Personal Finance

“They are coming to take your money away Ho Ho, Hee Hee, Hum Hum!”

I have been warning that government is getting VERY aggressive all because of the Sovereign Debt Crisis. I have warned that this problem CANNOT be solved in the manner in which they are pursuing – taxing everyone & everything. They are about to destroy the economy and we are headed toward a major period of authoritarianism. There is a steady flow of bills being introduced in Washington that are design to eliminate the Constitution all to save the Bureaucracy. They are going to make DWI a federal offense. Sure, drunk drivers are dangerous. The question becomes what is drunk? When there is money involved and profit for government, do not be foolish to really think they are doing anything for society. The kill switch on the Internet is to cut off the free press and to eliminate the right to assemble since they saw how the Arab youth used social media to organize their revolutions.

Now on January 1st, 2013, the US government will be requiring everyone to have direct deposit for Social Security checks and pensions. Why? Well guess what. There is another bill HR 4646 that will impose a 1% tax on ALL transactions in a bank account. This is not income. This is money flow – a 1% tax on all bank transactions which will include paychecks, retirement checks and Social Security checks. That will even include a 1% tax on your refund check from the IRS. They want direct deposit and eliminate “paper money” to enable them to now tax your cash flow regardless if you make money or not. This bill was introduced by Representative Chaka Fattah (D-PA). They will tax everything before REFORM because this is all about retaining power. The next target 2016 is looking very grim indeed. Forget the gold standard. They want everything electronic and eliminate cash!

….read more about the Sovereign Debt Crisis by Martin Armstrong HERE

Warren Buffett – Berkshire Hathaway First Quarter 2012 Fund Portfolio

Here is a current portfolio update of Warren Buffett ‘s Berkshire Hathaway (BRK.A)(BRK.B) portfolio movements as of the end if the first quarter 2012 (March 31, 2012). In total, he has 35 stocks with a total portfolio worth of USD75,300,250,000. Buffett bought two new companies and added seven additional stocks. The biggest influence had Wal-Mart ( WMT ) and Wells Fargo ( WFC ). Both had an impact of more than 0.5 percent of his portfolio. He decreased seven stocks and closed one.

Here are his top positions in detail:

Wells Fargo & Company ( WFC ) has a market capitalization of $164.41 billion. The company employs 264,900 people, generates revenues of $49,412.00 million and has a net income of $16,211.00 million. The firm’s earnings before interest, taxes, depreciation and amortization (EBITDA) amounts to $31,310.00 million. Because of these figures, the EBITDA margin is 63.37 percent (operating margin 29.22 percent and the net profit margin finally 20.03 percent).

Financial Analysis: The total debt representing 13.28 percent of the company’s assets and the total debt in relation to the equity amounts to 124.39 percent. Due to the financial situation, a return on equity of 12.19 percent was realized. Twelve trailing months earnings per share reached a value of $2.91. Last fiscal year, the company paid $0.48 in form of dividends to shareholders.

Market Valuation: Here are the price ratios of the company: The P/E ratio is 10.65, P/S ratio 2.03 and P/B ratio 1.26. Dividend Yield: 2.84 percent. The beta ratio is 1.34.

The Coca-Cola Company ( KO ) has a market capitalization of $167.20 billion. The company employs 146,200 people, generates revenues of $46,542.00 million and has a net income of $8,634.00 million. The firm’s earnings before interest, taxes, depreciation and amortization (EBITDA) amounts to $12,596.00 million. Because of these figures, the EBITDA margin is 27.06 percent (operating margin 23.06 percent and the net profit margin finally 18.55 percent).

Financial Analysis: The total debt representing 35.72 percent of the company’s assets and the total debt in relation to the equity amounts to 90.31 percent. Due to the financial situation, a return on equity of 27.37 percent was realized. Twelve trailing months earnings per share reached a value of $3.77. Last fiscal year, the company paid $1.88 in form of dividends to shareholders.

Market Valuation: Here are the price ratios of the company: The P/E ratio is 19.67, P/S ratio 3.59 and P/B ratio 5.30. Dividend Yield: 2.75 percent. The beta ratio is 0.52.

Intl. Business Machines ( IBM ) has a market capitalization of $225.94 billion. The company employs 433,362 people, generates revenues of $106,916.00 million and has a net income of $15,855.00 million. The firm’s earnings before interest, taxes, depreciation and amortization (EBITDA) amounts to $26,266.00 million. Because of these figures, the EBITDA margin is 24.57 percent (operating margin 19.64 percent and the net profit margin finally 14.83 percent).

Financial Analysis: The total debt representing 26.90 percent of the company’s assets and the total debt in relation to the equity amounts to 155.54 percent. Due to the financial situation, a return on equity of 73.43 percent was realized. Twelve trailing months earnings per share reached a value of $13.41. Last fiscal year, the company paid $2.90 in form of dividends to shareholders.

Market Valuation: Here are the price ratios of the company: The P/E ratio is 14.60, P/S ratio 2.11 and P/B ratio 11.31. Dividend Yield: 1.74 percent. The beta ratio is 0.66.

American Express ( AXP ) has a market capitalization of $63.76 billion. The company employs 63,700 people, generates revenues of $32,282.00 million and has a net income of $4,899.00 million. The firm’s earnings before interest, taxes, depreciation and amortization (EBITDA) amounts to $10,194.00 million. Because of these figures, the EBITDA margin is 31.58 percent (operating margin 21.55 percent and the net profit margin finally 15.18 percent).

Financial Analysis: The total debt representing 41.08 percent of the company’s assets and the total debt in relation to the equity amounts to 335.18 percent. Due to the financial situation, a return on equity of 27.64 percent was realized. Twelve trailing months earnings per share reached a value of $4.18. Last fiscal year, the company paid $0.72 in form of dividends to shareholders.

Market Valuation: Here are the price ratios of the company: The P/E ratio is 13.25, P/S ratio 1.98 and P/B ratio 3.43. Dividend Yield: 1.44 percent. The beta ratio is 1.82.

For an entire list of the holdings in Warren Buffet’s full portfolio go HERE

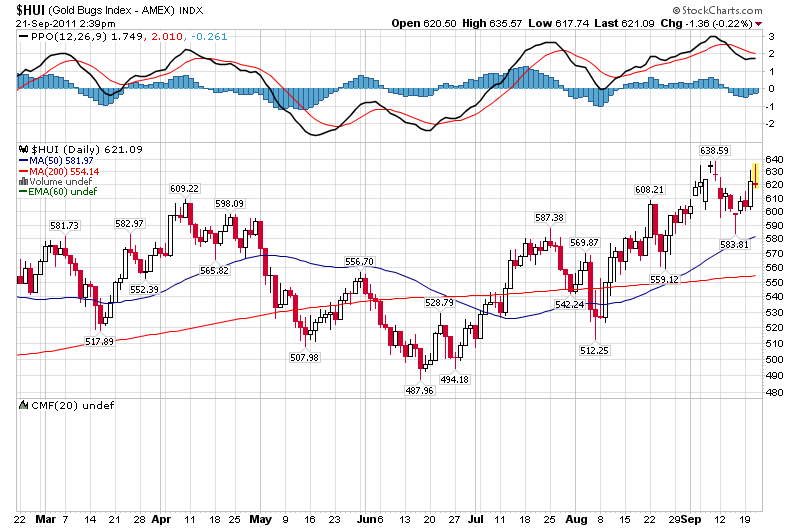

Gold bushwhacked the bears last week. It’s even got gold bugs talking about gold stocks … again.

After breaking gold bugs’ hearts by plunging to a new low for the year on Thursday, gold violently reversed. Measured by the CME floor close, the benchmark gold contract GCM2 -0.57% gained $38.30 on the day. It followed up on Friday by adding another $17, for a two-day gain of 3.31%.

The NYSE Arca Gold Bugs Index XX:HUI +0.21% jumped 5.29% in these two days.

Gold stocks’ outperforming the metal is significant, because they have been atrocious this year. As of Friday’s close, HUI was down 20.5% on the year, while gold was actually up 1.4% on the year. Just a restoration of late 2011’s multiples could produce serious gains.

If gold’s reversal sticks, it will be a triumph for the contrary opinion sentiment indicators. Nothing else had been offering any comfort.

The Hulbert Gold Newsletter Sentiment Index has been negative for a record 29 days. The far-sighted Australian bullion commentary The Privateer thinks something really significant has happened.

….read more HERE

It didn’t take long for Europe’s sovereign-debt crisis to reassert itself. Here we are in May, a short three months after the last bailout of Greece, and Europe is crumbling again.

Greece is on the ropes, and will most assuredly have to splinter away from the euro and take back its currency, the drachma. It’s the only way Greece can get out of its depression. Dump the euro, take back the drachma, devalue it, and inflate its way out of the mess and out of debt.

Portugal is reeling again, too. Spain is also going down the tubes. Depositors are making runs on the banks. Moody’s has downgraded virtually the entire Spanish banking system. Spain’s stock market is at 20-year lows.

It’s not much better in Italy, the most-indebted country in Europe. And France isn’t far behind. Now that the Socialists lead the country, you can expect France’s fiscal situation to worsen.

Meanwhile, the only economy holding Europe upright is also starting to slow. Germany’s giant export machine is wobbling, and so is its economy.

So it should be no surprise to you that stock markets are falling now. In order of weakness: Europe is the most-vulnerable, U.S. stocks are the second-weakest, and Asia’s equity markets are the least-weak of the three corners of the globe. Latin American markets will generally follow the U.S. markets.

But what about commodities? It’s certainly understandable that economic weakness would also take its toll on demand-sensitive commodities such as copper, foods, other base metals, and the like. After all, if economies are sinking anew, demand for these commodities is sure to fall.

And that’s precisely what I’ve predicted for the commodity sector. I was perhaps one of the only commodity bears out there for the past several months, but now my warnings are coming true. We’re seeing a sharp decline in most commodity prices.

The big question on most investors’ minds is why gold and silver are also falling. After all, when governments are on the verge of collapsing, shouldn’t that be bullish for gold and silver?

Under certain circumstances, yes. But not always. If the peripheral economies are collapsing, and their governments are under social attack, like what’s happening in Europe, then it’s not all that bullish for gold and silver. The core of the global economy, the U.S. and the U.S. dollar, can still suck up much of the frightened capital.

Again, that’s precisely what I warned, and precisely what’s happening. As scared capital flees Europe — it’s going primarily into cash, and into the U.S. dollar.

That’s pushing the U.S. dollar up, and taking the shine off of precious metals. Plus, always keep in mind that at the beginning of a crisis like we have now in Europe, investors want cash above all else. So gold is not the king right now. Cash is king.

That’s all going to change soon, because the world’s central banks despise runs to cash … they despise falling asset prices … and they absolutely abhor disinflation or, even worse, outright deflation.

So that means that central banks are soon going to start printing massive amounts of money again, flooding the global economy with trillions of additional dollars.

And when they do, you could just as easily see gold and silver bottom out and begin the next legs up in their bull markets.

I believe that’s not too far away. But it’s likely we will see further declines first. My models tell me that we are not yet at asset price levels that would send central banks into panic mode, forcing them to put the pedal to the metal with their money printing.

Here’s what my models are telling me. Look for further declines ahead …

- Down to below $1,440 in gold

- Down to below $26 in silver, to as low as $21

- Down to below $85 in oil

- Down to below 12,000 in the Dow Industrials

And mark my words: When the commodity markets do bottom out and central banks start printing money again — it will represent the beginning of the biggest phase yet in the commodity bull markets.

So get ready, because it’s right around the corner.

Best wishes, as always …

Larry

Larry Edelson has nearly 33 years of investing experience with a focus in the precious metals and natural resources markets. His Real Wealth Report (a monthly publication) and Resource Windfall Trader (weekly) provide a continuing education on natural resource investments, with recommendations aiming for both profit and risk management.

For more information on Real Wealth Report, click here.

For more information on Resource Windfall Trader, click here.

Mark Spitznagel: The Austrians And The Swan – Birds Of A Different Feather

On Induction: If it looks like a swan, swims like a swan…

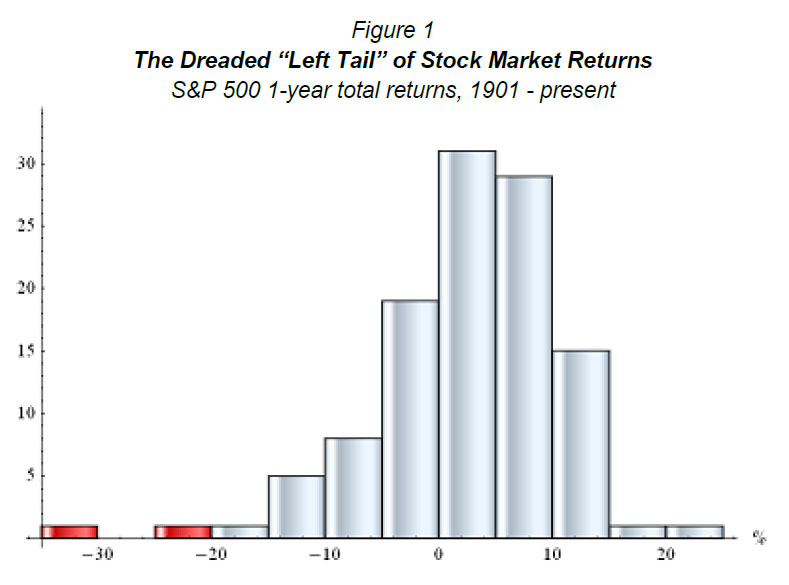

By now, everyone knows what a tail is. The concept has become rather ubiquitous, even to many for whom tails were considered inconsequential just over a few years ago. But do we really know one when we see one?

To review, a tail event—or, as it has come to be known, a black swan event—is an extreme event that happens with extreme infrequency (or, better yet, has never yet happened at all). The word “tail” refers to the outermost and relatively thin tail-like appendage of a frequency distribution (or probability density function). Stock market returns offer perhaps the best example:

\

\

What is a black swan event, or tail event, in the stock market?

It depends on who’s asking.

To those familiar with Austrian capital theory, the impending U.S. stock market plunge (of even well

over 40%)—like pretty much all that came before in the past century—will certainly not be a Black

Swan, nor even a tail event.

Nonetheless, the black swan notion is paramount—in perception: Market participants’ failure to

expect a perfectly expected event—that is, they price in only Anglo swans despite the Viennese bird

lurking conspicuously in the weeds—much like what is happening today, brings tremendous

opportunity.

….read the entire analysis including charts HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair