Bonds & Interest Rates

Spain was down again before we noticed it was up. Yesterday morning, stocks all over the world were rising on hopes of a solution to the euro problem. By afternoon, the rally was over. The Dow ended the day down 142 points.

But that’s the way the euro rescues go. The effects are more and more short-lived. Pretty soon, investors will realize they don’t work at all…and then there won’t be any up-surge, A new rescue plan will be announced. Investors will realize it is just another scammy fix. And stocks will go down.

When that happens the game will be over.

We might not be far from that point now.

Meanwhile, the US is worried too. About Europe, which is on the verge of total breakdown? Maybe. About China, which is growing at its slowest pace in 13 years? Maybe.

About the US itself…where the ‘recovery’ went missing? Almost certainly.

Here at our Daily Reckoning headquarters, we remain sans soucis. Which is another way of saying, we’re enjoying the show. What will the fixers do next, we wonder? Every fix makes things worse. But they keep at it.

For the benefit of Dear Readers with skin in the game, we leave our “Crash Alert” flag up for a few more days. This market could go to hell in a hurry. If you’ve got skin in the game, get it out.

And, for the benefit of everyone, we cast our weary eyes down to the pampas. Is there any policy so foolish the Argentines have not had a go at it? Is there any financial disaster so catastrophic the gauchos haven’t repeated it at least two or three times? Is there any trick so dishonest or so transparently fraudulent that the politicians south of the Rio de la Plata don’t make a regular habit of it?

Our Bonner Family Office chief investment strategist, Rob Marstrand, who makes his home in Buenos Aires, is visiting us in the US this week. He tells us that it is said to be a crime in Argentina to mention the “parallel” market in dollars. On the official market, the peso still trades at about 4.4 to the dollar. On the unofficial exchanges, that is, on the parallel market, the “blue” peso trades at less than 5.1 to the greenback.

But it’s apparently illegal to mention it.

So is it supposedly illegal to publish the real inflation rate. The Argentine feds have their rate; it’s a crime to contradict them.

The government is also trying to get Argentines to stop using the dollar as a protection against peso inflation. The president says she is converting her own dollar deposits to pesos, to set an example.

“I guarantee you she is not converting her accounts in Switzerland,” says Rob.

But the typical Argentine wasn’t born yesterday. He’s been around the block a few times. He knows that when the government gets in financial trouble, it can’t be trusted. He knows that it will seize whatever money it can get its hands on — especially if it is foreign currency. So, if he’s saved dollars, he’s hiding them…or getting them out of the country. Here’s the Reuters report:

BUENOS AIRES, June 8 (Reuters) — Argentine banks have seen a third of their US dollar deposits withdrawn since November as savers chase greenbacks in response to stiffening foreign exchange restrictions, local banking sources said on Friday.

Depositors withdrew a total of about $100 million per day over the last month in a safe-haven bid fueled by uncertainty over policies that might be adopted as pressure grows to keep US currency in the country.

The chase for dollars is motivated by fear that the government may further toughen its clamp down on access to the US currency as high inflation and lack of faith in government policy erode the local peso.

From May 11 until Friday, data compiled by Reuters from private banks showed $1.9 billion in US currency had been withdrawn, or about 15 percent of all greenbacks deposited in the country.

Feisty populist leader Fernandez was re-elected in October vowing to “deepen the model” of the interventionist policies associated with her predecessor, Nestor Kirchner, who is also her late husband.

She wants Argentines to end their love affair with the greenback and start saving in pesos despite inflation clocked by private economists at about 25 percent per year.

Fernandez set an example on Wednesday by vowing to swap her only dollar-denominated savings account for a fixed-term deposit in pesos.

But savers in crisis-prone Argentina are notoriously jittery.

Why would they be jittery? Because their dollar deposits were seized and forcibly converted to pesos 10 years ago? Because the peso was devalued by 66% in the last crisis?

Or because the Argentine peso of 50 years ago has been devalued by approximately 42 trillion percent. We don’t know how such a thing is mathematically possible…but that’s the report we’ve read.

Defaults, devaluations, hyperinflations — the Argentines have seen it all.

Americans have a lot to learn.

And another thought…

The British writer AA Gill once noted that…

“Europe is an allegory for the ages of man. You are born Italian, relentlessly infantile and mother-obsessed. In childhood, you are English: chronically shy, tongue-tied clicky and only happy kicking balls or pulling the legs off things. Teenagers are French: pretentiously philosophical, embarrassingly vain, ridiculously romantic yet simultaneously insecure. During Middle-Age, we become either Irish and fun loving, or Swiss and serious. Old age is German: ponderous, pompous and pedantic. And finally, we regress into being Belgian, with no idea of who we are at all.”

Bill Bonner

for The Daily Reckoning

Bill Bonner

Since founding Agora Inc. in 1979, Bill Bonner has found success and garnered camaraderie in numerous communities and industries. A man of many talents, his entrepreneurial savvy, unique writings, philanthropic undertakings, and preservationist activities have all been recognized and awarded by some of America’s most respected authorities. Along with Addison Wiggin, his friend and colleague, Bill has written two New York Times best-selling books, Financial Reckoning Day and Empire of Debt. Both works have been critically acclaimed internationally. With political journalist Lila Rajiva, he wrote his third New York Times best-selling book, Mobs, Messiahs and Markets, which offers concrete advice on how to avoid the public spectacle of modern finance. Since 1999, Bill has been a daily contributor and the driving force behind The Daily Reckoning. Dice Have No Memory: Big Bets & Bad Economics from Paris to the Pampas, the newest book from Bill Bonner, is the definitive compendium of Bill’s daily reckonings from more than a decade: 1999-2010.

Special Report: Wait until you see what could happen in America next… An unbelievable phenomenon is set to sweep the nation… The railroad, steel, and technology age – this phenomenon triggered them all. And now it’s taking shape again! Watch this special, time-sensitive presentation now for full details on how it could affect your job… your lifestyle… and your wallet. Here’s How…

Read more: Learning from the Best: Inflation Lessons from Argentina http://dailyreckoning.com/learning-from-the-best-inflation-lessons-from-argentina/#ixzz1xgGs861q

Last week in an interview on CBS Network News, Economist Mark Zandi, the chief economist for Moody’s, unwittingly revealed a central error of the global economic establishment. Zandi has made a career out of finding the middle ground between republican and democrat economic talking points. As a result of this skill, he has been rewarded with large quantities of airtime from media outlets that want to appear non-partisan, despite the fact that his supposedly neutral analysis often leaves listeners frustrated.

Last week in an interview on CBS Network News, Economist Mark Zandi, the chief economist for Moody’s, unwittingly revealed a central error of the global economic establishment. Zandi has made a career out of finding the middle ground between republican and democrat economic talking points. As a result of this skill, he has been rewarded with large quantities of airtime from media outlets that want to appear non-partisan, despite the fact that his supposedly neutral analysis often leaves listeners frustrated.

When asked about the recent deterioration in the global economy, Zandi said that “the worst possible scenario” at present would occur if Greece were to leave the Eurozone. He claimed that the economic gyrations and liquidations of bad debt that would result from such an exit would be sufficient to create a vicious cycle that could drag the global economy back into recession. As a result, he urged policy makers to take whatever steps necessary to maintain the current integrity of the 17 nation Eurozone.

Given what most economists now know, few would actively argue that Greece’s entrance into the Eurozone back in 2001 was a good idea. In fact most concede it was a terrible idea based on bad forecasting and outright fraud. There is little disagreement over the fact that Greece grossly misrepresented its financial position in order to gain initial entry into the monetary union. It is also widely agreed upon that in the ensuing decade Greece exploited its monetary advantages to borrow irresponsibly.

Much has been written about how the fundamental misfit between Greece’s economy and currency gave birth to a deeply flawed system that was destined to run off the rails. Most also agree that the countries like Greece and Germany are too economically and culturally disparate to exist under the same monetary umbrella. But despite all this, Zandi wants to maintain the status quo. In his opinion, it is so imperative to prevent the deflationary consequences of an economic restructuring that it is preferable to prop up a failed system, perhaps indefinitely, rather than allow a newer, healthier system to replace it. In the process, the moral hazard created not only assures that Greece will become an even greater burden on Europe, but so too will other nations whose leaders will be emboldened in their profligacy by the anticipation of similar help.

From Zandi’s perspective (and he is certainly in the majority on this point) the goal of economic policy is to keep GDP growing. It follows then that he will oppose large-scale debt liquidations which drag down GDP in the short term. But sometimes debt needs to be liquidated. Bad ideas need to be abandoned. Once economies stop throwing good money after bad, capital is freed up to flow into more economically viable purposes. But economists and politicians never look at the long term. Their job seems to be to manage the economy for the next election.

The same “damn the torpedoes” mentality dominates economic thinking with respect to the U.S. economy as well. Years of artificially low interest rates, and government subsidies that direct capital towards certain sectors and away from others, has created an economy with too little savings and production, and too much borrowing and consumption. The ultra-low interest rates currently supplied by the Fed serve to perpetuate this unsustainable artificial economy. Higher rates would work quickly to redirect capital to the more productive sectors. But high rates could bring deflation and liquidation, which few economists are prepared to risk.

We have too many shopping malls selling stuff, but not enough factories making stuff. We have too many kids in college studying liberal arts, and not enough in the workforce acquiring skills that will actually increase their productivity. Banks are loaning too much money to individuals to buy houses, and not enough money to entrepreneurs to buy equipment. We have too many tax-takers riding in the wagon, and not enough taxpayers pulling it. The list is long, but the solutions are short.

We need to let interest rates rise to market levels, and allow the economy to restructure without government interference. We need to stop beating a dead horse and hitch our wagon to an animal that can really pull. The process will be painful for many, but like ripping off a band-aid, the pain will be over relatively quickly. However, since a painful restructuring means recession, politicians resist the cure with every fiber of their beings. So instead of a genuine recovery, one that will provide productive jobs and rising living standards, we get a phony recovery that produces neither.

Preserving a broken system merely to avoid the pain necessary to fix it only makes the situation worse. Propping up sectors that should be contracting prevents resources from flowing to other sectors that should be expanding. Keeping workers employed in nonproductive jobs prevents them from gaining productive employment elsewhere. Encouraging activity or behavior the market would otherwise punish discourages alternatives that it would otherwise reward.

Unfortunately, leaders on both sides of the Atlantic put politics above economics, and economists like Mark Zandi provide the cover they need to get away with it.

For in-depth analysis of this and other investment topics, subscribe to Peter Schiff’sGlobal Investor newsletter. Click here for your free subscription.

Click here to buy Peter Schiff’s best-selling, latest book, “How an Economy Grows and Why It Crashes.”

For a more in depth analysis of our financial problems and the inherent dangers they pose for the US economy and US dollar, you need to read Peter Schiff’s 2008 bestseller “The Little Book of Bull Moves in Bear Markets” [buy here] And “Crash Proof 2.0: How to Profit from the Economic Collapse” [buy here]

For a look back at how Peter Schiff predicted the current crisis, read his 2007 bestseller “Crash Proof: How to Profit from the Coming Economic Collapse” [buy here]

Lately, we’ve seen firms advertise high interest rates again .. using such terms as “guaranteed”, “mortgage backed”, “secured by real estate” or “preferred rate of return” or similar misleading words.

We do understand the desire for monthly income, especially by older folks or retirees ! The financial industry is full of clever marketing people, many with little or no real world investing experience .. catering especially to the uneducated and the retired income seekers.

An annual return in excessive of perhaps 5 or 6% has RISKS ATTACHED. Most normal businesses in the western world CANNOT sustain, over a long period of time, 6%+ fixed distributions without exposing you to undue risk !

Many real estate firms or other investment syndicators have gone bankrupt or into foreclosure during the recession of 2008/2009. Just because the recession is over doesn’t mean a 12% annual return, paid monthly, is very doable. It is only doable under some very select scenarios – but with very high risk.

One such risky investment class is construction, especially in commercial construction, resort locations, rural areas or in tropical locations. Another one is land development. A 3rd one is poorly performing real estate, especially in unusual, often remote locations. If you are the lender and the project does not perform as planned your capital is at risk especially if your “mortgage backed” or “real estate secured” loan is in 2nd position behind an expensive construction mortgage in 1st position. This lender is in priority to you and may take the asset away, through a foreclosure process, and you lose all your principal.

Therefore, understand the nature of the business, the experience & proven track record of the operator and the position your investment is in – don’t look only at the glossy marketing material. Promises and fancy charts and brochures are easily created, but delivering results in the real world is very hard!

Also, have a look at their existing balance sheet. If you see other mortgages that are higher than perhaps 5 or 6% BEWARE. Commercial mortgage terms today are around 5-6% .. lower for apartment buildings, around 4%. Therefore, if you invest with someone that has 8% or 10%+ mortgages on their balance sheet, ask WHY IS THAT .. and the answer should be (but usually is not): “because our business is very risky and no commercial lender would give us reasonable terms !! Therefore we are looking for suckers such as you to be fooled by a 12% interest rate, paid monthly”. Best to walk away from such an investment !

Keep in mind that in a 3 year construction project, the “interest” paid to you on a monthly basis is just a return of capital, from your own money .. or from new investments. A modified Ponzi scheme really ! The income in these projects comes from selling land parcels or condos .. years down the road. Therefore, always consider return OF capital before you consider return ON your capital when evaluating any investment option !

Consider that you have a capped upside, but can still lose all of your invested principal if the project is not selling as fast as planned or for the prices targeted. Consider the risk adjusted return, please .. not just the promised return. A bit like gambling in Las Vegas, you can double your money in a few minutes placing it on “red” on the roulette table, but on average, you’ll lose. The risk adjusted return is negative, despite the ad “double your money with us” !

Our website also has a report on ‘8 mistakes to avoid when investing in real estate syndications” that you will finds useful to distinguish between swindlers and serious operators: http://www.prestprop.com/8mistakes.html

Sincerely + Successful Investing,

Thomas Beyer, President

Prestigious Properties Group

T: 403-678-3330 or 877-434-4345

P.S.: Check the latest investment offerings here to invest your cash or RRSP into inflation protected hard assets – income producing real estate: www.prestprop.com or call Scotty or Travis or email us at investor@prestprop.com !

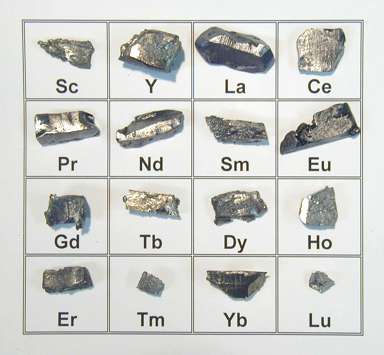

Resource developers, especially in the rare earths space, are suffering from the market’s obsession with immediate results, says Byron King, writer and editor for Agora Financial’s Outstanding Investmentsand Energy & Scarcity Investor newsletters and contributor to the Daily Resource Hunter. Nonetheless, he argues, large-scale demand for high-tech metals remains. The question is, which developers can weather the storm?

COMPANIES MENTIONED: ENERGIZER RESOURCES INC. – FLINDERS RESOURCES LTD. – FOCUS GRAPHITE INC. – LYNAS CORP. – MATERION –MEDALLION RESOURCES LTD. – MOLYCORP INC. – NEO MATERIAL TECHNOLOGIES – NORTHERN GRAPHITE CORPORATION – STANS ENERGY CORP.– UCORE RARE METALS INC.

The Critical Metals Report: In the last nine months, poor stock performance has shaken investors’ confidence in the rare earth elements (REEs) sector. What will restore their risk appetites?

Byron King: We need to see successful efforts from developers. Molycorp Inc. (MCP:NYSE) is not the success story it should have been. Molycorp presented itself as an all-American, mine-to-magnets resource, but when it joined forces with Neo Material Technologies (NEM:TSX), its research and development went to Singapore and its manufacturing to China. Its share price is down from a where it was a few months ago, let alone a year ago.

Lynas Corp. (LYC:ASX) was another great hope, but it has had trouble getting its plant in Malaysia up and running. Just as it was nearing the end of construction, local communities raised concerns about radiation in the materials the company is processing and bringing in from Australia. You have to wonder about the source of those problems. Cynics would say, follow the money. What do key Chinese players think about a new, Western player in the sector?

Looking at the smaller developers, their efforts have been slower and more expensive than expected. They prove the rule that nothing is easy in the REE space. It is a hard, technical space to work in. Many management teams are feeling their way through the maze.

Everybody is getting slammed. At the same time, some of the really smart money sees this as the perfect opportunity to buy low.” –Byron King

….read more HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair