Currency

“The European Central Bank has reached the limit of its mandate, especially in the use of non-conventional measures… In the end, these [efforts] are risks for the taxpayers.

“It’s like morphine, the LTROs provide relief from the pain, but are not a cure for the illness.”

–ECB Governing Council member Jens Weidman, May 25.

We have often thought that interventionism is the opiate of the intellectuals.

“Investors pulled $3.05 billion from junk-bond funds globally in the week ended May 23, the most since August.”

–Bloomberg, May 25.

“Home prices drop 2% to post-crisis lows.”

–Case Shiller, May 29.

“Consumer Confidence Plunges in May”

–Yahoo! News, May 29.

The Conference Board number for May is 64.9, down from 68.7 in April, which is the biggest hit since October. The consensus was for 70. February’s 71.6 was the highest in a year.

Note that junk-bond withdrawals and consumer confidence have quickly moved to numbers seen at the culmination of the last crisis–away back last fall.

Does this suggest that current distress is culminating?

Not likely, but it is poised for some relief.

Last year’s problems began to be revealed last May and culminated in late September.

CURRENCIES

The dollar has progressed to new highs for the move, as the sovereign debt crisis resumes. The short squeeze on the DX, which is one of the features of a post-bubble contraction, continues. We had thought that the action would briefly pause at the 81 level reached in January. It only spent a few days there and with some drama has popped to almost 83.

And this is the story–drama as the world discovers that last year’s “stimulus” is not working. Well, the global economy has been rolling over.

And yet, the establishment continues in its fanaticism that intervention will make a normal post-bubble contraction go away. Unfortunately, the rise in the dollar as well as yields in Euroland insist that it is not going away. Chart on Spanish bond yields follows.

However, last week we noted that the daily RSI had reached 77.7, which was a level that could limit the move. This is now at RSI 80 and that ended the last big rally, which was to 88.7 (for the index) in 2010.

This fits with the Euro now registering a daily Downside Capitulation.

Stability in the Euro would make most everyone think that the pressures are over and Ross’s model has been reliable in signaling a rally.

This would fit with our outlook for choppy financial markets through the summer.

As instructive as it is, let’s call it a mini-crisis that is close to ending with the dollar at a daily RSI of 80. A major crisis, as in 2008, could culminate with a weekly RSI out at the 80 level. Possibly later in the year.

COMMODITIES

Last week we noted that the CRB was getting as oversold, with an RSI at 22, as at the double bottom last fall. That was at the 281 level and it has dropped to 275 with an RSI at 21. Mainly, this seems to be due to this week’s extension of weakness in crude oil and the fresh hit to natural gas. Cotton and sugar have seriously extended their 52-week lows. Cotton has plunged from 115 a year ago to 71 now. Sugar has dropped from 27 to 19.5.

This really confirms that a cyclical bear started from our “Forecaster” signal in 1Q2011.

However, base metal prices (GYX) at 363 have yet to take out last fall’s low of 356. At an RSI of just under 30 it is getting oversold enough to limit the move.

The grain’s index (GKX) has dropped to 397 and is testing last December’s low of 397. Who cares if it takes out the low, but where are the inflation bulls when you really need them?

It seems that most commodities are beat down enough to expect choppy action through the summer.

Stock Markets

Last week, the S&P got down to an RSI of 23 which could be the momentum low for the move. With this week’s pressures the index has slumped to 1311, which we take as testing last week’s low of 1292.

This will likely hold and general stock markets could be choppy through the summer. Perhaps another new paradigm is developing – – the “All-One-Chop” model?

Other than that, we are looking for a “Typical” summer. Pundits will describe each rise as a “Typical Summer Rally” and each set back will be a “Typical Summer Doldrum”.

GOLD STOCKS RELATIVE TO BULLION

- Gold’s have generally underperformed since the economy and orthodox investments arose out of the crash in mid 2009.

- Base metal mining stocks outperformed the rise in base metal prices. That ended in 1Q2011.

- The gold sector is preparing to outperform most every sector—on the planet.

SPANISH BONDS

BOB HOYE, INSTITUTIONAL ADVISORS

E-MAIL bobhoye@institutionaladvisors.com

WEBSITE: www.institutionaladvisors.com

The first investor is Anne Scheiber, who turned a $5,000 investment in 1944 into $22 million by the time of her death at the age of 101 in 1995. The second investor is Grace Groner, who turned a small $180 investment in 1935 into $7 million by the time of her death in 2010. The third dividend investor is Warren Buffett, the Oracle of Omaha himself.

Dividend investing is as sexy as watching paint dry on the wall. Defining an entry criteria that selects quality dividend stocks with rising dividends over time and then patiently reinvesting these dividends while sitting on your hands is not exciting. While active traders have a plethora of hedge fund managers on the covers of Forbes magazine there are not many well-publicized successful dividend investors. Even value investing has its own superstars – Ben Graham and Warren Buffett.

….read how these investors did it HERE

Mark Leibovit: My reaction to Bernanke’s testimony in Congress yesterday is simply that the sooner this corrupt house of cards collapses, the better off we’ll all be!

Bernanke only knows one thing: How to print more money! If you think that is going to change whether you call it QE3 or secret actions masked under the protected cloak of the Federal Reserve, guess again.

A sixty point rally in the S&P 500, a 500 point rally in the Dow Industrials and a 420 point rally in the TSX is apparently ‘all she wrote’ for this upleg. Whether we’ve seen THE low for my predicted May to July cyclical trough, only time will tell. (Ed Note: Mark recently went Bullish on Stocks based on Cyclical and seasonal patterns)

VRTRADER.COM Trial Signup:

Here is the Special Trial Offer: Use this month to kick our tires. Pay 50% for the first 30 days (No refund) and sample our Silver or Platinum service and then decide what works best for you. If you aren’t 100% ready to move forward, simply email us to cancel one week before your 30 day 50% off trial subscription ends and it will be canceled and you will not be charged ANY FURTHER, no questions asked. Just send an email to mark.vrtrader@gmail.com” data-mce-href=”mailto:mark.vrtrader@gmail.com” data-mce-href=”mailto:mark.vrtrader@gmail.com“>mark.vrtrader@gmail.com“>mark.vrtrader@gmail.com” data-mce-href=”mailto:mark.vrtrader@gmail.com“>mark.vrtrader@gmail.com or call 928-282-1275 to cancel. You will receive an emailed confirmation of your cancellation at that time.

The 30 day trial is allowed one time only. By taking this 30 day 50% trial, you agree to be charged the full cost of the monthly Silver or Platinum service (choose one only) at the end of the 30 day trial subscription period, unless you cancel first. The regular Silver monthly rate is $49.40 and the Silver quarterly rate is $133.50. The regular Platinum monthly rate is $129.95 and the Platinum quarterly rate is $350.85. The special trial 50% off trial rates are listed below. Sign up today!

There are no refunds or pro-rata refunds offered at VRTrader.com for any subscription. You are being offered a 50% discount for trying our service for the first 30 days only!

SIX DAYS after they climbed back above $1600 an ounce, gold prices dropped back below that level on Thursday, as Federal Reserve chairman Ben Bernanke appeared before Congress at the Joint Economic Committee. (more below -Ed)

This is not the first time we’ve seen this. Back on February 29, gold fell $100 an ounce while Bernanke was testifying before the House Financial Services Committee. What on earth is the man saying to have such an adverse impact on gold prices?

Well, on the two occasions cited above, it wasn’t what he said, but what he failed to say that did the damage. In short, Bernanke failed to make any explicit promises of further Fed quantitative easing.

Last Friday, gold shot up 5% in Dollar terms, following disappointing US jobs and manufacturing data. Clearly, some traders were betting that the Fed would respond by announcing further stimulus, a bet that failed to pay off. Bernanke’s reticence in this regard is hardly surprising, though. It’s what central bankers do: they say as little as they can get away with to keep as many options open as they can.

They also talk to each other, and it seems the major central bankers have agreed a common script, one which has as its central theme a focus on the failings of fiscal policymakers (i.e. politicians). Here is European Central Bank president Mario Draghi speaking on Wednesday:

“Some of these problems in the Euro area have nothing to do with monetary policy. That is what we have to be aware of and I do not think it would be right for monetary policy to compensate for other institutions’ lack of action.”

And here’s Bernanke a day later:

“…under current policies and reasonable economic assumptions, the [Congressional Budget Office] projects that the structural budget gap and the ratio of federal debt to GDP will trend upward thereafter, in large part reflecting rapidly escalating health expenditures and the aging of the population. This dynamic is clearly unsustainable…fiscal policy must be placed on a sustainable path that eventually results in a stable or declining ratio of federal debt to GDP.”

Translation: don’t look at us.

Central bankers are trying to put pressure on their political masters to deal with problems that are beyond the scope of monetary policy. It is these problems, they argue, that are at the root of the current crisis.

It was put to Bernanke by JEC vice chairman Kevin Brady that the Fed itself is encouraging political inaction by keeping QE3, a potential third round of quantitative easing, on the table.

In other words, the belief that the Fed is on standby to combat any crisis makes a crisis more likely, reducing as it does the incentive to take difficult preventative action.

The trouble is, the Fed and other central banks daren’t row too far back from talk of stimulus for fear that this will provoke a crisis. This is why Bernanke made it clear the option was on the table, while also saying “Look over there” and pointing at the so-called fiscal cliff – the combination of tax cut expiries and mandated spending cuts that await the US should lawmakers fail to reach agreements to prevent them (a genuine risk in an election year).

So we are at an impasse, meaning gold prices are susceptible to marginal sentiment and bets on what monetary policymakers will do next. This has been the case all year. For example, gold prices rallied in January after the Fed published projections showing its policymakers expected near-zero interest rates until late 2014. Gold also saw a jump in March as Bernanke reiterated the need for accommodative policies.

The truth is, though, that there has been little rhyme or reason to these moves. If you look at what Bernanke actually said on each occasion, it is pretty much a rehash of what he’s said before. Fed statements since the start of the year have all broadly said this: “We’re not out of the woods, we’ll keep an eye on things, and we’ll do as we see fit.”

Details have changed, depending on the newsflow, but that’s all. Here’s an extract from Thursday’s testimony:

“…the situation in Europe poses significant risks to the US financial system and economy and must be monitored closely. As always, the Federal Reserve remains prepared to take action as needed to protect the US financial system and economy in the event that financial stresses escalate.”

Later on, Bernanke said there is “no justification” for fears that QE could spark inflation. Taking these comments together, one could make a case that the Fed are about to push the button marked ‘More Stimulus’. But of course, traders had already jumped to that conclusion last Friday, and so were forced to ‘unjump’.

The truth is, we don’t know when or if we will see more QE, and we doubt anyone at the Fed does either. QE is not about economic stimulus. Not really. It may be packaged as a way of boosting growth, but in our view its real aim is to fight crises in the banking sector.

This is where it gets difficult for gold investors. It may be that the Fed, along with other central banks, are holding fire until the banking stresses in Europe become really acute. As we saw last November and December, a banking crisis can be accompanied by sharp falls in gold prices, as gold is sold or leased to raise Dollars, increasing its immediate supply and putting downward pressure on prices.

Indeed, along with the disappointment that Bernanke was note more dovish following last week’s economic news, another possible explanation for gold’s fall this week is that uncertainty over QE raises the risk of a sudden funding crunch.

Another factor to bear in mind is inflation expectations. Bernanke said on Thursday that these are “quite well anchored”. But some argue that they are still too high to make QE an immediate prospect, with 5-Year breakeven rates – the difference in yield between inflation-linked and nominal debt – still too high:

There remains a significant chance we will yet see more Fed QE. But things may need to get quite a bit worse first. In the meantime, the only clues we are likely to get are those we can glean from the Orwellian radio static of central banker doublespeak.

Or, if you’re a long run investor, you could just ignore the noise being made by gold prices and crack open a beer…

Ben Traynor

BullionVault

Gold value calculator | Buy gold online at live prices

Editor of Gold News, the analysis and investment research site from world-leading gold ownership service BullionVault, Ben Traynor was formerly editor of the Fleet Street Letter, the UK’s longest-running investment letter. A Cambridge economics graduate, he is a professional writer and editor with a specialist interest in monetary economics.

(c) BullionVault 2011

Please Note: This article is to inform your thinking, not lead it. Only you can decide the best place for your money, and any decision you make will put your money at risk. Information or data included here may have already been overtaken by events – and must be verified elsewhere – should you choose to act on it.

Based on the June 7th, 2012 Premium Update. Visit our archives for more gold & silver analysis.

We have all seen the newspapers headlines about the troubles in Greece, Spain, Portugal, Ireland and the entire eurozone. The situation in the U.S. is not much better, even if the press is ignoring it for the moment. In both blocks there is high debt and large, long-term entitlement programs for citizens without any clear notion of where the money to fund these programs will come from. (Hint–the printing press.)

The global economic situation is unstable and untenable. How long can citizens in the West continue to buy more and more imported manufactured goods from the East? When the West’s appetite for unessential consumer goods will lessen as people learn to do with less because they have no choice, the economic situation in China and South East Asia will be even worse than it is in the west. The West can always go back to manufacturing, but it’s unlikely that Asia can go back to agriculture.

The month of May was possibly the worst month for gold prices in three decades, but it was unexpectedly followed on Friday, June 1, by the best daily climb–$66 — since last August. The principal catalyst was the dismal US job report by the US Labor Department. Economists had hoped to hear about the creation of 150,000 positions, but the actual number was half that, 69,000, which brought on expectations of another round of QE, (that is, Quantitative Easing, not Queen Elizabeth who celebrated her 60 years Jubilee this week). It was interesting to note how the same financial media outlets that had eulogized the bull market just a week ago were now celebrating its return as a safe haven.

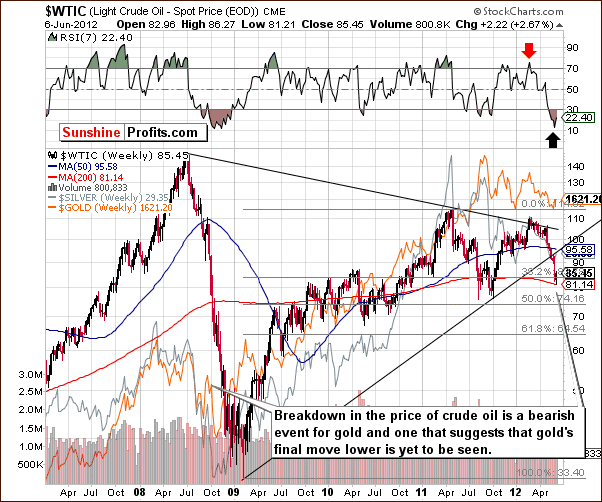

With that in mind, let’s take a look at the technical picture. Let’s begin with the analysis of the crude oil market (charts courtesy by http://stockcharts.com.)

,….read more HERE (comments & Charts on Gold

“A country that represents less than 2% of the Euro block and a tiny fraction of the world economy continues to be the tail that wags the dog. If it is resolved favourably there should be a fairly strong rally in precious metals prices. This would translate into gains for juniors though the current level of fear in the market would take time to dissipate.”

WORLD’S DUMBEST POLITICIAN

A country that represents less than 2% of the Euro block and a tiny fraction of the world economy continues to be the tail that wags the dog. We’ll all have to wait until June 17th to see whether Greeks vote with their emotions or with their heads. Currently it looks like it could be the former, which would not bode well for markets.

The US and Germany have both released decent economic readings but that won’t be enough to overcome fears of yet another debt meltdown unless the Greek vote goes the right way. Negative news out of Europe pummels the Euro and the correlation between the value of the Euro and commodities is currently very high. Metals prices aren’t going anywhere until the issue is resolved.

If it is resolved favourably there should be a fairly strong rally in precious metals prices. This would translate into gains for juniors though the current level of fear in the market would take time to dissipate. If things go well small producers, advanced developers and the occasional strong drill play would get some traction. Many others will need to rebuild their markets and balance sheets which wouldn’t start until autumn in many cases.

Keep an eye on the Euro chart and the polls out of Athens. It will be a volatile and none too predictable market until the polls close (again).

Everyone has a favorite in this race. The World’s Dumbest Politician contest never has a lack of entrants and some days it’s tough to choose between all the contenders. No longer, however. The events in Greece have lifted one contestant so far above the rest that we simply have to declare him the winner.

You may think this is a reference to Alexis Tsipras, the leader of the left wing Syriza party. We’ll get to him later. No, without a doubt the mantle of Dumbest of the Dumb Politicos has to go to Antonis Samaris, the leader of the “winning” New Democracy party in Greece.

You may recall that New Democracy was the party in power in Athens before Pasok which was just voted out. New Democracy was mainly responsible for cooking the books and hiding deficits (with the help of Goldman Sachs) so that Greece could gain entry into the Eurozone.

Having been caught out and tossed from office Samaris later agreed to vote with Pasok on the latest bailout agreement. The condition of his agreement was to force an election on the Greek populace rather than have the government of technocrats under the Pasok banner keep running things.

Even though largely responsible for worsening the mess in Greece, New Democracy apparently thought they would get voted back into office with a higher seat count. Can you say “in denial”?

To give Samaris some credit, he at least has enough sense to understand the repercussions of reneging on the bailout agreement, which is more than can be said for all of the other party leaders other than Pasok.

Post-election there are now seven parties in parliament and five of them are “anti-bailout” or “anti-austerity” as they would prefer to be called.

The leader of this pack is Tsipras, former communist and student activist who is now the man with the momentum in Greek politics. This party came in second place on May 6th but more recent polls indicate he’ll be number one in the next election that should take place in mid-June.

In a second vote, Tsipras could leach votes from both minor parties that have little chance of being in government as well as from the two “major” old line parties. Small party leaders eyeing spots in a new coalition after a second vote don’t want to be seen as disagreeing with the probable coalition leader.

Where to from here? A second election campaign will be dominated by a leader who insists the EU is bluffing when it says Greece could be ejected from the Euro.

In fact, all anti-austerity parties insist Greece will be keeping the Euro, come what may. This makes one wonder just how reality challenged these politicians might be. They seem either incapable of grasping that Euro membership has conditions or are so cynical they are ignoring it.

Canadian readers of a certain age will be familiar with the phrase “sovereignty-association”. This was the twofaced slogan of the Parti Quebecois during the late 1970’s and early 1980’s.

The PQ insisted that Quebec would be able to vote for sovereignty and then negotiate an agreement that would give them everything they wanted from Canada. The wish list included keeping current borders and access to whatever federal programs were advantageous and, of course, continued transfer payments from Ottawa.

Even those who remember the economic mismanagement of Pierre Trudeau’s administrations appreciate how much of an impact he had on the Quebec sovereignty debate. As a respected Francophone Quebecer who also happened to be Prime Minister of Canada he was one of the few with the credibility to face down the separatists. He was able to convince enough Quebecers that the deal PQ followers were dreaming of was just that—a dream.

It’s unknown if there is someone with similar credibility in Greece, though there seem no obvious candidates. The Greek electoral system will not allow enough time for someone new to take over either old line party before the next vote.

Polls indicate that 70% of Greeks want the last bailout package to be renegotiated. Ironically, that is exactly the same percentage of respondents that want Athens to do whatever it takes to stay in the Euro. Clearly, a lot of Greeks hope both of these diametrically opposed agendas can be run in tandem. Is this possible?

An Greek anti-austerity politicians are betting that the last debt workout actually strengthens their hand. That agreement effectively transferred the bulk of Greek sovereign debt from banks to EU institutions.

Tispras has alluded to this ownership change but is seriously misreading the situation. The EU is far more worried about financial system and bond market contagion than it is about taking a write-off itself. The EU is a large economy. Writing off $3-400 billion will not be the end of the world as long as the situation is containable. There is more willingness to force Greece out of the EU and take the loss on its debt now than at any time since the crisis erupted.

While the Greeks may still want a free lunch most remember just how much lower the standard of living was before the country joined the Euro block. Those with even longer memories understand that a return to the Drachma will mean a huge loss of purchasing power and probable bankruptcy for anyone unlucky to have large foreign currency debts.

All that said, the austerity measures taken by Greece, Spain, Portugal and Ireland are pretty extreme. It’s easy to watch this unfold from the other side of the Atlantic (or Berlin for that matter) and say “they need to do more”. To put the situation in perspective, the annual cuts that Athens has pushed through in each of the last two years as a percentage of GDP is five times the level of budget cuts that politicians in Washington could not agree to last August. It’s true governments in the debtor nations have to do more but you can’t say they aren’t trying.

Ultimately debtor countries DO need to do more, but cutbacks have reached levels that are extinguishing hope in these countries. There is real danger a negative growth spiral, which Greece is already in, will make it impossible to balance budgets.

You can’t fix debt with more debt but it may be time for the creditor countries in Europe to come up with some extra cash for infrastructures programs or something else that generates a bit of hiring. Money should be focused on the countries that are making structural changes—like Ireland and Spain—in the hopes this lightens the mood some. Getting the debt levels down is obviously critical but making structural changes that make debtor economies more flexible is the only thing that will have a lasting impact.

In the broader Euro Zone, statistics just released indicate that the region scraped by in Q1 with zero growth, avoiding a recession but only just. That is wholly due to a much stronger performance by Germany which posted 0.5% growth as opposed to the 0.1% consensus estimate. These figures will sharpen the debate between Germany and France. Newly elected President Francoise Hollande is demanding a “growth pact” that provide some new spending funded by EU institutions.

Germans will view today’s figures as a vindication of their fiscal conservatism. There is some truth to that but it’s also arguable that Germany’s success shows the value of an open trading block. Germany is an export powerhouse and the cheap Euro has been a boon to it. Just as the peripheral countries would see their currencies plunge if they went back to pre-Euro days Germany would see its scrip balloon in value.

This doesn’t belittle Germany’s great strengths when it comes to quality, innovation and its relentless drive for higher productivity. Those are the long term reasons for its success and qualities other Euro countries need to emulate. Nonetheless, being in the Euro zone has been very good to Germany and other nation states know this. Germans have good self-interested reasons to be accommodating, at least to a point.

Gold, the Euro and Resource Stock Despair

A gold chart would be redundant since the Euro chart on the right says it all. The next month will be dominated by an unnecessary election in a minor country that represents 2% of the EU economy.

The Euro has been crashing and will swing wildly with every Greek opinion poll until the next election. Yields are rising in Spain and Italy and this trend will continue as long as bond traders expect Greece to be ejected.

Although some European economies are victims of real estate bubbles, many of the region’s troubles are self-inflicted. The EU has been dithering about how to handle the crises for three years and providing nothing but half measures and stopgap “solutions”. This has to end or things will continue to get worse before they get better.

As soon as the campaign in Greece restarts the rest of the continent has to make it clear and be unequivocal that the vote is about being inside or outside the Euro zone and nothing else. Even if there is room to give Greece some breathing space on austerity measures it must be made clear that loosening of conditions will only apply if there is a pro-bailout government. Even then, Greece may breach some debt covenants before it has time to complete a new vote, assuming that vote results in some sort of coalition.

Many of the debtor nations have been and are making large strides in dealing with their debt overhangs. The market won’t care about this if bond traders get to play “who’s next?” if there is a Greek exit. Greece should have been ejected from the EU three years ago. That didn’t happen so northern Europeans and particularly Germans will have to be prepared to do what it takes to hold the zone together or face the consequences.

Most Greek debt is no longer held by banks. There would be fallout in the swap markets but if the February deal is anything to go by it will be smaller than many fear. The important thing is to ensure the bond markets for other peripheral countries are protected. The ECB should be prepared to extend unlimited (and we mean unlimited) buying power in defense of Europe’s bond markets. It’s far more important t ensure Spanish, Italian and French bonds don’t crash than it is to save Greece. Tough sledding, but that’s just how things are.

Until there is some visibility in Europe gold and other commodities will track the Euro and resource stocks will continue to see fear and liquidity generating selling. It’s depressing to see and avoidable problem blow up yet again. Time really has run out for Greece and for Europe. Let’s hope cooler heads prevail—very soon.

Ω

Published by Stockwork Consulting Ltd.

Box 85909, Phoenix AZ , 85071 Toll Free 1-877-528-3958

hra@publishers-mgmt.com http://www.hraadvisory.com

The HRA – Journal, HRA-Dispatch and HRA- Special Delivery are independent publications produced and distributed by Stockwork Consulting Ltd, which is committed to providing timely and factual analysis of junior mining, resource, and other venture capital companies. Companies are chosen on the basis of a speculative potential for significant upside gains resulting from asset-based expansion. These are generally high-risk securities, and opinions contained herein are time and market sensitive. No statement or expression of opinion, or any other matter herein, directly or indirectly, is an offer, solicitation or recommendation to buy or sell any securities mentioned. While we believe all sources of information to be factual and reliable we in no way represent or guarantee the accuracy thereof, nor of the statements made herein. We do not receive or request compensation in any form in order to feature companies in these publications. We may, or may not, own securities and/or options to acquire securities of the companies mentioned herein. This document is protected by the copyright laws of Canada and the U.S. and may not be reproduced in any form for other than for personal use without the prior written consent of the publisher. This document may be quoted, in context, provided proper credit is given.

©2010 Stockwork Consulting Ltd. All Rights Reserved.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair