Timing & trends

I’d love to tell you that all is well in the world. That Europe has solved its sovereign-debt and currency problems. That the U.S. economy is looking better than most believe. And that Asia is about to soar again.

But the fact of the matter is that none of that is true.

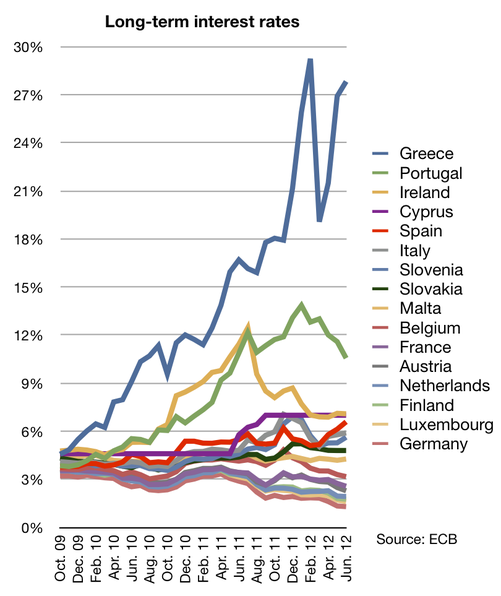

Europe’s in deep doo-doo. Spanish and Italian debt yields are soaring again. Moody’s has now downgraded Italy. Finland is threatening to pull out of the euro. The euro is tanking; it’s at a fresh multi-year low and threatening to plunge even more.

Here in the United States, corporate earnings are starting to disappoint. The U.S. budget deficit hit $904 billion in June and is on track to hit $1.17 trillion by the end of the year.

Our national debt is approaching $16 TRILLION, more than $51,000 for every man, woman and child.

Plus, our country is quickly heading toward a fiscal cliff of gigantic proportions ― uncertainty in just about everything, from tax policy … to fiscal policy … to monetary policy and more.

Also thrown into the mix: Underlying tones of class warfare, rising social unrest, stubbornly high unemployment, and more.

In Asia, China’s economy has slowed more than I expected. Though the region can bounce back quite quickly, there’s no doubt the added worries about Asia are also weighing on the global economy.

Bottom line: The short- and intermediate-term fundamental forces driving the markets are looking ugly.

That’s also precisely why the technical picture for most markets is also looking bad.

Consider this chart of gold: Many see some sort of bullish formation forming, all because gold has managed to hold the $1,522 to $1,545 level on at least five occasions.

But anyone who has truly studied the market knows that the more times a market tests a particular level, the greater the odds are that it will eventually break that level and plummet right through.

All my system signals remain bearish gold in the short to intermediate term. Once $1,545 is taken out, look for support levels at $1,495.50 … $1,446.80 … $1,400.80, followed by $1,373.10 and $1,346.80.

ONLY a close above $1,723 in gold would reverse the downtrend. Short of that, I strongly believe gold is headed lower.

Also consider this chart of Silver. Similiar to Gold, Silver has repeatedly tested — and worn down — the support level at the $26 area. The next time through it, and silver should plummet.

Look for support at $23.61 followed by $20.27 and $16.89.

Only a weekly close above $31.49 would reverse silver’s short- to intermediate-term downtrend.

Hard to believe silver could fall to $20 or lower. I know. But that’s what my systems are telling me. And the rout could come soon. So stay alert.

Also consider this chart of crude oil. It’s one of the ugliest charts I’ve seen in a while.

While oil is trying hard to hold the $80 level, it will soon fail to do so. Instead, a shocking decline lies ahead for oil, one that will see it plunge to below $60 a barrel.

Keep your eyes on the $77.33 level. Once that gives way, oil will spin a lot of heads as it tumbles hard. Only a weekly closing above $92.87 would turn the immediate trend around for oil.

As for U.S. stocks, don’t expect much upside there either. While the broader U.S. stock markets are in a new long-term bull market, they remain vulnerable to the downside in the short term.

There’s simply too much global uncertainty right now, and I see the Dow falling to at least 11,500 and possibly 10,500 — before any sustainable rally develops.

My view:

- Continue to keep most of your liquid funds in cash, ready to be deployed on a moment’s notice, but as safe as can be right now. The best way: A short-term Treasury-only fund in the U.S., or equivalent.

- Despite gold’s weakness, hold on to all long-term gold holdings. You do not want to let go of those. Long term, gold is heading to well over $5,000 an ounce. Short term, gold is heading lower. Consider inverse gold ETFs, such as the ProShares UltraShort Gold (GLL), to hedge your long-term holdings.

- Consider prudent speculative positions to grow your wealth. Like those I have recommended in myReal Wealth Report, which are doing great right now as silver falls, as the euro struggles, and more.

Most of all, don’t let the pundits on Wall Street kid you. The Fed will not prop up the markets for the elections … Europe will not be able to solve its sovereign-debt crisis … corporate earnings have seen their best for the current cycle … and there are more dangers to your wealth right now than there have been in the recent past, since at least 2008.

So stay cautious, but ready to pounce on new opportunities as they unfold.

Best wishes,

Larry

P.S. My Real Wealth Report subscribers have side-stepped the crash in gold and silver mining shares … have hedged up most of their gold holdings from much-higher levels … and they are also enjoying pretty nifty gains in their speculative positions, including inverse ETFs on silver and the euro.

Wouldn’t you like to join them? All you have to do is click here to start your risk-free Real Wealth Report trial today!

About Uncommon Wisdom

For more information and archived issues, visit http://www.uncommonwisdomdaily.com/

Uncommon Wisdom (UWD) is a free daily investment newsletter published by Weiss Research, Inc. This publication does not provide individual, customized investment or trading advice. All information is based upon data whose accuracy is deemed reliable, but not guaranteed. Performance returns cited are derived from our best estimates, but hypothetical as we do not track actual prices of customer purchases and sales. We cannot guarantee the accuracy of third party advertisements or sponsors, and these ads do not necessarily express the viewpoints of Uncommon Wisdom or its editors. For more information, see our Terms and Conditions. View our Privacy Policy. Would you like to unsubscribe from our mailing list? To make sure you don’t miss our urgent updates, just follow these simple steps to add Weiss Research to your address book.

Considering that interest rates have never been this low in our lifetime it’s hard to imagine that the biggest credit market risk we face is that rates keep falling…rather than going back up.

German and Swiss two year government bonds are currently around 40 basis points negative to par…that is, you give your money to the German or Swiss government and two years later they give it back to you minus a safekeeping charge. Even the French government was able to raise 6 month money this week at negative yields. We can understand that German and Swiss rates are low (perhaps we can even understand that they are negative) because of the flood of cash fleeing peripheral Euro countries…but France borrowing at negative rates…that’s hard to understand!

Once markets cross the Rubicon to negative interest rates then there is no way of knowing how low rates might go. (Our friend Dennis Gartman gives us good advice on this matter: “Never buy a market that is going down…you have do idea how far down…down is!”)

The US Treasury sold 10 year bonds this week at the lowest auction yield ever – 1.459% – in the face of very strong demand for the issue.

The Eurodollar futures market is current pricing short term rates over the next year at around 40 basis points…about the same record low levels reached last August after the DJI fell 2000 points in 3 weeks and the VIX (the fear index) jumped to its highest level since early 2009.

My question is: if the Germans and the Swiss and even the French can borrow money at negative interest rates when will the American and Canadian governments be able to do the same? What market conditions would likely have to exist for our interest rates to go negative? A serious recession? A financial meltdown in

For the past few years I have continually made the point that we are (in Gary Shilling’s words) in an Age of Deflation…that the simulative efforts of governments and central banks to maintain “growth” were only a rearguard action in the face of massive private sector deleveraging…that deleveraging is a consequence of “Way more money has been borrowed than will ever be paid back!”

Low and lower interest rates (on perceived top quality credits) are a natural consequence of this deleveraging. The fear that causes money to flee peripheral European countries and banks for the perceived safety of German, Swiss or French government paper is a natural consequence of the rampant deleveraging in peripheral

The city of

This week the Spanish government, in an attempt to meet Austerity demands from their lenders, proposed plans to increase the VAT from 18% to 21%, cut salaries for gov’t employees, and cut UE benefits (in a country with official UE around 25%.) Riots followed.

President Obama, in an election year cri de coeur, has declared that taxing the rich is the way to go…and the way to distinguish himself as the right political choice over filthy rich Romney (Obama’s personal net worth is publicly estimated to be ~$10.5 million.)

This week the Euro fell to a 2 year low against the USD and to a 12 year low against the CAD.

This week the Bank of England laid out a program of “rewards” for banks that increase lending to businesses and individuals.

If low interest rates have been a problem for struggling pension funds and life insurance companies imagine what will happen to them if interest rates go negative.

Betting against falling interest rates…and expecting that they have nowhere to go but up…because we think they are SO LOW relative to our lifetime experience…may be a bad bet!

For my own accounts: My long term savings are very liquid and very conservative…largely in cash. I move in and out of the markets with my short term trading accounts (rarely using much leverage) as I try to catch price swings of a few days to a few months. My net worth is ~95% cash with ~25% of that in USD, ~75% in CAD.

Victor Adair

Senior Vice President and Derivatives Portfolio Manager

Office Address

Vancouver, British Columbia

V7Y 1H4 Canada

Quote

“All war is based on deception. “ -Sun Tzu

Of Interest – Spanish not exactly loving austerity (Bloomberg)

Commentary

Expectations for China’s GDP growth were 7.6% and “magically” the number came in at 7.6% (lowest in three years). Do you sense the sarcasm in my writing voice?

Analysts noted that electrical usage in the country suggested real economic activity was likely lower than reported. We’re going with the electrical grid numbers instead of those massaged reported. Why? China’s satellite country, aka Australia, is showing signs China’s demand is fading; it reported a decline in June payrolls. We believe the Reserve Bank of Australia will act to lower interest rates. Normally, you might expect that would be good news for Australian stocks, but in a world still driven by hot money liquidity flows it may not be.

Action

As you can see, the three price series—RBA Cash Rate, Australian $- USD, and MSCI Australian Stock Index (EWA)—seem quite positively correlated from a monthly perspective.

We believe the RBA Cash Rate expectations is the driver of this pack. A cut in interest rates in Australia represents growth concerns, represents falling yield differential for the Australian dollar, and triggers money, a lot of hot money intially there for yield, to flow out. At least that is the attempt to link the movement of the price series togther, and we think it makes sense. Remain short EWA.

Be sure to listen to Michael Campbell interview Jack Crooks tomorrow on CKNW 980 @ 9:am PST Saturday June 14th/2012

This month’s calendar has been chock a block with one important meeting or vote or conference after another. Any one of these could have had a large impact on the endless Euro crisis. The most impressive result (sarcasm implied) from all these meetings and votes is the overall lack of impact. For all the wild swings in both debt and equity markets things have changed little in the past month and the European muddle through continues.

Greece has a new, pro-bailout, government with three coalition partners. The election turned out better than feared but the real work lies ahead. All of the parties in the election promised a much looser austerity program either through negotiation or simply by reneging on the deal. The winning coalition promised Greeks they could have their baklava and eat it too, to a lesser extent. Based on probably accurate leaks out of Athens the plan is to approach EU institutions looking for a two year extension to hit deficit targets. This would require about $20 billion in additional loans above the two Greek bailout packages in place already.

This news is not going over well in Berlin. Greeks took comments about trying to work with a pro bailout government to mean there would be some sort of completely new deal. Not likely. The Greek government has zero fiscal credibility, particularly since the winning party that dominates the cabinet is exactly the same one that had the biggest hand in creating the problem. Most Europeans, but particularly Germans, simply do not and will not believe Greece will stick to any deal.

German Chancellor Merkel is being vilified for being such a hardliner but she lives in a democracy and poll after poll shows German’s hate the idea of lending money that cannot be policed later. This is the core issue for the EU and has been since its inception. Most member governments are unwilling to give up any real fiscal sovereignty. This means that lender states have little or no control over what happens to their funds after the cheque is cashed. It was no secret this was a big problem when the EU was being created. Intricate rules and prohibitions were laid down that were meant to keep member countries on roughly the same plane when it came to deficit levels, etc.

Of course, these rules were broken by virtually every member state, including Germany itself. So many EU countries breached the maximum deficit level as a percentage of GDP rules that it’s hardly surprising these rules are now viewed as mere suggestions.

This mess would always have taken years to work through. The timeline is now longer, if anything. That is partially due to the multi-year contraction in most of the debtor economies. Even with harsh cuts it will take more time to balance budgets and there is no likelihood of surpluses that can reduce debt loads until debtor economies actually start growing again.

This news hasn’t gone over well with creditor nations. An understandable reaction since a long timeline inevitably means more loans to some of the debtor nations. Nonetheless, it’s becoming obvious that the creditors are not going to get a one way deal here. There is going to have to be some compromise before this drama ends. Unless creditor countries are willing to sweeten things, if only to improve sentiment in the peripheral countries, it will be hard for debtor economies to pull out of their tailspins.

Current hopes rest with the EU meeting that is currently taking place. This is the eighteenth meeting since the crisis erupted which should tell us what the chances of success are. The most important topic is some sort of EU level bank oversight and deposit insurance. This will take years to create but even putting together credible time line and laying out what sort of bank oversight is being worked towards will help.

As we have noted many times, the current danger point is Spain and it’s the victim of a real estate bubble, not bad governance per se. As this issue was being finished there was news of a compromise that will help the Spanish sovereign bond market. The EU has agreed that the latest loan package will not have preference. This is significant since it could and should give buyers of Spanish sovereigns more comfort since it will not place 100 billion euros of debt ahead of them if something goes wrong.

Italy’s government is more guilty of pure mismanagement but it matters not; the EU does not want to see the Italian bond market go south. It’s just too big to fix. Many of the leading banks are also too big for their home countries to deal with. Ireland and Iceland are the poster children for too big to fail banks (though, in retrospect, both countries probably should have let them fail anyway) but many other countries have banks that represent systemic risk, including Germany.

Bank oversight is not a bailout so much as something obvious and sensible that should have been put in place the day the Euro was created. Promising not to demand preference for the current loan package to Spain is a huge relief to the market but the most important part of the compromise is the promise to set up an EU banking authority.

In typical EU fashion the details on the banking authority were scant and the timelines will undoubtedly be longer than the market wants but it’s a big step in the right direction. One of the chief problems in Europe is the direct ties between bank recapitalization and sovereign debt levels. Up to now, whenever a country that could not recapitalize its banks went to the EU the money would have to be borrowed and distributed by the government. If this new bank authority is able to lend directly to financial institutions then every bank recapitalization will not automatically result in an equal increase it the home country’s sovereign debt level.

That is a huge change if the EU actually pulls this off. That said, this is Europe we’re talking about. There will be lots of meetings and position papers and bureaucratic wrangling involved before the details are agreed to. There is still room for things to go pear shaped if Germany and other creditor nations impose conditions so harsh that they cancel out the positive effects. That possibility could cap gains but this does feel like a real shift in the political landscape. The arrival of a large anti-austerity block headed by French President Hollande has changed the equation.

The Euro crisis is not over. Germany and its austerity block allies have yielded on a couple of important points but don’t expect a complete about face. There shouldn’t be one because Merrkel and her allies are right. The only long term solution is lower debt levels and structural changes to economies that make them more flexible and responsive to changing conditions. The former is going to take years to accomplish even under best case scenarios. The latter may too since confronting entrenched interest groups takes more political courage than most Euro area leaders seem to possess.

Expect more turbulence in the Euro market. Battle lines have been drawn between the pro and anti-austerity camps and there are many more fights ahead. The debt crisis and uncertainty about how to navigate it has done enormous economic damage to the Eurozone that will take a long time to repair. Even mighty Germany has put out recent economic readings that imply it is starting to stall. That may well be the real reason Merkel finally showed some flexibility. It would have been better by far if this had happened two or three years ago.

Hopefully this does not embolden the anti-austerity group to the point where they forget cost cutting and reforms are still a necessity. French President’s Hollande’s renewed promise to lower the retirement age in France was not a positive sign. Aside from being just plain stupid under current economic conditions it’s also exactly the kind of grandstanding that could stiffen the resolve of creditor governments and mess up further progress.

Economic readings outside of the Euro area have mainly come in better than expected. Not great, but good enough to add some pressure to the Euro on top of its internal issues. Announcement of the compromise deal is generating one the largest one day move in the Euro this year. Gold has been trading with a very high positive correlation to the Euro so it’s getting plenty of lift too and the entire commodity complex is following suit. This is all to the good but traders can be forgiven for remaining somewhat cautious. When it comes to Europe this is a movie we have all seen may times before. The devil is in the details when it comes to multi-lateral agreements. EU rescue funds still don’t and won’t have enough money to literally rescue Italy for instance. It’s unlikely it every will so the key will be regaining and retaining investor confidence. The EU must get bond traders on side and keep them there. If they can do that the world economy should be able to muddle through.

Even with that the summer doldrums won’t provide a lot of trading opportunities unless and until another company makes what looks like a major find. Volumes will climb only slowly but continued movement in the right direction politically in Europe may finally give us a set up for a meaningful fall rally in the resource sector. Let’s all cross our virtual fingers and hope the Eurocrats don’t find yet another creative way to wrest defeat from the jaws of victory.

Ω

©2010 Stockwork Consulting Ltd. All Rights Reserved.

Published by Stockwork Consulting Ltd.

Box 85909, Phoenix AZ , 85071 Toll Free 1-877-528-3958

hra@publishers-mgmt.com” data-mce-href=”mailto:hra@publishers-mgmt.com“>hra@publishers-mgmt.com http://www.hraadvisory.com

The HRA – Journal, HRA-Dispatch and HRA- Special Delivery are independent publications produced and distributed by Stockwork Consulting Ltd, which is committed to providing timely and factual analysis of junior mining, resource, and other venture capital companies. Companies are chosen on the basis of a speculative potential for significant upside gains resulting from asset-based expansion. These are generally high-risk securities, and opinions contained herein are time and market sensitive. No statement or expression of opinion, or any other matter herein, directly or indirectly, is an offer, solicitation or recommendation to buy or sell any securities mentioned. While we believe all sources of information to be factual and reliable we in no way represent or guarantee the accuracy thereof, nor of the statements made herein. We do not receive or request compensation in any form in order to feature companies in these publications. We may, or may not, own securities and/or options to acquire securities of the companies mentioned herein. This document is protected by the copyright laws of Canada and the U.S. and may not be reproduced in any form for other than for personal use without the prior written consent of the publisher. This document may be quoted, in context, provided proper credit is given.

Malaysia’s state-owned oil and gas company just made a multi-billion-dollar bet that Canada will choose to export its shale gas riches. Even though the odds of securing permission to export liquefied natural gas (LNG) from the Canadian west coast are still pretty poor, the costs of such an endeavor immense, and the timeline in question very long, Petronas is putting $5.5 billion on the table – far more than it has ever spent on an acquisition before – to secure a large foothold in the British Columbia shale gas scene.

It’s yet another sign that things are getting serious in the global race for resources.

The race for resources drives much of our thinking within the Casey Research energy group. It’s more than a common theme – we believe that it is one of the strongest forces at work in our world today, and that it plays a role in determining the tone of many international relationships and domestic policies. Countries that have resources, from Russia to Australia, are altering fiscal structures and ownership rules so as to glean as much benefit as possible from their riches, while still reserving sufficient supplies to fuel their futures. Countries that lack natural-resource wealth, such as Japan and South Korea, are racing to lock up projects and partnerships abroad that can supply their future resource needs.

And a race it is, because they are not alone. There are few countries in this world with natural supplies of all the energy commodities they need – Australia, Russia, and Canada are among the few that do – and everyone else has to constantly wheel and deal to secure imports. Now the easy deposits of many energy resources are disappearing, but global demand continues to rise. The result: stiffer competition.

Petronas’ deal is a perfect example. Petronas is buying Calgary-based Progress Energy Resources (T.PRQ) for C$4.8 billion in cash. Including convertible debt the deal is valued at about C$5.5 billion. In announcing the deal, Petronas also said it has chosen Prince Rupert, BC, as the home of its planned LNG export terminal.

So the company is spending billions of dollars to acquire 1.9 trillion cubic feet of proven and probable gas reserves… but there is no guarantee that they will be able to export any of that gas in the foreseeable future.

Pipelines have become a highly contentious issue in North America – just as US citizens are embroiled in a debate over the Keystone XL pipeline which would transport oil sands crude south, Canadians are arguing the merits and liabilities of the Northern Gateway pipeline, which would move oil sands crude to the west coast for transport to Asia. One of the big arguments against Northern Gateway is the danger of sending tanker traffic through the coastal waters of northern BC, where an oil spill would be near impossible to clean and would irreparably damage a pristine ecosystem.

The same arguments will surface with natural gas. The LNG terminal that Petronas envisions in Prince Rupert would send loaded tankers through those same sensitive waters, an idea that is far from accepted in the region at this point. The pipelines ferrying natural gas to that terminal would cross mountainous terrain burdened with heavy winter snowpack and dramatic summer melts that regularly cause hillsides to slide and rivers to swell their banks and take out bridges – all points that opponents will use to argue that the potential risks outweigh the benefits.

In short: Petronas and its peers face a steep, uphill battle in their quest to permit pipelines and LNG terminals on the west coast. But as we wrote last week, the potential for big profits will also play a role.

Remember, natural gas in its gaseous state is a landlocked commodity. Its low energy-to-volume ratio renders it uneconomic to ship, which means pipelines are the only option. To move natural gas over oceans it has to be condensed into LNG, increasing the energy-to-volume ratio dramatically and making it economic to load onto tankers and send around the world.

Many major global economies rely on LNG to meet their natural gas needs; and demand is on the rise. In 2011, global LNG trade grew by 9.4% compared to 2010, with Asia generating most of the demand increase. Japan is the world’s top LNG importer, having bought 79.1 million tonnes in 2011; South Korea is in second place with imports near 36 million tonnes. India, China, and Taiwan are all also major LNG buyers, helping to lift Asia into top spot as a regional LNG import market: Asian LNG buyers accounted for 63.6% of the global market in 2011.

That level of demand from a part of the world fairly short on supply means high prices. LNG in Asia is currently worth between $17 and $18 per million British Thermal Units (MMBtu) – six to seven times the price of natural gas in North America.

That price difference is precisely why Petronas is maneuvering to buy reserves in North America. The gamble is simply worth its while – if Petronas is able to build pipelines and an LNG terminal on the west coast, the company will be able to take a commodity worth a few dollars here and sell it for many times more in Asia.

The lure of that payout has drawn many players to this expensive, drawn out, and highly uncertain game. With this deal, Petronas joins a growing list of international energy companies including PetroChina, Mitsubishi, and CNOOC that are spending billions on remote natural gas plays in Alberta and BC, all of which share the same dream of selling the gas in Asian markets.

While these Asian energy giants take on the risk, Canadian gas explorers pretty much get to just enjoy the benefits. Depressed North American gas prices have brought most gas explorers to a standstill – investors and banks alike are not interested in funding projects where the cost of production is almost the same as the value of the product. But being bought out or finding a partner with deep pockets is a perfect solution. As Progress’ CEO said, “Our asset base requires extensive capital to develop its large potential and ultimately access international LNG markets. Petronas offers the size and scale that will enable our company to continue to grow and not be limited by the same cash flow challenges faced by many producers in the North American natural gas market today.”

Since Canada’s gas explorers are stuck in neutral, you might think that Asian energy firms would be making minimal offers, trying to acquire these resources on the cheap. Instead, Petronas offered C$22.45 a share for Progress, 77% more than Progress’ closing price the previous day. Are they trying to earn goodwill with Canadians? Perhaps, but there’s a more likely explanation for their generosity: pressure from behind. If they made a stink bid and Progress voiced displeasure, the dispute could draw attention from Petronas’ peers, which are also on the lookout for good natural gas deals. One of these peers might then swoop in and make a better offer, leaving Petronas empty-handed.

This is the impact of the race for resources. These Asian energy giants are racing with each other to secure resources for the future. The constant pressure to stay ahead in the race means companies will offer whatever it takes to secure a deal quickly, before anyone else trips up their efforts.

Shale gas riches have positioned North Americans as beneficiaries in the global race to secure natural gas supplies. However, complacency is a dangerous thing. Just because North America has gas doesn’t mean it has all of the energy resources it needs for the future. President Obama’s recent executive order on Russian uranium was a reminder that the US relies on imports to feed its nuclear reactors, and with the Megatons deal coming to an end, the United States is being thrust into the global race for uranium just as that race is heating up.

Scarcity is a powerful force and it leaves those in control of limited resources wielding great power. We think a scarcity of uranium will increase Russia’s power; control over some of the last big, easy oil deposits has earned Saudi Arabia great global influence. Petronas’ deal with Progress is a sign that shale gas could generate similar prowess for North America, and is a strong reminder that the global race for resources will provide some with money and power while leaving others in the dust.

North American energy resources don’t guarantee the US a comfortable position in the gas and oil sectors. Pipeline politics and eager Asian bidders may leave the United States literally out in the cold.

Disclaimer: Nothing in this commentary should be construed as investment advice or guidance or any recommendation to buy or sell any financial instrument. It is not intended as investment advice or guidance, nor is it offered as such. It is solely the opinion of the writer, who is NOT an investment counselor/professional. All content of this commentary is solely an expression of his personal interests and is posted as free-of-charge commentary and is subject to error and change without notice. Please do your own due diligence before investing in ANYTHING. The presence of a link to a website does not indicate approval or endorsement of that website or any services, products or opinions that may be offered by them.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair