Stocks & Equities

I TAKE my hat off to the global central planners for averting the next stage of the unfolding financial crisis for as long as they have, writes Chris Martenson.

I guess there’s some solace in having had a nice break between the events of 2008/09 and today, which afforded us all the opportunity to attend to our various preparations and enjoy our lives.

Alas, all good things come to an end, and a crisis rooted in ‘too much debt’ with a nice undercurrent of ‘persistently high and rising energy costs’ was never going to be solved by providing cheap liquidity to the largest and most reckless financial institutions. And it has not.

The same sorts of signals that we had in 2008 are once again traipsing across my market monitors. Not precisely the same, of course, but with enough similarities that they rhyme loudly. Whereas in 2008 we saw breakdowns in the credit spreads of major financial institutions, this time we are seeing the same dynamic in the sovereign debt of the weaker European nation states.

Greece, as expected, is a right proper mess and will have to leave the Euro if it is to have any chance at recovery going forward. Yes, all those endless meetings and rumors and final agreements painfully hammered out by Eurocrats over the past year are almost certainly going to be tossed, and additional losses are going to be foisted upon the hapless holders of Greek debt. My prediction is that within a year Greece will be back on the Drachma, perhaps by the end of this year (2012).

Greek default specter turns material

The weekend Greek revolt against the austerity measures imposed on its economy in return for Eurozone funding has elevated the prospect of a Greek default on its debts or a chaotic exit from the Eurozone.

The collapse in support for the mainstream parties that had reluctantly accepted the austerity program and the vehement opposition to the measures by the radical left party that finished the runner up in the weekend’s elections has made it almost impossible for a coalition to be formed that would persevere with the program.

It is likely new elections will have to be held next month but given the degree to which Greeks have protested against the harsh Eurozone prescriptions – and the 20 per cent shrinkage in GDP and 20 per cent-plus unemployment that has accompanied them – it is improbable that Greece will continue with the reforms it agreed in return for the next $300 billion tranche of Eurozone funding.

If it does walk away from that commitment there will be chaos in Greece and, to a lesser extent, elsewhere. Greece would inevitably default on its debts and could be forced to quit the Eurozone.

(Source)

There really is no choice for Greece but to leave the Euro, and the sooner, the better. Even then, there is a lot of hardship coming their way. But in my estimation, that’s better than the imposed austerity that is a guaranteed torture chamber. The institutions that avoided taking losses on their Greek debt on the first pass through, due to their preferred status in the process (the ECB among them), are almost certainly going to eat big losses this time, perhaps a full 100% of them.

Leaving the Euro is going to be quite a process, and the ripple effects are going to be large and somewhat unpredictable. I found this description of what will happen within Greece and its banking system to be well on the mark:

The instant before Greece exits it (somehow) introduces a new currency (the New Drachma or ND, say). Assume for simplicity that at the moment of its introduction the exchange rate between the ND and the Euro is 1 for 1. This currency then immediately depreciates sharply vis-à-vis the Euro(by 40 percent seems a reasonable point estimate). All pre-existing financial instruments and contracts under Greek law are redenominated into ND at the 1 for 1 exchange rate.

What this means is that, as soon as the possibility of a Greek exit becomes known, there will be a bank run in Greece and denial of further funding to any and all entities, private or public, through instruments and contracts under Greek law. Holders of existing Euro-denominated contracts under Greek law want to avoid their conversion into ND and the subsequent sharp depreciation of the ND. The Greek banking system would be destroyed even before Greece had left the Euro area.

There would remain many contracts and financial instruments involving Greek private and public entities denominated in Euro (or other currencies, like the US Dollar) that are not under Greek law. […] Widespread defaults seem certain.

Euro area membership is a two-sided commitment. If Greece fails to keep that commitment and exits, the remaining members also and equally fail to keep their commitment. This is not just a morality tale. It has highly practical implications. When Greece can exit, any country can exit.

As soon as Greece has exited, we expect the markets will focus on the country or countries most likely to exit next from the Euro area. Any non-captive/financially sophisticated owner of a deposit account in that country (or in those countries) will withdraw his deposits from banks in countries deemed at risk – even a small risk – of exit.

Any non-captive depositor who fears a non-zero risk of the future introduction of a New Escudo, a New Punt, a New Peseta or a New Lira (to name but the most obvious candidates) would withdraw his deposits from the countries involved at the drop of a hat and deposit them in the handful of countries likely to remain in the Euro area no matter what – Germany, Luxembourg, the Netherlands, Austria and Finland.

The ‘broad periphery’ and ‘soft core’ countries deemed at any risk of exit could of course start issuing deposits under English or New York law in an attempt to stop a deposit run, but even that might not be sufficient. Who wants to have their deposit tied up in litigation for months or years?

(Source)

The Greek banking system will be destroyed immediately upon Greece’s exit from the Euro, but the banking system there is already all but dead anyway. Best just to sweep the floor clean and start over. The idea is easy enough to understand; if your bank is about to go under, it is best to get your money out before that happens.

The only mystery to me is why so many people have left their money in the Greek banks this long. I suppose they were waiting for a clearer signal? Well, it would seem that the signal has now been sent and received:

Greek Depositors Withdrew $898 Million From Banks Monday

Greek depositors withdrew €700 million ($898 million) from the country’s banks on Monday, fueling fears of a bank run amid the growing political disarray.

With deposits falling, Greek banks become even more dependent on the European Central Bank to meet their funding needs, exposing the central bank to potentially huge losses if Greece leaves the Euro area.

Monday’s deposit withdrawal far outpaced Greek banks’ steady decline in deposits since the start of the country’s debt crisis in 2009, as depositors withdraw cash and transfer funds overseas. In the past two years, deposit outflows have generally averaged between €2 billion and €3 billion a month, though in January they topped €5 billion.

The latest data from the Greece’s central bank show that total deposits held by domestic residents and companies stood at €165.36 billion in March.

(Source)

Again, the real mystery to me is who still has 165 billion Euros in Greek banks at this stage of the game? Also a mystery is why Greece has not yet imposed a withdrawal moratorium and capital controls? It is only a matter of time, perhaps days, before they do.

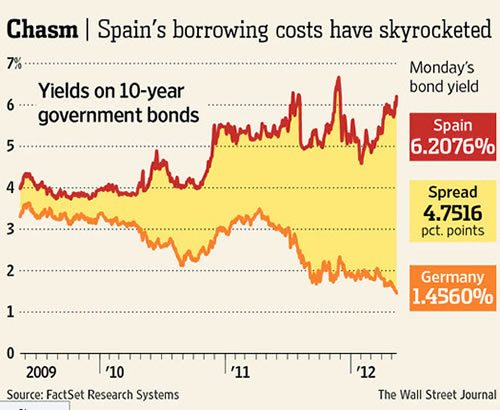

Of course, it is the contagion effect that most worries the market, because the same dynamic of utter insolvency leading to the intractable nature of Greece’s dilemma applies to Spain, Portugal, and Italy.

Indeed, the market is already adjusting to this possibility, as evidenced by the spikes in the yields of those country’s bonds:

Contagion Fears Hit Markets

LONDON – Investors battered European stocks, dumped the bonds of Spain and Italy, and bid the Euro down against the Dollar Monday after the collapse of weekend coalition talks in Greece edged that country closer to an exit from the Euro zone.

The sweeping market action dealt a blow to hopes that the damage of a Greek exit, should it occur, could be comfortably contained.

In the market carnage, Greek stocks fell to two-decade lows, and Spanish bond yields leapt to levels not seen since the panic of last November. Shares of a big Spanish lender dropped 8.9% on the Madrid bourse, pulling the benchmark index down 2.7%. The Italian market also fell 2.7%, and the Euro slid to $1.2845 late Monday in London, its lowest level in four months.

The worry and the carnage are both running deep. And they should. Everything is now interlinked to such a degree that there is no possible way for a run on Greek banks or continued declines in the value of sovereign debt to be anything other than exceptionally destructive.

Everybody owes everybody, and there’s not enough productive economy to mask the insolvency of the system any longer.

We saw this as Spain’s sovereign yields vaulted, Spanish bank shares plunged, a not-so-happy linkage courtesy of the LTRO funding which enabled (and encouraged) Spanish banks to load up on Spanish debt. A virtuous circle morphed into a vicious spiral, each element weakening the other all the way down.

That the US stock market is only down less than 5% from recent highs is a testament to the power of the liquidity that the Fed and US banking system have directed at keeping things elevated. However, this cannot last, at least not without another big quantitative-easing (QE) injection from the Fed. Without such an infusion, I am calling for another 2008-2009-style market rout of at least -30% but possibly as much as -50%.

The reason we need another QE injection is that the same dynamic of debt destruction is again stalking the markets. As expected, the Fed has been waiting for a clear signal that it is time for more thin-air money, and again they are going to wait too long to prevent more damage from occurring.

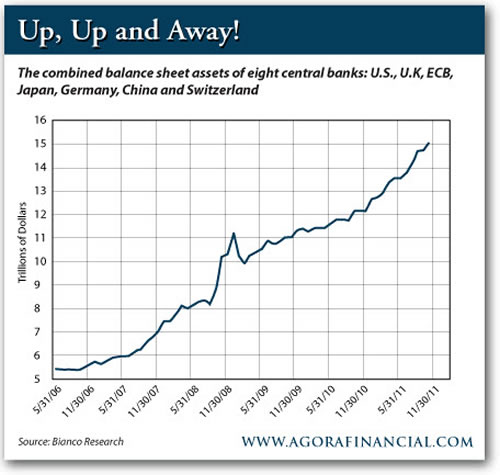

This time I am expecting a coordinated central bank action that will involve most or all of the major central banks of the OECD: Japan, UK, US, and Europe.

One day, we will wake up to find some global message about the need for a coordinated response to a major crisis, and each of the central banks will be issuing some massive new amount of thin-air money. Of course the programs will be called something fancy that will require shortening to an acronym and will involve buying some form of debt (sovereign debt, but maybe also bank debt), and we’ll track this via central-bank balance-sheet expansion.

Perhaps we’ll see this line go up a little steeper, or perhaps the same trajectory will be maintained a little longer:

Regardless, more printing is on the way, because the alternative is the utter collapse of the entire Western banking system. And quite probably a few governments, too.

To me, that is an unthinkable outcome, and one that I have every faith will be avoided at any every cost. It is the main reason that I am quite content to hold onto all of my gold at this juncture. Anybody selling physical gold here is either broke (and needs the money) or is just not paying attention.

To drive the point home, consider this picture posted on Zerohedge taken from German television purportedly showing the Ministry of Finance in Athens. A picture is worth a thousand words:

(Source)

By the time the Ministry of Finance is storing records in garbage bags and shopping carts, perhaps, just maybe, one might become a little concerned about loaning money to the Greek government. One hopes.

Greece, of course, is tiny compared to Spain or Italy. The situation in Spain – which is big enough to matter – is truly dire, very large, and getting worse.

Spain has been playing fast and loose with the numbers, and that fact has now been revealed to the world. It’s not a pretty picture.

Spain Underplaying Bank Losses Faces Ireland Fate

May 10, 2012

Spain is underestimating potential losses by its banks, ignoring the cost of souring residential mortgages, as it seeks to avoid an international rescue like the one Ireland needed to shore up its financial system.

The government has asked lenders to increase provisions for bad debt by 54 billion Euros ($70 billion) to 166 billion Euros. That’s enough to cover losses of about 50 percent on loans to property developers and construction firms, according to the Bank of Spain. There wouldn’t be anything left for defaults on more than 1.4 trillion Euros of home loans and corporate debt.

Taking those into account, banks would need to increase provisions by as much as five times what the government says, or 270 billion Euros, according to estimates by the Centre for European Policy Studies, a Brussels-based research group. Plugging that hole would increase Spain’s public debt by almost 50 percent or force it to seek a bailout, following in the footsteps of Ireland, Greece and Portugal.

“How can you only talk about one type of real estate lending when more and more loans are going bad everywhere in the economy?” said Patrick Lee, a London-based analyst covering Spanish banks for Royal Bank of Canada. “Ireland managed to turn its situation around after recognizing losses much more aggressively and thus needed a bailout. I don’t see how Spain can do it without outside support.”

(Source)

And this is just the losses that Spanish banks face on their real-estate portfolios. They are also now facing losses on all the Spanish sovereign debt that they bought with their LTRO funding as well. Very simply, Spain now needs a massive rescue, and soon.

Meanwhile German citizens are all done with helping their southern neighbors. Merkel has used up all of her political capital on the rescues performed to date, and it is far from clear that any more help is politically doable here. The only way that I can see such help coming is under some terms other than drawing upon the savings of Germany’s citizens. Printing, perhaps, but even that is a dicey political proposition here.

If Spain drops here, then you can just set an egg timer for when Italy will go. And then France. The dominoes will rapidly fall from there.

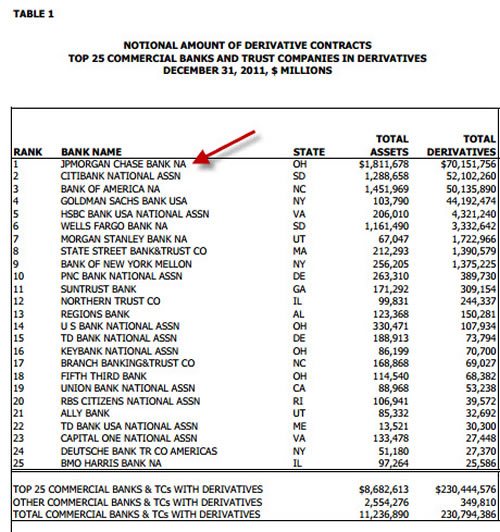

In describing JPMorgan’s recent $2 billion (or is it $20 billion…or more?) trading losses and Jamie Dimon’s (the CEO of JPM) awkward explanation of how certain hedging operations went wrong, the author of this next piece asks the obvious question:

Does Jamie Dimon Even Know What Hedging Risk Is?

But wait a minute? If you’re hedging risk then the bets you make will be cancelled against your existing balance sheet. In other words, if your hedges turn out to be worthless then your initial portfolio should have gained, and if your initial portfolio falls, then your hedges will activate, limiting your losses. That is how hedging risk works. If the loss on your hedges is not being cancelled-out by gains in your initial portfolio then by definition you are not hedging risk. You are speculating.

(Source)

We still don’t know the exact dimensions of JPM’s losses here (my expectation is that more bad news will follow soon enough), but we can be sure that the big banks have not learned from the mistakes of the past and are still engaged in risky practices involving derivatives.

Whatever JPM was up to (and I am still not entirely clear on what that was), it was not classic hedging, which serves to minimize losses, but something far more speculative.

The reason this gives me such cause for concern is that it once again exposes a small portion of the derivative monster that will certainly be awakened when the European situation goes into full meltdown over the Greek, then Spanish, the Portuguese, then Italian situations.

While derivatives are, in theory, a zero-sum game, and therefore could, in theory, be forgiven and forgotten in a pinch, the reality is that they’ve been used to pretend that risk did not exist and therefore losses don’t exist.

The ugly truth here is that we are at the tail end of a most unfortunate credit bubble – four decades of global excess by the OECD countries – and there are massive losses to account for. Just as the offsetting counterparties involved in the subprime CDO and CDS mortgage crisis did not zero out because the losses they were allegedly papering over were all too real, the same will prove true of the derivative paper allegedly covering sovereign and corporate debts.

Remember, the biggest holder of derivatives is the company that just demonstrated that it doesn’t really understand the concept of hedging.

Overall derivatives, especially interest-rate-linked derivatives, have increased by over $100 trillion since the crisis began. As JPM just evidenced, and as hinted at by the interminable hand-wringing over allowing Greece’s paltry $78 billion in credit-default swaps to be triggered, real dangers lurk here.

I wish I could analyze the situation better than the rest of the crowd that either screams catastrophe looms or coos that everything is safe, but I cannot. The situation is too opaque, too convoluted, and too complex to tease apart. I simply don’t know what the true nature of the risk really is – and the truth is, nobody really does. You might as well ask these analysts to tell you the exact size and shape of the first ten waves that will hit Laguna Beach exactly one year from now beginning at 12:05 p.m.

Instead, what I can offer to you is the idea that instead of reducing (let alone eliminating) risk, all that derivatives have done is mask risk. This means that whatever losses are resident in a system with four decades of debt-fueled malinvestment and overconsumption are still there just waiting to be realized.

It is this certainty that the losses remain, the risk is masked, and the bets have only grown larger that makes me very nervous these days as I contemplate the possible implications and repercussions of a Greek exit from the Euro.

Given this environment of massive, rapidly-accelerating, and obfuscated risks, the prudent among us are undoubtedly wondering, How the heck is this going to play out? And how do I prepare for it?

I expect central banks will once again attempt to ride to the rescue with gargantuan liquidity measures. But this next time won’t work as it did in 2008, in my estimation. I see central banks being near the end of their ability to influence developments at this point. More liquidity will affect different asset classes differently, and for the first time raise real (and valid) concerns about the widescale debasement we are witnessing across the world’s major fiat currencies.

Putting your capital into those resources best positioned to appreciate most as the result of money printing and hold or increase their purchasing power in such an environment should be a top priority for every concerned investor.

Get the safest gold at the lowest prices – with access to 24/7 live gold and silver trading – on BullionVault…

Chris Martenson, 18 May ’12

Unlocking the Crude Oil Bottleneck at Cushing

The U.S. oil infrastructure is the product of four decades of rising imports and falling domestic supply. As those trends have reversed over the last few years, America’s network of pipelines has failed to keep pace. Designed in part to ferry oil and refined gasoline from the coasts to the interior, those pipelines are now ill-equipped to handle the enormous amount of crude gushing from shale reserves in North Dakota and Texas. Which is why so much of that oil ends up trapped in the central Oklahoma town of Cushing, the primary crude oil storage hub for the U.S. Cushing developed as an oil trading center and then as the official price settlement point for West Texas Intermediate, the benchmark that most types of North American crude are priced against. Cushing is now best known as a bottleneck for the energy industry: Oil rushes in, but trickles out. There are now more than 44 million barrels of oil stuck in Cushing, a record, and 60 percent more than was stored there just five months ago. Overall U.S. crude inventories now sit at a 21-year high. Pipeline companies are racing to build new projects aimed at pushing more oil through Cushing toward refineries as part of a larger effort to revamp America’s oil infrastructure. The first of those projects goes online this week when the flow of the 500-mile Seaway pipeline is reversed. Seaway, with a diameter of 30 inches, was built in 1976 to take crude south from the Texas Gulf Coast north into Cushing. On May 17, about 150,000 barrels of oil will be injected into Seaway at Cushing. Twelve days later, that oil will start arriving in Freeport, Tex., along the Gulf Coast, where refiners can access it. As the pump stations provide more horsepower and increase the pipe’s pressure later this year, the oil will travel faster, taking just five days to reach Freeport and increasing Seaway’s capacity to 400,000 barrels per day by early 2013. By mid-2014, that flow is expected to reach 850,000 barrels a day.

The United States, meanwhile, becomes a recipient of global capital flows when uncertainty shadows over developed‐nations’ capital markets and emerging market growth prospects.

So, from an equities perspective the US has outperformed global stock markets; and from a global growth perspective commodities have been beaten down.

From here, if you believe global growth will remain subdued and other fundamental risks will hurt economies and markets throughout the world, it’s tempting to expect US stocks will play catch‐up and move lower with global equities and commodities. After all, the Federal Reserve hasn’t brought new quantitative easing to the table and likely won’t for some time.

But it may be a bit premature to expect US equities will plunge. Likewise, this downturn in commodities may be getting a bit long in the tooth.

Crude oil is falling… copper is falling… stocks are falling. Because of the European debt crisis, people are fleeing assets that are sensitive to economic growth… and flocking to “safe havens” like bonds and the U.S. dollar (cash). As you can see in the chart, the dollar is currently winning the world’s “least ugly” paper currency contest. It’s gained around 9% from its August lows. This doesn’t sound like much to most people, but it’s actually a huge gain for a major currency.

Of course, as the dollar rises, gold falls. The yellow metal traded for $1,750 an ounce in February. It’s now trading for $1,530. That’s a decline of 12.5% in three months.

On the surface, gold is falling because people are dumping assets to raise cash. Gold is a liquid asset, just like stocks and crude oil. So it gets thrown overboard when people are desperate for liquidity. But the “big picture” reason gold is experiencing a decline is that it’s simply “due” for a substantial period of sideways (or lower) prices. Gold has risen in price every single year for the past 11 years. No other widely traded asset or index can match that record of consistent gains. Gold is up more than six-fold during this relentless, relatively calm bull market.

With this amazing, once-in-a-century bull market in mind, we remind you that markets are like runners. They can’t run flat-out for miles without a break. The long-term picture for gold hasn’t changed. Western governments still have massive, unfunded debts and obligations that cannot be paid with sound, honest money. The people of Asia (especially China and India) are getting a little richer every year. These people have a centuries-old affinity for precious metals, like gold and silver… and they are still buying. Again, gold is simply due for a break.

To put its recent decline into perspective, let’s look at the “long view.” Below is a 12-year chart of gold. As you can see, gold could fall all the way down to $1,300 an ounce and remain in a bull market. That’s where it was in late 2010. In the context of gold’s massive bull market, even the latest decline isn’t severe…

Another bit of perspective: Rich, sophisticated investors don’t view gold as a conventional investment. It’s not like owning an income-producing rental property. It’s not like owning shares in a dividend-paying, blue-chip company like Coca-Cola. Gold is real money. It’s a form of “crisis insurance.” Rich people buy gold and hope they never have to use it. They don’t buy it with the hope that they’ll make hundreds of percent on their holdings. You can read more about the “rich guy” way to view gold in this short interview.

Speaking of rich people and what they buy…

This morning, the news services are reporting on the latest moves by billionaire investor Warren Buffett. His company, Berkshire Hathaway, has just filed reports with the Securities and Exchange Commission showing it has new stakes in automaker General Motors and media company Viacom. Buffett also increased his stake in global discount retailer Wal-Mart – one of Dan Ferris’ favorite World Dominating Dividend Growers. Buffett recently said he doesn’t think the Mexico bribery scandal will harm the company’s long-term earnings power. Dan agrees. He sees the recent selloff as a good buying opportunity.

Following the investments of legends like Buffett is a great way to find potential low-risk, high-reward ideas. The world’s best investors and traders have massive research budgets. They have the best contacts. They have the best computers and the most extensive databases. They’re able to achieve a tremendous “information edge” in the market. That’s why looking over their shoulders makes sense.

Over the past few days, we’ve told you a few details about our newest service, DailyWealth Trader. We have several goals with DailyWealth Trader. The main goal is to educate readers on the best ways to make low-risk, high-reward trades. The service also acts as a “digest” of ideas from the world’s best investors and traders.

For example, in the May 1 issue (which was made available only to Alliance memebers), we discussed one of the top ideas from legendary trader Jim Chanos. As one of the world’s best short sellers, Chanos makes money by betting on a company’s stock price falling. We highlighted his short position in Brazilian oil producer Petrobras. Chanos says the company is the picture of how government mismanagement wrecks companies. It’s also spending hundreds of billions of dollars to develop high-cost offshore oilfields. Chanos is bearish…

As you can see from the chart below, shorting Petrobras was a heck of an idea. The stock has collapsed from $30 per share to less than $20 per share in just a few months. As of yesterday’s close, that trade is up 17.5% in just two weeks.

Again, with a subscription to DailyWealth Trader, you’ll receive ideas from the world’s best investors and traders. You’ll also receive a priceless education on how to act on those ideas. If you’re new to trading… or interested in furthering your market education, you’ll get tremendous insights from DailyWealth Trader… at a very low price. You can sign up for our upcoming educational video and receive information on a trading technique we normally charge at least $1,000 to teach here.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair