Timing & trends

In this interview, famous short-seller Jim Chanos (runs his portfolio of $115M) talks about his background, first short, Chinese bubble, etc. Among his point of views are:

– China will have whatever GDP growth number the Government wants (even if the numbers do not add up);

– China makes Greece and Spain look like Childs’ play, due to bad credit;

– Many (mostly Chinese) companies on the Hong Kong Exchange do not even have financial statements.

Gold Sells Off Yet Is Still Out Performing All Other Commodities- Especially Real Estate

The chart above shows the S&P TSX Real Estate, Gold, Energy and Financial Services Indices as well as the Bank of Canada Commodities Index (CRB) all valued in CA$. In May 2012 the energy sector continued to sell off keeping a lid on the CRB despite the strong US$. Gold also continued its correction while real estate was flat and financials slumped. With a subdued CPI the “real” price of gold trend is rising. Gold is out performing all other commodities and especially real estate. Gold is very liquid while Real Estate can be a “slow” asset and become unsellable (See history notes here and here). Check your return on investment with this Evaluator; if buyers suddenly vanish you might have to look for tenants and then your hope for capital gains becomes a job of managing a Return on Investment, if there is one.

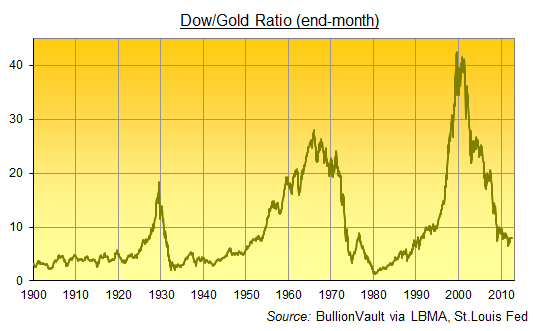

Dividing the Dow Jones index of stocks by the Gold Price 80 years after its low…

PLENTY OF PEOPLE pay close attention to the Dow/Gold Ratio. Eighty years after it sank to its Great Depression low, you might want to take a look this week, too.

This blunt measure of stocks versus stuff gets nearly 5 million results on Google, posting some 650 unique stories on the Dow/Gold Ratio. Search volumes for the term “Dow Gold” don’t quite match “Kim Kardashian” say, over the last 5 years (nor even “Reggie Bush”). But spiking in late 2008 and mid-2011, they very nearly matched search volumes for “Treasury bonds” – a market priced at twice the value of all the gold in the world. So why the interest?

The Dow/Gold Ratio maps, over time, how the Dow index of US stocks is performing in terms of gold, rather than just in nominal dollars. Dividing the number of points in the Dow Jones Industrial Average by the Dollars in the gold price per ounce is simple enough. The aim is more complex – to show how investing in corporate America – the “world’s most successful economy”, as Harvard professor Niall Ferguson reminds us – is doing versus a lump of non-yielding, relatively useless metal that does so little, it doesn’t even rust.

Investment in Corporate America was doing very badly 80 years ago today, for instance. As the Great Depression really got motoring, the Dow/Gold Ratio marked Independence Day by dipping to its lowest reading since 1900, just after the Dow Jones Industrial Average was first born.

That Friday, 8 July 1932, the Dow closed at just 41 points, while the gold price held firm at $20.67 per ounce, then its official price as mandated by the United States’ Gold Standard Dollar. Priced in gold (which was still money back then), the US stock market dipped below 2.0 – and showed a drop of over 90% from its peak of only three-and-a-half years before, hitting what then proved its lowest level of the 20th century.

Yet US Inc. came to do worse still compared to the gold price in January 1980, however, when the Dow/Gold Ratio fell to just 1.0 – down more than 96% from its new record high of New Year 1966. So today’s equity investors might take heart from the last 10 months’ turnaround. Because sliding from the Tech Stock Bubble’s new all-time peak above 40, the Dow/Gold Ratio has risen after hitting a two-decade low beneath 6.5 in September 2011.

Indeed, the Dow Jones index has outpaced the gold price by 25% since last summer. Just think what the outperformance would have been if, say, Apple had been added to the Average instead of, say, Cisco when the Dow was last updated in 2009.

But that’s the problem with taking the Dow as a serious guide to anything much. Or so say its detractors, and they have a point. Or five.

While it’s not immutable – as gold is – the Dow Jones index still changes little, despite the changing fortunes of America’s biggest stocks. The Dow also includes only 30 out of the thousands of listed stocks traded on US exchanges, and 30 hand-picked stocks at that, chosen by a committee with few hard rules. Nor does the index weight those 30 stocks by their size in the market. Instead, it adds up their share prices, and then divides by a “Dow divisor”, an arbitrary number (currently 0.132129493 according to the Wall Street Journal) which itself has to be changed any time there’s a stock split or switch in the membership. That means that highly-priced stocks have more impact than lower-priced stock in much bigger companies.

So as a guide to corporate America, the DJIA falls short. But are broader indices – weighted by market capitalization – any better?

Not much to choose between the DJIA and the more inclusive, more rigorous S&P 500 index then. Not when they’re used to judge equity investing against buying gold. Indeed, the Dow has performed less badly against gold since its all-time top than the broader index has. One ounce of gold now buys 5.1 times as much Dow index has it did in mid-2000, ignoring transaction costs (first into cash and then into stocks). But it buys 6.4 times as much of the S&P 500.

The Dow/Gold Ratio thus captures in a very broad way how badly money invested in productive, go-getting America has fared versus the ultimate lump of do-nothing, get-nothing-but-avoid-absolute-loss stuff. Gold has clearly been the perfect place to bury your savings as the returns to equity capital have been overwhelmed by the risks. That’s also made the Dow/Gold Ratio the perfect long-term indicator for über-bearish equity bears.

“I would expect this out-performance [by gold] to continue for the next few years,” said Swiss wealth manager and Asia-based author Marc Faber in 2005, five years after the Dow/Gold Ratio began its descent. In the end, he forecast, “Gold holders will be able to buy one Dow Jones with just one ounce of gold.” But by early 2009, Faber had revised his opinion – “One day the price of gold will be higher than the Dow Jones,” he told a Barron’s roundtable that January. That same 1:1 ratio – seen briefly in early 1980 as the Gold Price peaked and US stocks headed towards what proved table-banging chance to buy cheap – also appeals to fellow stock-market doomsayer Bob Janjuah of Nomura (see Nov. 2011, or March or April 2012).

“The US Dollar price of an ounce of gold and the Dow will, I believe, converge at or around 1, at some point over the next 2 years or so. I have extremely high conviction on this. What I am not sure on is whether we converge at 7000, or at 14000.”

Put another way, the Dow could hold where it is, or halve in value. The gold price will be many times higher either way on Janjuah’s analysis. (We can’t find him daring to imagine parity might be lower. In that event, with cash itself surging in value and driving the mother of all deflationary depressions, owning gold at a price of say $1000 would likely appeal to very many more people than trusting Dow 1,000.)

Now, you might think appealing to the Dow/Gold Ratio for an equity forecast pretty lame. Especially if you appeal to the ratio’s all-time record bottom as if some iron law of history says that the early 1980s’ low must be revisited before the bear market in stocks is done. It didn’t even get there during the Great Depression!

What’s more, mean reversion would suggest gold is already over-priced and stocks are cheap, with both the Dow/Gold and S&P/Gold Ratios now sitting at just 50% of their half-century averages. So less apocalyptic analysts might pick a less dramatic extreme turning point (as this one did in February 2009). Less aggressive investors might also want to avoid trying to nail the very lowest low, making do with the 6-fold rise in gold’s equity value already seen since 2000.

Thing is, there would be another 6-fold rise on the table if the Dow/Gold Ratio did fall to 1.0 – and even if, buying early ahead of the ultimate cataclysm in stocks, you missed the bullet of failed corporations (the New York Stock Exchange contracted by 1-in-14 listed equities during 1929-1933, and by 1-in-28 during 1978-1982), then the unlisted brokerages holding your stocks for you would still be sure to struggle as the equity market sank. Buying gold gets you off-risk for anyone else’s financial failure, giving you price-risk alone and free from the danger of absolute loss.

That’s what drove the Dollar gold price per ounce to parity with the Dow in 1932 and 1980. If the world’s relentless banking crisis pushes it there again, having the guts to make the switch from preservation to equity-risk will be a rare thing indeed.

Adrian Ash

BullionVault

Gold price chart, no delay | Buy gold online at live prices

Adrian Ash is head of research at BullionVault – the secure, low-cost gold and silver market for private investors online, where you can buy physical gold today vaulted in Zurich on $3 spreads and 0.8% dealing fees.

(c) BullionVault 2012

Please Note: This article is to inform your thinking, not lead it. Only you can decide the best place for your money, and any decision you make will put your money at risk. Information or data included here may have already been overtaken by events – and must be verified elsewhere – should you choose to act on it.

Today, let’s have some fun and play Fairy Godmother to Quebec . Let’s grant the province the wish it articulated in Copenhagen . Wave the magic wand and poof, wish granted. Shut down Alberta ‘s oilsands, except, since it’s Quebec making the wish, we have to call it tarsands, even though it’s not tar they use to run their Bombardier planes, trains and Skidoos.

Ah, at last! The blight on Canada ‘s reputation shut down. All those dastardly workers from across Canada living in Fort McMurray, Calgary and Edmonton out of jobs, including those waitresses, truck drivers, nurses, teachers, doctors, pilots, engineers etc. They can all go on Employment insurance like Ontario autoworkers and Quebec parts makers!

Closing down Alberta ‘s oil industry would immediately stop the production of 1.8 million barrels of oil a day. Supply and demand being what it is, oil prices will go up and therefore the cost at the pump will go up, too, increasing the cost of everything else.

But lost jobs in Alberta and across the country along with higher gas prices are a small price to pay to save the world and not “embarrass” Quebecers on the world stage. Not to worry though, Saudi Arabia, Libya and Nigeria can come to the rescue. You know, the guys who pump money into al-Qaida and help Osama bin Laden target those Van Doos fighting in Afghanistan . Bloody oil is so much nicer than dirty tarsands oil.

Shutting down the oilsands will reduce Canada ‘s greenhouse gas (GHG) emissions by 38.4 Mt (megatonnes). Hooray! It’s so fun to be a Fairy Godmother! While that sounds like a lot, Canada only produces two per cent of the world’s man-made GHGs and the oilsands only produce five per cent of Canada ‘s total emissions or 0.1 per cent of the world’s emissions. By comparison, the U.S. produces 20.2 per cent of the world’s GHG emissions, 27 per cent of which comes from coal-fired electricity.

The 530-square-kilometre piece of land currently disturbed by the oilsands (which is smaller than the John F. Kennedy Space Center at Cape Canaveral , Fla. at 570 square kilometres) must be reclaimed by law and will return to Alberta ‘s 381,000 square kilometres of boreal forest, a huge carbon sink.

Quebec , of course, has clean hydro power, but more than 13,000 square kilometres were drowned for the James Bay hydroelectric project, permanently removing that forest from acting as a carbon sink.

But Fairy Godmother is digressing all over the place. While the oilsands only produce five per cent of Canada ‘s GHGs, it contributes much more to Canada ‘s economy. After all, oil and gas make up one-quarter of the value on the TSX alone. Alberta is also the largest net contributor per capita by far to Confederation and there are only two more — B.C. and Ontario .

Quebec hasn’t made a net contribution to the rest of Canada for a very long time. This is not to be critical (after all, Fairy Godmothers never criticize), it’s just a fact. In 2009, Albertans paid $40.46 billion in income, corporate and other taxes to the federal government and received back just $19.35 billion in services and goods from the feds. That means the rest of Canada got $21.1 billion from Albertans or $5,742 for each and every Alberta man, woman and child. In 2007 (the last year national figures are available), Alberta sent a net contribution of $19.49 billion to the ROC or $5,553 per Albertan — more than three times what every Ontarian contributes at $1,757. Quebecers, on the other hand, each received $627 net or a total of $8 billion, money which was designed to help “equalize” social programs across the country.

Except, that’s not what is happening. Quebec has more generous social programs like (nearly) free university tuition (paid for mostly by Albertans) and cheap provincial day care (paid for mostly by Albertans).

But in this Fairy Godmother world, poof, those delightful unequal programs have now disappeared! Quel dommage!

The July 2009 Canadian Energy Research Institute (CERI) report states that between 2008 and 2032, the oilsands will account for 172,000 person-years of employment in Ontario during the construction phase, plus 640,000 for operations over the 25-year period. For Quebec, the oilsands will account for 84,000 person-years of employment during the construction phase, plus 292,000 for operations over the 25-year period.

In total, the oilsands are expected to add $1.7 trillion to Canada ‘s GDP over the next 25 years.

Wave wand and Poof, Jobs, gone! So, now that the oil industry has shut down and left Alberta , Alberta has become a have-not province and so has every other province. Equality at last! Hugo Chavez will be so pleased.

Meeting our Copenhagen targets suddenly looks possible, as most of us can’t afford to drive our cars or buy anything but necessities, so manufacturers have closed their doors and emissions are way down.

The dream of many Quebecers to form their own nation and separate from Canada has died at last. Alas, in Alberta , separatist sentiment has risen dramatically, citizens vote to separate and the oil and gas industry returns.

Albertans start to pocket that almost $6,000 for each person that used to get sent elsewhere and now their kids get free tuition. Fairy Godmother’s work is done. Wish granted. Quebecers must now sign up for a foreign worker visas to work in Alberta to send their cheques back home so junior can start saving up to pay for college.

Licia Corbella is editorial page editor of The Calgary Herald.

Please keeps this message going, forward to as many as possible.

There’s a plausible path to $10,000 an ounce gold. And it doesn’t require a breakdown in civil society…

Speculators see central bankers as modern-day superheroes, able to push markets around with a single phrase. In the minds of most investors, Ben Bernanke, Mario Draghi and Masaaki Shirakawa might as well be wearing tights, masks and capes. These superhero central bankers continuously swoop down into the financial markets to defend them from downticks…and to insure that they always deliver capital gains.

The reality, of course, is that these superheroes are frauds. They have no superpowers…other than the power of mass delusion. The powers of Mario Draghi and the other central bankers in Europe are waning. Excess debt is like kryptonite: Each new wave of printing has less impact on markets. As the popular phrase goes: “This is a solvency problem, not a liquidity problem.”

In other words, new money supply cannot restore health to sick loans and government bonds. The only way to restore solvency to the system is to deflate the economy or slash the amount of debt in the system through mass bankruptcy.

Or is there another way? Is there a “reset button” that central bankers can push (with the approval of political leaders) that would restore balance to the system?

We know central bankers would never want to deflate the economy or crash the value of debt, which would destroy the banking system. So how about inflating the money supply to dilute the value of debt? All in one fell swoop?

Right now, central bankers are diluting the value of debt very slowly by pushing interest rates below the rate of inflation. Some call this “financial repression.” It’s an unspoken policy that has many negative consequences. What is an alternative, since all attempts to “fix” the current system with more borrowing and printing are failing?

How about the classical gold standard, which stands out as the least flawed of all the systems we’ve tried. Each nation could choose to peg its local currency to gold at a price that allows for enough growth in bank reserves to greatly reduce the burden of public- and private-sector debts.

Re-pegging a currency like the US dollar to gold at the current price (about $1,550) has its pitfalls. Most notably, it would not deleverage an overleveraged banking system. But re-pegging the dollar to something like $10,000 an ounce might do the trick.

Hedge fund managers Lee Quaintance and Paul Brodsky from QB Asset Management wrote a fascinating outline on the potential reintroduction of gold into the monetary system, while simultaneously implementing what one might consider a debt jubilee. I recommend reading the entire outline. Zero Hedge posted it at this link. QB explains the mechanics of how it could work in the US:

|

This path would weaken the economy-sapping effects of debt created since President Nixon closed the gold window. It would transform a debt-based currency into an asset-backed currency. No longer would one ask the unpleasant question “What backs the dollar?” and come away with even more questions (and a headache). Right now, the dollar is backed by Treasuries held on the Fed’s balance sheet, which are in turn backed by dollars, which are in turn backed by faith in fiat money — i.e., nothing!

QB’s monetization scenario would impose losses on certain parties as the reset button is hit, but unlike most of the policy prescriptions we’ve seen lately, it seems to solve more problems than it creates. Most notably, politicians could argue that this reset would involve “migration of value, in real terms, from leveraged assets to unleveraged goods, services and assets.” Wage earners would be winners relative to asset owners, because “stable to higher nominal asset prices would require even higher nominal wage and consumable pricing looking forward.”

This scenario argues for holding some shares in producers of physical commodities (especially gold miners), even if it feels like we’re in a deflationary environment. A gold standard, after a one- time debt monetization, would make for a more-balanced, efficient global economy less prone to violent booms and busts.

As an added bonus: Central bankers would no longer be viewed as superheroes! Just meager servants, pegging the money supply to gold and letting the free market determine the price of money. After all, when in history has central planning worked better over time than the free market?

We can hope the central bankers of the world stumble their way to a solution like that proposed by QB Asset Management before they inflict even more damage to the foundation of the global economy. Unfortunately, conditions may have to get much worse in financial markets, banking systems and economies before such “outside the box” ideas are considered. A defensive portfolio with exposure to gold and other real assets seems like the right mix in today’s environment.

Regards,

Dan Amoss

for The Daily Reckoning

Editor’s Note: We like it when things make sense, fellow reckoner. And at a time when those in charge of the world’s money seem to have little of it themselves, we’re increasingly happy to have gold on our side. As Dan points out above, there are numerous reasons why a gold-backed currency simply makes sense, and after seeing this presentation, we can tell he’s in good company.

Click here to discover a long-lost gold “bible” penned by none other than Congressman Ron Paul…and how you can snag a copy for yourself.

——————————————————-

Here at The Daily Reckoning, we value your questions and comments. If you would like to send us a few thoughts of your own, please address them to your managing editor at joel@dailyreckoning.com” title=”joel@dailyreckoning.com” target=”_blank”>joel@dailyreckoning.com

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair