Personal Finance

Gold’s price has risen because of the abuse and mismanagement of our monetary and currency systems – throughout history, gold has always shone the brightest when trust breaks down, confidence falls and fear climbs.

Central banks money printing is out of control – gold’s price will continue, has to continue, too rise in value against all depreciating paper currencies.

Gold is up about seven times from its lows more than a decade ago. What’s the upside from here?

If gold hits $5000.00 an ounce it’s a triple from here. What if gold reaches $10,000 an ounce? Well, you’ve got a nice return and it’s this authors belief that gold and silver bullion and coins should be part of every investors portfolio.

But

History shows us, time and again, the greatest leverage to gold’s rising price is owning gold exploration/development junior mining stocks.

Will mainstream investors eventually catch on to the fact they need to own both gold and gold shares?

Investors are catching on to the fact they need to own precious metals and are buying shares in ETF’s and physical gold and silver. The buying of shares in companies involved in the search for and development of gold projects will not be too far behind.

“I am amazed by how nervous more and more Investors or shall I say Gold traders are becoming. Every Bull Market must always climb a wall of worry and this market will be no different. Since so many of you seem to be wavering between whether you should become short term traders or stay as long term investors, perhaps a refresher course in making money and a little bit of hand holding may be the order of the day.

While a few succeeded by trading commodity futures; stock options, day trading or short selling. Jesse Livermore, the most famous of the short sellers who caught the top in 1929, nevertheless died broke. After a great deal of study and research it finally sunk in that most of them that achieved their ultimate goals were those individuals who identified a major Bull Market or an individual stock and RODE it for all it was worth. They bought and held during both the pleasurable upswings as well as through the sharp, terrifying down drafts, during which times they all took advantage of the down drafts to accumulate more stock. Then, when the Bull Market appeared to be in its final, frothy stage, they gradually sold their holdings to the late comers (who Joe Granville named the Bag Holders), who’s blind greed had them clamoring to get in at the top.” Aubie Baltin

Gold juniors are going to be the most rewarding, the most lucrative way to garner the huge rewards from the coming freight train rush to gold. Those golden tracks are being laid today using the world’s currencies as ballast – when your cash is trash your gold is shining.

There will be fierce merger and acquisition (M&A) competition for the juniors with stable safe gold ounces in the ground by producers having to replace their reserves in an extremely competitive environment. There aren’t very many decent sized deposits, ones over two million ounces, left in politically stable countries.

Junior resource companies, not majors, own the worlds future mines and juniors are the ones most adept at finding these future mines. They already own, and find more of, what the world’s larger mining companies need to replace reserves and grow their asset base.

If I was looking for superior investment vehicles to take advantage of what I think I know regarding precious metals I’d be assembling a portfolio of junior producers, near term producers and companies that are in the post discovery resource definition stage with the occasional green field exploration play thrown into the mix.

Company stage – risk v. reward

Only you can decide the level of risk you can tolerate and how much patience you have to sit while developments, the story, plays out.

The most upside (and by far the greatest risk) comes from buying a junior when they are exploring and make an initial discovery. Great drill assay results can send a juniors share price skyrocketing. The reverse can also be true. Junior explorers, the green field plays, are the riskiest plays by far. Strike out on assay results and it could be goodbye to a share price rise for a very long time – till the company finds another project they can work on. If you’re buying into this kind of play make sure the company has another fallback project in its portfolio.

My favorite stage junior is a junior in the post discovery resource definition stage (also known as brown field stage companies). These companies have all ready found something, the share price has settled back after the initial discovery and the company is going in to see what they have and hopefully produce a 43-101 compliant resource estimate and build upon it. The risk has been greatly reduced, the waiting time for a discovery non-existent and the reward very nice considering the much lower amount of risk.

For nearer term producers – for those further down the development path towards a mine – you have:

- Preliminary Economic Assessment (PEA) or scoping studies are done to examine potential mining scenarios and economic parameters – A PEA or scoping study is an important milestone for a mineral project, it’s the first step in a company’s economic and technical examination of a proposed mine

- Preliminary feasibility studies or pre-feasibility studies are more detailed than PEA’s and are used to determine whether or not to proceed with a detailed feasibility study. They are also used as a reality check to determine areas within the project that require more attention

- Feasibility studies will determine definitively whether or not to proceed with the project. A feasibility study or bankable feasibility provides budget figures for the project and will be the basis for raising capital to build the mine

Remember all these different stage studies are only yes/no decisions on whether to move to the next stage. NONE of them mean you are going mining, there’s no mine till every stage is completed, permits approved and the necessary financing has been arranged.

Because these companies are well advanced along the development path a lot of the guesswork about grade, size, costs and metallurgy have been taken out of the equation for us. They have done sufficient work to give investors a certain level of confidence that their project will successfully move towards being a mine.

The later stage companies (those doing feasibility, permitting and money raising) can have an excellent entry point for investors – they often enter a quiet period when they are doing the advanced studies and raising money to go into production. They often base (a flat share price) for quite a while through this period – possibly a good time for accumulation of their shares if you believe in the story. After the money is raised for production investors can see they are going mining – cash flow is just over the horizon – and the share price will often break out of its trading range.

With producers you have to look at the balance sheet, consider their plans for the future and judge for yourself the ability to meet those plans.

Remember cash flow is king, but can they grow that cash flow? These large well established producers have the least risk and the least upside. But gains could be steady and maybe they pay a dividend.

“As every contrarian speculator knows, no market ever moves straight up or straight down indefinitely…Pullbacks are entirely normal and healthy in major bull markets and should be expected and embraced as wonderful opportunities to “buy the dips”, as our tech friends used to prudently say before their bubble burst. Short-term pullbacks are necessary to relieve temporary overbought conditions and graciously grant new entry points for fresh capital, as well as lay the foundational groundwork for drawing in ever increasing numbers of investors.

A powerful bull market requires a slow, steady march northwards in spectacular rallies and then sharp pullbacks to ultimately seduce the greatest amount of capital possible to bid on the market and drive up prices. If gold is indeed to run to the $5000 range as I suspect before all the dust settles on this new gold bull in coming years, it needs to run up as cautiously and methodically as possible at first. Each pullback offers the golden bull a crucial feasting opportunity to gulp down more fresh capital which feeds it the energy necessary to gallop aggressively to new highs in the next major upleg rally.” Adam Hamilton

Remember, our junior resource companies, the same ones who today are so oversold and undervalued, are the present owners of the world’s future gold supply.

“Richard Cantillon (died 1734) the Irish economist and financier who wrote one of the earliest treatises on modern economics and whose treatment of the theory of money was of pioneering importance give a pithy description why both these metals posses all the qualities needed in money. Gold and silver, wrote Cantillon, are alone are of small volume, of equal goodness, easy of transport, divisible without loss, easily guarded, beautiful and brilliant and durable almost to eternity. Anne-Robert-Jacques Turgot (1727-81) the French economist was more adamant and asserted that gold and silver became universal money by the nature and force of things, independent of all convention and law; consequently to proscribe either of them by law from being used as money is a violation of the nature of things.

It is because of this almost immutable law of value, recognized by most thinking people, that gold was not only the Ancient Metal of Kings but the future standard currency in a post-fiat money system.” overlordsofchaos.com

Junior resource companies, the owners of the worlds next precious metal mines, are soon going to have their turn under the investment spotlight and should be on every investors radar screen.

Are they on yours?

If not, maybe they should be.

Richard (Rick) Mills

www.aheadoftheherd.com

If you’re interested in learning more about the junior resource and bio-med sectors please come and visit us at www.aheadoftheherd.com

Markets yawned at rate cuts from the European Central Bank, China’s “central bank,” and more quantitative easing by the Bank of England. Money is draining from emerging markets,as discussed last week. Corporate earnings forecasts are being managed lower. The global macro view we’ve held for a while seems to be playing out on cue-unfortunately for those of us that live in the real world.

… During the Dow Jones Industrial Average swoon in the midst of the last credit crunch crisis, gold fell about 27% peak to trough. We expect a similar pattern to emerge. Remain short for now!

Market Vitals for July 6th/2012

Quote

“Civilized countries generally adopt gold or silver or both as money.” Alfred Marshall

Of Interest

Lagarde Says IMF to Cut Growth Outlook as Global Economy Weakens (Bloomberg)

Entire Commentary

Markets yawned at rate cuts from the European Central Bank, China’s “central bank,” and more quantitative easing by the Bank of England. Money is draining from emerging markets, as discussed last week. Corporate earnings forecasts are being managed lower. The global macro view we’ve held for a while seems to be playing out on cue—unfortunately for those of us that live in the real world. Private deleveraging seems to be overwhelming public sector debt creation (or shall we call it the “bastardized Keynesian scream of panic” from clueless policymakers). For as much as we have criticized the Keynesian policies supporting government deficit spending, it seems very doubtful Keynes would approve of what’s going on now, no matter what Paul Krugman or Larry Summers say. Gold is the one asset targeted again, or shall we say, continuously, by global investors looking for a place to hide during this storm.

And from a longer term time frame, it has been very good. But it has also not played the role of safe haven when most needed (see chart below); and we don’t believe it will this time. We think the private sector liquidity demands i.e. need to sell a good asset to cover the ones gone bad, will push gold sharply lower as it did during the initial stages of the credit crunch.

Action

During the Dow Jones Industrial Average swoon in the midst of the last credit crunch crisis, gold fell about 27% peak to trough. We expect a similar pattern to emerge. Remain short for now!

![]()

But the concept of inflation is poorly understood. In today’s world it is thought of as simply rising prices due to shortages. In economics there are several forms of inflation that appear in different circumstances.

Overall governments favor low inflation because it gives the appearance of rising wealth as prices rise, provided that these levels are restrained around, say 3%. Above that and savings are visibly damaged and consequently the economic power of a nation.

But we are moving far away from such a concept now. In today’s world the bulk of inflation has come from rising oil prices [an insidious, usually imported inflation] and the like. At the moment, we are at a time when inflation is at very low levels, so low they no longer represent a fear or concern.

Deflation is now the global fear, far more so in the developed world than in the emerging world. But the deflation we are talking about is not simply an economic slowdown. Today’s deflation is a decay of trust, of confidence and consequently, hope. Deflation breeds prudence, caution, discouragement, which attacks growth. Banks slow down their lending, delay the processing of loan requests, take only very secured collateral for their loans. Individuals save in the hope that they can manage those rainy days they see coming.

As the current type of deflation persists, it accelerates slowly but surely. Central banks [particularly Mr. Bernanke] are aware of this and try to simply promote an expansion of money that replaces lost asset values and no more. It is critical that no more than has been lost to asset/debt deflation, be added.

There is a point where adding too much by way of newly issued money, that it is inflationary, cheapening the price and value of currency itself. This inflation is a very different animal to the one the public perceives it to be. As deflation rises, so there is a point where inflation takes off and becomes much more difficult to control. In fact, that point becomes ever more mercurial as deflations spreads and confidence continues to sag, as it continues to do in the States and in Europe right now. It is probably a misnomer to call it inflation because it is a cheapening of the value of money.

Since 2008 we have seen the process of money creation happen first through QE, then as the European Central Bank used swap arrangements with the Fed to do the same, through the unlimited window of credit to European banks. This has left the banking system relatively solvent, when it would have collapsed without it. But what looks to be a set of now relatively healthy balance sheets ignores the continuing asset/debt deflation that goes on unabated. The reason it becomes mercurial in nature is because new money issues have less and less affect as the deflation progresses. As this ineffectiveness in producing greater economic activity grows, the only answer appears to be to defer, or seemingly halt, more deflation and recession, so more money is issued. This is where the current impasse between Germany and the weaker members of the Eurozone are in conflict now.

But more new money can only provide a temporary solution, because it is only greater economic activity that can resolve the problem. It is growth that produces economic health and the ability to repay debt.

As debt mires such growth reliance on new money at some point exacerbates the problem giving rise to a greater and greater demand for more money. Money cheapens during the process, but if governments can act in concert to stop that from being seen in falling exchange rates, then an atmosphere of normalcy is maintained. This does fool most people for a while, but its fragility grows. We are now seeing an exchange rate between the dollar and the euro moving so little that it is hiding the real extent of the Eurozone crisis!

At some point politicians and bankers have to make an extremely difficult choice. Do they let the economy suffer the full range of symptoms of deflation, or, for the sake of political stability and civil calm, do we keep patching up the mess with bandages of ‘new money’. With votes needed to continue their careers, politicians are likely to go for the soft option of ‘new money.’

Loss of asset value hits cash too

During this time the value of savings are destroyed either through providing no, or nearly no real return, as we see now in the States and almost in Europe, or all [except cash holdings] drop in price. As interest rates are unlikely to rise for the next couple of years, cash yields are nearly zero.

You would think that savings wouldn’t drop in value during deflation and that with asset prices falling, the old adage that “cash is king” would hold true. It doesn’t, because in this global world of ours, exchange rates can easily decay and lower the international value of cash. As this happens, imported goods increase in value giving cash less buying power. So we have to re-define what we mean when we say “cash is king”. What cash? U.S. dollars [it has a coming debt crisis that dwarfs that of Europe, postponed by the system of monetary and fiscal union it has] or the Swiss Franc [the government is holding the exchange rate down, killing it as a ‘safe-haven’ or the Yen [they are doing the same as the Swiss]? Many investors are turning to property in the belief that that will hold value in the most cosmopolitan of nations and cities. But will it? The evidence is that only in relatively exclusive cities is this happening, but in many nations property has failed to retain value.

Demand for liquidity blossoms

Then there comes a point where the demand for liquidity continues to grow and overwhelm the liquidity available [remaining stagnant in favored pools, in banks and balance sheets, too fearful to venture outside].

At this point we see the “Black Hole” of deflation sucking in more and more money. So just to stand still and hold what economic activity there is, the demand for money continues to grow and overwhelm whatever is thrown at it, but still not producing greater economic activity.

And this is the trigger point, when cash deflates in value. This is the start of runaway inflation, producing no good at all. Money itself has lost confidence and ceases to be an expression of value as its issuance accelerates. At its worst this process becomes hyperinflation.

By this time businesses are collapsing, banks failing and the only people who are thriving are those who avoid money, changing it into some asset or goods immediately it is received.

For example;

One must own the farm that produces food, own the transport that takes it to market, own the market stall and have access to asset into which to change it before its value is depleted.

Meanwhile, social extremes are being seen in politics, at community levels when stress takes a firm grip on ordinary citizen’s lives. The social consequences of the process scar entire generations.

Right now it is that fear that is holding back Germany from loosening the reins on its solvency as memories of the Weimar Republic and its hyperinflation in 1923 re-surface in the following generations.

During this entire process of deflation, fuelling growing inflation, politicians come under greater and greater pressure to do something. But the system of Democracy itself mitigates against their ability and willingness to take effective action! It takes a collapse of the monetary system and political system, before there is sufficient will in people to rectify matters.

You, the reader, have to decide not just where we are in this process but can it be halted now? Is there the political and financial will to halt the process or are we silently watching that point pass in the calming waters of media and political reassurance? How close to such extremes happening are we now?

What happens to gold and silver during this time?

The joys of both silver and gold are that they are both cash and an asset at the same time.

– Gold and silver can’t be printed.

– They have always been internationally accepted cash.

– More importantly they are acceptable in the world’s monetary system as money in the form of reserve assets.

– Gold becomes collateral that facilitates loans at cheaper interest rates.

These qualities grow throughout the above deflation and subsequent inflation.

Member’s only:

– Measures of value and eventual confiscation

Get the rest of the article. Subscribe @

U.S. software stocks are about to enter a period of seasonal strength. The North American Technology-Software Index has a period of seasonal strength from the first week in July to the last week in September. Average gain per period during the past eight periods was 9.0 per cent. The trade was profitable in six of the past eight periods. What are prospects this July?

The reason for seasonal strength in the sector is anticipation of revenue and earnings gains related to new consumer electronic products expected to launch prior to the Christmas shopping season. Companies are busy developing compatible software prior to launch of the next generation of new products. This year, the launch of next generation products prior to the Christmas shopping season is exceptional. Most notable are the expected launch of iPhone5 in October and the official launch of Microsoft’s Windows 8 operating system as early as this month.

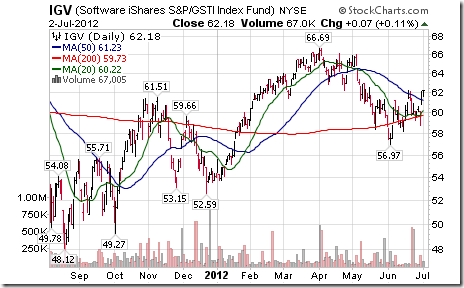

Three North American software Exchange Traded Funds (ETFs) trade on U.S. exchanges. The most actively traded ETF is the Software iShares (IGV US$62.18). Management Expense Ratio is 0.48 per cent. The portfolio holds fifty four actively traded U.S. software stocks listed on U.S. exchanges. The second most actively traded ETF is PowerShares Dynamic Software Portfolio ETF (PSJ US$26.65). Management Expense Ratio is 0.60 per cent. The portfolio holds 31 software stocks. The third ETF is SPDR S&P Software & Services ETF (XSW US$61.49). Management Expense Ratio is 0.35 per cent. The portfolio holds 138 software stocks.

Investors can choose an ETF based on their risk/reward profile. The two most actively traded ETFs are fully diversified with well-known big cap software stocks. Top ten holdings in Software iShares are Microsoft, Oracle, SalesForce.com, Intuit, Adobe Systems, Citrix Systems, Red Hat, Symantec, CA and AutoDesk. The SPDR S&P Software & Services ETF focuses on small and mid-cap holdings with greater price volatility.

On the charts, Following is an eight year seasonality chart on the S&P North American Technology-Software Index.

Software iShares (IGV $62.18) has a positive and improving technical profile. Intermediate trend is up. Support is at $56.97 and resistance is at $66.69. Units moved above their 20, 50 and 200 day moving averages last week. Short term momentum indicators are trending higher. Strength relative to the S&P 500 Index turned positive last week.\

Preferred strategy is to accumulate software ETFs and related equities at current or lower prices for a seasonal trade expected to last until the end of September.

Don Vialoux is the author of free daily reports on equity markets, sectors, commodities and Exchange Traded Funds. He is also a research analyst at Horizons Investment Management, offering research on Horizons Seasonal Rotation ETF (HAC-T). All of the views expressed herein are his personal views although they may be reflected in positions or transactions in the various client portfolios managed by Horizons Investment. Horizons Investment is the investment manager for the Horizons family of ETFs. Daily reports are available athttp://www.timingthemarket.ca/

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair