Stocks & Equities

05/22/12: Yesterday, stocks bounced…just as they should have. After two weeks of falling, they were ready to bounce. Heck, even a dead congressman will bounce, if you drop him from high enough.

The Dow rose 135 points. Not very impressive, after so many down days.

Everything has been sinking… Stocks, commodities, oil…

In Europe and emerging markets the damage has been even worse than in the US. Even China is slowing down.

It’s just like…well…a Great Correction!

And look at Facebook. We knew the Facebook IPO would cost a lot of saps a lot of money. But we didn’t expect it to happen so fast. We figured Wall Street would get a chance to squeeze the lumpen a little longer before they fled the market.

As it turned out, the mom and pop investors came into the market to buy Facebook and got whacked right away.

Here’s one completely un-savvy buyer quoted in The New York Post:

“I’m very psychic when it comes to stocks, I really am. I have no retirement, I have no pension, so I try to make money on the market.”

The press reported that cab drivers and plumbers were buying Facebook shares on the first day…for the wrong reasons, of course. One buyer had recently had his house foreclosed. He was buying the stock, he said, to help put his children through school. Good luck on that!

Colleague Justice Litle called it ‘Facebust!’ The hype sent shares up in early trading on Friday. The insiders who moved fast were able to cash out at over $40. But then, the selling overpowered the buying. Justice, writing over the weekend:

Countless idiots, er, optimists expected Facebook shares to pop 50% or more on their first day of trading, not taking into account the fact that, when EVERYONE IN THE WORLD has the same universally telegraphed notion as you — with ability to execute by mashing a mouse button — it is probably not the sharpest play.

At any rate, after a very anemic “pop” reminiscent of discount bin champagne purchased from a gas station, FB shares fell straight to the $38 level (where the IPO was officially priced).

At $38 the underwriter investment banks came in, vigorously “defending the shares” as a matter of business honor. Without the heavy buying of Morgan Stanley and others, for the express purpose of propping up the shares, FB could have seen a death spiral on its first day of trading. This would have forever marred said underwriters’ reputations, which is why it didn’t happen.

(Investment banks are paid a very pretty penny for bringing an IPO to market; one of the services they provide, in exchange for that fat payday, is propping up the shares, i.e. “creating a price floor,” with their own dough as need be, to keep the offering from looking like a dog. This is completely legal and sanctioned by the SEC.)

The Facebook IPO was a sort of psychological fulcrum point. It was perhaps the biggest public participation event of all time, in terms of getting “the man on the street” to take a flyer on a stock. When such tomfoolery works out badly, Joe Sixpack’s taste for risk — the mother’s milk of Wall Street — is that much further soured. (It should be noted that a whole raft of other “social media” stocks — Zynga etc. etc. — fell hard when Facebook came up short.)

In addition to the above, virtually every large mutual fund and long-only money manager on Wall Street felt compelled to purchase Facebook shares (for fear of missing out on “the next Apple” had they not).

If the Facebook hype fails, then — if the Maginot line of $38 price support gives way — it could have an incredibly demoralizing impact on the market as a whole, alongside the ominous “doom loop” that is Greece.

Such are the conditions in which “unease” turns to “maybe we should get out,” which then has a nasty habit of escalating to “GET ME OUT NOW,” acted upon by groupthink investors en masse.

And yesterday, the Maginot Line gave way…

“Market Up, But Investors Dump Facebook,” was the headline report from Reuters. The stock sold off…finishing the day down 11%. What happened to the underwriters, everyone wanted to know. The stock fell below the IPO price on its first full day of trading. Apparently, Wall Street was not willing to come to the rescue — not with its own money.

We had a hunch that Facebook might become the hinge event for this stock market. Shares had been selling off for two weeks prior to the FB launch. But the selling was orderly.

After so much selling for so many days, buyers are bound to come back. So the Dow went up yesterday.

But the FB hinge has creaked…and squeaked…and warned retail investors. They came in the door. They didn’t like what they saw. Many will take to the exits quickly. Others will stick around, until a growing sense of revulsion, mixed with losses, eventually pushes them out.

Ray Dalio calls it a “beautiful de-leveraging.” We don’t see the beauty in it. But we admire it for what it is — a natural and necessary response to the grotesque debt build-up of the last half century. It may not be beautiful, but it is doing its work as best it can under the circumstances.

Households are lowering their debt levels. Businesses are hoarding cash. The private sector, generally, is getting itself into better shape. All very natural…and all things in nature have a beauty, of sorts.

It doesn’t hurt that interest rates are so low. Even the price of gasoline is going down. In this sense, the Great Correction itself is helping…beautifully. The whole world economy is slowing down, lowering prices for energy and housing — two of the biggest items in the household budget.

The way to cut debt is to first cut expenses. Then, you have more money available to pay off your loans. And it’s fairly easy to cut expenses when interest rates are so low.

In 2005 and 2006 we advised Dear Readers to sell their overpriced real estate and rent. Now it’s time to reverse the procedure. At today’s rates…and today’s prices…it’s time to buy.

Here’s why:

In some areas, house prices are down 50%

In those very same areas rents have risen.

At 3% (which you can get on a 15-year fixed rate mortgage) your monthly mortgage payment might be only HALF your rent payment. So you can save money there.

Then, you deduct the interest from your taxes.

And then, the Fed gives you a bonanza when its monetary inflation finally turns into consumer price inflation…or even hyperinflation. Your mortgage balance could be reduced 10%…30%…80% in just a few months.

In other words, you get paid to wait for the feds to wipe out your mortgage!

Cut your expenses. Get into cash. Remember, our ‘Crash Alert’ flag is up. And a lovely correction is underway.

Tomorrow: how the vandals in Washington and at the Fed are defacing the “beautiful de-leveraging.”

Regards,

Bill Bonner

for The Daily Reckoning

Since founding Agora Inc. in 1979, Bill Bonner has found success and garnered camaraderie in numerous communities and industries. A man of many talents, his entrepreneurial savvy, unique writings, philanthropic undertakings, and preservationist activities have all been recognized and awarded by some of America’s most respected authorities. Along with Addison Wiggin, his friend and colleague, Bill has written two New York Times best-selling books, Financial Reckoning Day and Empire of Debt. Both works have been critically acclaimed internationally. With political journalist Lila Rajiva, he wrote his third New York Times best-selling book, Mobs, Messiahs and Markets, which offers concrete advice on how to avoid the public spectacle of modern finance. Since 1999, Bill has been a daily contributor and the driving force behind The Daily Reckoning. Dice Have No Memory: Big Bets & Bad Economics from Paris to the Pampas, the newest book from Bill Bonner, is the definitive compendium of Bill’s daily reckonings from more than a decade: 1999-2010.

Special Presentation Shocking gas price prediction released…A former Big Oil executive’s shocking prediction- “Gas prices could soar to “$7 to $8 a gallon.” Smart Americans are getting ready for gas price spike, but they’re setting themselves up to get rich as gas prices rise. Get the full details…

While it might not look like it now, the most investable trend over the next 20 years is going to be in the resource sector, the renewable and non-renewable resources, the minerals, ores, fossil fuels and biomass a wealthier and growing global population is increasingly demanding from finite supplies and already strained production capabilities.

For example:

The metal content of copper ore has been falling since the mid 1990s. A miner now has to dig up an extra 50 percent of ore to get the same amount of copper. As grade drops the amount of rock that must be moved and processed per tonne of produced copper rises dramatically – all the while using more energy that costs several times more than it use to. With the lower grades of ores now being mined energy becomes more and more of a factor when considering economics.

The average grade of gold deposits has been dropping as well.

“We took the nice, simple, easy stuff first from Australia, we took it from the U.S., we went to South America. Now we have to go to the more remote places.” Glencore CEO, Ivan Glasenberg in the Financial Times describing why his firm operates in the Congo and Zambia

Ed Note: Richard Mills entire argument & charts to support the conclusion posted below can be read in its entirety HERE

Conclusion – Junior’s, An Argument for a Contrarian Investment

Our reality – we’re living on a relatively small planet with a finite amount of reserves and a growing human population.

The world’s major miners are making immense profits but they are having an extremely difficult time replacing reserves let alone growing them. Mining is the story of depleting assets, that asset must be constantly replenished, miners that want to stay in business must replace every pound, oz and gram taken out of the ground.

Juniors, not majors, own the worlds future mines and juniors are the ones most adept at finding these future mines – majors do not make discoveries, juniors do, that’s their function in the resource food chain. Junior resource companies already own, and find more of, what the world’s larger mining companies need to replace reserves and grow their asset base.

Junior resource companies – the same ones who today are so oversold and undervalued – are the present owners of the world’s future commodities supply and, most important for investors seeking outsized returns, they act like leveraged exposure (with price gains many times that of the underlying commodity) to the specific commodity(s) investors want exposure to.

Are there a few junior resource companies, with exceptional management teams operating in politically safe jurisdictions, on your radar screen?

If not, maybe there should be.

Richard (Rick) Mills

If you’re interested in learning more about the junior resource and bio-med sectors please come and visit us at www.aheadoftheherd.com

Site membership is free. No credit card or personal information is asked for.

I am a contrarian by nature. I generally try to do the opposite of the crowd in every situation I find myself regardless of whether I am in a movie theater or trading options. As expected, the gold miners have shown relative strength recently. The miners were just absolutely massacred during the recent selloff in equities and precious metals.

CLICK HERE to read the full article

The challenge current investors face is that sovereign debt default via inflation/currency debasement obviously doesn’t create any new wealth but it certainly reallocates it amongst economic participants, and it is a process that takes place largely unnoticed until it is too late for most.

Sadly, that is the entire point of the ongoing zero-interest rate policies – to quietly expropriate as much scarce capital as possible for the benefit of bankrupt but politically influential sectors of the economy – particularly in finance and real estate.

Where do you invest in such a world – a world of negative real interest rates, bloated central bank balance sheets and solvency challenged governments? I do not intend this letter to be a definitive answer to that question by any means, rather a quick overview of some ideas which we believe are worth consideration.

There are still pockets of good risk-adjusted returns to be found in the developed world despite the relentless overall deterioration in western growth fundamentals – or perhaps due to the dogmatically Keynesian mindset of our monetary and fiscal authorities, because of them. I hope it does not come as a surprise that for the diligent researcher there are ways outside of gold to go long monetary malfeasance while obtaining some growth exposure and perhaps a margin of safety as well.

Consider the value of commodity-linked returns in a politically stable part of the world – western Canada. Commodity production assets, or more generally commodity linked cash flows, have interesting inflation hedging characteristics, can be useful tail risk hedging tools (farmland) and when located in Canada provide linkage to emerging market growth and tight supply dynamics without emerging market risk. In addition, agriculture and energy have another useful quality in volatile times – highly inelastic demand curves.

For those unfamiliar with western Canada’s commodity endowment, it is a region with less than 10 million inhabitants but is the epicenter of one of the world’s most impressive concentrations of real assets. Its approximate global reserve rankings (or production rankings in the case of beef, timber and wheat) are as follows:

- Potash – 1

- Oil – 2

- Uranium – 3

- Timber – 5

- Wheat – 6

- Gold – 7

- Beef – 10

- Natural Gas – 20

The advantage of producing the commodities that the emerging economies need and importing the manufactured goods they make is significant – western Canadian growth rates have averaged twice those of central Canada over the last decade. So for investors looking for commodity linked returns with political safety – western Canada is a good choice.

Why the reference to political risk? When seeking to generate commodity linked returns political risk can never be ignored, as I believe it is a key differentiator of returns. Just ask investors in Sino-Forest or YPF to name just two recent demonstrations of this principle.

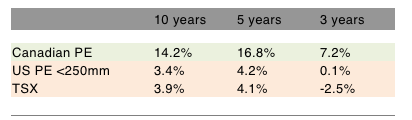

Private Equity (“PE”): Canada has some of the best PE returns globally (particularly smaller transactions):

At the most basic level western Canadian PE returns are linked to commodity prices and the consistently higher and more stable rates of growth that have been occurring in this market. However, there are some additional factors driving returns as well: Firstly, there is a strong supply of small & medium enterprise deal-flow in western Canada due to high levels of entrepreneurship (roughly speaking a “SME” is a business with less than 100 employees or an enterprise value of less than $10 million). SME penetration in the west is almost 30% higher than the Canadian per capita average.

Secondly, the number of Canadian baby boomer retirees has been increasing rapidly and is projected reach more than 40% of the working age population by the late 2010s. It is no secret that baby-boomers continue to be an influential cohort and in retirement will have a significant effect on the pricing of assets, just as they did during their key investment years, except now they are entering liquidation mode. The effect on the private equity market is simple – retiring baby boomer entrepreneurs must sell their numerous SME businesses which should create both deal flow and downward pressure on cash multiples. Phrased another way, PE returns should improve.

Saskatchewan Farmland: Since the beginning of 2007 Saskatchewan farmland has appreciated at a rate of over 12% per year due to increasing agricultural commodity prices but much more because of a large price discount to fundamentally identical land in the neighboring province of Alberta. In fact, the differential between the rate of appreciation of similar land in Alberta and Saskatchewan is over 50% with Saskatchewan farmland generating substantial “margin of safety” returns as the long-term price parity with its neighbour is restored. On a fundamental price per bushel of yield basis Saskatchewan stills trades at a material discount to global averages, a diminishing legacy of regulatory barriers to capital that have disappeared for domestic investors.

Conventional Heavy Oil: When investing in conventional heavy oil in western Canada, you are subject to two discounts: 1) the discount of heavy to WTI prices and 2) the discount of WTI to global prices. Conventional heavy oil represents a relatively inexpensive oil BTU and we believe spreads will compress over time, enhancing returns to heavy oil production assets. In addition, we are experiencing historically low natural gas (“NG”) prices. The perverse effect of low NG prices is to force operators with high levels of NG in their production mix to sell oil production assets to raise capital. This in turn tends to creates oil production deal flow – even though oil cash flows are robust.

Natural Gas: For the extreme value oriented investor with a long-term horizon, NG assets with large reserves and low production levels necessary to maintain leases represent a low cost-of-carry long position. Our analysis leads us to believe that for this purpose such a position has distinct cost, volatility and return advantages over traditional long NG futures exposures or investments into operating companies. Assuming that the market will find a way to exploit one of the most inexpensive BTUs in world (North American NG) then we should expect prices to recover over the medium to long term as these BTUs are eventually pulled into other markets – perhaps in the form of feed stocks (ethylene & propylene), finished goods (fertilizers) or LNG. Obviously this is not an investment with a view to an immediate return but for value investors who believe in the long-term strength of the energy markets surely something worth considering.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair