You might hear people say, “It’s not a bull market in gold… It’s simply a bear market in the Dollar.” You see, if the US Dollar is crashing against other currencies, it’s likely also going down in terms of gold. So it looks like gold is in a bull market. But what if gold is falling in terms of the Euro or Yen while it’s rising against the Dollar? That’s not a gold bull market.

If the average price of gold is up in all four currencies versus the previous month…the Buy Gold. Repeat the next month. That’s it.

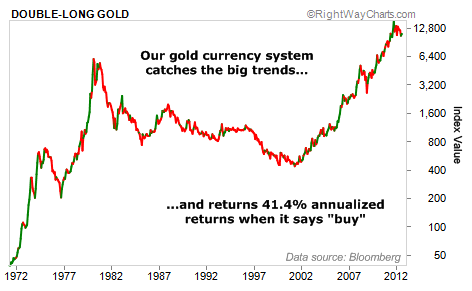

I know it sounds too simple, but it works. We want to own gold when this system says “buy”. We’ve tested the idea on 40-plus years of data. The results are astonishing.

Based on history, buying a double-long gold fund when this system says “buy” is good for 41.4% annualized returns.

Yes, that’s right. This system returns over 41% a year when it flashes “buy”.

Importantly, these signals are somewhat rare. Our computers say “buy” less than one-third of the time. Meaning, on average, we’ll only get about four buy signals every year.

And right now, the True Wealth Systems computers tell us now is the time to Buy Gold and ride it higher.

The thing is, we still don’t have the uptrend, based on our “Gold Uptrend” system. I’m not concerned, though – that system is a bit slow to signal. Our “Gold in Currencies” signal can be a great “early sign” of a new uptrend in gold.

In short, based on our historical testing, we could be at the brink of a major breakout in gold, but without a confirmed uptrend as yet. Now, I pored over the data and found an incredible result…

In 40-plus years of testing, we’ve seen six MAJOR gold bull trades. (That doesn’t sound like many. But remember, gold went down, consistently, between 1980 and 2000.) Our “Gold in Currencies” system said “buy” before our “Gold Uptrend” system did at the beginning of every trade except one. (In that case, they signaled at the same time.)

In these five cases, our “Gold in Currencies” system signaled “buy” one to three months before the “official” uptrend kicked off. However, being a few months early can “juice” our long-term gains.

The average return on our five gold uptrend trades was 110%. That’s an incredible return. However, by following our “Gold in Currencies” system into the trade a few months early, we’re able to increase our average return to 133%.

Importantly, every one of these trades was MORE successful because of following the currency system in early.

Today, we could be on the verge of another major move in gold. Of course, we can’t know if this is the case. But simply based on history, we want to own the yellow metal when our “Gold in Currencies” system says “Buy Gold“. Historically, it’s good for 41.4% annualized returns, regardless of predicting a new uptrend.

You get the idea – right now is a great time to Buy Gold. It is still a bit hated, and we could be on the brink of a major uptrend.

Get the safest gold at the lowest prices using world #1 for physical ownership – off-risk for anyone else’s financial performance – BullionVault…