Bonds & Interest Rates

Written by David Einhorn via huffingtonpost.com

A Jelly Donut is a yummy mid-afternoon energy boost.

Two Jelly Donuts are an indulgent breakfast.

Three Jelly Donuts may induce a tummy ache.

Six Jelly Donuts — that’s an eating disorder.

Twelve Jelly Donuts is fraternity pledge hazing.

My point is that you can have too much of a good thing and overdoses are destructive. Chairman Bernanke is presently force-feeding us what seems like the 36th Jelly Donut of easy money and wondering why it isn’t giving us energy or making us feel better. Instead of a robust recovery, the economy continues to be sluggish. Last year, when asked why his measures weren’t working, he suggested it was “bad luck.”

I don’t think luck has anything to do with it. The blame lies in his misunderstanding of human nature. The textbooks presume that easier money will always result in a stronger economy, but that’s a bad assumption. Here is a good example of how a real family responds to monetary policy.

Consider my neighbors, Homer, Marge, and their three adult children, Bart, Lisa and Maggie. Homer has retired from the nuclear plant, and he and Marge live off savings and Homer’s pension. Bart is in a bit of trouble with too much credit card debt and an underwater mortgage. Lisa has been putting away her salary and has enough for a downpayment on her first home. Maggie owns her own business and is ready to expand.

When interest rates are high, Homer and Marge park their savings in CDs or Money Market accounts and get a decent return. There is no incentive for them to take much risk with their money. Bart gets into trouble very quickly and defaults on his loans. Lisa decides she can’t afford a mortgage until rates fall. And Maggie, who’s been helping out Bart with some of his expenses, believes that she’d make money if she grew the business, but possibly not enough to service the debt she’d be undertaking.

When interest rates are low, everything changes. Homer and Marge are getting only a little interest on their savings, and are struggling to live off Homer’s pension. They need to rethink their finances. Bart can manage to keep up the minimum payments on his credit cards and stay in his house. Lisa can get a cheap mortgage, and Maggie doesn’t need to make such optimistic assumptions in order to expand her business.

Everyone agrees that low interest rates are a good way to stimulate a stalled economy. The Fed takes this logic a step further. It believes that if low interest rates are good, then zero-interest rates must be even better. As a brief emergency measure, such drastic behavior is reasonable and can even be necessary. In 2008, Chairman Bernanke had near unanimous support for his decision to drop rates to near zero. At the peak of the crisis, it made sense. But that was four long years and many jelly donuts ago. In the 2012 economy, a zero rate policy not only adds no benefit, it’s actually harmful. Just ask the Simpsons.

When Homer was approaching 65, he and Marge met with a financial planner to figure out if they had enough money saved for retirement. They assumed they’d live to be 90, and could count on receiving a fixed amount from Homer’s pension and social security checks. Marge, the cautious one, has not forgotten that stock market meltdown better known as the bursting of the tech bubble. She didn’t want to take any investment risk and was content to have just enough for regular haircuts for herself, a bowling and beer budget for Homer, and visits with the children. They were told that, with nominal interest rates at 3%, they could safely retire with $200,000.

“What happens if interest rates go to zero and stay there?” Marge asked the advisor.

“You mean indefinitely? If you weren’t willing to start taking investment risk, you’d need 50% more in savings, or $300,000. But why would you ask such a silly question?” asked the advisor.

To which Marge replied, “Well, we were thinking about moving to Japan…”

Homer and Marge aren’t the only ones doing this sort of math. Every single day for the next 19 years, more than 10,000 Baby Boomers will turn 65. Those who started saving for retirement 15 years ago are suddenly finding themselves with insufficient savings to do so.

Some will stay in the work force longer, some will drastically reduce their spending, and some will do both. In a recent survey, 20% of U.S. workers say they have postponed their planned retirement age at least once during the last year. And those who have already retired have fewer options. Returning to the workforce could be challenging. David Rosenberg points out that the workforce for those 55 and older has expanded by 4 million since the start of the recession, and they are returning to the workforce at lower wages. Even more challenging is trying to find safe investments that generate a decent yield.

To Read More CLICK HERE

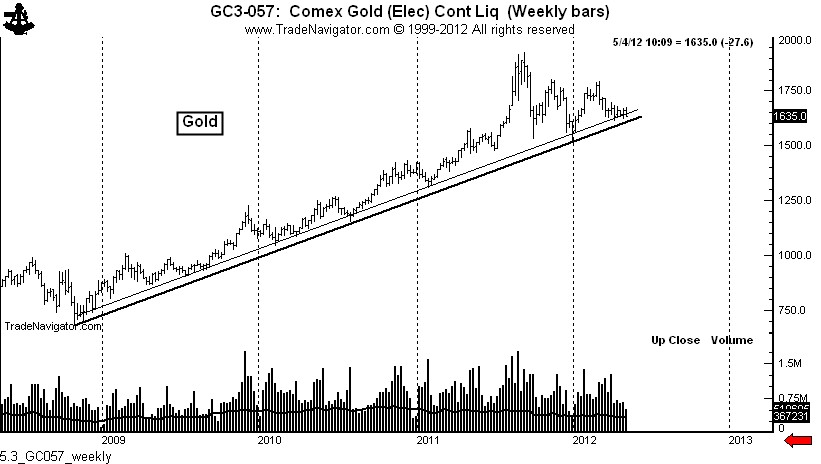

On April 24 I posted a blog stating that Gold was within a week or so of declaring its next $250 move. See here.

The Gold market worked higher for about a week after the post above, reaching a high of $1,672 on May 1 (a day that became a one-day minor reversal).

Has the $250 move in Gold begun? I am not sure — but I am sure that Gold is right at the edge of the cliff hanging on by its finger nails.

The weekly chart below of Gold shows the major trendline from the 2008 low under the orthodox lows (thick line) and through the week-end closes (thin line).

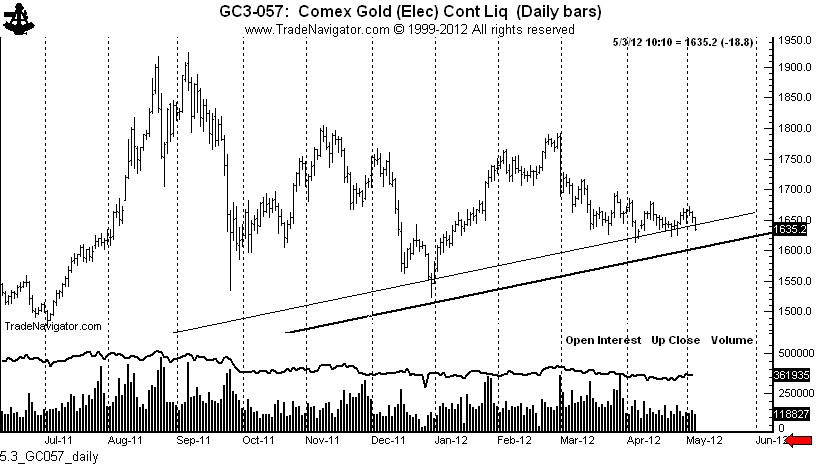

The next chart is a blow up of the previous graph — showing the two key trendlines superimposed on a daily chart.

I need to openly declare that I want to be a bull in Gold — yet I am not presently long. I accept the conventional wisdom bull story in Gold — even though I know that conventional wisdom is usually wrong.

Yet, as the daily chart shows, Gold needs to make a stand at present levels. A move below the April low at $1613 (especially if it’s on Friday) would not be good news for the bulls. Of course there is always the chance the market will spring an historic bear trap by taking out all the stops beneath the April low and immediately turning higher. But, fortunately, bear and bull traps quickly reveal themselves and provide excellent opportunities to get right with the market. Yet, as a chartist, I would have to respect a decisive violation of the trendlines just below the market.

To Read More CLICK HERE

Munch’s “The Scream” may be all the rage today, but to Jim Grant, in his latest interview on Bloomberg TV, the record price paid for the painting is not so much a manifestation of modern art as one of modern currency: “This is the flight into things from paper” . Thus begins the latest polemic by the Grant’s Interest Rate Observer author whose topic is as so often happens, the Federal Reserve (for his latest definitive expostulation on why the Fed should be disbanded and why a gold standard should return, delivered from the heart of Liberty 33 itself, read here). The world in which we invest is a world of immense wall to wall manipulations by our friends in Washington. And people get off on Goldman Sachs because it has done this and this, it is pulling wires… The Federal Reserve is the giant squid of squids, it is the vampire squid of vampire squids.”

He continues: “They – the vampire squids – have manipulated virtually every single price and valuation in the capital markets. People ought to recognize when they invest that one of the unspoken risks is the risk that this hall of mirrors, this Barnum and Bailey world that the Fed has created for us is going to vanish one day because they will not be able to hold it any more… It’s not as if there is nothing to do in investing, but one must always keep in mind that the valuations that we see, that the prices that we watch flicker across the tape are prices that are fundamentally manipulated by these well-intended, dangerous people in Washington called the Federal Reserve“. And to think that 3 short years ago Grant would have been branded a loony, tin-foil hat wearing gold bug, while now it has become trendy for hedge fund managers to bash the Fed with impunity. It is all downhill from here.

To Watch the Video CLICK HERE

It was Bob Prechter of Elliott Wave fame, likely among others who noted that correlations between all asset classes are quite strong during a Depression. This is true in a cyclical sense but not in a structural sense. Stocks tumbled in the 1929-1941 period while commodities, led by Gold and gold producers, increased in value. We’ve experienced similar phenomena in the past 12 years. Cyclically, there has been a correlation between these asset classes. Structurally, stocks have been in a bear market and resource sector has been in a bull market. The driving force has been a weak economy and bear market which usually leads to more inflationary policy, which in turn benefits the resource sector. Are we soon to see a replay of this scenario?

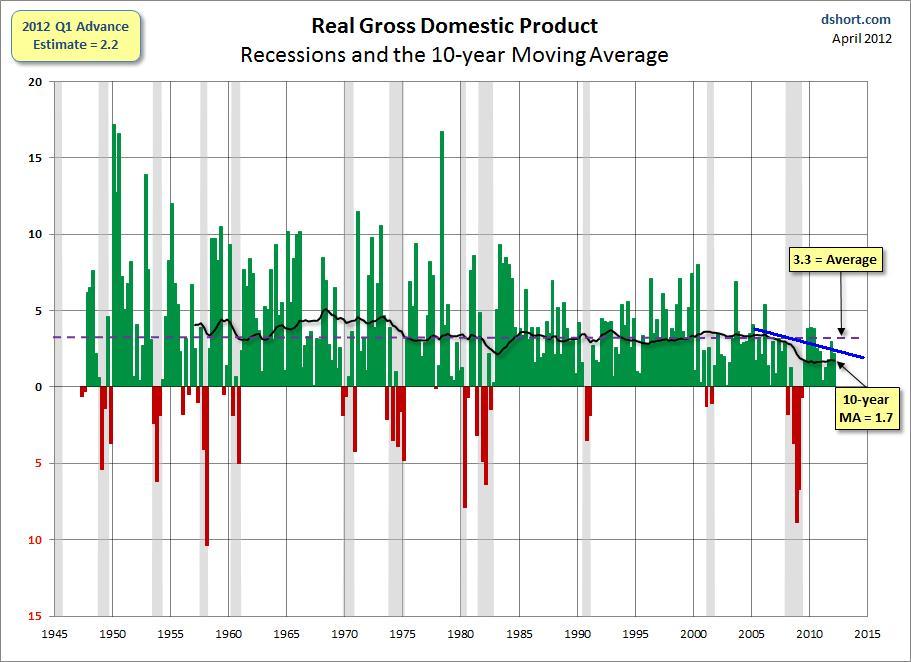

Despite unprecedented monetary inflation, stimulus and bailouts, the economy has barely recovered. The chart below (from Doug Short) displays post-war real gdp growth. The black line shows the 10-year average which has been in a steep decline since 2006. At the time, the Bush II recovery was the weakest on record. It has been surpassed by a pathetically weak recovery (statistically) under Obama. The growth rate in each of the past seven quarters has been below the the 10-year moving average.

Meanwhile, economic data as a whole is okay but is currently failing to meet expectations. The Citigroup Economic Surprise Index, (economic data relative to expectations) has gone negative for the US, and the rest of the world is not far behind. Clearly, continued disappointing economic data combined with any weakness in equities would prompt more Fed action. Judging from what happened in 2010 and 2011, it is a near certainty.

To Read More CLICK HERE

“Instead of looking for opportunities to invest in real products, Wall Street awaits the minutes of each Federal Open Market Committee meeting with bated breath, hoping that QE3 and QE4 are just around the corner.”

– Ron Paul

There have been bouts of risk aversion over the last few years – some sustained, most not; but all unquestionably due.

We understand that the final arbiter is price, regardless of what the fundamentals suggest about an investment or underlying economy. But it’s hard to maintain such necessary agnosticism when the news is so consistently bad.

And therein lays the problem – consistency.

One might instead use the term “mindless recitation,” but the steady — consistent — dose of ‘bad’ has rarely spooked investors (those still playing, anyway). Sure, a confluence of ‘bad’ has served to ruffle feathers periodically, but, ultimately, the markets continue chugging along because we always know ‘just how bad’ or ‘just how good.’ For as long as everyone knows what’s going on, the cause for worry is diminished. Why? Because investors rationalize their above average, selective stock-picking ability and fabricate a false sense of security (trading bias) which, in a self-reinforcing sort of way, creates the apparent absence of uncertainty.

Bringing the black swan concept into this, analysts have sought to uncover potential risks that would bring on massive shocks to the markets; it’s become a well-tred path to popularity and influence in the investment world since 2008. But, by definition, predicting a black swan event is impossible.

As we move further and further away from the credit crisis of 2008, and as we are further desensitized to the words ‘bad’ and ‘worse’ by government and central bank officials’ action, investors seek out risky investments because they have not found a black swan (and, because of the low interest rate background, nothing else pays.)

To Read More CLICK HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair