers adds, “If the world economy gets better, I earn my money on commodities. If the global economy gets worse, then they will print more money and I will make money in commodities.” More of the whole interview HERE

(The CRB Commodite Index is Orange, The SP500 Index is White)

This list of Quotations should give anyone a good idea of this extraordinary man’s Investment Philosophy. Biggs, former Morgan Stanley head strategist and research director warned of the dotcom crash. He just died at 79:

- “Good information, thoughtful analysis, quick but not impulsive reactions, and knowledge of the historic interaction between companies, sectors, countries, and asset classes under similar circumstances in the past are all important ingredients in getting the legendary ‘it’ right that we all strive so desperately for.”

- “[T]here are no relationships or equations that always work. Quantitatively based solutions and asset-allocation equations invariably fail as they are designed to capture what would have worked in the previous cycle whereas the next one remains a riddle wrapped in an enigma. The successful macro investor must be some magical mixture of an acute analyst, an investment scholar, a listener, a historian, a river boat gambler, and be a voracious reader.Reading is crucial. Charlie Munger, a great investor and a very sagacious old guy, said it best: ‘I have said that in my whole life, I have known no wise person, over a broad subject matter who didn’t read all the time — none, zero. Now I know all kinds of shrewd people who by staying within a narrow area do very well without reading. But investment is a broad area. So if you think you’re going to be good at it and not read all the time you have a different idea than I do.’”

- “[T]he investment process is only half the battle. The other weighty component is struggling with yourself, and immunizing yourself from the psychological effects of the swings of markets, career risk, the pressure of benchmarks, competition, and the loneliness of the long distance runner.”

- “I’ve come to believe a personal investment diary is a step in the right direction in coping with these pressures, in getting to know yourself and improving your investment behavior.”

- “As I reflect on this crisis period so stuffed with opportunity but also so full of pain and terror, I am struck with how hard it is to be an investor and a fiduciary.”

- “The history of the world is one of progress, and as a congenital optimist, I believe in equities. Fundamentally, in the long run, you want to be an owner, not a lender. However, you always have to bear in mind that this time truly may be different as Reinhart and Rogoff so eloquently preach. Remember the 1930s, Japan in the late 1990s, and then, of course, as Rogoff said once with a sly smile, there is that period of human history known as ‘The Dark Ages and it lasted three hundred years.’”

- “Mr. Market is a manic depressive with huge mood swings, and you should bet against him, not with him, particularly when he is raving.”

- “As investors, we also always have to be aware of our innate and very human tendency to be fighting the last war. We forget that Mr. Market is an ingenious sadist, and that he delights in torturing us in different ways.”

- “Buffett, a man, like me, who believes in America and the Tooth Fairy, presents the dilemma best. It’s as though you are in business with a partner who has a bi-polar personality. When your partner is deeply distressed, depressed, and in a dark mood and offers to sell his share of the business at a huge discount, you should buy it. When he is ebullient and optimistic and wants to buy your share from you at an exorbitant premium, you should oblige him. As usual, Buffett makes it sound easier than it is because measuring the level of intensity of the mood swings of your bipolar partner is far from an exact science.”

“Fifty some years ago, Sir Alec Cairncross doodled it best:

A trend is a trend is a trend

But the question is, will it bend?

Will it alter its course

Through some unforeseen force

And come to a premature end?

- “Nations, institutions, and individuals always have had and still have a powerful tendency to prepare themselves to fight the last war.”

- “[W]hat’s the moral of this story? Know thyself and know thy foibles. Study the history of your emotions and your actions.”

- “At the extreme moments of fear and greed, the power of the daily price momentum and the mood and passions of ‘the crowd’ are tremendously important psychological influences on you. It takes a strong, self-confident, emotionally mature person to stand firm against disdain, mockery, and repudiation when the market itself seems to be absolutely confirming that you are both mad and wrong.”

- “Also, be obsessive in making sure your facts are right and that you haven’t missed or misunderstood something. Beware of committing to mechanistic investing rules such as stop-loss limits or other formulas. Work very hard to better understand how you as an investor react to both prosperity and adversity, and particularly to the market’s manic swings, both euphoric and traumatic. Keep an investment diary and re-read it from time to time but particularly at moments when there is tremendous exuberance and also panic. We are in a very emotional business, and any wisdom we can extract from our own experience is very valuable.”

- “Understanding the effect of emotion on your actions has never been more important than it is now. In the midst of this great financial and economic crisis that grips the world, Central Banks are printing money in one form or another. This makes our investment world even more prone to bubbles and panics than it has been in the past. Either plague can kill you.”

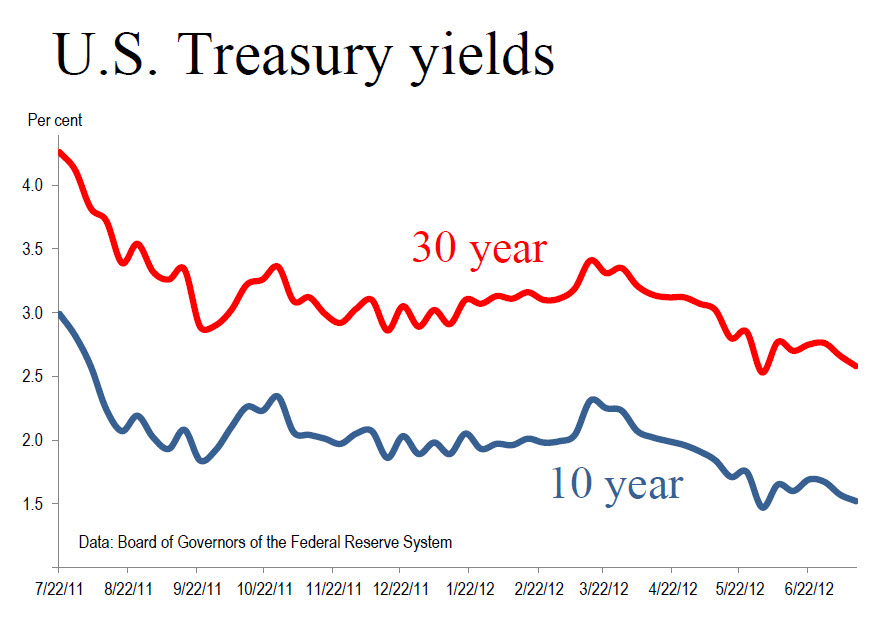

First, let me state that if you are looking for someone who has called the US treasury market correct this past decade, look no further than Lacy Hunt.

I had a nice conversation the other day with Lacy Hunt at Hoisington Investments. We agree on many aspects of the global economy and I have a few excerpts of Hoisington’s latest forecast below.

While I have been US treasury bullish (on-and-off ) for years (more on than off), and I can also claim to have never advocated shorting them (in contrast to inflationistas running rampant nearly everywhere), Lacy has correctly been a steadfast unwavering treasury bull throughout.

Will Hoisington catch the turn?

That I cannot answer. However, one look at Japan suggests the actual turn may be a lot further away than people think.

For a viewpoint remarkably different than you will find anywhere else, please consider a few snips from the Hoisington Quarterly Review and Outlook, for the Second Quarter 2012 (not yet publicly posted but may be at any time).

….read this report and more beginning at Abysmal Times Confirm the Research HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair