Timing & trends

IN THE PAST, major Gold Mining exploration has tended to occur when the Dow was down and out. In this interview with The Gold Report, geologist and Exploration Insights writer Quinton Hennigh talks about a coming gold rush and what that could mean for existing companies.

The Gold Report: While the NYSE Arca Gold BUGS Index (HUI) is up a bit from its May low, it is still lagging the Gold Price and not living up to expectations based on the role it has traditionally played as a safe haven for investors. Are we close to a turning point in that dynamic?

Quinton Hennigh: Many investors and speculators are deservedly frustrated and dejected by the recent performance of gold and, more specifically, the Gold Mining sector. For many of us in this business these ups and downs are the norm; however, I see the current down as a critical one.

Something is going to happen. It could be a month, six months, a year or two years from now. We can’t know. We may continue to see more pain in junior stocks until then, but a change is coming, and investors should take heed.

TGR: Where are we in the cycle now?

Quinton Hennigh: Below is a chart of the Dow:gold ratio over the past 112 years. The peaks generally mark points when the Dow was running hot and gold was in the dumper. Conversely, troughs mark times when gold was riding high and the Dow was down. I have added a few interpretations to the chart. First, I projected this chart forward 25 years with a red line that I believe reflects a pattern that we are likely to experience, given a look back at history. Note that the red line bottoms out as the chart did in 1932 and 1980 and then slowly rises over the subsequent 25 years.

(Figure 1: Dow to gold ratio from 1900 to present and projected to 2035. Vibrant periods in the Gold Mining and exploration sector are highlighted in yellow.)

Second, yellow shading has been added to highlight periods when Gold Mining and exploration were generally more vibrant than other times.

TGR: How do you define more vibrant times for gold miners?

Quinton Hennigh: This is a bit subjective, but I see these as times when gold mines often made consistent money, the public felt comfortable investing in this sector and perhaps most important, exploration was well-funded, thus contributing to a plethora of great discoveries.

TGR: Why wouldn’t Gold Mining and exploration proliferate as the price of gold rises and the Dow:gold ratio falls?

Quinton Hennigh: At first glance, this pattern does appear counterintuitive. When the Dow is down, uncertainty and doubt rule as they do now. We are still climbing the “wall of worry” and that does not aid investment in possible future rewards.

Vibrant periods in the gold world appear to commence around peak Gold Prices and persist as gold slides downhill. Answers to this conundrum can actually be seen in the world around us right now. The Gold Mining world is presently experiencing ever increasing capital costs, unpredictable and almost universally high cost of production, and other uncertainties, such as increasing taxes and royalties in countries eager to take advantage of the rising Gold Price. It is not a comfortable time to invest in this sector.

TGR: So, when will that change?

Quinton Hennigh: I do not profess to be an economist, nor do I know when this pivot point, the bottoming of the Dow:gold ratio, will happen or at what level. I simply see this pattern as rather compelling. In fact, it is so simple even a geologist can understand it.

TGR: How can investors capitalize on these trends?

Quinton Hennigh: Mining and exploration trundle along during the “white” periods, but it is during the “yellow” times that things are really hopping. These are times when the “gold rush” mentality is alive; geologists are scouring new frontiers for fresh finds and big discoveries are made, one after another. During the period from 1980 through 1997, for example, there was a succession of world-class gold discoveries: Hemlo (15 million ounces (Moz)), Goldstrike (60 Moz), Pipeline (12 Moz), Yanacocha (35 Moz), Pierina (9 Moz) and Busang, the ultimate bubble top. These were discoveries that “made” companies.

Many investors scored huge returns on explorers that struck it big. Investments in majors also paid off. Looking back to the gold rush period from the 1930s through the 1950s, huge discoveries were made in the Witwatersrand of South Africa as well as numerous gold camps across the Canadian Shield. Again, these were discoveries that “made” companies. An investment in Homestake Mining in 1929 would have returned 600% by the late 1930s, the height of the Great Depression.

Looking still further back at the cycle that extended from the late 1800s through the early 1920s, gold rushes abounded in the western US, Australia, Canada, Africa and beyond. Great gold producers made investors fortunes during this boom.

TGR: Are many of these companies still around?

Quinton Hennigh: Not surprisingly, most major gold producers have roots in these “gold rush” periods. Although there were miners that found their start during the “white” periods, most of these are no longer around, likely because they were gobbled up in the subsequent frenzy. It will be interesting to see what happens to up-and-coming producers over the next few years—do they get bought or survive through acquisitions?

TGR: What comes next?

Quinton Hennigh: If the next few years play out as I think, we could be approaching a pivot point, one that ushers in the next gold rush. Given current market conditions this may sound crazy, but we could soon see a massive inflow of money similar to what occurred when gold last peaked.

Such a capital influx will likely accompany a sharp run-up in Gold Prices. Euphoria over gold, although likely short-lived, will pull in speculative money fleeing other sectors that are losing value. This influx of money will likely feed the next cycle of discoveries and acquisitions as it did in the early 1980s.

Again, I don ‘t know when this pivot point might occur. It could be a month from now, six months, a year or two years. The significance of the cycles is that legitimately profitable deposits will be highly sought after as we roll into the next “up” cycle for gold acquisitions and exploration.

Some 2,000 junior exploration companies are struggling to survive right now. They universally claim to be cheap and in possession of stellar projects. Some actually are cheap and a few do own above average projects. It is our conviction here at Exploration Insights that the few companies holding exceptional properties and deposits will outperform the general junior market and be the target of larger mining company growth strategy. It is our intention to own some of these.

TGR: How can an individual investor know which companies are worth owning?

Quinton Hennigh: We need to be positioned for this turnaround; specifically we need to understand what a major company is after and how it makes its acquisition decisions. This is something both Brent Cook and I are experienced with and have been involved in while working for major mining companies. There is much more to it than a good drill hole or reading a third party preliminary economic assessment. The resource has to be evaluated in the context of mining, operating and capital costs. Furthermore, location, existing infrastructure, jurisdiction, sociopolitical realities and environmental issues need to be factored into the price a major can afford to pay for a mineral deposit. But rest assured, if history is any guide, a turnaround is coming.

TGR: Thank you for your insights.

Buying Gold? Get physical bullion at the lowest prices on BullionVault…

When there is a crisis of confidence in a currency then it is the precious metals that gain. Visit any city in Germany or Austria this summer and there is a gold shop in a prominent location.

They have not quite replaced the banks yet. But the message is there for anybody with eyes to see. It is noticeable too that this is not just a phenomenon in the peripheral eurozone but in its teutonic heart.

Spanish interest rates

Then again you certainly are getting good rates on your money in Spain and Italy these days, let alone Greece. Spanish bond yields have passed the danger point of seven per cent.

This is what happens when debtors become scarred about not getting repaid. Interest rates go up. No matter than the ECB has set official rates at a record low.

You can only wonder how much further this trend will go before it ends. The trend is always the investor’s best friend but so often missed for the surrounding noise.

Can anybody really see a solution in sight to the eurozone sovereign debt crisis? Does one exist? The requirement is for a federal Europe that is still a planner’s dream and even then this is no magic solution.

Besides US observers who think Europe has it all wrong and that they have the debt problem cracked are among the most deluded of our time. The US also has a temporary solution based on continuing to borrow money and that is also coming to the end of the road.

For what is happening in Spain will also hit the US in the future. The central banks can only hold interest rates low as an emergency measure, eventually market forces will take over, crush the bond market and raise interest rates.

Historical precedent

You would almost think this is stating something controversial. It is simple stating the blindingly obvious.

History also tells us that when confidence in paper money fails, that is to say bank notes and bonds, it is to precious metals that the population turns. This process happens very gradually and then there is a crunch, a crash and a reset of valuations.

…more articles at Arabianmoney

I began writing what I thought would be a report. Toward the final chapters in Adam Smith’s Wealth of Nations, he wrote about Public Debt asking why anyone considered it to be quality since all government defaulted on their debts and never paid them off. I assumed the list wasn’t that long, since everyone knew about the defaults of Spain, France, and England. The more I began to investigate since Smith merely made that statement with no reference to such defaults, the more I was left in a state of devastating shock. When it comes to research, those that know me understand that I leave no stone unturned. I allow the research to carry me along a journey of exploration. I neverPRESUME anything and try to LEARN myself to round out my knowledge.It is almost finished. I am publishing for the first time the Table of Contents. There just seems to be such profound conviction that everyone will flee to gold, gold will save the world, and there is always an alternative for capital to flee. The emails from the Goldbugs just refuse to understand that there is also DEFLATION. Here is the latest:

“You assume two things here, sadly both are wrong. You assume firstly that the US dollar will always be more stable than (for example) the yuan, the Brazilian Real, the Euro. A dangerous and flawed assumption, one perhaps made by a dying Roman empire, and the British Empire too. Nope, always something new out there to step in. Your other assumption, even more flawed, and currently being proven wrong as I type the world over, is that capital will flee to another fiat. Nope, much of it will flee to (or try to flee to) solid physical gold. Because that is what the world has always done. ‘Giant’ money is already there, the US’s strategic enemies are already there, and adding gold reserves every month, rather than soaking up the ever-growing flow of US dollar debts.”

….read much more HERE

The acute global economic crisis today is the direct result of the continued wilful obstruction and overriding of the normal checks and balances that should operate within a capitalistic system of commerce. This interference has been perpretated by powerful banks and governments acting in collusion, for reasons of profit and power. At every instance in recent years when it looked like the economy was slipping into a necessary recession they have assumed a godlike role and stepped in to head it off. These periodic recessions are necessary to prevent excess debt building up within the system, but the banks liked the ever growing debt, because it meant ever bigger profits for them as they created money out of thin air and then lent it to everyone and everything and raked in massive interest payments. Being immensely powerful they exerted more and more control over governments and succeeded in bending them to their will, culminating in them “coming out” by actually maker bankers into Presidents and Prime Ministers, as has recently occurred in Greece and Italy. So there you have it – the world is now controlled and governed by bankers. The problem with this situation is that their objectives, which are the accumulation of ever greater profit and power, are at odds with those of the population at large.

….read more HERE

An urgent report on the next, explosive stage of the European crisis now unfolding before your eyes …

Yesterday’s election in Greece is just one chapter in this saga.

Regardless of its consequences, the European Union, the largest economy in the world, is now suffering under the weight of TWO traumatic crises striking simultaneously:

Trauma #1. Europe’s governments are in big trouble — debts out of control, tax revenues plunging, interest costs surging.

Trauma #2. Europe’s banks are under siege — drowning in massive losses, swamped with withdrawals, and lining up for bailout money that no government can afford.

Find it hard to believe that the largest economy and banking system in the world is collapsing even as you read these words? Then, read on for the evidence …

Trauma #1. Governments in Big Trouble

Debts out of Control

Tax Revenues Plunging

Interest Costs Surging

Some people seem to think the European Union’s sovereign debt problems are limited to just a few countries that have been in the news.

Others seem to assume that the debts are relatively static and unchanging.

But the hard data shows that, in reality …

Europe’s debt troubles are widespread, making almost every country vulnerable to the contagion now spreading across the continent.

Of course you already know about the countries in the headlines:

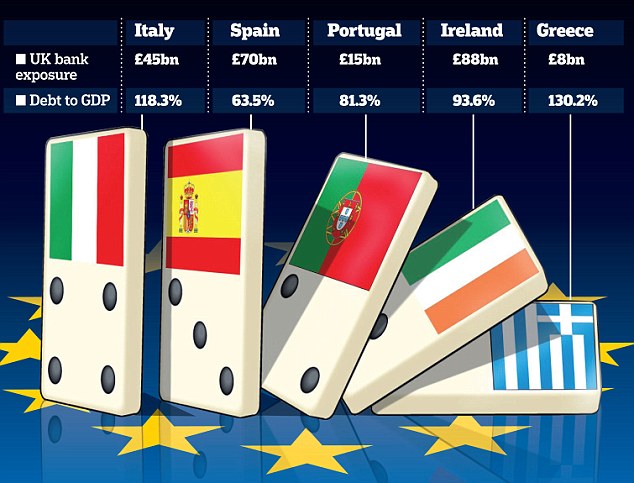

Greece with gross government debt of $315.8 billion … Spain with more than double that amount ($839.9 billion) … and Italy with debts that are SIX times larger than Greece’s (nearly $2 trillion)!

But what about the countries that have so far been viewed as “stronger”? Are they debt free?

Absolutely not!

France’s debts are almost as large as Italy’s — $1.8 trillion. And Germany’s debts are actually larger than Italy’s — nearly $2.1 trillion.

Plus, don’t forget others in the European Union, including Austria ($230.1 billion), Belgium ($374.3 billion), Finland ($101.1 billion), Ireland ($180.3 billion), the Netherlands ($427.6 billion), Portugal ($188.5 billion) and more!

Needless to say, not all countries are equal. Relatively speaking, some are stronger and others are weaker.

But here’s the key: They all belong to the same economic entity (the EU) and they’re all entangled in the same financial mess (the sovereign debt crisis).

That’s why it’s so important to note that TOTAL government debts owed by EU countries are now $8.6 trillion dollars — all based on the data from official sources compiled by Weiss Ratings.

Worse, despite all the sworn promises of austerity and all the solemn pacts to control deficits, the hard evidence also demonstrates that these debts are growing by leaps and bounds.

Official data shows that EU countries have added nearly $1 trillion in new debts just since the sovereign debt crisis began! And that doesn’t even include the massive new obligations of the EU institutions providing bailout funds!

And what’s most shocking is that nearly every effort to cut deficits has resulted in even larger deficits.

The main reason: Government cutbacks have slammed the economy. They have strangled the finances of the people. And they have bankrupted their businesses. So when all that happens, the end result is inevitable — they can’t pay their taxes!

Spain is a classic example. In fact, right now, the collapse in Spanish tax revenues is replicating the pattern in Greece, where fiscal revenues have fallen 4.8% in the past 12 months and Value Added Tax (VAT) revenues have plunged 14.6%.

The Daily Telegraph of London says “Spain is in the gravest danger since the end of the Franco dictatorship.”

Spain’s former premier Felipe Gonzales calls it “a total emergency, the worst crisis we have ever lived through.”

And just remember: Spain is NOT alone!

Surging Borrowing Costs

Spain’s borrowing costs have soared to 7%, widely considered the dividing line between stability and chaos.

Italy’s short-term borrowing costs have jumped wildly, as much as 164 basis points in a single day!

Other European interest rates are on a similar path.

This means that …

On top of collecting a lot less in revenues, they now have to pay a lot more for the money they desperately need to borrow.

But sinking government finances and financing is just one of the traumas striking Europe today. Also consider …

Trauma #2. Banks Under Siege

Drowning in Massive Losses

Swamped with Withdrawals

Lining up for Bailout Money

In addition to America’s banks and thrifts, Weiss Ratings now issues Financial Strength Ratings on all of Europe’s large banks.

And among the largest EU banks (with $200 billion or more in assets), there are now SIXTEEN institutions receiving a Weiss Rating of D+ or lower:

What does our rating of D+ mean?

According to a landmark study by the U.S. Government Accountability Office (GAO), it’s the equivalent to “speculative grade” (junk) on the rating scales of Moody’s, S&P and Fitch.

And also according to the GAO, Weiss was the only one that consistently warned ahead of time of future financial failures.

Indeed, if track record is any guide, our tougher grades — based strictly on the facts without any conflicts of interests — are consistently the most accurate.

Like Moody’s, S&P or Fitch, we look at each bank’s capital, earnings, bad loans, liquidity, and other factors.

But unlike the other rating agencies, we have never accepted — and WILL never accept — any compensation from the banks for their ratings.

Nor do we give big banks special credit based on the “too-big-to-fail” theory. We’ve said all along that, when push comes to shove, governments will have to save their own necks first and let failing banks fail.

Or, alternatively, they will have to print money and devalue the banks’ liabilities (YOUR deposits) in order to keep the banks alive.

Either way, depositors are at risk!

In Spain, we first gave Bankia its E+ rating (meaning “very weak”) three months ago — well before its massive losses were revealed, setting off the latest phase of Europe’s debt crisis.

But despite its $396.3 billion in assets, it’s not the largest Spanish bank in jeopardy:

Banco Santander is FOUR times larger with over $1.6 trillion in assets and merits a rating of D-, also deep into junk territory; while Spain’s BBVA bank, with nearly $775 billion in assets, gets a D.

And based on our metrics, Spain’s Caixabank (a $350 billion bank) is just as weak as Bankia with a rating of E+.

In Italy, Unicredit SpA gets an E+, despite its $1.2 trillion in assets; Intesa Sanpaolo merits a D-, and Banca Monte Dei gets an E.

What most people don’t seem to realize, though, is that most of the largest weak banks in the EU — and in the world — are headquartered in …

France! Crédit Agricole (with a massive $2.2 trillion in assets) is a candidate for failure with a rating of E and Societé Générale is not far behind with a D-. Plus, there are two other large French banks in jeopardy — Natixis and CIC.

But here’s the biggest — and most important — surprise of all:

Germany is NOT the safe haven most people think it is, especially when it comes to banking: In fact, the largest weak bank in the world is Deutsche Bank with $2.8 trillion in assets and meriting a D.

Commerzbank, with $857.6 billion in assets, is even weaker, getting an E rating.

All based on the same kind of objective, conflict-free analysis that helped us name nearly all the major failures of the last debt crisis well ahead of time! (See “The Only Ones Who Warned Ahead of Time.”)

Bottom line:

The total assets of just these 16 banks alone is $15 trillion, or about $1 trillion more than the total assets of ALL commercial and savings banks in the United States!

Who Saves Whom?

Late last year, the bonds of major European governments were sinking fast and Europe seemed on the brink of a meltdown.

So the European Central Bank (ECB) decided to come to the rescue with the aid of the largest banks.

The plan was simple:

The ECB hands the money over to the banks via special loans.

The banks hand the money over to sovereign governments by buying their bonds.

And everyone’s happy, right?

Wrong!

The plan has backfired: The government bonds have sunk anyhow. And the banks are stuck with even greater losses.

Now, a “new” old plan is hatching. Instead of banks helping to bail out their governments by buying their bonds … the idea is for governments to bail out their banks with money borrowed from the stronger governments of the European Union.

So one day they talk about banks saving the sovereigns. Next day, it’s the sovereigns savings the banks. They can’t seem to make up their minds as to who will save whom.

But …

Now the Public Is Beginning

To See Through This Charade!

They remember how many times the authorities have vowed that “the crisis is over.”

They know, first hand, how unemployment has gone through the roof.

They see the crisis feeding on itself.

So they are beginning to ask the real question of the day: Who sinks whom?

Will the sovereign debts sink the banks?

Will the banking crisis tear down the sovereign governments?

Or will they both go down in a spiraling cycle of bond market collapses and bank failures?

Our Suggestions …

1. Keep most of your liquid funds in cash, ready to be deployed on a moment’s notice, but as safe as can be right now. The best way: A short-term Treasury-only fund in the U.S., or equivalent.

2. Hold on to all long-term gold holdings. You do not want to let go of those. We feel gold could be headed to $5,000 an ounce over the next few years.

In the short term, however, we would not be surprised to see gold — and silver — move lower.

3. Consider prudent speculative positions to grow your wealth.

But no matter what you invest in — stocks, bonds or commodities — always be open to playing both the declines and the rises.

Even gold, silver and oil, despite major long-term bull markets, are bound to suffer further declines before turning higher.

And never forget this critical fact: As we’ve demonstrated here repeatedly, the U.S. government and U.S. financial institutions have made many of the same mistakes and are vulnerable to most of the same dangers.

Best wishes,

Martin and Larry

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair