Gold & Precious Metals

IT’S A HARDY perennial for anyone studying the gold market, writes Adrian Ash at BullionVault. And with the British summer being more like November this year, very hardy perennials are just what is needed.

But will the Gold Price blossom on schedule?

\\

\\

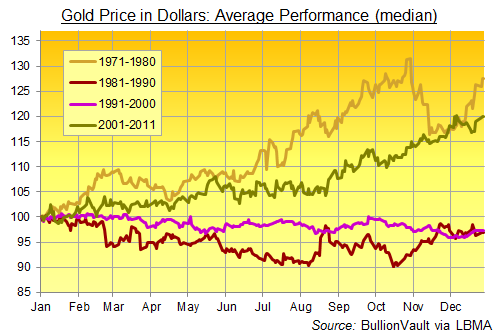

Greener than George Monbiot’s socks, we’re happy to recycle this fact yet again. The Gold Price tends to display a seasonal pattern – rising in spring, slipping or flat-lining in summer, only to rise once more in the fall and then winter.

No, the pattern was shot in 2011 as we noted last July. But such profitable “summer sales” have occurred most frequently during longer-term bull phases, as we told the Financial Times in 2009.

For Dollar investors, Buying Gold even at the highest price in July or August has only failed three time to deliver a gain by year’s-end since this bull market began in 2001 (extending a pattern we noted in 2010. Lehman’s collapse threw 2008 out of sync). Indeed, buying gold regardless of price in July or August has paid off 20 times in the last 44 years all told – and delivered an average 5.1% profit even with the losses included.

Now, this is hardly the way to time a serious move into gold. Buying regardless of price? Just because history says the summer average rewards it by year’s end?

Viewed as crisis insurance, however, gold comes at a cost – your premium being the price you pay when you take out your policy. Sensible home economics says you should look for best value. Only here, cutting your premiums needn’t void your insurance.

The Gold Price could well go cheaper from here. But if it doesn’t, and people scramble once more for the security, liquidity and diversification only a lump of rare yellow metal can bring, then the current lull could be offering insurance at summer sale prices.

To date, this summer’s lull is looking utterly typical so far.

Cut your costs further – get the safest gold at the lowest prices using world #1 online,BullionVault…

Adrian Ash runs the research desk at BullionVault, the physical gold and silver market for private investors online. Formerly head of editorial at London’s top publisher of private-investment advice, he was City correspondent for The Daily Reckoning from 2003 to 2008, and is now a regular contributor to many leading analysis sites includingForbes and a regular guest on BBC national and international radio and television news. Adrian’s views on the gold market have been sought by the Financial Times and Economist magazine in London; CNBC, Bloomberg and TheStreet.com in New York; Germany’s Der Stern andFT Deutschland; Italy’s Il Sole 24 Ore, and many other respected finance publications.

I think first of all investors must realize that the impact of a slowdown in the Chinese economy, which in my view is much larger than what the government has been reporting, the government says GDP has been growing at 7.8%, in my view it’s much lower because we have very reliable statistics.

The two countries where the exports were predominantly China-geared – Taiwan and South Korea and where the statistics are more reliable than what the Chinese announced in GDP growth, these countries have negative export growth on a year-on-year bases in the last month in June. If these countries have declining exports, it tells you something about the Chinese economy.

We have other reliable statistics like gaming revenues in Macau and so forth. The overall revenues are still up but the junkit turnover is down. These are middle men who bring the gamblers to Macau. Their growth rate has slowed down, luxury consumption has slowed down and electricity consumption is basically flat. Steel and cement production is up maximum 2-4% year-on year and so we have some reliable statistics.

Macdonalds just reported that their sales in Asia year-on-year is down more than 1%. Believe me if in a growth region, where markets are not yet saturated and where shops like MacDonalds are like prestige things for families to go and where their sales are down believe me – something is not quite right. I can see it with my own eyes. I don’t think that in Asia at the present time there is any economic growth.

When the Chinese economy was strong 2000-2008, it drove up commodity prices and that boosted growth rates in emerging economies such as Brazil, Argentina, and the oil-producing countries in the Middle East, and central Asia, Russia and of course also Africa and Australasia.

When the Chinese economy slumps, then obviously the demand for commodities goes down and these countries have less money and so they buy less and so it has a very strong multiplier effect on the global economy.

I think that the slowdown in the Chinese economy – and believe me, the Chinese economy did not grow in the second quarter by 7.8% – in my view, maximum 3%.

07/18/12 Madrid, Spain – You can’t help but feel sorry for the bankers. Yesterday, one of them was so upset and humiliated he tended his resignation — at a Senate hearing.

One after another the bankers mount the scaffold. Goldman, JP Morgan, Barclays…and now HSBC. One loses money. Another rigs LIBOR rates.

One fiddles an entire nation’s books. And another helps terrorists, drug dealers and money launderers with their banking needs.

That last charge is the one leveled against HSBC yesterday, causing the bank’s chief of compliance to quit, on the spot. Here’s the accusation:

…using a global network of branches and a US affiliate to create a gateway into the American financial system that led to more than $30bn in suspect transactions linked to drugs, terrorism and business for sanctioned companies in Iran, North Korea and Burma.

This spectacle may be entertaining, but in our view, it is fundamentally meaningless.

Here’s what really happened:

The feds created a funny money, back in the early ’70s. Unlike the gold-backed dollar, this one was almost infinitely flexible. It would allow the financial system to create trillions-worth of new cash and credit, vastly expanding the amount of debt in the system…and greatly increasing the profits of the banking sector.

The financial industry — the dispenser of the need money — set to work, creating fancy new ways to move the new money around. Each time it closed a deal, it made a profit. Naturally, it was encouraged to find all manner of clever ways to make deals.

Then, when the credit bubble blew up in ’08-’09 many of these tricks of the trade didn’t look so clever. They looked sinister. Stupid. Or crooked.

“When the tide goes out,” says Warren Buffett, “you see who’s been swimming naked.”

It is not a pretty sight.

Billions of dollars were lent to people who shouldn’t have been allowed to borrow lunch money. And now, there are losses — trillions worth.

The real question — the only question of great significance since the blow-up — is: who will take the losses? Or, to put it another way: How will the system be cleaned up? Who will decide who wins and who loses?

Mr. Market or Mr. Politician?

Let investors and speculators take the losses…or put them on savers and taxpayers?

Who will lose? The rich? Or the rest?

We’ve given you our answer many times: let Mr. Market sort it out. He’s completely impartial. He’s honest. He’s fast. And he works cheap.

In a flash, back in September-December of ’08, he probably would have wiped up the floor with the bankers. In a real crash, few of the big banks would have remained standing. Investors and lenders who had put their money in them…and who had invested in the things their phony credits supported…would have lost trillions. The rich wouldn’t be so rich anymore. And we’d now be in some phase of real recovery with many new financial institutions.

But we’re not in a position to impose our will on the world. And the politicians are. So, they’ve decided to do it another way. Instead of allowing Mr. Market to do his work they make their own choices…generally trying to direct the losses towards groups of people who don’t make campaign contributions…and don’t know what is going on. That is, towards the masses…and the unborn…

The idea has been to kick the can as far down the road as possible…borrowing and printing trillions more dollars to prop up the financial system…while also parading a few bankers through the streets with nooses around their necks. The press insults them. The mob spits upon them. The public spectacle continues…

…and nothing really changes.

Regards,

Bill Bonner,

for The Daily Reckoning

Bill Bonner

Since founding Agora Inc. in 1979, Bill Bonner has found success and garnered camaraderie in numerous communities and industries. A man of many talents, his entrepreneurial savvy, unique writings, philanthropic undertakings, and preservationist activities have all been recognized and awarded by some of America’s most respected authorities. Along with Addison Wiggin, his friend and colleague, Bill has written two New York Times best-selling books,Financial Reckoning Day and Empire of Debt. Both works have been critically acclaimed internationally. With political journalist Lila Rajiva, he wrote his third New York Times best-selling book, Mobs, Messiahs and Markets, which offers concrete advice on how to avoid the public spectacle of modern finance. Since 1999, Bill has been a daily contributor and the driving force behind The Daily Reckoning. Dice Have No Memory: Big Bets & Bad Economics from Paris to the Pampas, the newest book from Bill Bonner, is the definitive compendium of Bill’s daily reckonings from more than a decade: 1999-2010.

Special Video Presentation: Urgent Message About Your Net Worth The single, solution-packed book that could… literally… mean the difference between growing wealthy or suffering an ugly, vicious decline in your net worth. Discover how to claim a FREE copy of this book, right here.

Read more: A Crisis Veiled in Public Spectacle http://dailyreckoning.com/a-crisis-veiled-in-public-spectacle/#ixzz214kPGzyg

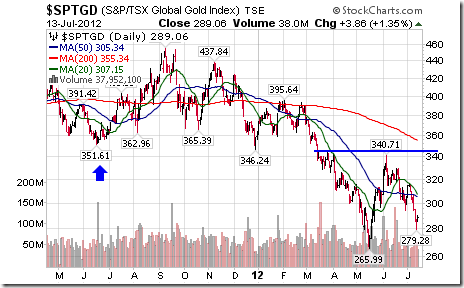

Gold equities and related exchange traded funds listed on the TMX finally came alive on Friday after gold bullion prices rose sharply on news that China’s second quarter GDP recorded a healthy 7.6 per cent annual growth rate. Gold advanced to US$1,587.10 per ounce and briefly broke above its 20 and 50 day moving averages.

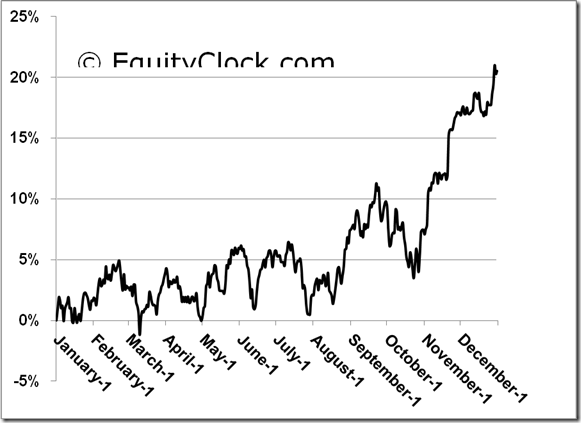

Seasonal influences for gold and gold stocks are starting slightly earlier than usual this year as they did last year. Thackray’s 2012 Investor’s Guide notes that the period of seasonal strength for the gold equity sector is from July 27th to September 25th. The equity sector trade has been profitable in 17 of the past 25 periods including 11 of the past 14 periods. Average gain per period for the past 25 periods was 7.2 per cent.

On the charts, the S&P/TSX Global Gold Index at 289.06 has a negative, but improving technical profile. The Index bottomed in mid-May at 265.59, rose strongly to 340.71 in early June followed by a recent test of its low. The Index remains below its 20, 50 and 200 day moving averages. Short term momentum indicators are deeply oversold and showing early signs of bottoming. Strength relative to the TSX Composite Index has been positive since mid-May. A move above 340.71 completes a modified reverse head and shoulders pattern. Preferred strategy is to accumulate gold equities and related ETFs at current or lower prices between now and July 27th for a seasonal trade lasting until the end of September.

Canadian investors can choose between five ETFs when interested in entering the sector. Each ETF has unique characteristics;

The most actively traded gold equity ETF in Canada is iShares on the S&P/TSX Global Gold Index Fund (XGD $18.01) The fund tracks the performance of 59 precious metal stocks that make up the S&P/TSX Global Gold Index. The Index is capitalization- weighted. Largest holding are Barrick Gold, Goldcorp, Newmont Mining, Kinross Gold, Anglogold Ashanti and Agnico Eagle. Management expense ratio is 0.55 percent.

Horizons offers the BetaPro S&P/TSX Global Gold Bull + ETF (HGU $7.08) and the BetaPro S&P Global Gold Bear + ETF (HGD $12.59). Both are leveraged ETFs that track the S&P/TSX Global Gold Index. The Bull ETF is designed to generate twice the daily upside performance of the Index. The Bear ETF is designed to generate twice the daily downside performance of the Index. Management expense ratio is 1.15 percent.

Horizons also offers the AlphaPro Enhanced Income Gold Producers ETF (HEP $5.88). The ETF tracks the performance of a portfolio holding 15 equally weighted senior global gold and silver producers. At or near the money listed call options are written against security positions. Option premiums and dividends earned by the fund are distributed to unit holders on a monthly basis. The strategy is enhanced by high implied volatilities on the call options of senior gold producer stocks. Management Expense Ratio is 0.65 percent.

Bank of Montreal offers the BMO Junior Gold Index ETF (ZJG$13.28). The ETF tracks a diversified portfolio of 35 junior gold stocks that make up the Dow Jones North American Select Junior Gold Index. The Index is capitalization weighted. Largest holdings are Allied Nevada Gold, Coeur D’Alene Mines, Alamos Gold, AuRico Gold and Nova Gold Resources. Management Expense Ratio is 0.55 percent).

Below: The Nine year seasonality chart on the S&P/TSX Global Gold Index

Don Vialoux is the author of free daily reports on equity markets, sectors, commodities and Exchange Traded Funds. He is also a research analyst at Horizons Investment Management, offering research on Horizons Seasonal Rotation ETF (HAC-T). All of the views expressed herein are his personal views although they may be reflected in positions or transactions in the various client portfolios managed by Horizons Investment. Horizons Investment is the investment manager for the Horizons family of ETFs. Daily reports are available at http://www.timingthemarket.ca/ & http://www.equityclock.com/

Some people only ever say BUY gold and God help you if you say SELL! They justify their one-sidedness saying if gold ever does down, it is a conspiracy and it must always go up every day. There is no such market that acts in that manner. There are legitimate reasons to buy physical gold – they just ain’t what the Goldbugs say they are!

The Truth About Gold & Why You Should Buy It

Some people only ever say BUY gold and God help you if you say SELL! Even the pro-Gold radio shows will bar you if you do not agree with them. Guess Mainstream applies to them in reverse! The pro-Gold radio shows are just as biased and prejudiced as they say everyone else is against gold, but in reverse. They just don’t get it! This is NOT a religion. This is trying to survive an economic meltdown. You have to be careful not to lose during the short-term battle if you ever hope to make it through the war! Sometimes it is best to SELL and then buy back more when the correction is over. Yet they justify their one-sidedness saying if gold ever does down, it is a conspiracy for it is the exception to everything and must always go up each and every day. There is no such market that acts in the manner they wish to portray as normal. There are legitimate reasons to buy physical gold – they just ain’t what the Goldbugs say they are!

Ed Note: This is a very long and detailed article with lots of charts & graphs which you can read in full HERE. In the meantime here is Martin’s conclusion:

So Don’t Worry – Be Happy. Gold is not going up because of all the conspiracy claims nor because the real gold will conquer the paper gold. This is all about reality. Gold standards do not work because you cannot fix the price of money regardless what you call it. To try to do so is communism where the real attempt was to eliminate cycles. Gold is a viable part of the portfolio. It will rise to the occasion when the timing is right. The very people accused of keeping it down are the very people who will turn around and send it up as well. This is just about time. Nothing more! When the time is right and people realize that the Governments have no Clothes, look out – there will be a stampede at that time. For now, that still appears headed into 2017.

via Martin Armstrong @ Armstrong Economics

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair